|

Voyager RNS Log Weeks Commencing 14/10 & 20/10 of 2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. In my last Voyager Log written two weeks ago, I commented that Mr Market had the jitters as displayed by the fall in all of the major LSE indices. Since that time, Mr Market has continued to fret and all the indices have declined further; more so here than on Wall Street. It just seemed so predictable to me back in the early summer that our EU/UK politicians were going to make a dog's dinner of the whole negotiation process. Oh, my apologies to any dogs that may read this log as I am sure you have far more sense than our glorious political leaders on both sides of the channel. Currently, I am feeling fairly vindicated in moving heavily into cash over the last five months. I still retain some attractive stocks and just like fellow investors holdings, these have declined a touch as the overall jitters continue. However, any bottom line decline is not that painful as it is heavily cushioned by the cash under the mattress. That cash will be used and gradually reinvested once the imbeciles settle down and agree on a way forward for the UK. However, with the world of the private investor, there is always something on the radar that may cause turbulence and with that in mind, I wonder how much longer the ridiculous single currency of the EU will last for. Something to look forward to I suspect. I repeat myself time and again; yes, ok, no need to agree! Firstly investing is a long game, it’s not a race. It does not matter unless you are selling of course, what your portfolio’s performance was yesterday, last week, last month, this year etc: what matters is you return over three or five years. Secondly, yes boring again, the application of risk management to one’s portfolio and by this, I mean having a risk management plan to protect your capital. Again on social media, I see that many folks are licking their wounds as their profits decline. If you invested at the top of the market then my sympathies, it happens: stocks go up as well as down. On the other hand, if you have less profits now than you had a few weeks ago, take comfort from the profits you have accumulated in the last 3,4,5 years of this friendly bull market: I suspect that overall most investors have done very well over the medium term. During turbulent times like we have been experiencing since the start of October, newsflow from companies is almost irrelevant in that even good news is insufficient to halt the gradual slump in stock prices. In fact, in terms of newsflow, it’s been rather light for the Voyager and this is down to having a reduced number of positions plus simply very few RNSs appearing. Oh, I should say that all my spread bets have now been closed for a couple of months: in my view, open spread bets at the moment are really too much of a gamble. Sometimes I tend to think that the words of the song Private Investigations, written by the excellent Mark Knopfler, sums up the logic of our friend Mr Market: well any excuse will do for me to play a few tunes by Dire Straits, the lyrics: It's a mystery to me, the game commences for the usual fee plus expenses, confidential information…….. I go checking out the reports, digging up the dirt, you get to meet all sorts in this line of work. Treachery and treason there's always an excuse for it and when I find the reason I still can't get used to it….. Now for a quick look at the few RNSs relevant to the voyager over the last two weeks: I won’t go into the usual detail as anything apart from a premium takeover bid causes a stocks price to decline at the moment. So, more of a summary note plus a few observations on some stocks that have been jettisoned from the Voyager in recent months as profits or an occasional slight loss taken: RNS newsflow from stocks currently within the Voyager: Tuesday 16/10/2018: IG Design Group: IGR: Mkt Cap £430m: RNS Trading Update: My View: a very sound update from what I consider to be quite an exceptional, high-quality business run by competent managers capable of communicating openly with investors. The trading update reads very positively with progress in all geographical areas and branches of the business. The big acquisition of Impact Innovations is performing well and I suspect will perform even better now it’s in the IGR stable. Overall, currently IGR is performing in line with management expectations but I have a sense that they will have an outturn at the top end of those expectations. I am happy to continue and touch away just a smidgen more of share price weakness. Thursday 18/10/2018: Games Workshop: GAW: Mkt Cap £1010m: RNS Trading Update: Following on from the Group's update in September, trading to 7 October 2018 has continued well. Compared to the same period in the prior year, sales are ahead and profits are at a similar level to the prior year. However, the Board remains aware that there are some uncertainties in the trading periods ahead for the rest of the 2018/19 financial year. A further update will be given as appropriate. My View: well according to my fag packet calculations when comparing actual to broker expectations, GAW is performing a touch ahead of expectations: the broker consensus was for a slight decline. Ok, so far so good, but then Mr Market frets about the “uncertainties” comment yet two things here: firstly that style of comment is now almost commonplace in company RNSs as the country struggles with the Brexit plague and secondly it’s the very same comment that GAW included in a trading update back in July 2017 yet Mr market worries!! Even worse still, I got a web copy of an article published by a journal that people actually pay for saying that the trading update was an unscheduled one; what utter nonsense as anybody who reads RNSs will appreciate. Do you own research and by all means test your thoughts with other respected investors but don’t blindly follow the shoddy work of journalists. Well after that little rant, I am more than happy to continue to hold. Monday22/10/2018: D4t4 Solutions: D4t4: Mkt cap £77m: RNS Trading Update Briefly: Adjusted profit is expected to be comfortably in line with management expectations & also confirmation of a strong cash position. My View: yes indeed a sound update and even Mr Market is his mean mood grudgingly let the shares rise a few %. My current batch of D4t4 was bought at 118p and despite a decent appreciation, I am happy to continue to hold as the valuation does not look overstretched and the returns on capital attractive. A few brief thoughts on stocks I have sold in recent months and NO LONGER HOLD who have issued RNSs recently: Softcat: SCT: which I sold at 846p as part of my derisking exercise, issued a reasonable trading update but with a note of caution: the shares are now at 670p. Good company and one to maybe return to later. Tristel: TSTL: a stock that had been very kind to me and my final batch was sold at 275p again during my Brexit risk management plan. TSTL issued final results which looked reasonably decent but lacked the USA market penetration evidence and the shares duly fell back to 210p: they were at 340p at the end of June. Again a very nice business but maybe a touch overly generous in terms of management rewards; silly me, I thought the directors were happy to simply work hard for a decent salary! Sadly and so many companies are doing this, we have adjustments for share-based payments. Once you consider share-based payments as simple remuneration, the PBT for Tristel is actually flat year-on-year and not the +15% adjusted claimed. Where did the 15% go, yes, to the directors/staff as remuneration which is simply a true cost to the business! RWS issued a confident trading update with revenues driven by that exciting acquisition of Moravia back in November 2017. I think I was right to sell at the time of their indigestion RNS at the end of April but maybe I should have bought back in when things improved. A quality business worth keeping on my watch list. Zytronic: ZYT: issued a run of the mill profits warning. Unfortunate but not totally unexpected from this rather nice well-managed business. I had held ZYT for a long period but the final significant batch left the Voyager last October when the share price became a touch overheated for my liking at 580p. Again a lovely little niche business but with an over-reliance on a small number of customers and difficult to forecast (potentially lumpy) sales. Patisserie Holdings: CAKE: well the snippets of news keep emerging and the extent of the fiddling may even go deeper as we now hear of nondisclosed share awards to directors. I won't comment further other than to say I am so glad I followed my gut instinct back in September 2017 when after visiting Patisserie Valerie I asked myself “so, where are all of these supposed customers; why aren’t they crowding out this near empty shop”? As ever, I sincerely hope current holders have something when the shares come back from suspension. Air Partner: AIR: issued interim results which looked fairly ok but after making some decent profits on AIR in the past, I just can’t get excited about a firm that loses some hefty invoices and seems to have systematically covered it up in their accounts for a few years: not for me, why take the risk? Finally, on an ex-holding XPD sold at 78p taking profits in August again as part of my Brexit risk management, the share price has during October fallen by some 40% yet no worrying RNS; strange times! A bargain now or further to fall? As Mark Knopfler of Dire Straits would sing: It's a mystery to me, the game commences……… I hope these notes encourage a few investors without an investment management plan/risk management strategy that just maybe having one is worthwhile. Things will every so often jump up and threaten your wealth on the markets; you can’t change that, it will always happen. Something you can do is be prepared by having a carefully thought out plan that you can execute in a cool collected fashion if required and believe me, every few years it will be required. Well, that’s it for this week except to say I have made one very significant purchase and a few little top-ups to current holdings. The significant purchase was some lazy money for the IPO of Smithson which gives me some global exposure within an IT to what in Terry’s terms are smaller and mid-cap global companies; in my world, they are fairly significant market cap companies. This weekend, despite industrial action on some trains, I am heading down to London for the Hatters game against AFC Wimbledon; hopefully, I will arrive in London early enough to make an interesting day of it. Whatever you are doing, have a good weekend as we turn the clocks back; never a good feeling is it! As ever, happy investing!

0 Comments

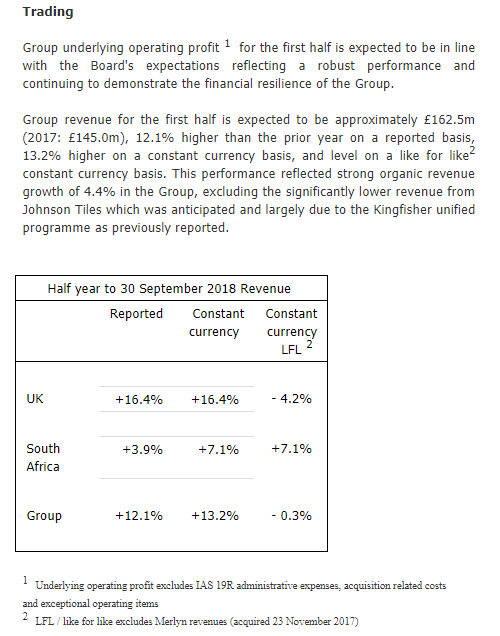

Voyager RNS Log Weeks Commencing 06/10/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Well, Mr Market has certainly got the jitters these last couple of weeks and can any investor genuinely be surprised as we head towards Brexit with so many uncertainties and remember Mr Market does not care too much for uncertainty. Since it’s high point in mid-May 2018, the FTSE100, FTSE250 and FTSE All Share are all off by around -11% with a similar story on the AIM100 down by -14% in just a few days with the FTSE AIM All-Share down by -12% since the start of October. Now I note that a fair number of investors on social media are posting how dreadful the market has been this October with losses of x%. What I always say is that your performance over 1 day, 1 week, 1 month is of little relevance and will almost be forgotten in a year or so from now. Performance needs to be measured over to my mind, a minimum of 3 years and I suspect that many private investors feeling a little pain at the moment will have done very well indeed over the last 3 or 5 years: it’s a long game, not a sprint. I would suggest that investors don’t thrash themselves over performance so far this October; it’s investing and these things happen! Any regular readers of the Voyager will know that from early summer I have been derisking my portfolio and moving more and more into cash at least until this Brexit debacle reaches a conclusion with some visibility on the way ahead; currently I am about two thirds in cash, that’s the highest cash position since the dark days of the 2008 financial crisis. Now, I am not saying that we are about to hit another massive drop as in 2000 or 2008 but rather saying that having invested through those tough periods, that I appreciate the security of cash until the storm has passed. Incidentally, I have been writing about the gathering storm clouds since early summer and I have been banking some very decent profits rather than take unnecessary risk. The storm that has arrived whilst it‘s having an adverse impact on the smaller number of stocks that I hold but this is greatly buffered by the cash pile. For what it’s worth, I see this current drop as more of a combined wobble coupled in the UK with Brexit worries some of which will pass when we have an agreement with Brussels regarding the terms of our departure. Uncertainty is never a good thing for the markets and we are currently being hit by Brexit worries. I am not about to do a Tim Martin style rant or defend the views of either camp but rather comment on my sadness in that our politicians have strived to cock things up right from the fake-news of the Brexit campaigning to the plans for departure. To ask the public to vote on such a complex issue back in 2016 was to my mind simply political abdication for short-term party gain. If the voting public makes a regrettable mistake in a normal election, then we only live with the consequences for a few years. With this vote, we live with the uncertain consequences for generations to come. Just my view but any referendum much more complex than “red sauce or brown sauce on your sausage sandwich” is a just too complex for folk to anywhere near handle. Yet here we are and as investors are confronted with such uncertainty, I would suggest it wise to have a plan other than bury your head in the sand: a plan that may review the situation and maybe take no action is a plan but to simply not have a plan is not that wise. My approach, when faced with this type of uncertainty, is to derisk, head for cash and then try to take advantage of a future market upturn. Profits have been very good in the last few years and indeed 2018 whilst not been stunning, has been fair. So, my approach is as ever to take some profits, reduce exposure in uncertain times and protect your capital. Currently, the Voyager carries only a relatively small valuation of stocks and certainly the lowest percentage for quite a number of years. Myself, I just don’t buy into this outdated argument of avoiding dealing costs by simply holding. That argument may have been true 25 years ago when dealing charges were so high but these days that are almost insignificant. A simple truth of investing is to ride the wave when it's in your favour but simply don’t stick around and be greedy when the wave changes direction. So at the moment I will sit on the cash pile as it were, and wait for the shakeout to play out before I go bargain buying. I do suspect that many relatively new private investors, let's say those from 2010 onwards are feeling a touch wobbled at the moment having experienced a run of fairly fruitful years until 2018 but this is the normal world on investing. We can't expect outperformance every year; this is simply business as usual. Well, that’s enough joy, let's take a look at what's been going on with the Voyager and its such a shrunken Voyager in terms of positions held that I may well also look at some previous holdings that were jettisoned over the past year. Monday 08/10/2018: Bioventix: BVXP: Market Cap £155m: Final Results  My View: the results in terms of how the company has performed looked absolutely fine; so all good or indeed very good for the year ended. However, I did in early September have this nagging doubt in my mind due to the company not issuing a trading update with possibly a teasing paragraph or two on the troponin project with Siemens. The comment in the results on this project was a little reserved and as I always bang on about risk, I halved my position in BVXP @ £31 which means that my residual holding, rather like that in KWS, is now riding for free. I really do like BVXP but just feel that that degree of uncertainty will be a handbrake on the share price in the coming weeks and as I have written before, we have enough uncertainty around anyway. If promising news follows regarding troponin then I can always buy further shares and enjoy a less risky ride. Monday 08/10/2018: XP Power: XPP: Mkt Cap £550m: Trading Update: A couple of lines from the TU Order intake for the nine months ended 30 September 2018 was robust at £153.3 million (2017: £137.5 million) which was 11% higher than the prior year on a reported basis. In constant currency this was an increase of 18%. On a “like for like” basis, removing currency effects and the impact of the Comdel and Glassman acquisitions, order intake increased by 8%. Order intake remains healthy, although the rate of growth has moderated slightly during the period. Production volumes in China and Vietnam remain robust and we are encouraged by our design win pipeline and overall momentum across the business. The Board anticipates the Group’s performance for the full year will be in line with its current expectations as outlined at the time of the Group’s interim results on 30 July 2018. My View: XPP simply continues as a quality business with a decent enough in-line trading statement. Yet the market has the jitters and the price has continued to drift. It all seems solid enough to me and is simply out of favour in this nervous market. I will continue to hold. Wednesday 10/10/2018: Telford Homes: TEF: Mkt Cap £290m: Trading Update: It was a cautious update painting both some positives and some uncertainties and if anyone was shocked by what was said then goodness knows where they have been for the last few months. The positives were that Telfords houses in London are of the more affordable end of the market and should continue to sell. The more difficult end of the market, the higher priced houses are proving more difficult to sell. My View: Well, over recent months I have taken very good profits on housebuilders and TEF was my one remaining housebuilder stock but the TU although written very honestly, just leaves too much doubt for the immediate future. Regrettably, as Lord Sugar would say, Telford has been fired, I really like the business as I have written or bored readers within the past but that sentiment will not stop me from making the unemotional decision to sell and escaping with a small profit. Maybe I will return another day! On the day of this RNS I felt it a little odd that other housebuilders had held up fairly well on the day and was tempted to short a few. The other builders duly fell the following day. Thursday 11/10/2018: Norcros: NXR: Mkt Cap £162m: Trading Update  My View: to me this looks a sound enough update from NXR and as their strategy projects, the real growth comes from acquisitions with group LFL sales excluding the Merlyn acquisition down by a small amount -0.3%. If we do a quick “fag packet” estimation of this H1/H2 stretch we see the ratio as 2.05 which compares well to the same 2.05 ratio averaged over the last three years for H1/H2. The stock is on a very undemanding PE of 6.2 with a yield of 4.3%. Although I sold half of my NXR holding in the application of my derisking strategy in recent months, I am happy enough to hold the residual 50% in the Voyager; it’s been a boringly yet steadily profitable stock over the years. A few thoughts on stocks I once held that have issued RNS this week: Note I no longer have positions in these stocks but have covered them in some detail in the Voyager Log together with my reasoning for selling them at the time. Firstly Amino, AMO, who issued a profits warning on Monday 08/10/18. The reason I sold and reported my concern in the Voyager was the rather large H1/H2 stretch required to make their numbers for the year. To do this, simply take a look at historic H1/H2 ratios, then take into account any mitigating circumstances and ask yourself if the H2 gap can with reasonable confidence be closed. With AMO, which is a decent business, in my opinion, I decided that it was a stretch too far and sold. Secondly Patisserie Valerie, CAKE, where I had an almost surreal experience that day in Lincoln with queues at some other coffee shops yet hardly anybody in Patisserie Valerie: odd I thought, maybe just an anomaly as their reports suggest good customer numbers? After my acceptable but slightly expensive breakfast at Patisserie Valerie, I then moved on and had a couple of pre-match beers with a group of friends and their partners where we got onto the subject of Patisserie Valerie and surprise surprise, their experiences at outlets in other locations were similar to my own. I decided that all may not be as well as I would have hoped, I just did not feel comfortable and if I don’t feel comfortable I get out: a few days later sold all of my entire holding in CAKE for a 20% profit. Now I appreciate that this was not in-depth analysis and to be fair their accounts looked fine but often such observations can give you an indication of how well a business is doing. For example, the almost always empty Carpetright stores or Halfords a couple of years ago contrasting with the crowded “always have to queue” WH Smith travel shops: simple stuff but often of real value. For shareholders expecting a trading update at 7am on 10/10/2018, the black clouds began to form with a 7:30 am RNS which gave nothing at all in terms of current trading but simply said that he shares were to be suspended from AIM until some serious financial irregularities could be sorted. On a newscast the previous night there was a suggestion od a £20m black hole in the accounts. Further bad news was to follow during the day with a second RNS concerning a serious tax issue for one of the group companies. Then in the early afternoon of 11/10/18 another RNS saying “Without an immediate injection of capital, the Directors are of the view that there is no scope for the business to continue trading in its current form”. What happened to one of the attractions of Cake, the self-funding of the rollout of new shops? Also what a real slice of luck for some of the directors in selling over £20m worth of shares earlier in the year! I really do hope this “difficulty” is resolved soon; maybe Luke Johnson can sort something out and rescue the business and leave holders with something? A very sad position that I doubt anybody could have detected from the accounts. My commiserations to all involved, shareholders and staff alike; just glad I popped in for that pre-match breakfast, I simply felt uneasy after my on-site visit and talk with friends who had used PV: I got lucky; no skill involved at all. A quick look at another stock I sold due to an unusually high H1/H2 stretch being required to meet the market expectations; OTB. This stock and my reasoning was also covered in an earlier Voyager article back in May this year. When I looked at the H1 figures it told me that there was simply too much risk involved to remain as a holder as the H2 stretch was just too much. I sold at some distance above 560p. The market was slow to react but eventually did; hot UK summer etc and the shares fell to below 420p, a slow but steady decline of over 30%. Yet OTB were rather skilfull in managing market expectations slowly down from a turnover of £102.7m to £95.4 and sweetening the associated profits decline with a cut back in costs. Hence to my mind, derisking their likelihood of issuing a profits warning; that’s clever in my book! Then we have an RNS on 16/08/18 telling us that the profits will be broadly in line, a phrase which means slightly below, expectations. This was sweetened again with another snippet of news in the form of a tasty acquisition and the shares rose. Now I am not saying that OTB is a bad business, far from it, all I am saying is look closely at the newsflow from the business and do a fag packet calculation for yourself. If you do, you may find yourself way ahead of some of the analysts. Incidentally, I still reckon there may be a slight sting in the tail to come with OTB but I could be wrong. Well, that’s all for now. Have a good weekend and as ever, happy investing whilst remembering that it’s a long game and not a sprint. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed