|

Voyager RNS Log Weeks Commencing 04/11 & 11/11 of 2018, As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. A few thoughts on October/November 18: I just do not get fazed by such periods as I have simply been investing too long I guess; I have the scars and hopefully the bolted on wisdom having invested through the bear markets of 2001 & 2008 which taught me the value of moving heavily into cash. Having been through some tough periods in the past, I feel that’s its imperative that an investor has a plan, a strategy and when they see the cliff face looming they at least consider executing that plan rather than waiting until their toes are dangling over the cliff and acting in panic mode. All through 2018 we have had the Brexit virus looming and threatening to deliver massive uncertainty which as we all know is what the market hates. As I have been continually writing in this log during this year, I chose to execute that plan and place a high reliance on a very substantial cash position. In fact, the overall cash position in the Voyager is the highest it has been since the financial crisis of 2008. In both 2001 & 2008 global factors were at work, sadly this time around the threats are far less global and largely self-inflicted by the UK upon the UK. Am I right with this strategy? Well maybe, maybe not but it’s a thought-out strategy that sits there to be used in case it’s needed and it’s rather like a Fire Assessment for a hotel i.e. you don’t wait until the smoke alarms go off to develop a plan for evacuation and safety. One thing is for sure is that our politicians right from the start of the referendum campaigning to this very day, have presided over a total shambles acting with the dignity and honesty of a Chinese AIM-listed company. One final comment on being in or out of the market: fund managers have little choice other than to be in the market and use the slogan “it's about time in the market not timing the market”. On the other hand, hugely successful investors like Minervini may withdraw from the markets for a period of time when things just don’t look favourable. Anyway, a few thoughts on the man at the top of a company, the CEO and certain traits they may have that I dislike, traits that ring alarm bells. This Magical Person The CEO: One bias that has developed with me over the years is that if I have doubts about the CEO of a business then it’s best on balance to listen to those doubts and maybe just leave it alone. You have probably come across such individuals yourself; the ones that may display some of the following traits:

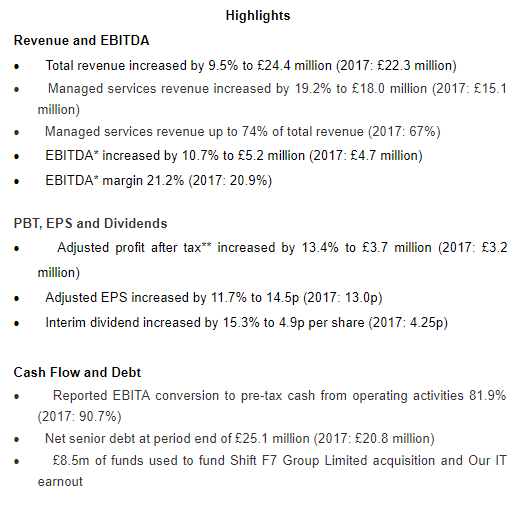

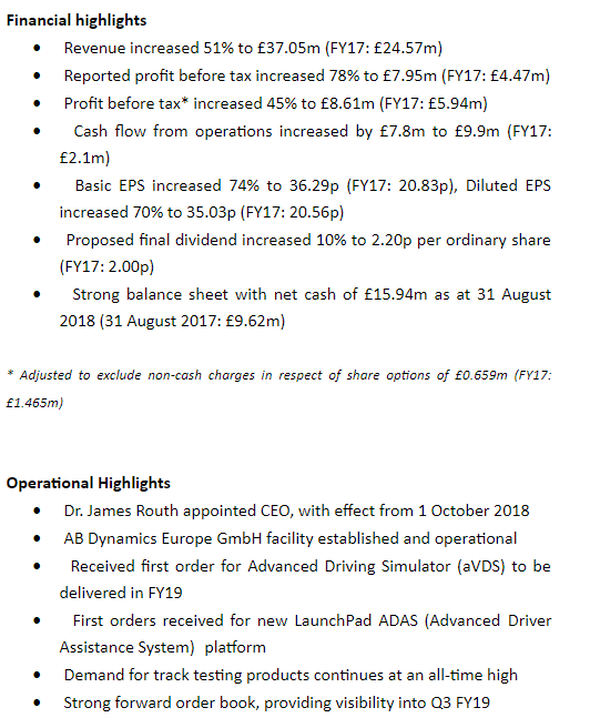

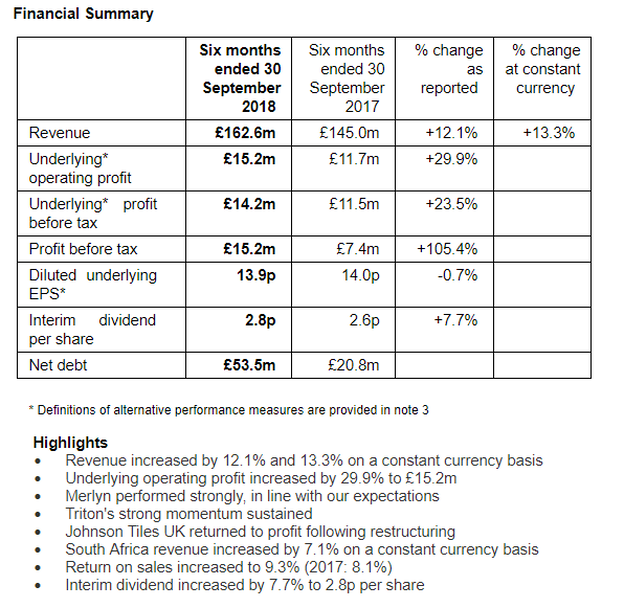

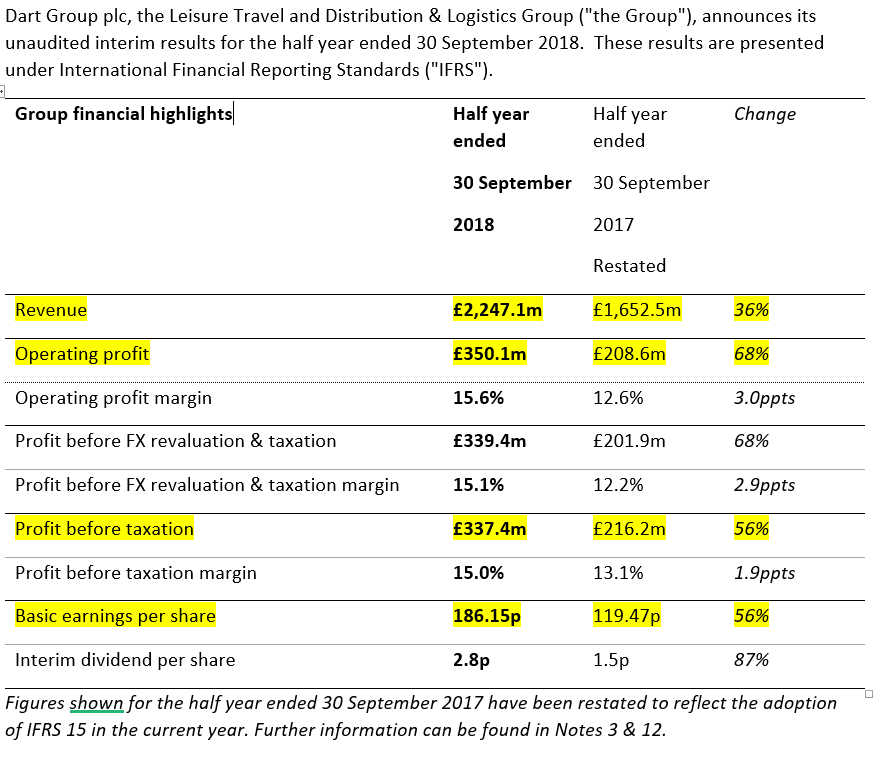

Although I don’t remotely claim to be a forensic accountant, I am after all a chemist by profession, I firmly believe that any investor who takes the time can dig around in the dirt to get a picture of what is really going on. In a good number of cases, if you take the time, you may well have a better picture of what’s going on with a stock than many of the brokers/analysts. Oh heck, why not, a few examples of companies that have exhibited some of the above traits in my opinion: ADT, CLLN, UTW, TRAK, TSCO, TCM, TSTL, CALL, VCP, VRS I should say that these are only a very brief example and I could actually produce a very long list to bore you with. Indeed, I have held a couple of those companies above. In fact, I made a very good profit on TSTL but sold when my fag packet told me that once the boys had been rewarding themselves and adjusting profits (sorry lads, share-based payments are remuneration in my book), profits look a touch flat. I did not own VCP but it was on the watch list. VCP alarmed me with the following in the Outlook statement from the CEO “I often hear non-shareholders worrying that they have "missed the boat" with Victoria - although I am at a total loss to understand why they would think that”. Indeed since that July statement, VCP has been down from its recent highs by as much as 50% in mid-October. The above are just some of the things I look out for in RNS or other communications by companies. Anyway, after a fairly quiet period, no RNS Log for three weeks as there has been very little to talk about, let’s have a look at what has been going on with Voyager stocks in recent days: Wednesday 07/11/2018: ITV: Mkt Cap £6bn: RNS Trading Update My View: finally lost patience with ITV after holding for quite some time and following this “dressed up” trading update, a little bit of digging and removing the cosmetics suggests that the ugly sister remains the ugly sister and maybe nobody will come along to buy her and take her out of her misery. Sold for a loss of 10%. Note: I never feel bad about taking a loss, especially one of 10% or less as part of the key to successful investing in my view is the protection of capital by jettisoning underperformers from the good spacecraft Voyager. Tuesday 13/11/2018: AdEPT Technology: ADT: Mkt Cap £88m: RNS Interim Results  My View: well the Poppycock EBITDA all looks impressive enough but that no surprise as Poppycock earnings are designed to impress, paint a potential ugly duckling as beautiful and just maybe mask what’s really going on underwater with our duck. So with my dislike of EBITDA claims and armed with the trusty fag packet I did dig a touch into the interim figures. Without boring you with the full conclusions of said fag packet, I am not overly impressed as I am left with the feeling that the true profits i.e after removing adjustments are only just sneaking up via the recent acquisitions which in themselves don’t appear that exciting and the pre-acquisition business is not doing what I reckon it should in order to comfortably make their full-year figures. Overall, for me, I get a whiff of more adjustments being needed to get anywhere near the full year expectations with Poppycock EBITDA in full flow. I may well be wrong but I sold at a 5% loss on my fairly recent purchase: again, if I don’t feel comfy with a stock, it’s cast out into outer space to drift. If I am wrong, I can always go back in again but rather suspect that I will listen to my reservations about cocky CEOs; indeed for that reason, it was a hesitant purchase in the first place. Wednesday 14/11/2018: AB Dynamics: ABDP: Mkt Cap £270m: RNS Final Results  Outlook Since its formation in 1982, Anthony Best Dynamics has gone through many changes to establish itself as a market leader in its targeted segments within the automotive R&D market. Our customers remain very active in introducing ever more complex ADAS equipment into their vehicles and in the development of semi- and fully-autonomous vehicles. Vehicle safety standards continue to evolve under Euro NCAP and NHTSA and their safety ratings are expected to continue to include more and more ADAS and crash avoidance systems, such as future Autonomous Emergency Braking and Autonomous Emergency Steering developments. Despite our very strong growth, order intake has continued to run ahead of sales and this has provided the Group with a healthy order book into our new financial year and, as usual, visibility into our third quarter. Against this pleasing backdrop, our progress continues to require ever greater investment in systems and our operational capability to ensure that we are fully capable of supporting current and future growth. In the coming year we expect to make further investment in new product development, marketing, service and support, our growing overseas footprint and, of course, our people, whose skills and energy remain so important to our future success. Inevitably this investment will provide some constraint to our operating margin, but the Board remains confident that, under the leadership of our new CEO, we are positioned to deliver a year of solid progress. My View: well nice to see relatively clean numbers and what appears a very good set of finals from one of my medium-term portfolio holdings, bought in mid-2016 and topped up since. The headline numbers are reported in almost real money as PBT, I say almost real as we have adjustments for those naughty little remuneration tricks; whoops, I mean share-based payments. Strangely this time around if you deduct share-based payments from this year and last years PBT calculations, which of course we really should do, rather than an increased PBT of 45% as published, you get a more meaningful figure of 79% which is simply outstanding. My fag-packet calculations also suggest that the lease adjusted ROCE has risen from 19.7% to about 22.5% & the EBIT margin at 23%; nice! Note: as the drag of capital expenditure reduces in the next couple of reporting years, I expect the ROCE to return to around the 30% level. The new facility at Bradford is now fully functional and demand for the product is high (implies that demand may well outstrip supply, what a lovely position); an outstanding business in a niche area; happy days! Incidentally, I have seen so much ill-informed crap written about ABDP via various sources including social media that it totally reinforces my fundamental belief that to have success in this private investing game you must cut out the noise. Simply study the figures and the RNS news flow and if you are minded to, talk to management. I have to admit that I took the opportunity to top up my holding of ABDP during the October market falls. Thursday 15/11/18: Norcros: NXR: Mkt Cap £176m: RNS Interim Results  Summary and outlook The Group has delivered a substantial increase in underlying operating profit in the six months to 30 September 2018 against the backdrop of a challenging trading environment in our key markets. This growth reflects the successful integration and performance of the recently acquired Merlyn business, the return to profitability of the Johnson Tiles UK business, the strong performance of our market leading Triton business and share gains in a number of our other brands. The robust performance in the first half continues to demonstrate the strength of our market positions, our leading brands and the financial resilience of our diversified business model. The Board remains confident that these attributes will continue to drive market outperformance and will enable the Group to make further progress in line with its expectations for the year to 31 March 2019. My View: A very good set of interims and yes, of course, the dreaded Brexit virus gets a cautionary mention. Anyway, as I say the results look good and NXR delivers a confident in line with expectation outlook for the remainder of the year. I should also make a mention of the pension deficit. In my mind, the worries about this deficit have been greatly overplayed by the market in recent years and that opinion I have offered in this log for the past few years. The scheme is a mature one with the average age of around 80 and as seen in these interims, the pension deficit aided by a 0.3% increase in the discount rate has fallen from £48.0m at 31 March 2018 to £28.8m at 30 September 2018. I will continue to hold NXR. Thursday 15/11/2018: Bodycote: BOY: Mkt Cap £1.5b; RNS Trading Update Summary and outlook in the Trading Update As anticipated, the pace of revenue growth will moderate in the last two months given the strong prior year comparator. Bodycote's outlook for 2018 remains unchanged. My View: a decent enough trading update for months 7 to 10 of the trading year. In the first 6 months of their financial year BOY had a turnover of £368.0m & months 7 to 10 was £243.5m giving a banked turnover of £611.5m leaving a gap of £115.5 to meet revenue expectation for the full year; fairly easily satisfied in my view. I am happy enough and will continue to hold. Thursday 15/11/2018: Dart Group: DTG: Mkt Cap£1.4b: RNS Interim Results   Outlook

With winter 2018/19 Leisure Travel bookings in line with expectations and notwithstanding the important post-Christmas booking period that is still to come, the Board expects current market expectations for the year ending 31 March 2019 to be met. Looking ahead, significant cost pressures such as fuel and other operating charges, plus the necessary continued investment in our products and operations including that required to retain and attract colleagues, are emerging headwinds. This, coupled with the overall uncertain UK economic outlook particularly related to Brexit and how it may impact on consumer spending, means we remain unclear how demand will develop in the medium term. However, our strategy for the long term remains consistent - to grow both our flight-only and package holiday products. On the assumption that the UK Government secures a pragmatic and balanced Brexit agreement with the EU, the outlook remains bright and we continue to have confidence in the resilience of both our Leisure Travel and Distribution & Logistics businesses. My View: well a fairly stunning set of half-year results as DTG become a really substantial player in air travel and package holidays. However, as good as these results are and with the company saying that they expect to meet full-year expectations, Mr Market predictably acted in slight panic mode latching onto talk of emerging headwinds & the routine mention of Brexit. So, lets cast back to the interims of 2017 when the company made similar comments “However, we are seeing the emergence of certain cost pressures as we continue to invest in our airport operations, colleagues and other related areas. Nevertheless, and despite the current uncertainty around the "Brexit " negotiations, we remain confident in the resilience of our Leisure Travel business, supported by our recent elevation to the UK's second largest Package Holiday Operator”. Essentially repeating most of what had been said a year ago i.e it’s usual cautious guidance and following the 2017 interims the share price appreciated by some 50% over the next 12 months. The company also mentions in these 2018 interims that they are investing in new aircraft and staff in order to continue their expansion; all suggests to me that the long-term future is rather bright for DTG. I will continue to hold DTG a stock that I first bought at just over 200p back in 2013. I still view the stock as a bargain at just over 800p but won't really know if my view is right or wrong until about a years time. Top-ups and new holdings: The following portfolio stocks have been topped up a touch in October/ early November: using just a little of the cash pile at what I considered to be bargain prices in the last three weeks: BVXP, KWS, PMP, DTG, ABDP, XPP & IGR (at below £5): I consider these small top-ups prices to be at rather attractive prices but the question is will there be more Brexit damage still to come? Only time will tell but it seemed reasonable to use a little of the cash pile whilst keeping a large chunk in reserve. New position: after such a good write up by Rhomboid on Twitter, Goodwin GDWN. I should say that I do see a difference between listening to the thoughts of a seasoned & respected investor and don’t consider this as noise. Leavers from the Voyager: LGEN, BKS, D4t4, SPSY & HSL: in all cases very decent profits were taken. Two stocks sold at very small losses: ITV & ADT: overall a very profitable effect on the bottom line delivered by the leavers. I did say early in the year that I thought the storm clouds were gathering and hence my move from the spring heavily into cash. Sadly, I rather feel that the degree of uncertainty thrust upon the UK by this “Brexit dogs-dinner” has the potential to turn into a fairly serious storm; we will see. I have to say that I just feel more comfortable holding a small number of stocks, currently standing at 12 stocks until we either move away from the Brexit cliff or start to bounce into recovery after falling over the edge of that cliff. Boringly as ever, I will say that it's been a brilliant run over recent years and at times like this it’s prudent to preserve profits and protect capital. Of course, having a relatively small number of stocks will reduce the frequency of the Voyager RNS log appearance and I would guess that until the walk along the cliff edge is negotiated, it will be more like monthly. Well, that’s it for this week, I will be back when there is something to report on and in the meantime will use my Voyager absence to add other parts to the StockWhittler site. Have a good weekend and as ever, Happy and risk-averse investing!

0 Comments

|

Archives

October 2019

Categories |

RSS Feed

RSS Feed