|

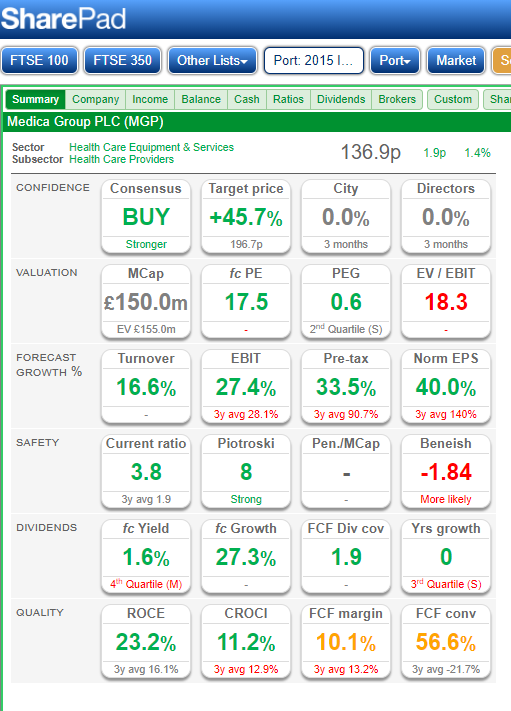

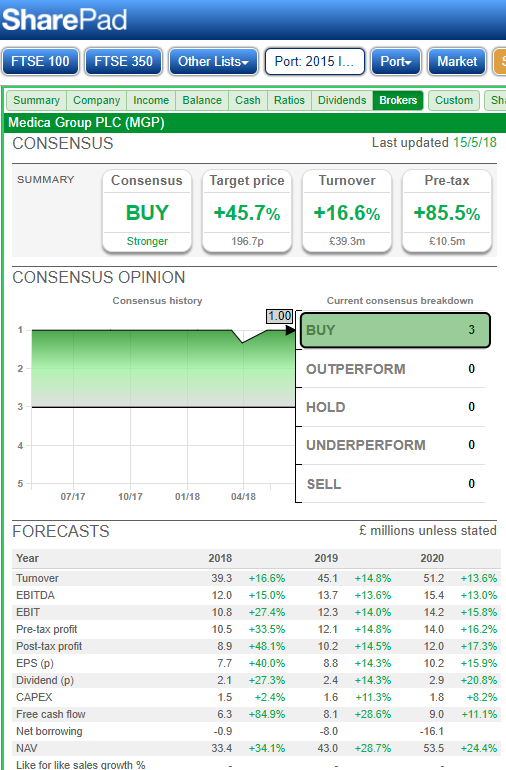

Voyager RNS Log WC 20/05/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Well, that’s the Royal wedding out of the way and I suspect that although it cost the country a fair bit to stage it probably brought in its own way, brought much more income to the UK. In reality, I can’t claim to be a royalist although I do appreciate the work that they do particularly in charitable areas. Still, I guess that many folks had a good day out in the sunshine enjoying a peaceful day and that can’t be bad. This week I have been doing a bit of an audit looking at the top 10 current holding ranked by value in the Voyager; it’s just a bit of an exercise really as I sometimes think that I should really slim down from the current 24 holdings to say 10 to 15 but that’s maybe work in progress. As for the top 10, the average return over the last 18-24 month period has very substantially exceeded the fairly challenging benchmarks I use (see earlier article about my approach to benchmarking my portfolio NOTE: it’s not benchmarking as in tracking but simply me saying “if you can’t beat great guys such as Terry Smith, Giles Hargreave, Gervais Williams then maybe it’s time to let them manage your investment). Indeed, it has truthfully been a very profitable period yet such fertile times don’t come around year after year and that’s the reason why I believe that it’s best to assess one's performance over at least a five year period. How long will these fertile times last? Well, I suspect that most investors found the going to be tougher during the last quarter of 2017/18 compared to earlier in that FY but, that’s investing. Of course, I have “RNS Managed” the portfolio by continually adding to the winners and jettisoning any positions that carried a risk to my capital e.g. on lesser news/profits warning, 95% of the time I simply kill the risk and sell. My reasoning for any decisions or actions that I carry out are all briefly discussed within the Voyager RNS Log. Many of those decisions arise from my “RNS fag-packet calculations” giving me an instant early view of short term to medium term prospects for a particular holding based on my assessment of the latest news: as an examples see last week’s RNS log for PMP and a week or so earlier the fag-packet on OTB. I intend to supplement this log in future by including the fag-packet as a regular feature; I may also produce a short dedicated article to introduce the fag-packet. Anyway, on to this week's Voyager: Monday 21/05/2018: No RNSs of significance to the Voyager Tuesday 22/05/2018: No RNSs of significance to the Voyager Wednesday 23/05/2018: Restaurant Group: RTN: Mkt Cap £630m: Trading Update RNS. Current trading Our strategic initiatives are driving improved performance in our Leisure business in a market in which like-for-like sales remain challenging. Like-for-like sales for the 20 weeks ended 20 May 2018 declined 4.3% and total sales declined 3.1%. Trading in the period was heavily impacted by the adverse weather and on an underlying basis, excluding the impact of snow, like-for-like sales were down 3.1%. In the first seven weeks of the second quarter like-for-like sales declined 1.8% as we began to lap the significant price investments made last year in order to re-establish our value credentials in our Leisure business. Our Pubs and Concessions businesses continue to outperform the market. Property During the first 20 weeks we have opened nine new units. The pipeline of new openings within our Pubs business has been further strengthened with the acquisition of four pubs from Ribble Valley Inns. Including these we now expect to open around 10 pubs this year. Strong progress has been made in our Concessions business with expansion into new travel hubs. We now expect to open at least 12 new concession sites this year. We have successfully exited a further five closed sites in 2018 bringing the number of sites exited to 26 out of 41 closed sites. Outlook We are comfortable with the performance in the first 20 weeks of the current financial year and expect to see further benefit from our strategic initiatives as the year progresses. We expect to deliver results for the full year in-line with current market expectations. My View: In terms of a recovery stock and the market reservation that things may not be gradually improving i.e if the decline were getting worse, there were no unpleasant shocks in the trading update. Also, reassuringly the comment “we expect to deliver results for the full year in-line with current market expectations”. The market certainly seemed to be quite taken by the results and the shares rose a few %. Personally, I feel the recovery will continue for some time yet and whilst it does, I will enjoy the 5%+ dividends which are well covered by free cash flow. In my view apart from utility stocks or pseudo utilities, FCF dividend cover is the measure investors should use for a sustainable dividend security. Conventional dividend cover of EPS/DPS can be a touch risky especially if the company is having to reinvest stacks of capital back into the business over a period of time. Note: I did a brief write up on RTN in the Voyager for week commencing 15/04/2018. Wednesday 23/05/2018: Medica Group: MGP: Mkt Cap £148m: AGM Statement RNS: Medica's Chairman, Roy Davis, will provide the following update at the AGM: 2018 has started well. Medica is performing in-line with the Board's expectations and recruitment of radiologists has continued to be strong. The anticipated full year 2018 results remain in line with the Board's expectations. My View: Well what does that mean? Let’s have a look at expectations as far as the brokers are concerned:  So, what I like about the statement is that firstly it tackles the worry some folk may have had about recruitment of radiologists; excellent, no problem there. Secondly, it reassures that with almost 5 months of the FY passed, the board anticipates results being within their expectations (we have to, of course, assume that the board's expectations are aligned to market expectations; why not just say in line with market expectations: always a bit frustrating). All in all, comfortable enough in my opinion for this stock that was hit overly hard in mid-January: see write up in last weeks voyager regarding my recent attraction and purchase of MGP. The market reacted well to the results initially up 5% but there still seems to be a touch of late in the day selling as possibly one large holder gradually exits their position.

Thursday 24/05/2018: No RNSs of significance to the Voyager Friday 25/05/2018: No RNSs of significance to the Voyager Whats on the horizon over the next week or into early June? I suspect we will hear trading updates from AMO, BOO, BOY & GAW. We also have finals from my favourite housebuilder, Telford, on 30/05/2018. Then the following day, 31/05/2018, finals from AIR whose results were delayed following the discovery of a touch of creative accounting; previously covered in this log. Have a great weekend and for sports lovers, there is plenty to entertain with Real Madrid v Liverpool, the various playoff finals and just to dampen the spirit, the test match. As ever, happy investing & hope to catch you next week.

0 Comments

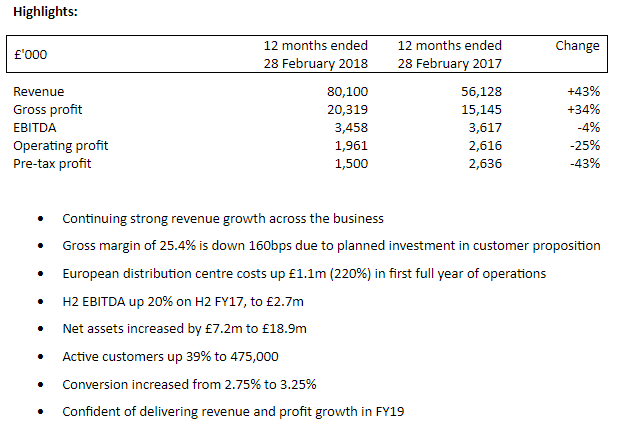

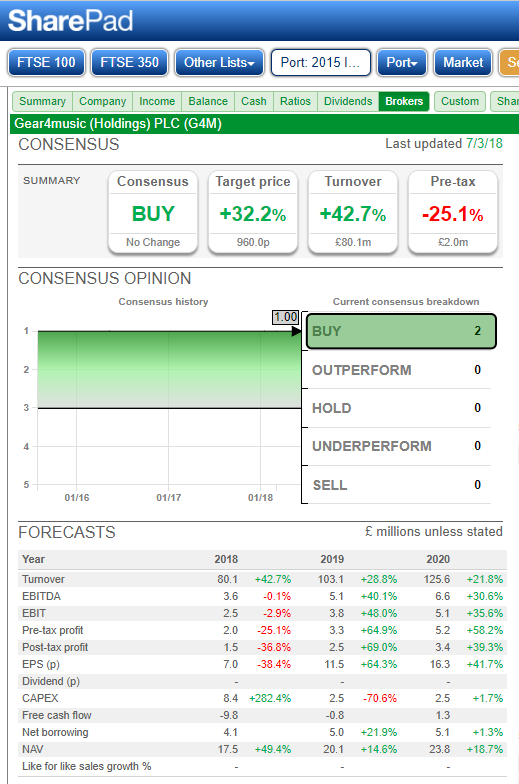

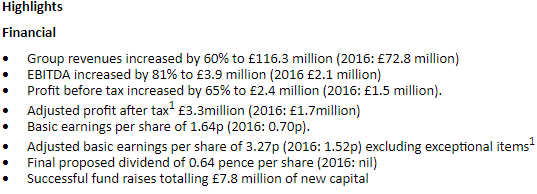

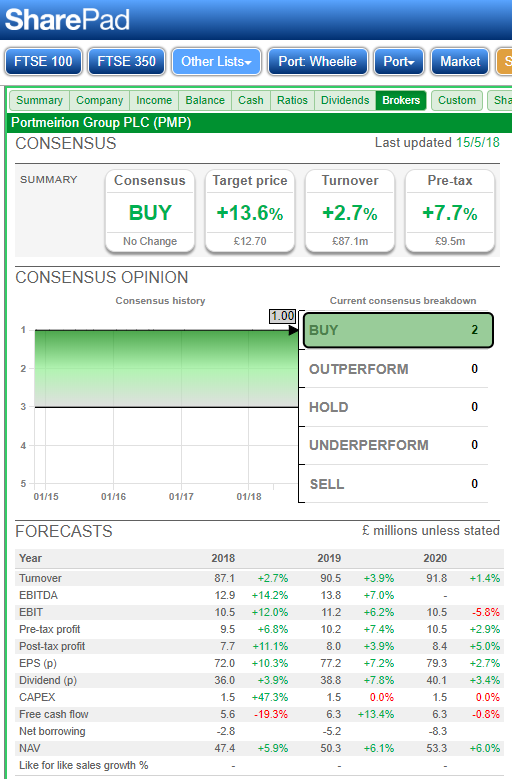

Voyager RNS Log WC 13/05/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. It’s a tough life being a sort of full-time private investor, you can simply finish work so very early and I mean really early. So, as well as enjoying time working in the gardens especially in this warmer weather, I have been entertained by the playoff competitions in the football league and whilst its entertaining especially for the neutral, it’s become a massive commercial exercise. Sadly I suppose that our national game is now owned by SKY/BT and rich overseas folk who become somewhat bored with lower profile pastimes. I have to say though what was so nice in watching the Villa games was the form of Jack Grealish. He is a lad who has really turned his life around after previously been a touch astray with social temptations. It’s just not easy for a youngster who becomes wealthy almost overnight and has bags of money, free time, away from home and hangers-on who take advantage of them. They really do need some social care and parental mentoring by the clubs that employ them. Then, of course, we have the parasitic agents who have zero interest in what is best for a young rising star and only wish to take their fee for arranging a move: modern football! Anyway, on to this week's Voyager: Monday 13/05/2018: Spectra Systems: SPSY: Market Cap £49m: G20 Central Bank begins Funding Sensor Development RNS: Spectra Systems Corporation, a leader in machine-readable high speed banknote authentication and brand protection technologies, announces that it was engaged on Friday to commence Phase I of a four-phase funded sensor development with a G20 central bank for use with polymer banknotes. The successful completion of all phases is expected to result in a long-term Sensor and Materials Supply Agreement commencing around 2022. Dr. Nabil Lawandy, Chief Executive Officer, stated: "We are excited that one of our polymer security features is on track for adoption by a G20 central bank. Once completed, this will be a decade or longer direct sale rather than a license and supply arrangement through a partner. We expect that this will firmly establish our capabilities and products for use in the growing polymer banknote segment of the market". My View: Reference to the new security feature was made in the finals RNS on the19th March 2018. Once again one of the major attractions this builds upon is in the next few years, post-2022, is the predictable licence income for a good number of years. At this stage, no quantification is given for future revenue enhancements. I know the business has some risks including the dominance of the President/CEO but I see he still owns just over 4% of the business. I doubt this one will become one of my top 10 holdings and I also doubt that the steady future income streams will either be picked up by or excite many investors. For now, I see SPSY as a steady business that may slowly appreciate in its share price over time; happy to stay on board and enjoy the ride & will try to pick up a few more on the next dip to 100p. Tuesday 15/05/2018: Gear4music: G4M: Market Cap £151m: Final Results RNS: A transformational year of growth and investment   Commenting on the results, Andrew Wass, Chief Executive Officer said: "This has been a transformational year of investment for Gear4music. During the year we raised an additional £4.2m of growth capital, our European distribution centres became fully operational, and we moved into our new Head Office. We accelerated investment in our employees, systems, marketing and customer proposition, to firmly establish ourselves as one of Europe's leading online retailers of musical instruments and music equipment. In my report last year, I explained that FY18 would be a period of targeted investment, and that would have short-term profitability implications. FY19 will be focused on achieving returns resulting from these investments, with the objective of delivering strong and sustainable revenue and profitability growth. As a result of the significant efforts of our team, and the investments we have made during FY18, we move into the new financial year with a market leading e-commerce platform, infrastructure and customer proposition. Whilst still early in the financial year, I am pleased to say that trading to date is in line with expectations and we are confident of achieving our objectives and hitting expectations for FY19." Outlook Whilst FY18 profitability reflects the investments made in our European operations and customer proposition to drive market share, we remain confident in our outlook for the new financial year. As we continue to implement our long-term growth strategy for FY19, we expect to see ongoing strong revenue growth, alongside increasing profits and cash generation. My View: If you look at the results and the consensus forecasts, they are pretty spot on; so although at first sight, a fall in profitability may have looked an “ouch” it actually was expected due to the expansion activity of the business. The G4M turnover in the UK continued to increase by 27% and the international revenue increased by an impressive 69%. Note in 2017 international sales accounted for 38% of revenue and for 2018 this had risen to 45% of revenue and to my mind should all being well, increase appreciably in 2019 as the European distribution centre kicks in further. Now, I should say that I originally bought G4M at the end of 2016 and again in early 2017 but took profits after a dizzy rise to over 800p. I then repurchased again when the share price cooled and to be clear, this is one of my special situation purchases and not the base Capital Return/FCF that is more usual in the Voyager. In fact, as I said last week, good capital return/FCF/increasing revenue/profit companies are becoming a touch harder to identify so, maybe the special situations will even become dominant in the next few months. Overall, I appreciate the high PE rating may not sit well with some yet anybody who regularly reads my text will know that I am not a big PE fan yet at the same time, I do recognise that a stock rated as highly as G4M could easily tumble on “below expectations” or even if the overall market cools hence I doubt it will become one of my top 10 holdings due to my risk management. For now, though, I am more than happy to continue to hold. Tuesday 15/05/2018: Xpediator: XPD: Market Cap £71m: Final Results RNS:  CEO Statement 2017 has been a transformative year for Xpediator and it has been a pleasure to be a part of the business's growth. We achieved many of our objectives in terms of the stock market listing and expanding the scale of the business but most importantly we are well placed to continue to grow. Demand for transportation services in our core markets of the UK and Eastern Europe is strong and is being further enhanced by the significant increase in e-commerce activities. These trends match the services we provide and this makes Xpediator well placed to take advantage of these opportunities. We have clear expansion plans for all three divisions and a pipeline of potential acquisitions, which we anticipate will further support the growth of the business. Outlook The markets in which we operate are in growth mode. Demand for road transportation is increasing across Europe, supported by economic stability together with a burgeoning e-commerce sector. Xpediator is well placed to capitalise on this positive market environment and has invested behind the existing business and in complementary acquisitions to capture an increasing share of the freight management market in Europe and further afield. We look forward to a further year of progress in 2018. My View: This company first came to my attention in February with a particularly encouraging trading update signalled rather positive progress with XPD which had only come to the AIM market in August 2017. Unfortunately, a couple of unforeseen events in life necessitated me taking some time out from investing and writing; these things happen. So, the opportunity in February 2018 passed me by but nevertheless, my interest was rekindled by the recent PI World Mellor presentation organised by that absolute angel Tamzin; honestly, Tamzin does some wonderful stuff for us PIs and I can’t let the moment pass without congratulating the excellent David Stredder who continually organised events bringing private investors and companies together. One watching the presentation I reminded myself “wake up you dozy bugger, you should have bought this a couple of months ago”. A quick calculation on the fag-packet to get a feel for organic growth versus acquisition growth: Acquisitions: Benfleet 22/10/2017 RNS: Year to 31/03/2017 Revenue £21.0m PAT £1.35m: Pro Rata: £3.5m & £0.22m Reg Fleet Express06/11/17 RNS: Year to 31/03/2017 Revenue £6.0m PAT £0.2m: Pro Rata: £1.0m & £0.04m We also have EMT but PAT figures are estimates based on recent acquisition cost/PAT ratio and I estimate for the 9 months of 2017 the PAT contribution was £0.75m So, lets roughly say acquisition accounted for extra PAT of £1.0m. Then that gives us a rough feel that acquisitions contribute 30% to PAT during the FY 2017 i.e most of the growth was organic at 70%. As I say, a fag-packet estimate but I don’t think it will be too far out and at least gives a feel for how the profits were routed from and the comfort of knowing that about very roughly 70% of profits are organic rather than via acquisition. Overall, the company looks quite a promising one and I bought a starter position @ 61p at the end of April 2018. I think that it’s had its gallop of late and suspect that it will now consolidate in price for a while now so that fairly small starter position will do for now. Tuesday 15/05/2018: Amino: AMO: Market Cap £150m: RNS Amino selected for 4K UHD service in Slovenia: Amino selected for pioneering 4K UHD service rollout in Slovenia Amino Technologies plc (LSE: AMO), the global provider of digital TV video solutions to network operators, is to support T-2, one of Slovenia's largest multi-service telecoms operators, in its launch of the country's first 4K UHD TV services. Working closely with T-2, Amino is deploying technology that will underpin a major service upgrade, which will expand T-2's service to include 4K UHD content and value-added Video on Demand and Subscription VOD services. My View: Sounds reasonable but as so often with such RNSs, no quantification is given in terms of what this could mean financially to the business. So, a quick search tells us that the population of Slovenia in 2016 was 2m and 0.6m of the population were connected to broadband; maybe this has increased to 0.7m by 2018. T-2 are one of the larger broadband providers and given that this is the first 4K UHD TV service in Slovenia, the fag packet would assume that it’s probably a nice little earner rather than a game changer in terms of revenue: I am happy to continue to hold. Wednesday 16/05/2018: No RNS relevant to the Voyager portfolio. Thursday 17/05/2018: Portmeirion: PMP: Market cap £121m: AGM Statement Trading Update RNS: "Total Group sales are up 15% for the four months ended 30 April 2018 relative to the same period last year, driven by strong growth in both ceramic and home fragrance product divisions. On a constant currency basis total Group sales are 20% ahead of last year. We are delighted with the start to the year, however due to the seasonal nature of our business and the importance of second half trading we continue to expect full year profit before tax to be in line with market expectations." My View: at first sight a simple “in line” update but let’s dig a little further: a quick rough calculation of what these numbers may actually mean come the end of the year. What we know is that PMP’s H2/H1 ratio is always biased towards H2 so I am fine with that being a comment in this RNS i.e. the usual H2 weighting fear does not apply. In fact, over the last four financial years, the finals have shown a year end turnover averaging 2.55 x the interims turnover and the range of those 4 years of Finals Revenue/Interims Revenue is 2.46 to 2.69; so that’s a fairly reliable historic guide ratio. The update tells us that the turnover is 15% ahead of the same first 4 months of the FY period last year; let’s forget constant currency stuff as we will come on to that a bit later. So, let’s estimate this years H1 turnover as H1 2017 of £33.1m x 1.15 = £38.0m Now apply the full year/H1 turnover average of 2.55 and we come to a fag-packet estimate for the fully FY of a turnover of £97m which appreciably exceeds the current analyst's expectations of turnover £87m. The average EBIT margin over the last 4 years has been 11.85% (it has not dramatically varied over the 4 years); then using this against my projected turnover gives an EBIT of 11.5 which is quite a bit ahead of year-end the consensus of 10.5; see below:  Suffice to say that I am sufficiently impressed to very significantly increase my holding early on the morning of the RNS. Note: if you apply the constant currency quote of 20%, then its even more impressive but I have stuck with the 15% figure. I expect analysts to revise their expectations upwards shortly; quite a decent business PMP with a decent yield of just over 3% and for stock rank fans, it comes in at an SR of 90. Also EV/EBIT of 10.8, ROCE 17.4%, CROCI 13.4 (I usually work on the last 3 years average with CROCI & this is a healthy 13.3%) and gross margin of 56% (I have of course used EBIT margin in the above estimate). There are just so many numbers/ratios there that I like. As for my fag-packet estimates, that’s all they are my rough estimates but based upon what we know of the first 4 months of the current FY. Notes on a New purchase: Medica: MGP: Mkt Cap: £148m What do they do: well they provide outsourced teleradiology services; so, that’s simple enough. Actually, it’s a simple enough idea but requiring specialist interpretation & that’s sometimes where things can slow down and hence the market space Medica is trying to fill by operating a team of leading UK based consultant radiologists to interpret imaging such as CT, MRI, nuclear medicine, mammography, CT Colonography and also offer an emergency service called Nighthawk with a 24/7 routine capability. Now given the pressure on NHS funding and targets for patient care, it seems an ideal opportunity for an occasional outsourcing service for such expert services particularly out of routine working hours. You simply don’t waste resources by having an excess of locally based expert waiting around either in normal or outside of hour just in case they are needed, you simply use IT to send the images to on-call experts for rapid determination. I don’t envisage it would ever replace the local consultant radiologist but merely supplement the service or peak-lop if you like. I do like the model and I rather like the financial numbers: The risks: I always like to consider the risks & downside, in fact, I spend quite a bit of time on risk & risk mitigation. Medica seems to have thought through the risks well and as much as they can, have reasonably mitigated the risks. Of course, the risk of NHS funding availability will forever be a risk. Looking at the numbers that attract me:   Director Talk From RNSs in past 4 months: The Mild Profits Warning 16/1/2018: Overall the Board expects the Company's performance to be slightly behind market expectations. The Outlook Statement from the finals on 12/03/2018: Looking forward to 2018, the year has started well, with trading in line with the Board's expectations. The prospects for new work from existing and new clients and the pipeline for recruiting radiologists in the new financial year continues to be strong which gives me confidence in our outlook for 2018. As the market evolves the Board is confident that, in the short- to medium-term, Medica will continue to grow revenues at a double-digit rate similar to that seen in 2017. Yet the market was not impressed and the share price continued to drift bottoming out at about 120p which is a 33% discount to its debut on the official list in March 2017. The market worry is probably centred around the availability of budget for its main customer, the NHS. I bought an initial holding this Monday at 131p as the shares were demonstrating some momentum recovery. As ever, this is just me sharing my thought process and should not be seen in any way as a recommendation to buy shares in Medica. Reading the tea leaves, sorry, I mean technical analysis:  Friday 18/05/2018: No RNS relevant to the Voyager portfolio.

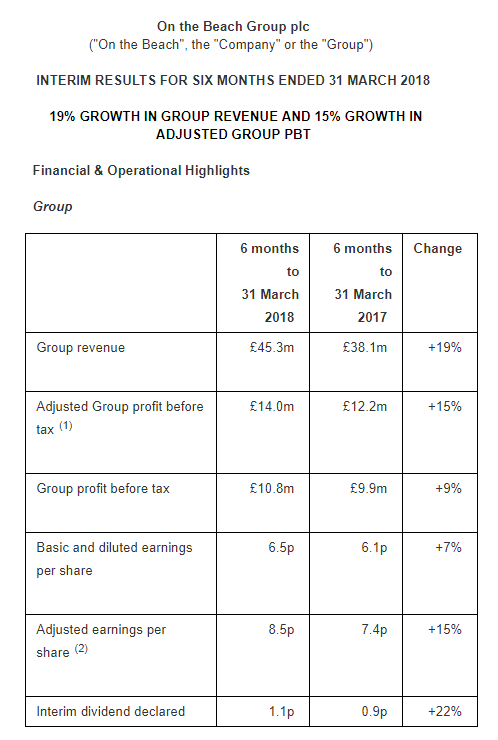

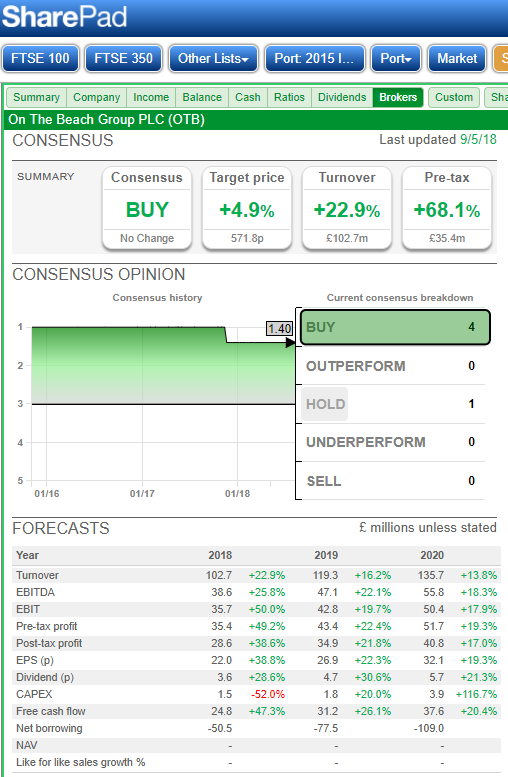

I should also say that an old friend from the past, Zytronic (ZYT) issued what was possibly an expected less than sparkling set of interims. I did write that back in February I sold the residual shares I held in ZYT after what I felt was a very mild profits warning “broadly in line with the equivalent period last year". I had also heavily top sliced this old favourite I had held for a while, that heavy top slice was taken when they had raced away towards the £6 mark. Now I tend to feel the share price will drift to maybe 360-380p when I might, but only might be tempted to buy back in but as ever with ZYT, the company is so reliant on a handful of customers. However, having said that, I do expect the company with it’s sometimes “lumpy” order book to pick up in the coming year: note they have stacks of cash on the books and currently an EV/EBIT of 8.3. Why don’t I quote PE ratios very much? Well anyone who reads my stuff will know that I am most definitely not a fan of the ubiquitous PE ratio; too easily manipulated by the CEO/CFO, nothing to do with their bonus payments of course, and takes no account of debt/cash on the books. Incidentally, there are a couple of expressions, among many that reside on my red flag list, that I am not that fond of in an RNS, they are: Broadly in line with expectations: I take this as at the lower end of expectations i.e a mild profits warning. In a trading update or at interims: Results will be weighted to H2. There are exceptions of course with the likes of Telford where there is strong contract/completion visibility and also companies whose profits are historically weighted to H2, see PMP above, but generally, H2 weighted really does up the risk of an earnings miss. Another classic is the CFO leaving with immediate effect; always one to make you sit up and think. Glad I Am Not There: SPRP: the ongoing car crash has now passed the 2-year mark; surely the directors are a touch worse than just simply accident prone. I don’t hold but I do feel for the many private investors who have remained loyal to SPRP. Sadly I feel that the directors are simply not fit for purpose as they drag their mistakes toolkit along with then each financial year. I did own these back in 2016 but sold for two reasons. Firstly my usual action on a profits warning is to say goodbye 95% of the time unless there was a compelling reason to stay & in SPRPs case director “bad luck” suggested simply sell. Secondly, the more I continued to occasionally dig a little since 2016, the more I got a picture of almost a masterclass of incompetence where the directors demonstrated an ongoing mastery of continually snatching failure from the jaws of success: IF IN DOUBT GET OUT. I did write about SPRP and my further concerns in both March and April of this year and to my mind, the red flags just kept appearing including as I said at the time the “oh dear!” with the finance director leaving with immediate effect. Having a quick scan of the results does to an extent explain the drawdown of £3m from the credit facility with HSBC at the end of March 2018. I have to ask within the 2017 numbers how did the company squander £11.3m from its £14.3m cash pile? Sadly, I honestly feel that far more than the FD need to go from this inept BOD: definitely not one for me as it just has bungling and unacceptable risk written all over it. As I have written about SPRP on many occasions, I feel justified in saying that for any investor there were to my mind, just so many red flags suggesting “time to head for the exit”. I have not held any position long or short in SPRP since April 2016. What may be coming up next week: at the moment there appear to be no scheduled announcements for stocks within the Voyager. Have a great weekend & as ever, Happy Investing! Voyager RNS Log WC 06/05/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. It's becoming increasingly difficult to find attractive companies that meet my cash flow requirements and are on offer at reasonable entry prices. Also, it’s getting a bit thinner on the ground in terms of special situations, those oh so rewarding companies where something may be changing that causes them to move up a gear or two. Is all of this a sign that overly stretched optimism may be priced into the market? There are certainly some very attractive companies on the market but in most cases, you really have to pay high rated prices to purchase them. I suppose if I were to be really brave then I could search much deeper below my £50m market capitalisation threshold but then the problem on the normal market size and thinness of the order book can so easily bite you in the bum particularly if bad news strikes and you decide to make a rush for the exit. On another financial front, I am challenging the council tax banding of my property. In honesty, this is something I should have done 18 years ago when I moved in but as ever, I guess I am just a touch to laidback. It’s a very nice property and I certainly don’t have any complaints on that score as it’s a few hundred years old and certainly has character but why it should be rated so much higher in council tax band terms, I really can't fathom out. Anyway, after first being refused by the powers in charge, I provided sufficient evidence for them to at least initiate a review. If that does not do the trick then I will take it to an appeal tribunal which I am familiar with having conducted one for my Laboratory which yielded over £1m return of overpaid council tax; maybe if I can get upwards of £10k back for overpayment over 18 years then that would be a result. Turning to a review of RNS for stocks within the voyager, last week was a very quiet week and this week seems only a touch more active. One to catch up on from last week is Games Workshop; bizarrely a stock I first identified as a buy some 15 months ago but my prejudice regarding the surreal practice of adults playing war games with toys, just kept me away from the early ride. Strange really, in that I can't stand video games yet went in heavily to KWS but I suppose seeing my two sons keep faith with the pastime these last 25 years gave me a better acceptance if not tolerance. Anyway, the GAW trading update was “ given the high operational gearing of the business, profits for 2017/18 to date are therefore slightly above expectations.”. The market did not react dramatically and I suppose some punters were again looking for “greater than expectations” buy so far, so good. Of course, the operational gearing is something to keep a close eye on at the first sign of change in fashion for the GAW products; probably a fair risk in my opinion. This week’s RNSs for the Voyager: Tuesday 08/05/2018: No RNS significant to the portfolio Wednesday 09/05/2018: No RNS significant to the portfolio Thursday 10/05/2018: ITV Mkt Cap: £6.5b: RNS 1st Qtr Trading Update: Carolyn McCall, ITV Chief Executive, said: "We have started the year well both on and off screen. Total external revenue increased 5%, driven by 11% growth in ITV Studios revenue and 41% growth in online revenue. ITV total advertising which includes NAR, online and sponsorship was up 3%. "Our strong viewing performance has continued, with total minutes viewed across the ITV Family up 4%, share of viewing up 6% and time spent viewing online on the ITV Hub up 31%. This reflects the strength and breadth of our schedule across our platforms. Highlights include strong performances from Coronation Street and Emmerdale, the successful return of Dancing on Ice and both Saturday Night Takeaway and our long-running drama Vera delivering their best series ever. And we have an exciting schedule for the rest of the year including Britain's Got Talent, the Football World Cup, the return of Love Island and our new period drama Vanity Fair, from the producers behind Victoria and Poldark. "ITV Studios has delivered a strong performance with organic revenue up 9%. We have a solid slate of new and returning programmes internationally for both broadcasters and OTT platforms with Unforgotten, The War of the Worlds, Snowpiercer, Good Witch, Suburra, The Voice, The Chase, Big Star's Little Star, Queer Eye for the Straight Guy, The Four and Forged in Fire. "While the economic environment remains uncertain online advertising continues to grow strongly. We expect ITV total advertising to be up 2% over the first half, but profits will reflect the timing of the Football World Cup. Over the full year we are on track to deliver double digit growth in online revenue and good organic revenue growth in ITV Studios. "The strategic refresh is progressing well with great input and engagement from ITV people across the business. I look forward to sharing an update at our interim results in July." My View: encouraging enough words from Carolyn McCall and revenue streams are all just about moving in the right direction. My simplistic view is that ITV has made a decent start with this first quarter and should be on target to meet expectations and I eagerly await their interims in July to see how profits are panning out. I will continue to hold but still just a little underwater with this one; great potential but will Mrs McCall be able to steer the cast of Coronation Street and the appalling Love Island to apparently safer waters to be possibly gobbled up by a predator? Thursday 10/05/2018: On The Beach: OTB:Market cap £710m: Interim Results RNS:   My View: Since the turn of the year, OTB has been a phenomenal performer with the share price possibly getting a touch beyond itself. Again applying my trusty fag packet (incidentally it’s decades since I smoked) I tend to think that they may well have to really stretch to meet the market expectations for the year. It’s just simply that my quick calculation suggests that in the most recent ½ years, that’s discreetly H1 & H2, their turnover has been in £m:

2016: 35.5, 35.8: Ratio H2/H1 = 1.01 2017: 38.1, 45.5: Ratio H2/H1 = 1.19 2018: 45.3, forecast 57.4 : Ratio H2/H1 required to meet expectations = 1.27 Note: the Sunshine Holidays acquisition (The Board believes that the acquisition will be earnings enhancing in the current financial year to 30 September 2017 because of the Group's ability to quickly leverage its modular technology platform) we were told was earnings enhancing from financial year ending September 2017 so you would expect to see a really significant effect in FY 2018 and that will be built into the consensus/expectation for a turnover of £102.7m. From my fag packet, see above, that looks a bit of a stretch to meet turnover expectations. Given the fact rather high valuation of the business, I just think that the lurking chance of a mild profits warning in the October 18 trading update (“at the lower end of expectations”) exposes me to too much downside. Now, without doubt, OTB is a quality business but I now suspect there may be a touch of short-term risk as an investment; it’s simply travelled so far in a short space of time and given the interims, may just be overstretched. It was also bought as a special situation whilst also having some attractive ROCE figures which are in truth a bit flattering/unreal as it is really an asset-light matching service; matching ticket flights from the various airlines with hotels. So as ever, relying on the trusty fag packet calculation, I sold on the morning of the RNS for a very decent profit of well over 60%. I will keep an eye on OTB and maybe buy back in at some time but for now, thanks for the ride. If in doubt, get out and protect your capital. Thursday 10/05/2018: XP Power: XPP: Market cap £668m: Acquisition RNS: Acquisition of Glassman High Voltage Inc. Glassman, based in New Jersey, USA, supplies the industrial and technology sectors with a range of standard, modified and custom high voltage, high power conversion products, which are generally used in applications involved in the ionization and acceleration of particles. Typical applications include semiconductor manufacturing equipment, vacuum/plasma processing, analytical instrumentation, medical diagnostics and test equipment. Glassman has the most comprehensive standard product portfolio in its sector, with the capabilities to also provide customer specific power solutions. In the fiscal year ended 31 December 2017, Glassman recorded sales in the US of US$17.3 million (£12.4 million), profit before tax of $2.9 million (£2.0 million) and had gross assets at the year end of $9.5 million (£6.8 million). The Acquisition also includes the purchase of Glassman’s small European sales business. Total consideration of US$44.5 million (£31.8 million) will be paid in cash on completion which is expected to be effective in May 2018. The Acquisition is on a debt and cash free basis and was funded with a US$45.0 million extension of the Group’s existing revolving credit facility. The Acquisition is expected to be enhancing to XP Power’s earnings in 2018*. My View: well it looks a decent acquisition, not massive relative to the current XPP turnover but overall quite attractive as Glassman made $2.9m PBT on a turnover of $17.3m. XPP are paying $44.5m and that suggests they are getting Glassman for about 15x PBT which in takeover terms, seems decent enough. The earlier acquisition of Comdel was at about 13x PBT & XPP itself trades at around 20x profits. The change in the net debut situation again seems quite manageable and the trusty fag packet suggests that after the acquisition debt won't be a show stopper at 0.7xEBITDA. Also, I reckon that EPS should be enhanced by 3 or 4 % this FY by Glassman. All in all, it looks a decent acquisition and that aligned with the good track record of XPP’s management give me confidence to maybe top up a little on the dips. Friday 09/05/2018: No RNS significant to the portfolio What’s on the horizon next week? Well, not a great deal; at the moment I can only see one of the Voyager stocks with a scheduled RNS; G4M year-end results on 15/05/18 but you never know, so let’s see. As ever, it pays to remember that no matter how diligent you may be, the next profits warning may just be around the corner. On that cheery note, may I wish you a great weekend and as ever, Happy Investing |

Archives

October 2019

Categories |

RSS Feed

RSS Feed