|

A reasonably quiet week with the main piece of exciting news within the portfolio being that from KWS shown below. What a chunky addition that is for KWS and thankfully the market seems to love it. KWS is now up by a factor of 4x since my original purchases about 18 months ago. This will never do, I like boring, boring stocks and maybe KWS is just too exciting: oh well, such is life. Returning to the truly boring stuff, quite a few chunky ex-dividends dates have kicked in this week and pleasingly the portfolio has held up very well prior to the eventual arrival of the dividend payments and subsequent reinvestment. Note: historically I always reinvest dividends usually, but not exclusively, in the parent company and if not in the parent company then something showing positive momentum within the portfolio. Over time the contribution of reinvested dividends is simply incredibly significant in terms of total stock market returns.

Maybe this relatively quiet week and the drawing to the end of civilised temperatures as we reach the end of October has brought my hibernation tendencies out: I was probably a grizzly bear in a previous life! Anyway, that seems a reasonable excuse for me sleeping in this morning; I did not wake until 06:35 and by that time I would normally be ploughing through the water. Looks like I will be a grumpy bear with a sore head today. Enough of this and on to this week’s RNS stories for shares within the portfolio: Monday 23/10/2017: No RNSs directly relevant to stocks within the portfolio. Tuesday 24/10/2017: Keyword Studios: KWS: Market Cap: £798m: Two RNSs, firstly one relating to the proposed acquisition of VMC & secondly one relating to a placing to fund that proposed acquisition: The Acquisition: A major acquisition in North America; significantly earnings enhancing Keywords Studios plc, the international technical services provider to the global video games industry, is pleased to announce that it has entered into a conditional agreement to acquire the entire issued share capital of VMC Consulting Corporation and Volt Canada Inc. (collectively, "VMC"), a leading provider of video game Functional Testing and Customer Support in North America (the "Acquisition"), from Volt Information Sciences, Inc. ("Volt") for a cash consideration of approximately USD $66.4 million, subject to certain working capital adjustments. The Consideration and working capital adjustments and related transaction costs are intended to be funded by a fully underwritten cash placing of approximately £75 million (before expenses) of new ordinary shares in the capital of the Company (the "Placing"), details of which have been announced by the Company separately today. The Board believes that the Acquisition has a compelling strategic and financial rationale as it:

The Placing: Keywords Studios plc, the international technical services provider to the global video games industry, announces its intention to undertake an equity placing of up to 5,750,000 new ordinary shares of 1 pence each in the capital of the Company (the "Placing Shares"), equivalent to approximately 10 per cent. of the Company's existing issued share capital (the "Placing"). The Placing, which is underwritten, is intended to raise gross proceeds of approximately £75m (before expenses) (the "Placing"). Rationale for the Placing and use of proceeds The Placing is being undertaken to fund the Company's proposed acquisition of the entire issued share capital of VMC Consulting Corporation ("VMC"), a leading provider of Functional Testing and Customer Support in North America (the "Acquisition"), and certain of its affiliates, from Volt Information Sciences, Inc. ("Volt") for a cash consideration of approximately US $66.4m (the "Consideration"), subject to certain working capital adjustments, as separately announced by the Company today. Transaction costs and working capital expenses are estimated to be a further US $5.0m. The additional proceeds raised will be used to finance the Group's strong acquisition pipeline. The Placing will allow the Group to maintain its conservative gearing policy. Certain Directors of the Company have indicated their intention to subscribe for Placing Shares. Further details of the Placing and any participation by such Directors will be set out in the announcement to be made on the closing of the Placing, which is expected to be made later today. The Acquisition is expected to be completed on or around 30 October 2017, conditional upon, amongst other things, completion of the Placing. Hold on, RNS No 3 of the day telling us that the placing has been fully taken up at 1400p which is a slight premium to yesterday’s close price and that some of the directors have also stumped up a few shillings to take part. My View: well, where does it all end for the “King of Meccano” with yet another bolt-on acquisition and this one is certainly the largest one to date. I have gone through the numbers in the rationale for the acquisition & to my eye, I can see some claimed advantages. The target company, VMC, do have recently declining YOY revenue but that's due to exiting low margin areas of business & I am sure KWS have done their due diligence stuff and are therefore happy with this high reputation bolt-on. My slight concern with KWS is the management coping with and integrating all of these bolt on businesses. I rather visualise a KWS board meeting to have a centre table with a whole series of plates spinning on sticks and directors running around to make sure none start to stutter and stall. Not to worry, with all investments I probably spend as much time asking myself What could go wrong” as I do thinking about what may go right. Anyway, Mr Market seems to like it and I guess those presented to must have been impressed, in fact, the shares motored up almost 20% by close of trading on the Thursday. Also, yes, yes, yes, I know it’s a placing, costs are saved etc but once again the good old faithful PI once valued in the embryo years of the now significant business is not as much as mentioned; not even as much as a “Mrs Brown feck-off”. I do confess to becoming a touch itchy with my KWS holding and that’s even after taking out my entire original invested capital a few weeks ago ; I simply bought them at such a low price, I still have a very substantial investment in them “riding for free” and even after top slicing they are still in the top five of my % of portfolio value. Maybe I am just feeling Octoberish, who knows but for now I will hold and see what happens. Wednesday 25/10/2017: No RNSs directly relevant to stocks within the portfolio. Thursday 26/10/2017: Bodycote: BOY: Market Cap £1.77bn: Trading update for third quarter on the year: Trading Update Bodycote, the world's leading provider of heat treatment and specialist thermal processing services, is issuing a trading update covering the three month period from 1 July to 30 September 2017 ("the period"). Current trading Group revenue for the three months ended 30 September 2017 was GBP169.0m, 16.6% higher than the same period last year and 12.9% higher at constant currency. Organic growth(1) was 9.1% at constant currency, reflecting 9.6% growth in our Aerospace, Defence and Energy business and 8.7% growth in the Automotive & General Industrial business. The year to date organic constant currency growth was 6.2%. The following review of the Group's markets quotes all movements on the basis of organic growth against the same period in 2016 at constant currency: Civil aerospace revenues grew 3.0% and continued to be driven by growth in Western Europe. The recovery in the North American onshore oil & gas market began during the second quarter and continued during the period. The overall growth of our energy revenues was 24.5%. Defence revenues continued to decline in the period. We saw continued growth of 8.3% in the car and light truck market, with strong growth in Western Europe and our emerging markets, while North American revenues were down. General industrial revenues were 11.0% higher against a weak comparable. General Industrial growth was achieved in all geographies, and was strongest in Western Europe. Financial position Net cash as at 30 September 2017 was GBP23.8m compared to net cash of GBP17.7m at 30 June. The interim dividend of 5.3p per share will be paid on 3 November 2017, at a cost of GBP10.1m. Summary and outlook Bodycote's performance in the period has been in line with the Board's expectations and, accordingly, the Group's outlook for the year as a whole remains unchanged. My View: I really like Bodycote and it has been kind to me, increasing in value by some 70% since I bought into it just over 18 months ago. I have also made further top us purchases of BOY along the journey; something I tend to do with the more compelling positions whilst the story unfolds. Today’s TU did not disappoint and I suspect that BOY will meet their year end numbers, we are in the 3rd quarter, with relative ease. Happy holder and I will continue to hold. Thursday 26/10/2017: BBC News item about a single traveller on a Jet2 flight from Glasgow to Crete. Just an observation but what a great bit of publicity for Jet2. The way I look at it, they probably had to go to Crete anyway to collect passengers returning to the UK from Crete so no money lost in real terms. Instead, they get a well-covered BBC news report showing the splendid care given to this single passenger. As I say, great almost free PR that hits budget competition such as Ryanair & its charming Michael O’Leary right out of the park: nice one for fellow Dart (DTG) holders in my view. Friday 25/10/2017: No RNSs directly relevant to stocks within the portfolio. Glad I’m Not There (GINT): well a nomination for this weeks GINT presented itself at 7:00 on a Monday morning with a weasel worded Trading Update from Dialight (DIA) blandly informing the markets that “due to short-term production challenges, we now expect EBIT for the year ending 31 December 2017 to be in the range of GBP13.5m to GBP15.5m”. Now in anybodys book thats a pretty hefty profits warning when you consider that the consensus was for GBP18.2m; if we take the mid-point of DIAs wide “we don’t have a clue” new range that’s a 20% shortfall on market expectations. Now these things do happen indeed they happen occasionally to my holdings that’s the nature of investing but unless you had the consensus figure at hand, the first impression a reader may be given is “ok, they have some production challenges but they do give us an indication of what EBIT will come in at”. Nowhere in the RNS do DIA say that they will have a very serious shortfall in profits: I would have expected at least a “materially below market expectations” comment from DIA to be worded in the RNS. Sorry, DIA, simply not good enough. Thursday also saw a rather unpleasant RNS from Lombard Risk Management (LRM), the only reason I came across this company is because it came up as a “high avoid” on the smoke & mirrors. Not one I would wish to ever own and I see on Twitter that it had been recommended by a journal tipster. That in truth is one of my major criticisms of investment journals; they are compelled to write up numerous weekly buy recommendations and I would think that over a two year period they would have suggested getting on the 50% of the shares listed on the LSE as buys. Finally, I did tweet about a planned purchase of an AIM company that was going to be added to my Hi Yield portfolio: well the order price I set was not reached so no purchase made but that’s the way it goes! On Thursday I cancelled the limit order as there was something that I originally missed in the figures that watered down my enthusiasm; as ever, it’s all about managing risk and protecting one's capital. I truth I rarely purchase any AIM stocks just for their yield and although I am of the opinion that there are some terrific stocks on AIM if one takes the time to research them, my AIMs are much more biased to growth than safe income. Next week: well it looks fairly quiet but maybe we will get the odd trading update maybe KWS will announce another acquisition; maybe they will go for ITV, who knows. Can you imagine the products of such a marriage? Coupled with my utter dislike for gaming, the possibility of Simon Cowell look alikes and the cast of Corrie being zapped by the press of a button on the latest KWS-ITV streamed game: maybe not a bad thought after all! This weekend the Hatters take on the mighty Coventry City at home so it’s a relatively easy 150 mile round trip to the theatre self-deception. Whatever your plans, have a good weekend and the markets will still be there come Monday.

0 Comments

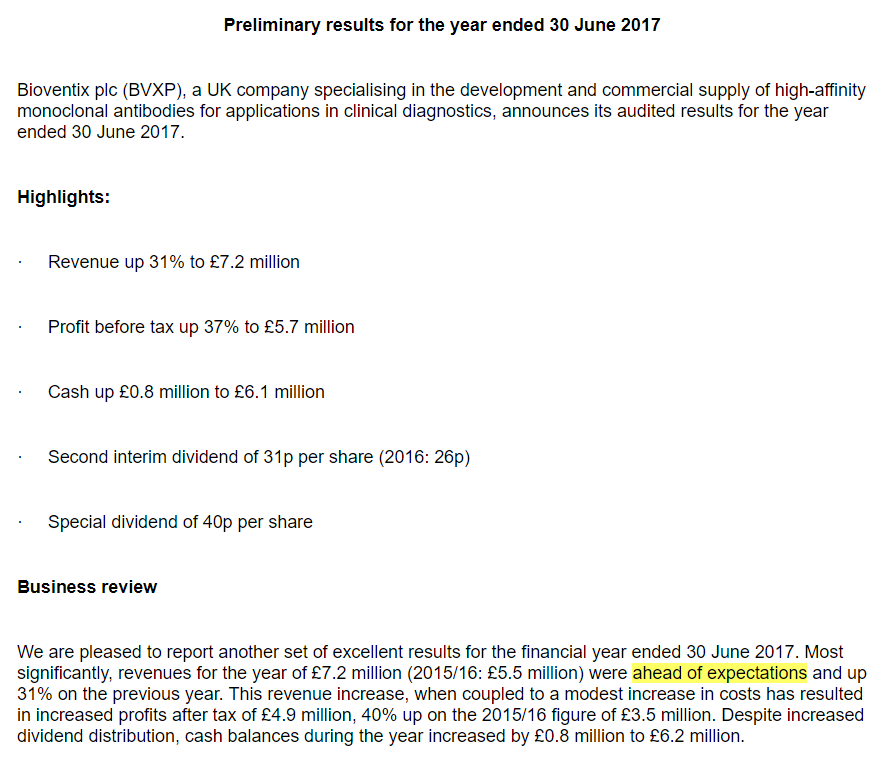

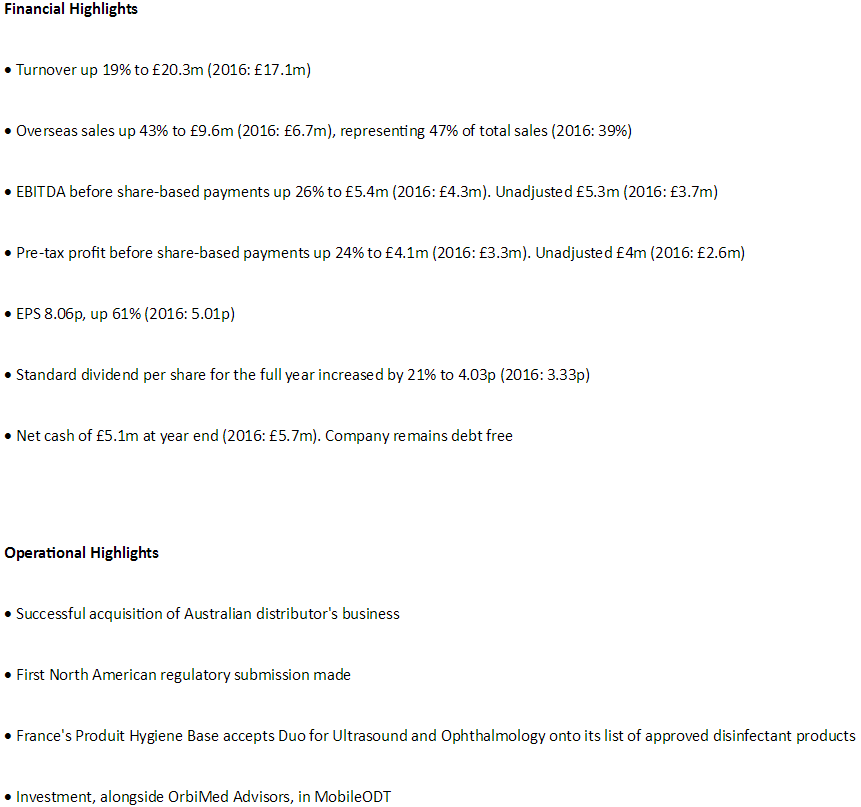

Well what a touch of good fortune this week as I received a letter from The International Postcode Online Lottery informing me that I had won £725,000. Now that is doubly fortunate as having never bought a ticket in the first place to actually win is simply amazing. I must call the telephone number on the letter and arrange to pay the few £000’s in order for my win to be released. Honestly, I sincerely hope that nobody falls for such a scam. Anyway, back to my whittling; a little bit of activity for the portfolio this week as I added a new holding, RWS Holdings; see notes below for Wednesday 18/10/2017. I also did a hefty top slice of Bioventix as well as some Zytronic. Both of these companies, BVXP & ZYT, are included in this log. Some of the proceeds of these sales were used to add further to my ITV holding which I have been continuing to add to since mid-September. I should say that I am now getting a touch concerned about the general Midas feel that investors have; should I feel that concern? Well, I have written before about the need to exercise some caution and remember that in a bull market valuations and indeed cult stocks can become terribly stretched like a stressed piece of elastic as the price of these Klondike microclimate stocks detaches from reality. Examples can be seen all over the place including a couple I write about in this note; e.g. although Tristel is a great business does it comfortably warrant such a high rating based on “things to come”? I am also evaluating the return of BOO to the portfolio, a stock I previously took profits in albeit a touch early, but yet again, the great business that it obviously is, does it really warrant such a sky-high valuation. Sorry, I simply don't have the answers but that does not preclude me from viewing the Klondike with caution. Monday 16/10/2017: Bioventix: BVXP: Final results for the year ending 30/06/2017:  Pleasingly a 40p special dividend has also been declared which added to the collective routine dividends of 51p for this year gives 91p which amazingly is equivalent to 13% of my purchase price of BVXP. As ever, the CEO, Peter Harrison, is very balanced with his comments: The revenues resulting from the success of the Siemens troponin project will be important in replacing approximately £1 million of NT proBNP sales that will be lost from the 2017/18 accounts due to the termination of a specific technology license. Conclusion We are delighted to be able to report such positive news for the current year. For the financial year 2017/18, our challenge will be to make up for the approximately £1 million of lost sales mentioned above with revenues from the newly launched Siemens troponin project and modest growth from additional vitamin D antibody sales and royalties. Beyond that, growth in the period 2018/2020 will be linked to our troponin project and the success of Siemens in their product launches around the world. We continue our research activities as we look to seed additional projects that will germinate in the period 2020/2030 creating additional shareholder value. My View: BVXP have performed exceptionally well in the three years that I have held them and Peter Harrison always modestly and conservatively looks at the future usually under promising yet overperforming. They have had an exceptional last three months with a 50% rise in the share price and as may be expected, this has drifted back a touch since the finals. Just to balance the risk of the touch of uncertainty over take up of new diagnostics, I have top sliced the shares up to 175% of my original investment. That leaves me still with a decent sized chunk "riding for free" and as an investor, I am very happy to continue to hold this reduced amount for the long term. Some of the proceeds have been used to purchase further ITV shares to add to my current holding. Monday/Tuesday/Wednesday: The daily news from RBG regarding their proposed takeover by Stonegate plus the “leaving with immediate effect” RNS about the CEO. Now before I go any further, I should declare that I no longer have financial interest in RBG having evaluated the “Stonegate Ultimatum”, I sold last Friday at 200p and booked a very tidy profit. Stonegate, I believe really backed themselves into a corner with their “Final Offer” and in effect scuppered any chance of solely increasing their offer above 203p as they have to abide by the Takeover Panel rules. The proxy votes and investors votes were not sufficient to get above the 75% YES threshold and so the deal was off. Now after selling I kept an eye on the RNS flow and saw that sadly some investors either don’t understand takeover panel rules or simply can’t add up even after the proxy results were reported on the Monday before the Tuesday shareholders vote, it was blindingly obvious that the 75% threshold just mathematically could not be reached in favour of Stonegate. Finally, as a non-invested bystander, I did smirk a touch when the news was announced on Wednesday 18/10/2017 that the CEO was leaving with immediate effect and the post to be temporarily covered by the chairman. They seem to have this type of misfortune at Revolving Door Group, sorry RBG as they lose CFO’s and a CEO. Anyway, due to the tight profit margins and type of business it is (I detest Vodka), I simply thank RBG for the short ride and wish them and all current shareholders all the best and to be honest, I reckon they will eventually do ok. Wednesday 18/10/2017: RWS Holding: RWS: Market Cap £1263m. Three RNSs this morning. Firstly the proposed acquisition of Moravia: RWS Holdings plc, a world leading provider of intellectual property support services (patent translations, international patent filing solutions and searches), commercial translations and linguistic validation, today announces that it has entered into an agreement (the "Acquisition Agreement") to acquire the entire issued share capital of Moravia US Holding Company, Inc. and Moravia Lux Holding Company S.à r.l. (together "Moravia"), a leading provider of technology-enabled localisation services, from Moravia Holdings II, LLC (the "Acquisition") for a cash consideration of US$320m (the "Consideration") plus working capital and certain other adjustments and transaction costs. The Consideration, adjustments and transaction costs are intended to be funded by a c.£185m (before expenses) cash placing of new ordinary shares in the capital of the Company (the "Placing"), details of which have been announced by the Company separately today, and a new US$160m term loan which will refinance the Group's existing facility (the "New Facility"). The Board believes that the Acquisition has a compelling strategic and financial rationale as it: Brings to the Group a highly successful business with a strong track record of profitable and cash generative growth: Long term relationships with some of the largest publicly traded technology companies in the world Has increased revenues by a CAGR of 26.0% from US$100.3m in 2014 to US$159.2m in 2016 and adjusted EBITDA by a CAGR of 52.6% from US$11.6m in 2014 to US$27.1m in 2016 Creates a third RWS division of scale with significant growth prospects: Growth opportunities include increasing share of wallet with its long-standing clients, winning new clients, introducing complementary solutions and growing new verticals and geographies Will operate as an autonomous division, replicating the successful creation of a Life Sciences division through the Group's acquisitions of CTi and LUZ, giving the Group three divisions of scale in attractive global markets, all with strong track records of profitable, cash generative growth Further diversifies RWS, as it is expected to represent approximately one third of the enlarged group's profits, and strengthens its global operational base Provides significant additional market opportunities for both companies due to their complementary business activities, geographies and client base, including the potential cross-selling of patent translation services to Moravia's intellectual property-rich clients Brings a strong, well established management team to the Group Is at an attractive valuation for one of the few major localisation providers focussed on the high growth technology sector in a highly fragmented market Is expected to be highly and immediately earnings enhancing for RWS shareholders Secondly, we have an RNS telling the market about a placing of 45,000,000 shares with institutions in order to fund the acquisition. Finally, later in the morning an RNS informing the markets of the success of the placing at 425p: sadly PIs have been overlooked from consideration, it seems the larger a company gets the less it treasures its PIs. My View: quite an interesting one for me this as I dithered on a purchase following their excellent trading update of 03/10/2017 “adjusted profit before tax (before amortisation of intangibles, share option costs and exceptional acquisition costs) is also expected to have performed strongly and ahead of market expectations”. Luckily the acquisition and placing announcements of 18/10/2017 gave me a second opportunity to climb on board at a reasonable price. My “fag packet” calculations very much agree with the RWS statement that this deal should be very & immediately earnings enhancing for shareholders but that’s not all, a quick scan around the Moravia web site reveals a tantalising list of customers:  Is RWS expensive? Well, readers will know that I am just not at all impressed by the ubiquitous “Arfer Daley” PE, I much prefer to base my comfort on ROCE, CROCI and free cash flow and RWS scores highly in these areas. So, on board now and look forward to the ride which I hope will be a long one. Thursday 19/10/2017: On The Beach: OTB: Market Cap: £587m: 2017 Full Year Trading Update “Strong H2 revenue growth across all markets” The Group has traded well in the year with adjusted PBT performance expected to be in line with Board expectations. UK revenue growth for the year was 17% on the back of a strong H2 performance with growth of 26%. Excluding the acquisition of Sunshine.co.uk Limited, UK revenue growth was 14%, with H2 revenue up 21%, with continued progression in UK EBITDA margin compared to 2016. The Group experienced significant growth for the majority of the key summer trading period, despite some softness in the weeks that followed the Barcelona terrorist attack in August and we have exited the financial year with strong forward momentum. My View: looks fine to me and although reference is made to the Monarch failure, I can’t visualise that this will be more than a small blip on the one year figures. Overall I am happy to continue to hold. Thursday 19/10/2017: Tristel: TSTL: Market Cap: £126m: Final results for year ending 30/06/2017 and I have screenshot the headline numbers below:  Well, the year ended 30/06/2017 look very good with the company heading in the right direction so no complaints there. However, I really would encourage Tristel to clearly include an outlook statement rather than leave the investor to glean what may be going on from the residual text published: sorry TSTL not good enough. Maybe the lack of an outlook is down to the delay/uncertainty with the North American venture? Well ok, be open and simply include a note in the phantom outlook statement.

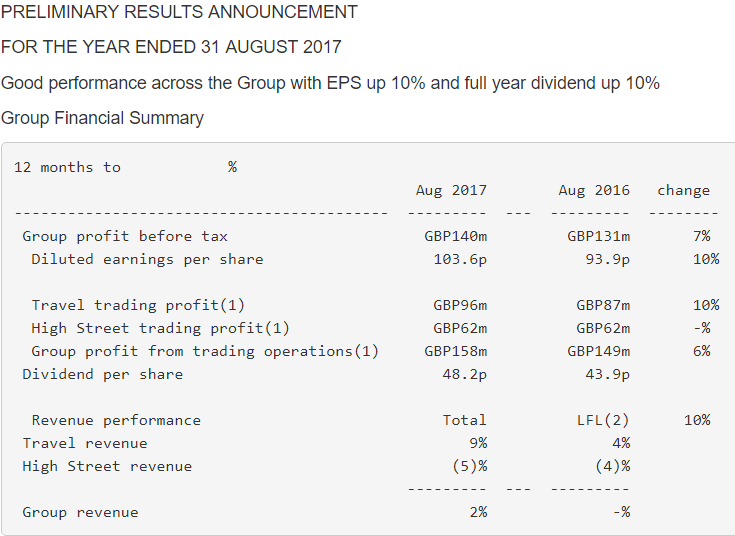

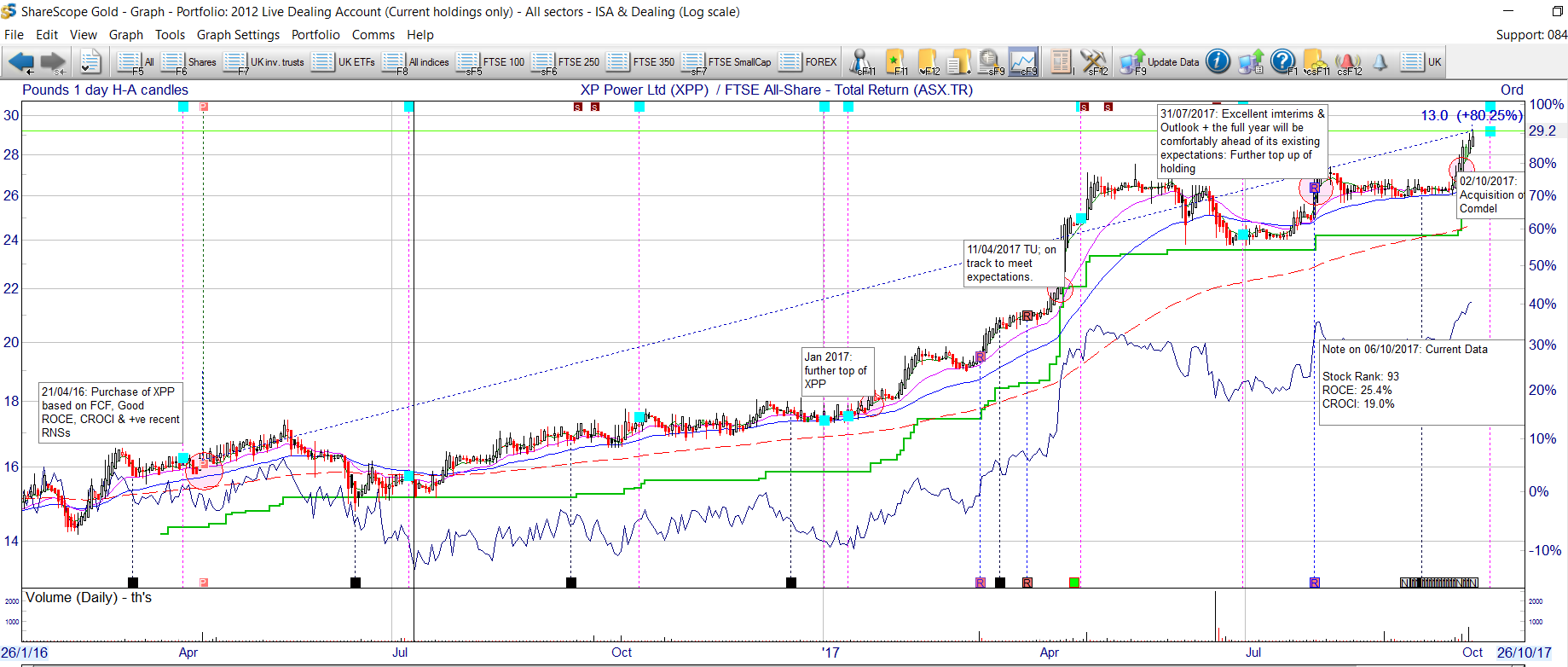

My View: well I have had my reporting rant so what do I really feel about this business that I first took a fairly sizable stake some years ago when the price was 69p and that holding was then sold for 124p when a RNS gave me concerns about greedy share based payments and slowing down sales in the UK. Indeed at the time, the market was not overly impressed and the shares drifted over the next five months from a high of 145p to 90p. In the rising 90’s I re-entered the stock and then top sliced at 200p; wise or not, it was simply becoming too dominant a position within the portfolio and for risk management, I cut it back a touch. Overall, historically the company has been one of my favourites but what about the future? Firstly the stock does have great expectations built into the price which itself has appreciated by 90% since the turn of the start of the year and some 40% since July. Balancing that we have to consider that if regulatory approval is gained for North America then despite what appears to be a high rating, the stock should nicely continue to increase in value. On the other hand, I note some investors consider the stock to be expensive and should there be further USA delay or even a refusal, then the share price could easily be under severe pressure. On balance, I will continue to hold my remaining shares although I have to say that I appreciate the comfort of having banked very good profits on this one. Finally, if I did not already hold some TSTL, would I see TSTL as a compelling buy? I have to be brutally honest with myself and say no. Thursday 19/10/2017: Zytronic: ZYT: Market Cap: £96m: Trading Statement: The Board of Zytronic is pleased to provide the following pre-close statement ahead of announcement of the Group's results for the year ended 30 September 2017, which is expected to take place in December 2017. Revenues have continued to show good progress over the prior period, and results are expected to be in line with market expectations. My View: simply looks fine to me and despite my top slice this week, I am very happy to continue to hold a decent slice of ZYT which has handsomely delivered for me since my initial purchase in early 2015. I did have a scan round the quotes from other PIs and saw some remarks such as “an uninspiring trading update” but there you go, ZYT can't be expected to be “ahead of expectations” all of the time. I have seen an argument run to say that the valuation on a PE of 20 is historically on the expensive side but you know what, I think that the placing of an over reliance on the PE alone is simply misleading. For starters, if you strip out the cash that ZYT holds this PE comes down quite nicely. Now to my preferred measures: ROCE, CROCI, free cash flow & FCF conversion and I see a real quality business and it’s up to the individual investor to decide if the current share price offers reasonable value. The risk; well with reliance on a limited numbers of customers there is a risk of hitting a bump in the road. Personally, I decided that for a relatively small company ZYT had due to its success, really pulled it's weight & some more since the start of 2017 and that a top slice would be a prudent measure (Note: I am beginning to sound like Gordon Brown in saying prudent, HELP!) The remaining chunk, I am happy with and will continue to hold. Thursday 19/10/2017: Keyword Studios: KWS: Market Cap: £780m: Well, I was beginning to worry having not read of an acquisition by KWS for a few weeks but those needless worries have been set aside by the announcement of the acquisition of d3t ( you know this all gets a bit confusing as I already hold D4t4 but what’s in a name?); anyway the RNS for KWS: Keywords Studios, the international technical services provider to the global video games industry, today announces that it has acquired d3t ltd ("d3t"), for a total consideration of £3 million from the founders Jamie Campbell and Stephen Powell and others (the "Sellers"). Based in the North West of England, between Liverpool and Manchester, d3t delivers premium quality outsourced software development services for video game developers and publishers internationally. The acquisition of d3t is in line with Keywords Studios' strategy to grow organically and by acquisition as it selectively consolidates the highly fragmented market for video game services. d3t brings additional skills, client relationships and geographic reach to Keywords, extending the strength and scale of its recently established Engineering service line. Founded in 2011 and now employing 44 staff, d3t is an award-winning software development company with capabilities including HD re-mastering, porting, optimisation, rendering and game systems development. Over the course of the last six years they have delivered consistent high quality across dozens of projects for clients such as SEGA, Codemasters, Sony XDev and the BBC. Jamie Campbell and Stephen Powell, along with the rest of d3t team, will remain with the business. In the year ended 31st of July 2017, d3t achieved revenues of £2.8 million and an underlying adjusted pre-tax profit of £0.4 million. Under the terms of the acquisition Keywords is paying a consideration comprised of £2.4m in cash and the issue of 42,368 new ordinary shares in Keywords, which will be subject to a two-year lock in period. Giacomo Duranti, Chief Operating Officer, commented: "The acquisition of d3t complements our recent acquisition GameSim's capabilities to extend the services, scale and geographical presence of our Engineering offering. With increasing demand in the video games industry for reliable, high-quality outsourced software engineering services, we are building a strong offering to support our clients globally. My View: As I wrote a couple of weeks back, I still have a very significant holding in KWS that I am essentially running for free having taken out the value of my original investment in the business; it still remains one of my major holdings. The share dilution and cost of the acquisition are fairly insignificant so it’s really a question of bedding the new business in and continued delivery; something that KWS appears to be rather good at. I try to imagine how this gaming Mecano company that bolts on so many acquisitions manages the growing empire and that’s my only concern with the stock. Personally, I absolutely detest all gaming, it just does not relax me but that could possibly be because I am totally crap at it; give me the full TV series of Breaking Bad any-day! However, investment is not about one’s personal preference, it’s about attractive and hopefully sound companies and KWS continues to meet my selection criteria. To be honest, I think I may be holding this company for many years to come. Friday 20/10/2017: IQE: IQE: Market Cap: £940m: RNS regarding the under-payment of US Tax due to an unfortunate third party accountancy firms regrettable ignorance: Settlement of Prior Years Taxes: The Group recently engaged the services of an international tax firm to assist with a routine US tax filing for the year ended 2016. Unexpectedly, this exercise has identified taxes due in the US relating to the profits of an overseas subsidiary for the years ending 2013, 2014, 2015 and 2016, which follow the acquisition of the epitaxy business of Kopin in January 2013. This firm has estimated the tax due as approx. £4.2m, and is in the process of calculating the actual amount, which may take up to 4 weeks. IQE immediately initiated the payment of the estimated amount to the relevant tax authority, and will adjust any over/under payment in due course. On the advice of this firm, IQE has also accrued interest due of up to £0.4m. As a result of a Group re-organisation initiated in September 2016, but unrelated directly to this previously advised tax treatment, it is believed that no similar tax liability arises in 2017. The wildly optimistic line which I think is total fantasy is that IQE feels that they can claim full recompense from a local tax advisory service for the issue. In my opinion, that's daft. Whilst they may be able to gain some claw back on fees, the US taxes are clearly owed by IQE and not down to the activity of the third party accountancy firm. IQE is clearly extremely disappointed with the previous professional advice received and will be pursuing full recompense as a matter of priority with the previous advisors. I guess the reassuring part is a hint on current trading: The Group has enjoyed a strong Q3 with continuing growth driven largely by the ongoing strong VCSEL ramp in support of a highly significant mass market consumer application, and the new Foundry expansion remains on course to open in H1 2018. As a result, the Board remains confident the Group is on track to deliver full year expectations, including that of net debt. My View: lots of the figures may well be brushed away as exceptional items and at least the company has been responsible in highlighting the issue and also giving a flavour of current trading. Glad I am not there: well on a few occasions as I pen these notes I have and will continue to declare that I hold or held a “Glad I am not here” as they occur. Let’s face it, I am most definitely not clever enough to invest only in companies that never have issued bad news or profit warnings. This week the flavour is slightly different with RWS which did not treat it’s PIs that well with the placing and that hit current shareholders, particularly as they were not included in the offer. However, I bought straight into RWS on the day of the acquisition & placing announcements but at the same time feel for those PIs treated a tad shoddily by the lack of consideration by RWS. I suppose those PIs were important to RWS at one stage but just like stepping stones on a stream, they become less significant when the company has grown and crossed that once challenging stream: sad but a fact of investment life. This weekend my football travels continue to watch the table topping Hatters (yes that's right, table topping) at Crawley. I will make the fairly easy journey by train and have a couple of pints of decent ale in the Brewery Shades Inn before the game. Whatever you are doing, I hope you have a great weekend & as ever, happy investing. Voyager RNS Log WC 08/10/2017 Note: as ever nothing I write here is in any way a recommendation; well apart from the superb meze. Just view this as me meandering through my thought process concerning various regulatory announcements and sharing my views. It has been quite a busy week but in terms of the portfolio, the composition apart from reinvested dividends has remained constant without any transactions taking place. My thoughts on the various RNSs relevant to companies that I hold are: Monday 09/10/2017: XP Power: XPP: Market Cap £596m Trading Update: I did comment on XPPs acquisition of Condel last week and in a pleasant start to this week we have an excellent “ahead of its previous expectations” Trading Update. Trading Trading in the third quarter has been robust. Revenues for the nine months ended 30 September 2017 increased by 34% over the prior year to £123.9 million (2016: £92.6 million). In constant currency the increase in revenues was 21%. Order intake for the nine months ended 30 September 2017 was strong at £137.5 million (2016: £95.8 million) which was 44% higher than the prior year. In constant currency this was an increase of 30%. Our third quarter order intake was £44.1 million (2016: £34.2 million). The momentum in our order intake is encouraging, particularly the continued growth we are experiencing in our North American markets. Outlook We are encouraged by another quarter of strong order intake with our end markets remaining buoyant. The Group believes it is continuing to take market share as its portfolio of industry-leading power technology products is increasingly designed-in to new equipment by our target customers. These design wins will translate into orders as our customers’ projects move to production phase over the coming years. The Board now anticipates the Group’s performance for the full year will be ahead of its previous expectations outlined at the time of the Group’s interim results on 31 July 2017. My View: well, how can I be anything but happy with that RNS: I am happy to continue holding. Tuesday 10/10/2017: Revolution Bars: RBG: Market Cap £100m: a string of put up the money, no we will not, swipes between RBG and Deltec that culminated with Deltec declaring that they would not be making a cash offer for RBG; hardly a surprise in my opinion as Deltec was debt ridden and did not have the cash. So it’s back to the 203p which I won’t grumble about as it gives me a fortunate 70% profit on stock I repurchased as a special situation recovery stock; I was simply lucky: right place at the right time etc. Note: on Thursday, Stonegate in an RNS, indicated that their bid price for RBG would remain at 203p. Wednesday 11/10/2017: Telford Homes: TEF: Market Cap £308m: Trading Update: reads well enough to me: The Group's reported profits in any given period are driven by the number of open market completions achieved and there were far fewer of these in the first half of the year than the number expected in the second half. This is purely down to development timings which are all on track and in accordance with the original programmes but do not fall equally across the year. Completions of individual properties are proceeding exactly as planned with no unexpected delays. As a result of the imbalance of completions across the year pre-tax profit for H1 2018 will be significantly lower than H2 2018 and also lower than the corresponding period last year but will be entirely in line with expectations. The interim dividend is proposed to increase in accordance with the anticipated full year profit growth. The Group is on track to deliver full year profit before tax in excess of £40 million in accordance with market expectations and the Board's longer term positive outlook is unchanged. My View: I feel that Telford are an impressive company that without fuss simply gets on with the or business plan and monotonously delivers: just the sort of company I lIke to own. The table below reproduced from SharePad, compares five housebuilders that I either own or have owned over the last 18 months. As you can see from the table, Telford has many attractions and in my view is the housebuilder I would choose to own if I were limited to holding just one stock in this particular sector.  Thursday 12/10/2017: Norcros: NXR: Market Cap: £103m: Trading Update: Oh how nice to read an NXR release update where even the dull accountants take a positive note. The thrust of the TU is overall good progress and in-line. Group revenue and underlying operating profit(1) in the first half is expected to be in line with the Board's expectations. Group revenue for the first half is expected to be approximately GBP144.9m (2016: GBP128.8m), 12.5% higher than the prior year and 7.1% higher on a constant currency basis. The growth reflects a robust performance in our UK business and continued growth in our South African business. My View: I still think this is an astonishingly undervalued business whose share price has been held back by the perception the market has over its pension deficit. NXR have also done very well in reducing debt from £27.5m in 2016 to £21m in 2017. I did a write up on NXR at the time of the AGM at the end of July when I commented that in my view Mr Market is being far too pessimistic about that pension deficit which is well managed and has a very high average age per member. Thursday 12/10/2017: WH Smith: SMWH: Market Cap £228m: Preliminary Results:  Stephen Clarke, Group Chief Executive, commented:

"We have delivered a good performance across the Group. "The Travel business continues to perform well with strong revenue growth, up 9% in the year. For the first time, revenue in Travel has overtaken High Street and Travel is now the largest part of the Group in both revenue and profit. Profit in Travel is up 10% to GBP96m, now over 60% of Group trading profit. "During our 225(th) anniversary year, we were delighted to open our 225(th) international store and now have 233 stores open. We have won 273 stores across 25 countries, including new stores in Singapore and Rome. "The High Street business performed well - matching the particularly strong profit performance from last year. Our investment in new product design continues to drive stationery revenue and we have been pleased with the success of the recently launched Tom Fletcher Kids Book Club. "The Board has proposed a 10% increase in the final dividend and we have today announced a further share buyback of up to GBP50m reflecting the Group's cash generation and our confidence in the future prospects of the Group. "This performance is only possible through the hard work and commitment of our 14,000 colleagues across the business and I am grateful for their continued support. "Looking ahead, we will focus on profitable growth, cash generation and new opportunities to profitably invest in the future. While the economic environment remains uncertain, we are well positioned for the current year and beyond." (1) Group profit from trading operations and High Street and Travel trading profit are stated after directly attributable share-based payment and pension service charges and before unallocated costs, finance costs and taxation. See Note 3 to the financial statements and Glossary on page 31 for an explanation of the definition and purpose of the Group's alternative performance measures. (2) Like-for-like sales are calculated on stores with a similar selling space that have been open for more than a year (constant currency basis) My View: well anybody who follows my writings will know that SMWH is truly one of my favourite investments; incredibly boring and they just deliver. It’s interesting to see that the continued growth of the travel offering which has been a huge success: when was the last time I did not have to queue at a Smiths at either a motorway service station or airport? Maybe market research at it's best! Despite the 35% rise in SP since the start of 2017, I am happy to continue to hold. Thursday 12/10/2017: Just Eat: JE. Market Cap: £477m RNS regarding Hungryhouse merger:- CMA provisionally clears Just Eat / Hungryhouse merger Just Eat plc (LSE: JE) welcomes today's announcement from the CMA that it has provisionally cleared the company's acquisition of Hungryhouse. We are pleased that the CMA has provisionally concluded that this transaction does not lessen competition. We look forward to continuing to deploy our technology and expertise to help more independent restaurants develop and grow their businesses, while offering an even better service to consumers. My View: The market seems to like the news and the shares kicked on over 6%. Admittedly not my usual style of purchase being on such a stretched valuation but I will console myself by calling it a “special situation”. Friday 13/10/2017: no RNSs of mote involving shares within my portfolios Glad I Am Not Here: well I of course always like to think that things will turn out well for shareholders and particularly so with the case of AIM stocks where generically the universe is a tougher place if one does not take care. This week we had the rather astonishing announcement from Mytrah Energy informing the market that the chairman had taken an “unauthorised loan” from the company to purchase a property; just how did that escape corporate governance from a business that is loss making and with terrible cash flow? Now I do honestly believe that on AIM there are some really excellent well managed companies that are very worthy of an investment, in fact over a third of my portfolio is invested in AIM companies but they are ones where I have trust in the management of the company. Just a case of being diligent and doing research plus the all important risk assessment. Having said that, remember that the next profits warning is maybe just around the corner; simply the nature of investment particularly in small companies. Another qualifier for the Glad I Am Not Here weekly award is Character Group: CCT. Now this is a share I have owned a couple of times over the years and and on Wednesday they were firstly a little naughty with a late RNS offering the markets a trading update at 08:00 a touch late in the day for my liking and really just unacceptable; I mean did the accountant break the news to the CEO over the morning bowl of corn flakes? Actually, that’s a reasonable scenario as they are a serial profits warner; sorry, I will get my coat! The RNS tells us that “At this early stage of the Group's new financial year the Board consider that, based on the latest sales and market data available to them, the Group's performance for the year ending 31 August 2018 is now expected to be significantly below current market estimates. Nevertheless, the Directors believe this to be a temporary downturn and that the Group anticipates returning to its previous growth pattern during the second half of the 2018 calendar year, and this ultimately is expected to be reflected in the financial performance for the year ending 31 August 2019”. Now for my part, I began to lose confidence in management, again, with some trading updates and also a video presentation the company did; the whole thing just started to appear to be a risk in my opinion and I sold in January 2017 for a smidgen on an overall gain. As I always say, once you doubt something about a company it’s simply time to go; I may not always be right but it’s a question of comfort and managing perceived risk. It’s just a question for the individual investor and what you feel comfortable with. For example, some discomfort sales over the last four years in addition to CCT have been SAL, SHOE, SPRP, PMP, TCM & TRAK. With it’s strong balance sheet, I suspect CCT will go on and do what it usually does i.e. a mix of good progress sprinkled with the occasional profits warning. Next Week: I expect to see trading updates from ZYT & AMO early next week and in fact the market has been racing ahead a touch with ZYT so obviously, some investors feel there is good news to come but for my part, I am much more cautious with small-cap companies. Sometimes the order book can be lumpy and disappoint so let’s wait and see. We also have the finals from BVXP which has enjoyed an incredible increase in share price of over 100% in 2017. Have a great weekend and as ever, happy investing Voyager RNS Log WC 01/10/2017 Well, quite a lot to talk about this week on the portfolio front with a number of announcements that made interesting reading after ploughing a steady mile in the pool. Strange how we all have some “addictive” pursuit; just could not imagine the early mornings without a nice calming pool in front of me. Just as a general comment and maybe a take care reminder; the markets we currently trade in are probably at one of their easier moods than I have generally experienced over the last 30 years of investing and I fear that there are many investors out there who have never experience a bear market or serious correction. It seems that the world and his brother are making 20%, 30% etc at present and that does genuinely please me but do remember that the music will not keep playing forever: just a reminder that “everybody is a winner in bull markets” and they simply don’t continue forever and careful stock selection of quality businesses is to my mind essential. A couple of Whittler Rules:

Anyway the universe/folio RNSs: Monday 02/10/2017: XP Power: XPP: Mkt Cap. £546m: RNS Regarding their acquisition of Condel Inc.: The RNS reads: XP Power, a world-leading developer and manufacturer of critical power control solutions for the electronics industry, announces that it has acquired the business and assets of Comdel Inc. ("Comdel"), a designer and manufacturer of radio frequency ("RF") power supplies (the "Acquisition"). Total consideration of US$23.0 million (GBP17.0 million) was paid in cash on completion. The Acquisition is on a debt and cash free basis and was funded with a new revolving credit facility of US$40.0 million with a US$20.0 million additional accordion option. The new facility is in place to assist the company's inorganic growth strategy. Comdel is based in Massachusetts, USA, and supplies the industrial and technology sectors with a range of standard, modified and custom high power RF power conversion products. Comdel typically supplies RF power supplies to the semiconductor, thin film, photovoltaics, and induction heating industries. In the fiscal year ended 31 December 2016, Comdel recorded sales of US$16.5 million (GBP13.0 million), profit before tax of $1.8 million (GBP1.4 million) and had gross assets at the year end of $10.9 million (GBP8.5 million). The Acquisition is expected to be enhancing to the Company's earnings per share in 2018*. My View: Looks a decent acquisition to me and will hopefully boost XPP growth prospect over the coming years. Is XPP expensive? Well even on the ubiquitous and often manipulated PE ratio, not terribly expensive for a company experiencing attractive growth in my opinion. As ever, I look to the returns on capital which are very attractive and confirm my view that I am very happy to continue to hold. In fact, I am a little niggled with myself as although I have made various top-ups over the last 18 months, I really should have been more committed to my “fag-packet calculations” that kept shouting to me to make a further significant purchase. I reckon we all have the gift of wisdom after the event! Click on chart to enlarge:  Monday 02/10/2017: On The Beach: OTB: Mkt Cap: £526m: an RNS statement regarding Monarch Airlines: On the Beach Group plc, (LSE: OTB), the UK's leading online retailer for beach holidays, notes the recent announcements by the Monarch group and the Civil Aviation Authority that Monarch Airlines Ltd and other companies in the Monarch group have entered administration. On the Beach is contacting customers that are currently in resort to assist with their return travel and also those customers booked to fly with Monarch Airlines in the coming weeks and months. The Group has Scheduled Airline Failure Insurance in place which covers the failure of Monarch Airlines Ltd including monies paid to Monarch Airlines Ltd and also the costs to repatriate customers currently in resort. The Board anticipates that there will be a one-off exceptional cash cost associated with helping customers to organise alternative travel arrangements or providing refunds and will update shareholders in due course. The Group has no exposure to Monarch Holidays Ltd bookings as it only offered Monarch Airlines Ltd seat-only flight options on its website. My View: this sort of thing happens in the travel industry and with the pressure on airfares it will undoubtedly happen again maybe not to OTB but certainly elsewhere. I take a fairly relaxed view to this event and will continue to hold my current position. Tuesday 03/10/2017: Revolution Bars Group: RBG: Mkt Cap: £105m: Results For Year Ended 31/07/2017. The results in truth mean very little as RBG is the subject of an agreed takeover by Stonegate at a price of 203p; that price may of course rattle up a little if Deltic who are ponderously carrying out due diligence on RBG, come in with a higher offer before 5pm on 10/10/2017 the deadline set by The Takeover Panel. Of course, there is always the possibility that a third potential bidder may enter the contest and for that reason, I am happy to stay invested with the comfort that the Stonegate 203p is near as money in the bank. Readers may recall that earlier in the year following the announcement that the second FD was to depart RGB having only been in post a handful of months, I took this as a major red flag warning banner and immediately sold my holding. An extract from my RNS Log of 04/08/2017 reads I originally bought into RBG in January this year but following an announcement that the second CFO in a few months had declared he was leaving the business I sold my entire holding; 2 x CFO’s leaving in a short space of time just did not sit well with me. A few months later, May 2017, RBG duly issued a profits warning and the shares were absolutely caned eventually bottoming at about 50% of the pre-profits warning price in early July: hardly surprising as management credibility had declined and with it the trust of many investors. On Tuesday last week, RBG issued a very reassuring trading statement and it appeared the new CFO had brought a bit of sanity and reassurance to the business. I pondered for a couple of days and then bought back in on Friday afternoon. Back to the RBG Results: The results do reveal an accounting mess at RBG before the time of the current FD: Our results Our reported results show good progress against the prior period, with sales growth of +9.2% and even stronger growth in adjusted EBITDA*** at +16.0% against the restated figure for the prior period. We consider adjusted EBITDA*** to be the key measure that best represents the business' underlying performance as it excludes exceptional items and bar opening costs that are a function of the timing of the new venue development programme rather than the underlying trade. Last year's adjusted EBITDA*** has been restated from GBP15.6m to GBP13.0m. Operating profit was GBP3.7m (2016 Restated*: GBP5.3m) but this was after charging exceptional items of GBP4.4m (2016 Restated*: GBP1.4m). During the year, there was significant change within our finance team. This included the Chief Financial Officer, Sean Curran, and the Group Financial Controller, who had both been with the business for over ten years, both leaving the Group. Chris Chambers replaced Sean in the autumn of 2016 but resigned shortly thereafter in February 2017. Mike Foster joined the business in March 2017, initially as interim Finance Director, before being appointed to the Board and as the Group's Chief Financial Officer in early June 2017. Our Finance and IT teams play a critical role in providing the systems and reporting to facilitate running an efficient business. Significant IT developments have been undertaken in the year to support the Sales, Operations and People Development teams. Our Finance team has had much to contend with in the last year and it is now very clear that our accounting systems and processes were in need of upgrading. Improvements have been made, and will continue to be made, in this area to provide a more robust financial infrastructure and in so doing bring additional benefits. My View: All in all a bit of a financial reporting muddle at RBG and it’s just as well in my opinion that another company looks like taking them over albeit at a probable bargain price just north of 200p. Reference Note: Note: now just to reiterate, I do NOT OFFER ADVICE on specific shares but merely share my rationale and methodology of investing, However, I have over the years built up a series of Whittler Rules that sit on my office wall. In the case of RBG at the time of my initial exit as two FDs sought other opportunities, the rules that applied, again as on my office wall, were:

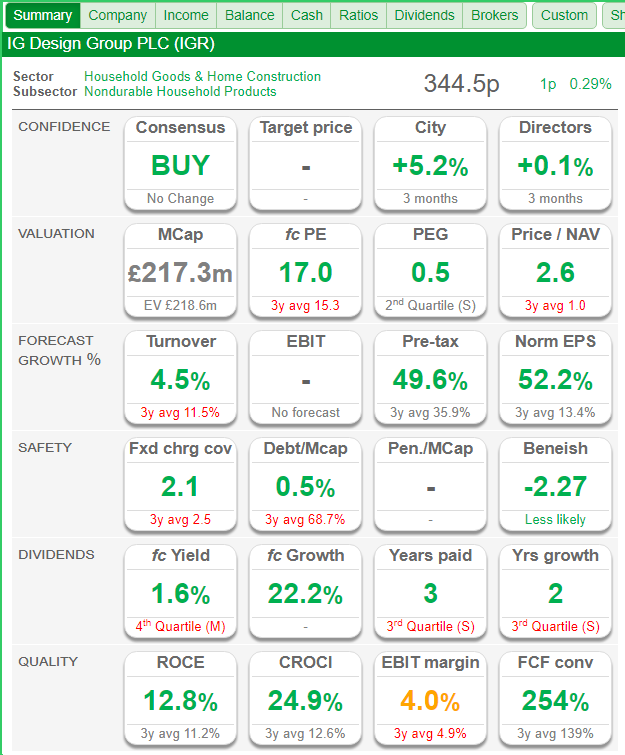

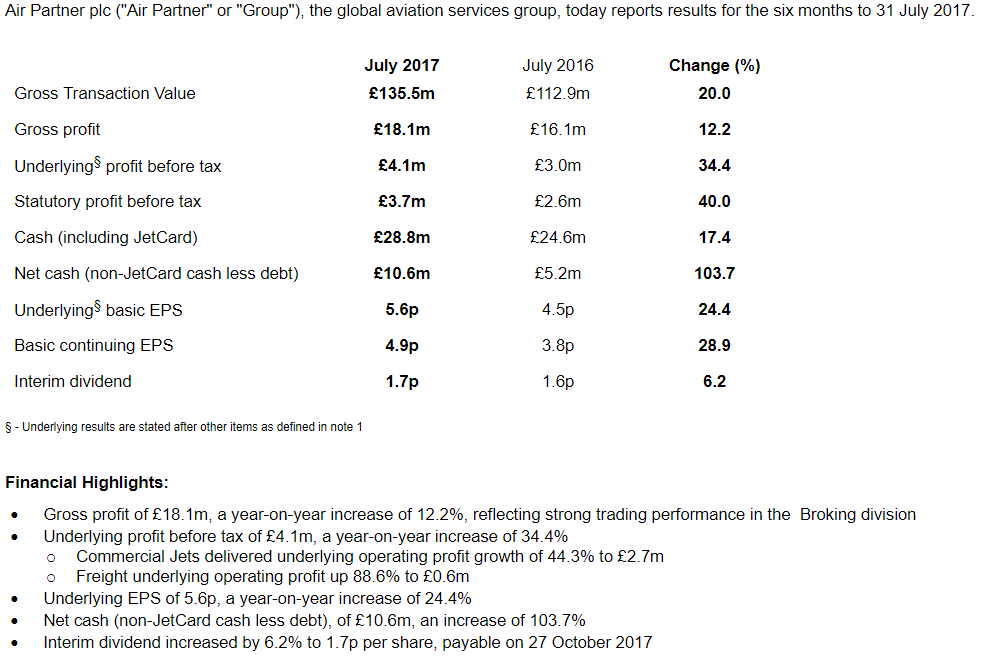

Tuesday 03/10/2017: AB Dynamics: ABDP: Mkt Cap £114m: Pre-Close Trading Update: The Group has performed well in 2017 and the Board expects revenue and profit before tax (excluding share option charges and latest IFRS 15 adjustments) to be slightly ahead of analysts' forecasts. The Board has chosen early adoption of IFRS 15, from 1 March 2017, and this is expected to lead to a reduction in the level of reported revenue for the year to 31 August 2017, but with no consequential impact on profit before tax. Despite the adoption of IFRS 15, it is anticipated that reported revenue will nevertheless remain in-line with current market expectations. My View: I like ABDP and it’s rewarded me nicely since my couple of batches purchased in June & July of 2016 following a fall back in the previous high flight path of the stock. Within the update are the pleasingly reassuring words that the PBT will be slightly ahead of analysts expectations: much nicer wording than management expectations as after all, what are management expectations! Is the share expensive? Well, I personally think not given its niche state of its business and forecast profits growth over the next couple of years. Also the returns on capital, ROCE & CROCI have been historically high and look like staying that way. Probably one I will hold for quite some time to come. Wednesday 04/10/2017: No RNS relating to a share within my universe or portfolio. Thursday 05/10/2017: Only one RNS of serious note for the portfolio in that Deltec came out with a very wordy RNS essentially suggesting a non-cash takeover/merger of Deltec & RBG. I guess this one may drag on for a while and hopefully may either flush out an improved bif from Stonegate or suck in another bidder who may see the RBG offering being undervalued at a touch over 200p. I think I will just sit on my hands and not get overly excited until the end game is a touch closer. Friday 06/10/2017: No RNS relating to a share within my universe or portfolio. Glad I Am Not Here: well, its a fairly sad one this week for holders of Accrol Group: ACRL with an apparently disastrous announcement that the shares are to be suspended with the likelihood that much of the forecast profits for this year will be flushed down the pan along with the companies tissues that they manufacture. You could go on with the puns but in truth it’s simply not a happy position for investors who bought into ACRL when It was listed on AIM not that many months ago. I have to say that I very rarely invest in IPOs and take the view that I would rather have a decent look at the minimum of a few months listed trading and numbers to anywhere near give me an acceptable degree of comfort. An added deterrent for the ACRL float was the enticement of a fat yield in order to get investors on-board. Were there any warning signs? Well, I would say there was one that would not sit well with me and that is the RNS dated 07/09/2017: giving a TU and the announcement of the appointment of a new CEO: the RNS reads: Accrol Group Holdings plc (the "Company" or "Accrol"), the AIM-listed leading independent tissue converter, announces that Gareth Jenkins has been appointed as Chief Executive Officer with effect from 11 September 2017. Gareth joins the Company having spent 24 years at DS Smith plc, one of Europe's leading packaging companies manufacturing corrugated solutions for the retail, FMCG and industrial markets. He spent the last four years as Managing Director of the UK & Ireland packaging division and has extensive strategy, commercial, M&A and operational experience, gained in both the UK and in Europe. Gareth will replace Steve Crossley, who is leaving the Company and stepping down from the Board with immediate effect to pursue other interests. My view: That sort of statement does set the warning bells ringing very loudly especially as there was absolutely no hint of Steve Crossley's "unplanned" departure in the year end results RNS published just 8 weeks earlier. Had I have been an investor I would have very rapidly sought significant reassurance that all was well or otherwise: see my notes in red above "rules on the wall". I should also add that I steer away from companies that promised large dividends that are nowhere bear covered by FCF & also carry debt. Next Week: we have preliminary results for my favourite boring company WH Smith and I hope there is zero excitement and my boredom may continue. SMWH are up over 25% so far this year and I have to say have done me proud over the years. I also suspect we may see a trading update from Amino: AMO next week. Have a good weekend and as ever, happy investing. The Voyager RNS Log: Week Commencing 24/09/2017 Note: as ever nothing I write here is in any way a recommendation; well apart from the superb meze. Just view this as me meandering through my thought process concerning various regulatory announcements and sharing my views. Well having returned from my routine September visit to my favourite restaurants in Kyrenia; I just love authentic meze. However, it’s nice to get back behind the keyboard; and so refreshing not to even look at share prices over the last couple of weeks but just kept an eye on RNSs via a distinctly awful wifi and costly 3G. I have to say that Erdogan’s antics are likely to prevent me from flying via Istanbul again; can you believe four baggage x-rays, a compulsory change of plane and a body search with swab tests on my IT kit just to get back home; Erdogan seems a total paranoid madman. Anyway, a couple of RNSs to catch up on before I touch on this week’s events. Firstly: Tuesday 19/09/2017: Keyword Studios: KWS: Half Year Report and once again another very solid picture of growth emerges with adjusted profits up some 60% and adjusted eps up 55%. Note: the nature of the adjustment is integration expenses of EUR0.5m (H1 2016: EUR0.7m), share option charges of EUR0.4m (H1 2016: EUR0.3m), amortisation of intangibles of EUR1.2m (H1 2016: EUR0.6m) and foreign currency loss of EUR1.96m (H1 2016: EUR1.77m). Now adjustments are without doubt a pain in the bum for us private investors so what does the profits growth look like when stripping back these adjustments? Well, to my “fag packet calculation” it looks pretty blooming good. Has the share price got a touch ahead of itself? Well, that’s the perennial question with all growth stocks that prove popular with investors and see their share price appreciation in such a dynamic way. In my case KWS has appreciated about 4 to 5 fold since my original batches purchased and to mitigate a touch, especially as KWS was becoming a touch heavy in the portfolio, I sold some shares that covered my entire initial investments value thus leaving a very significant amount of stock riding “for free” within the folio. Hang on, “riding for free”, what a silly concept/quote that I remember seeing in share tip sheets in the late 90’s. Whatever does it mean? Whoopee, a profits warning but that won’t hurt me as they are riding for free! My View: I am very happy to continue to hold what seems to be an ever-increasing weighting in my portfolio even after the recent sale of my original investment in £. Incidentally, surprisingly I managed to sell that part holding at the top of the market; now that does not happen often! Is the share currently expensive? Well, difficult one to answer after such a great run but the measures I like, ROCE, CROCI, Free Cash Flow Conversion look so attractive as does the forecast growth rate in eps. Another aspect that attracts me is the huge addressable market where gaming companies outsource such services as those offered by KWS. Also, KWS appears to have a good reputation with its customers, an impressive client list and confidence in the continual expansion of the business. I personally see this one as a 3-5 year hold in which you have to acknowledge the risks associated with such an acquisitive company but worth “sensibly” tucking away in my opinion. Thursday 21/09/2017: Revolution Bars: RBG: RNS ruling from takeover Panel ruling that Ranimul, the parent company of Deltic the other bidder competing with Stonegate for the acquisition of RBG, must announce by 5 pm on 10/10/2017 if they intend to make an offer for RBG. Interesting times and I feel a rather happy investor. Thursday 21/09/2017: IG Design Group: IGR: RNS Re: Acquisition of a leading Australian greetings card business: In the year to 30 June 2017 the business generated sales of AUD13.4m with an operating profit before tax of AUD2.9m. The total transaction and restructuring costs are estimated to be AUD0.6m (GBP0.4m) which will be treated as exceptional costs. While of negligible impact to underlying earnings in 2017/18 due to the timing of completion, the acquisition will be earnings accretive from the next financial year underpinned by synergies in sourcing, design and logistics net of amortization of intangible assets. My View: anybody who reads my various notes about IGR will no doubt already be aware that I consider this to be a well-managed business that has delivered in recent years. Is it expensive or not? Well, you may well know that I just don’t have much faith in easily manipulated PE values preferring to consider returns on capital invested whilst looking for an attractive entry point. In this case we have a decent CROCI and IGR nicely converts profits into cash. Overall I am happy to happily hold IGR which has doubled my original investment over the last 18 months. Dashboard from the excellent SharePad:  Monday 25/09/2017 to Wednesday 27/09/2017: only a few routing RNSs for stocks within the Whittler universe/portfolio. Thursday 28/09/2017: Air Partner AIR: Interim Results and to my eye a very good set of interims with the headlines shown below:  So with the numbers, all looks to be very encouraging as is the outlook statement: Outlook: The new financial year has started well and we are making good headway against our strategic objectives. Trading since the period end has remained solid. We enter the second half with continued confidence that our expectations for the remainder of the year will be met, whilst the final quarter of the financial year can be the most challenging. We have built a strong platform from which to continue to grow the business. Our long-term objective to create a more equal balance between our two divisions, Broking and Consulting & Training, will deliver higher quality and increasingly visible earnings to our shareholders and will further align us to the needs of our global customer base, enabling us to continue to provide exceptional service and value. One part to keep an eye on in the next update/results will be the progress with Clockwork research which has had a challenging first half since it’s recent acquisition by AIR: At the end of 2016, we acquired fatigue management consultancy, Clockwork Research. First half trading has been challenging, but with a good pipeline of projects we are confident in the longer-term prospects for the business. We have undertaken work to further strengthen this pipeline and leverage the Baines Simmons offering. An encouraging example of the cross selling opportunities that have arisen following acquisition, is that Clockwork Research is now carrying out work within the rotary sector with a Baines Simmons client. On the same day as the interims, AIR announced that it had paid £3m to acquire SafeSkys Limited: On 27 September 2017 Air Partner plc acquired the entire share capital of SafeSkys Limited for a total net of consideration of £3.0m, obtaining control of the company on that date. SafeSkys Limited is a leading environmental and air traffic control services provider to UK and international airports. The acquisition has been funded from the Group's cash resources. Due to the proximity of the transaction to the reporting date, the purchase price allocation accounting has not been finalised. Details of the acquisition accounting will be provided in the annual report for the year ending 31 January 2018. The acquisition of SafeSkyes was itself the subject of a separate RNS on 28/09/2017: Air Partner plc ("Air Partner"), the global aviation services group, is pleased to announce the acquisition of SafeSkys Limited ("SafeSkys"), a leading Environmental and Air Traffic Control services provider to UK & International airports. The acquisition has been funded from Air Partner's existing cash resources, aligns to Air Partner's long-term strategy and objectives, and is expected to be earnings enhancing in its first full year of ownership. SafeSkys reported revenue of c. £1.8m for the year ended 31 July 2016. SafeSkys was founded in 1993 by Richard Barber, and over the past 24 years of his ownership, has grown to be recognised as a leading provider of Environmental and Air Traffic Control services working across 16 civilian and military airports in the UK, employing over 80 trained staff working every day onsite at the customer airport. Hopefully we will have some more details provided about this acquisition at the time of the finals and certainly AIR must be confident having paid £3m for a company with a current turnover of £1.8m; digging around at companies house I also gleaned some information from the latest accounts for 2016, SafeSkys have net assets of £637k which included £223k of cash. From what I can deduce from the SafeSkys site, they seem to operate almost as an agency style of operation so extrapolating the 80 staff to the £1.8m turnover can give a duff figure of salary estimate per employee.  Friday 29/09/2017: no RNS significant to stocks within the Whittler universe/portfolio.