|

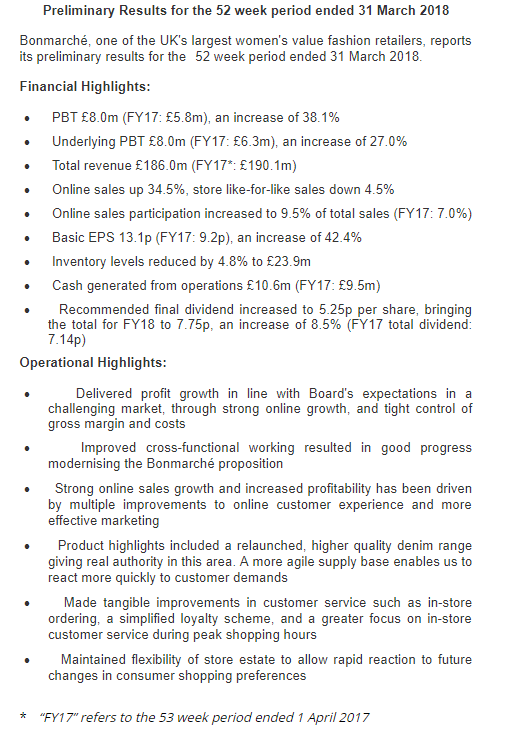

RNS Log For Shares Within Portfolio Voyager RNS Log WC 24/06/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Just having a look at my diary and I see that its almost a year now since I introduced the Voyager RNS log to the site; amazing how time flies by, frightening in a way. The log does take little bit of leg-work but it only really formalises and records the approach I have had for a good few years. All of the stocks are based upon either good cash-flow/returns on capital or what I deem to be special situations. Noise, including recommendations from magazines, tipsters etc is just about totally ignored with only a passing interest taken of broker recommendation upgrades/downgrades. The life-blood of the portfolio is raw RNS news pondered in reasonable detail and of course, my trusty fag-packet calculations. I was going through one of my archive files the other day, it was rather nostalgic to look at my print out sheets from CD Refs in 2001 calculating my expectations for VP at 85p, estimating potential upside if this scenario or that scenario came into play. I eventually bought VP at close to that price and they did very well for me but I ditched them as the financial crisis unfolded. Strange you know, as VP still looks a decent stock today even though its price is now over £10 per share. It’s just my view but I reckon that the keeping of notes where an investor records ones thought process for either buying/selling or indeed continuing to hold a stock, is invaluable: you learn from your mistakes as well as feeling good about your more positive outcomes. As investors, we will never get our investment decisions always perfectly right or indeed, perfectly timed. Without a doubt, each of us will suffer the occasional profits warning and also every so often, the consequences of possibly poor decision making; that’s all part of life as an investor. The important point is to learn from those mistakes and try to learn from them rather than perfecting that mistake and watching the outcome repeating itself again and again. As we move into deep summer, the RNS news flow and market activity dry up like a chalk stream in a drought. With that in mind, for the months of July and August, the Voyager will probably move to a monthly review returning to a weekly review in September with more newsflow and activity. In terms of my recent market activity, I have continued to heavily top slice or even close some positions over the last month as I get a feeling that the markets will tend to fall a touch more as Trump does his thing and we ponder over the sausage sandwich game, sorry, I mean Brexit. I am not one that takes notice of any market noise but I tend to sense these are loud claps of thunder and just maybe a real storm is brewing. So, with that in mind, it’s capital preservation time and I have now moved fairly significantly into a cash-rich position within the Voyager. Yes, I know that I may well miss a chance or two with some of my reduced positions but as the last few years have been so productive, I would rather play the risk management card a touch more whilst the sun is still shining. So, onto a fairly brief RNS Log. One catch up from last week: Tuesday 12/06/2018: Bonmarche:BON: Mkt Cap £59m: Year End Results:  Outlook: Trading since the beginning of the new financial year has been in line with the Board's expectations. The financial position of the business continues to be sound, with no net debt, and the robust balance sheet provides a stable platform for the future. We will continue to improve our proposition, through the implementation of a series of self-help initiatives. Whilst we anticipate that the market will remain difficult, we expect these ongoing improvements to make a real difference to customers, and we look forward, with confidence, to delivering further progress in the coming financial year. My View: The results were generally marginally higher than the consensus forecast and pleasingly the dividend generously increased by 8.5% to give a total of 7.75p for the year which going forward offers holders a very decent yield of over 7%. The market reacted well to the results which again showed an appreciable increase in online trading which although not massive at the moment, continues to increase nicely. I will continue to hold. This Week: Monday 25/06/2018: No RNS relevant to the Voyager Tuesday 26/06/2018: D4t4 Year End Results.  Outlook Going forward, our focus remains on the collection, management and analysis of data thereby assisting our clients to derive considerable value from their customer data and on delivering highly scalable, analytical platforms with our hybrid cloud analytic services. The first few months of the year have started in line with our plan and we continue to attract new partners, new opportunities and new clients. This leads us to be confident for the year ahead. As a group we have invested in our people, our systems and our products and we look forward to keeping you up to date on progress during what looks to be a very interesting and profitable year. My View: These appear a sound enough set of results and tend to reinforce my view that the business is possibly undervalued by Mr market. Initially, I guess some folk were spooked a little by the greatly increased level of trade debtors but to my view, in this case, it’s simply work possibly yet to be completed for which the customer will pay probably in H1 of 2018/19. Personally, I reckon the September trading update/November interims could make interesting reading. I will continue to hold what is a reasonably profitable position. Tuesday 26/06/2018: Ramsdens: RFX: Mkt Cap £54m: Series of mid-afternoon RNSs regarding director sales. I can’t say that I am overly impressed with the way RFX have conducted this trio of sales of significant numbers of shares: Peter Kenyon CEO, sold 500,000 shares which was about 30% of his holding. Now whilst I see that the CEO does not draw down a massive salary, about £170k, and I can understand the need for a little reward, my criticism is in the way that the sale was handled. It was probably done on block to an institutional investor but surely such a sale warranted some degree of explanation from the directors i.e. to meet institutional demand or whatever. No, sorry RFX, that does not impress me and you have destroyed my earlier confident stance and have left the portfolio for a small manageable loss. You can’t win them all and only a fool expects to win then all whilst I like to think a wise man simply says “hey this one did not work out” and moves on. It may well be that the share price could soon recover up to the 200p region but for me, the management were a touch naïve in the management of the series of sales; as Duncan from Dragon’s Den would say “I’m out”. However 24 hours later: after that afternoon RNS and my sale of RFX, it fell a few % more the following day and I have to admit, I could not resist the temptation of a long spread bet at 166p. Why a spread bet? Well, I certainly don’t have enough conviction to entrust the management of RFX with a brown envelope containing a few £k of my precious ISA pot. Wednesday 27/06/2018: No RNS relevant to the Voyager I really don’t know why I bother with the 6:30 am swim on a Wednesday as half of the pool is roped off for the youth swimming club: nothing wrong with that by the way. However, what I can’t understand is why some rather weak swimmers more interested in talking than swimming, just turn up on such a crowded day; makes a swim really difficult and the mile feels more like two miles. Still, I suppose it continually tests one’s tolerance to those oblivious to their surroundings. Thursday 28/06/2018: No RNS relevant to the Voyager : Friday 29/06/2018: No RNS relevant to the Voyager: yet I could not let Friday pass without reference to that almost unbelievable bungling management team at Sprue Aegis (SPRP). Not only have these clowns steered their calamity of a company from accident to accident and continually destroyed shareholder wealth: the shares have fallen 80% since early 2016, they now have changed the company name to Fire Angel Safety Technology. I have previously written a few times that historically a change of name does frequently not bode well for the companies future; I mean who really cares what a company is called? In this case, the management has displayed incredible naivety by adopting the TIDM (EPIC) of FA; what more can one say? Incidentally, I don’t hold a position either long or short in FA/SPRP but at 75p and a fall of 65% in five months, surely a company supplying such worthy products must have a chance even with Captain Calamity & his crew at the helm! Finally, a comment on Versarien (VRS): I don’t hold any VRS but being a scientist I am interested in the potential of the technology. Having said that, being an investor, I am very wary of the stock. There is a bull case as graphene may well prove to be a wonder material. However, the bear case really does put me off the stock with the CEO’s maybe ill-advised use of Twitter, the insignificant RNS’s (we had one recently that smacked of a deal with Trotters Independent Traders) and the warning bell of a mass bulletin board following of experts on the new science. I have simply been around too long and have seen so many similar technological Midas touches: turning softwood into hardwood, new battery technology wonders of the universe, bitcoin. I think the CEO of VRS would be well advised to limit the newsflow to significant milestones and cease to engage so much on social media. VRS is not one for me just yet. If it does take off then I will be happy to get on board for maybe a 40% gain of something rather than full ownership of a stock so heavily ramped on social media and bulletin boards. In a gold rush, the risk-averse guys who make the money are the merchants who sell the picks and shovels to the speculators. If VRS does take off, then there will be plenty of time to make really significant gains “picks & shovel” style rather than being a speculator in these early days. The Summer:

Well, time for me to take some holidays and enjoy the summer months plus of course the World Cup which this time around is providing some great entertainment. Do make sure you enjoy this lovely summer and hope to catch up with the Voyager again at the end of July holidays and general enjoyment permitting. Cheers for now.

0 Comments

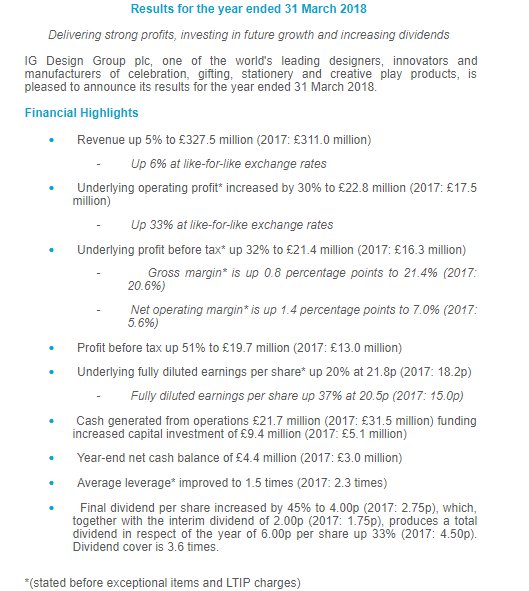

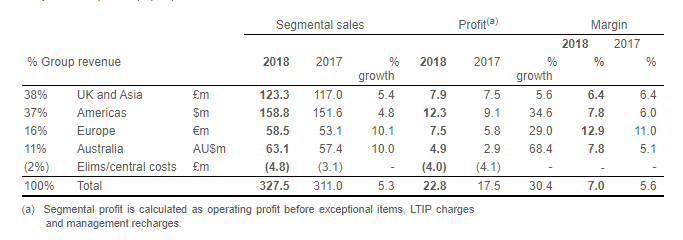

Voyager RNS Log WC 10/06/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Oh great excitement this week as we head towards the FIFA World Cup; such a fine organisation FIFA and according to the various guys who have run the organisation over recent years, operates without the slightest sniff of corruption. Call me a fool, but honesty and integrity lead me to admire such an organisation who for the 2022 venue choose Qatar, a country where the temperatures during the June and July of the tournament will be around 42C; simply ideal for football: in FIFA we trust! Yet sadly my own planning for the current world cup held in Russia the very cradle of democracy, hit the buffers on Tuesday evening when the Samsung TV issued a profits warning and suspended itself from trading. Never mind, in truth, the TV has had a fine run but never been exposed to the likes of the X-Factor or Love Island so I suppose that helped its longevity. Well, the new one, a rather nice big OLED job should be up and running for the Portugal/Spain Iberian battle on Friday evening so, we will be up and rolling with a modest supply of cold beer. Incidentally, I never would have thought a few years back that the Americans would be capable of brewing a decent beer as their “stolen” Budweiser and Miller are tasteless fizz; yet these days the smaller independent lads are brewing some incredibly good pale ale. Anyway, enough of this football and beer stuff and on with this week's log. Monday 11/06/2018: IG Design: IGR: Mkt Cap £294m: Full Year Results   Outlook Following the transformation of the Group over recent years, there is considerable scope for further growth across all aspects of the business. We remain focused on the profitable development of our business and confident that we have the team and agility to deliver further successes. We will continue to create value for all stakeholders through our strategy of developing diversified income streams across broad categories and markets, both organically and through well considered acquisitions. With a strong order book in place and a positive start to the new financial year, we are excited about the opportunities to deliver further growth in 2018/19. Note: video on results delay courtesy of Tamzin & PI World: Link www.piworld.co.uk/2018/06/11/ig-design-group-igr-full-year-results-2018/ My View: once again another very sound set of results from IGR that meet expectations and pleasingly contain a very positive outlook on the future growth of the business. I felt it worth including the table of Turnover, Profit and margin growth for 2018 v 2017 and it’s a credit to IGR in how they are making their geographic areas very efficient and delivering profit growth significantly ahead of revenue growth. If you get the chance, do have a look at the video on the link above where Paul Fineman, CEO of IGR, discusses the results and gives an insight into the forward strategy of the business. I see IGR as a very well managed business with the guys in charge being a safe pair of hands; ok, some might see the business as dull and unexciting and indeed it does not pay a massive dividend at around 1.4% but for me it simply ticks so many of the quality boxes I look for in my long-term holds. My purchase of IGR back in 2016 was not based on the Stock ranks system but nevertheless its pleasing to see that that worthy system gives IGR an SR of 88.  Monday 11/06/2018: Somero: SOM: Mkt Cap £224m: AGM Trading Update: Trading Update Somero is pleased with the broad contributions to the Company's growth at this early stage of the year and the positive market conditions we continue to see across our portfolio of territories. North America and Europe remain healthy markets with robust activity levels and we remain encouraged by the performance in China in the period as we continue to work on gaining traction in this significant market. We are similarly encouraged by solid activity levels in the Middle East, Latin America and our Rest of World territories and we see opportunities for growth in each of these markets. The Company continues to focus heavily on future growth initiatives and product development efforts, and has progressed in developing a solution for concrete leveling in the structural high-rise market segment. In summary, the Company feels comfortable with the positive trading environment across our footprint, and the growth opportunities visible in North America, Europe, China, Middle East, Latin America and our Rest of World territories. This constructive environment combined with solid margin performance and healthy operating cash flow generation means the Company's trading to date is ahead of the comparable prior year period and in-line with market expectations for the full year ending 31 December 2018. My View: An encouraging enough trading update from SOM which rather like IGR but of course in a totally different sector, is a well managed conservative business in my opinion.; so, yes, I am happy with that. Its also encouraging that SOM is very responsibly working on a three-year plan for the succession of the guys at the top of the business: I guess the identikit for the process would include qualities such as a) modest b) humble & c)realistic. I see the very credible Stock Ranks system also gives a boost of confidence with an SR of 93. Monday 11/06/2018: Keywords Studios: KWS: Mkt Cap £1160m: Acquisition of Blindlight: Acquisition of Blindlight Keywords goes to Hollywood Keywords Studios, the international technical services provider to the global video games industry, today announces that it has acquired Blindlight LLC ("Blindlight") for a total consideration of up to $10m, from the founder, Lev Chapelsky (the "Seller"). Founded in 2001 and based in Hollywood, California, Blindlight enjoys a leading position in the provision of Hollywood production services for the video games industry. The company works on behalf of game publishers and developers in procuring specialised talent and managing the entire production processes for the parts of games that benefit from Hollywood production resources. Blindlight's service disciplines include voiceover production, celebrity acquisition and rights management, game writing, music, sound design and motion capture. Blindlight works with top game producers around the world (including Bethesda, NCSoft, Sony Interactive Entertainment, and Ubisoft)making the creative expertise of Hollywood readily available for the video games industry. The addition of Blindlight to the Group will increase the value of the services provided by Keywords and contribute to making those services more accessible to a wider customer base. Blindlight achieved EBITDA of an average of $1m per annum over the three-year period to 31 December 2017. Under the terms of the acquisition Keywords is paying an initial $3.64m in cash and will issue 64,521 new ordinary shares in Keywords to the Seller on the first anniversary of the acquisition which will then be subject to orderly market provisions for a further 12 months. Deferred consideration of up to $4.8m will be payable to the Seller in cash depending on the performance of the business in the 12-month periods to the first and second anniversaries of the acquisition. Andrew Day, CEO of Keywords Studios commented: "Following our recent acquisition of music services companies, Cord Worldwide and Laced, we see excellent opportunities for Blindlight to bring these services to Los Angeles, as well as providing access to further opportunities for our downstream production services of translation and localised voice over." My View: the multiple paid by KWS for Blindlight appears reasonable and it will add a little to earnings on 2018 & 2019 plus, and I don’t know how significant this really is, gives them this Hollywood link. In truth, I ask myself what the hell am I doing here as I don’t either like or play video games. There again my conscience is rebalanced as I don’t wear mature ladies clothes but have some shares in Bonmarche (honestly, I don’t wear any ladies clothing but do confess to having bought men's shorts from BOO). So the question is are the shares expensive? Well, that’s a question for each investor to answer for themselves and a current PE of 42 may suggest initially that they are. However, a quick scan of the market for companies valued at over £1b suggests to me that they are not really overvalued as there are so few large companies with that historic & projected growth. Of course, my comment does include the proviso that the expected growth will continue and the track record and market position that KWS is carving suggest to me that it will continue to deliver. Monday 11/06/2018: Air Partner: AIR: Mkt Cap £52m: 2017 Finals at last: I will restrict the text here to just an overall impression of the results in bullet point form:

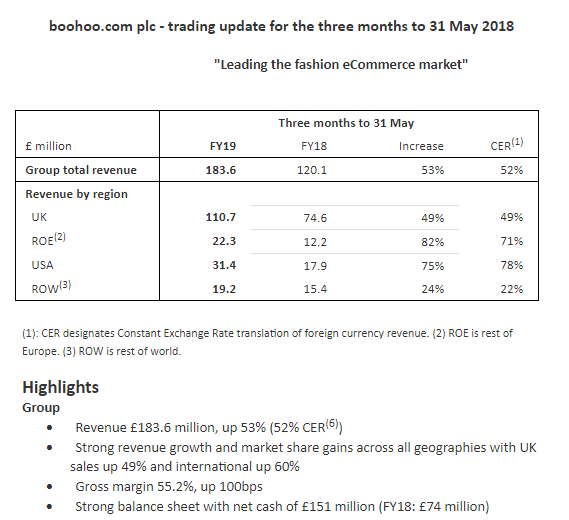

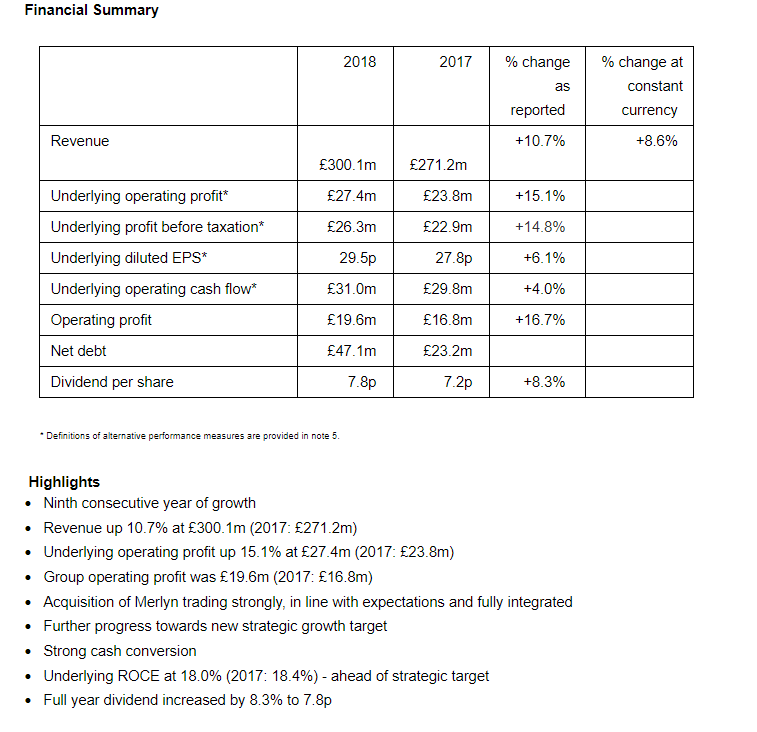

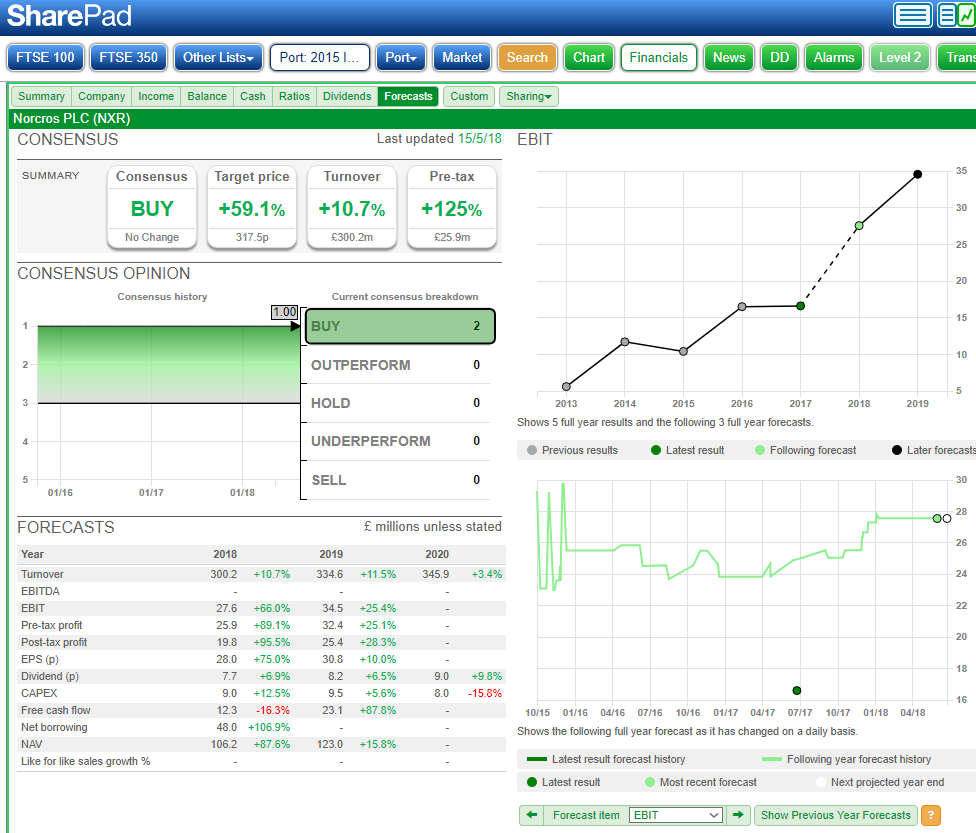

Tuesday 12/06/2018: Boohoo:BOO: Mkt Cap £2.53b: Trading Update:  Highlights Group Revenue £183.6 million, up 53% (52% CER(6)) Strong revenue growth and market share gains across all geographies with UK sales up 49% and international up 60% Gross margin 55.2%, up 100bps Strong balance sheet with net cash of £151 million (FY18: £74 million) boohoo Revenue £97.2 million, up 12% (10% CER) on last year's Q1 record growth Gross margin 52.0% (FY18: 53.9%). Retail gross margin 54.6%, down 170bps year on year, and improved progressively throughout the quarter, with an exit rate up year on year PrettyLittleThing Revenue £79.2 million up 158% (160% CER) Gross margin 58.7% up 490bps, driven by strong full-priced sales performance (retail gross margin 60.3% (FY18: 56.2%)) Nasty Gal Revenue £7.2 million up 149% (163% CER) Gross margin 58.9% (FY18: 69.9%), in line with FY18's exit rate and expectations My View: well it seems the excitement is in travelling to the trading update and then despite a decent update, the price eases back a touch: probably not unreasonable as the shares have had a very decent rally in recent weeks. The original core offering Boohoo is still growing nicely but is now rapidly being caught up in terms of turnover by Pretty Little Thing: Boohoo @ £97.2m and PLT @ £79.2m. Interestingly the combined revenue of Pretty Little Thing + Nasty Girl in this first quarter was almost half of the groups turnover and show an appreciably better gross margin (52% original BOO and 58.8% for PLT & NG). Overall a decent trading update with plenty of detail & guidance: I am happy to continue to hold. Wednesday 13/06/2018: Norcros: NXR: Mkt Cap £170m: Results for the year ended 31 March 2018 'Excellent progress towards our strategic objectives.'   My View: A decent enough set of results from NXR that meet expectations. The net debt has of course increased due to the acquisition during the year of Merlyn so, no shocks there. Whilst as I have written before, I don’t see the pension deficit as an issue that seems for some reason to be a touch misunderstood by the market, it’s pleasing to see it reduced from £62.7m in 2017 to £48m in 2018. As I have noted before the pension scheme is closed to new entrants and indeed 68%of those on pension average an age of 77: is there really a big risk there as time takes it’s toll on the population of claimants each year?

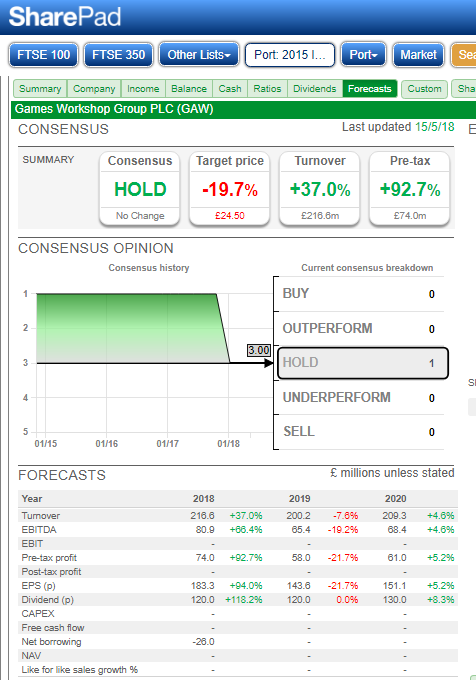

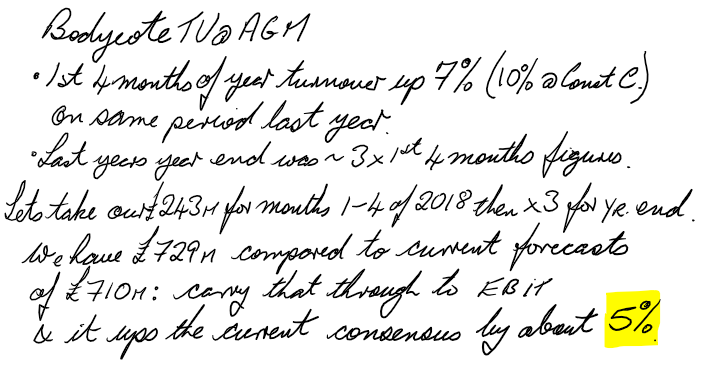

Norcros trades on a meagre PE valuation of 6.5, offers a yield of 4.2% that is very well covered (about 3x) by free cash flow and whilst it’s never going to be a stock to get the pulse racing, it has certainly earned its keep in the income portfolio. I am happy to continue to hold and rather think that at some time the market may well wake up to the attractions of NXR. Thursday 14/06/2018: AB Dynamics: ABDP: Mkt Cap £217m: Contract Win: First order for an advanced vehicle driving simulator (aVDS). The aVDS order, placed by a Chinese test house is valued at more than GBP2.0m with delivery expected in early 2019. Most of the value of the contract is expected to be recognised in the Company's next financial year commencing 1 September 2018. My View: Not material to this FY but as the note says, material to the next FY. Good to see a first sale and particularly good if other sales follow. Friday 15/06/2018: No RNS Relevant To The Voyager Folio: It’s been a busy week so a quiet day is very welcome/; an early finish by 09:30 beckons! Glad I Am Not There ( GINT): I should say these are not “clever dick” notes just simply an attempt to help investors learn from their mistakes and let's face it, we all make mistakes: the crucial point is what we learn from those mistakes. Well, predictably a mention has to go this week to Connect Group (CNCT) with a disastrous trading update that saw it’s share price collapse by 45% on the day. It was hardly a high expectation share within the market and happily one that I did not hold. Yet investors had plenty of time to look at the picture, heed the January 2018 profits warning followed by the continuously declining chart and reallocate their funds. I know it’s a case of each to their own but boringly I repeat that it's simply so crucial to protect capital by examining the downside in almost more detail than you may the upside. Another odd one and one I held profitably selling at the Stonegate hostile bid period is Revolution Bars (RBG) that issued an odd profits warning on Thursday 14/06/18 firstly blaming the cold snap in March and then blaming the unusually hot weather in May: “The adverse, wintery weather conditions in March combined with the unusually hot weather throughout May and early June, has curtailed typical late-night week-end trading”. The new CEO starts in a couple of weeks time and unfortunately for him, it looks like somebody has already chucked away the kitchen sink before he can get his hands on it; maybe he will find another kitchen sink to chuck thus clearing the decks with another warning? I feel there is the chance of a further profits warning here as the new CEO clears any semblance of bad news and also I can visualise the words “sales during a warm summer were impacted by the World Cup”; note this is the first world cup since RBG have been listed. Will another suitor be resisted by the new CEO I wonder? Whats On the horizon next week: I can’t see much apart from Bonmarche finals 19/06/18 also D4t4 but that’s pencilled in for the following week. Have a good weekend, catch you all next week. Happy investing; Update Note added 11/06/18 for Ramsdens RFX; did not have the time last week to complete my wandering fag-packet thoughts. On the chart below I have included a few notes on increasing ROCE, increasing EBIT margin and an excellent Net Debt progression that now stands at an impressive minus £12.7m. We also have the comfort of a proposed dividend yield of 3.3%. As ever, this is not investment advice and is just me sharing my thoughts on a stock. Although I am not a great lover of the PE ratio due to its susceptibility for massaging, the accounts seem reasonably clean and taking into consideration the cash, the PE falls from 12 to a very attractive 9.5. That all looks interesting and attractive but what does not look so bullish is the meagre broker's forecast for 2019 which has only been revised up by the slightest tad recently. A viewing of CEO’s Peter Kenyon’s discussion of the results, link below, paints a much more upbeat future than the brokers estimate projects and I rather think these expectations will be revised upwards as the year unfolds. Link to results video : www.brrmedia.co.uk/broadcasts/5b180e2df0b0144f05917d16/ramsdens-holdings-plc-full-year-results My scratchings of the chart:-  Voyager RNS Log WC 03/06/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Great news and on my birthday as well as I received a letter confirming my successful appeal against my council tax banding and a fairly substantial refund going back to 1999; happy days! Incidentally, my request for a re-evaluation was rejected at first but after more legwork, I was able to provide sufficient evidence for the process to begin. If anybody else is considering this approach then I suggest you give it a try & link guidance: https://www.moneysavingexpert.com/reclaim/council-tax-bands-change. For my birthday meal with family, I relaxed my low salt diet and had a very tasty if salty, Lamb Rogan Josh. Incidentally talking of salt, I remain convinced that if the general public reduced their salt intake on a daily basis to less than 6g then the profits of the pharmaceutical companies would decline as the blood pressure of the population reverted towards something more like 120/80. On a general note, often when I sell a share especially if I do so as I see something I don’t immediately like yet still feel the business if of decent quality, I will not be averse to buying back in either as a spread bet or as shares once I deem that the fall is complete and I see a bowl of recovery on the chart. Two very recent examples where I bought back in via spread bets are RWS & OTB and pleasingly after both had been heavily marked down they are both rapidly heading upwards. The reasons for my earlier sales of both RWS & OTB which of course were RNS catalysed, can be found in earlier RNS weekly logs on this site: as ever if I see a doubt I either get out or substantially reduce my holding. I suppose it makes me sound like a trader but that’s not how I work: once I see a risk, I take action to either diminish or remove that risk and should an attractive opportunity occur again with that company, then I will happily re-enter. In the case of RWS & OTB, both of which I consider as quality companies, they really to my mind became oversold and hence sufficiently attractive to me after their price falls. Anyway, onto this weeks log which I apologise in advance for being possibly a touch less in depth as I have been away from the office for so much of the time. Monday 04/06/2018: Xpediator: XPD: Mkt Cap £71m: Acquisition of Anglia Forwarding: Xpediator, (AIM: XPD) a leading provider of freight management services across the UK and Europe, is pleased to announce it has entered into an agreement to acquire the entire issued share capital of Anglia Forwarding Group Limited ("AFGL"), a UK-based international freight forwarder with road, sea and freight capabilities (the "Acquisition"). The initial cash consideration payable upon completion is £1.5 million, plus a further cash payment reflecting AFGL's surplus working capital position at completion estimated to be approximately £700,000. Deferred cash consideration of up to £2.0 million may also be payable contingent on profits generated by AFGL over the two years ending 31 May 2020. My View: to my eye, the acquisition of Anglia Forwarding for £1.5m plus deferred cash of up to £2m; looks a very sound purchase. Looking at the numbers provided it looks a reasonable enough acquisition for XPD and I suspect that more acquisitions will follow. The EBIT margin of XPD is by nature of the sector, not massive but from what I can put together it suggests that the margin will slightly increase as these bolt-on acquisitions come into play plus of course other synergies offering cost saving and contract opportunities. XPD is at the moment is only a small starter position within the folio. Monday 04/06/2018: Amino: AMO: Mkt Cap £149m: Kabelnoord rollout and on Wednesday 06/06/2008 a Trading Update Kabelnoord, the leading Dutch cable operator, is to deploy Amino's MOVE end-to-end multiscreen video platform. This will allow Kabelnoord to offer next generation TV services as part of a major rollout of its fibre-to-the-home (FTTH) network. Then the TU: Amino entered the current financial year with a strong order backlog and during H1 2018 booked over 40% more orders than in the first half of 2017. This, along with good pipeline coverage, means that the Board's expectations for the full year remain unchanged. As communicated previously and following the change in phasing of orders by one of our major customers, we expect to return to our normal seasonality in the current financial year, with revenues weighted to the second half of the year. Consequently, we expect revenue for H1 2018 to be lower year-on-year at approximately $41 million (H1 2017: $49.8 million). (Sterling equivalent H1 2018: approximately GBP30 million revenues; H1 2017: GBP39.9 million revenues). We continue to see momentum in areas of strategic priority, such as software and recurring revenues. Earlier this week we announced that Kabelnoord, the leading Dutch cable operator, is to deploy Amino's MOVE end-to-end multiscreen video platform in the second half of the year. Revenues from software and services sold on a standalone basis continue to increase and are expected to be 12% of total revenue in the period (H1 2017: 8%). Exit annual run rate recurring revenues increased in the period to circa $5 million (H1 2017: $3.7 million). (Sterling equivalent H1 2018: GBP3.8 million revenues; H1 2017: GBP2.9 million revenues). Net cash at 31 May 2018 was $15.1 million (31 May 2017: $16.8 million). (Sterling equivalent 31 May 2018: GBP11.3 million net cash; 31 May 2017 GBP13.1 million net cash). My View: well the roll-out contract win sounds encouraging but no real financial numbers can be offered and I can’t offer even a rough scratch calculation on the revenue significance; so, we will just take it as encouraging. However, what did not strike me as quite so encouraging is the required stretch from H1 revenues ( as predicted in this RNS) to H2 full year expectation. I am not saying it's not achievable or indeed doubtful but to my view simply looks a touch more challenging than I would feel comfortable with. I note that AMO tell us that expectations for the full year remain unchanged but a quick dig into the current H1 prediction & the full year expectation does worry me a tad; they may well make the numbers but after looking at recent historic H1/H2 ratios for AMO, it just looked a bit risky to me. My Action: I did try to sell 50% of my holding at the market open but as is so often the case with small-cap/AIM stocks, a decent trade selling price can be difficult to achieve on screen. However, I did take profits on 50% of my holding the following morning. My reasoning for this 50% sale was simply to control risk and AMO, which still looks a decent attractive business, is now demoted from my top 10 holding. Monday 04/06/2018: IQE: Mkt Cap £856m: Not an RNS as such but an AGM statement that can be found on the companies We are pleased to confirm strong wireless activity and that we are actively engaged in VCSEL qualification programmes with over 10 additional key VCSEL chip manufacturers, which are progressing in line with the board’s expectations. We confirm our guidance for a 40:60 revenue split H1:H2 2018, with a shift back from wireless to photonics as we enter H2 2018. The commissioning of the new Newport Foundry is progressing to plan, with the first five reactors now all on site and in various stages of acceptance testing, commissioning and qualification. The second five reactors are expected to be delivered on site commencing Q3 2018, with acceptance testing, commissioning and qualification during the rermainder of 2018. “Our new technologies portfolio, including GaN on Silicon, NanoImprint Lithography (NIL), Crystalline Rare Earth Oxide (cREO), and Quasi Photonic Crystals (QPC), is rapidly gaining strong traction and engagement with key customers around the globe for a wide variety of high volume applications.” The Group will announce its Interim Results for the six months ended 30 June 2018 on Tuesday, 4th September 2018. An analyst briefing will be held later that day at a time and venue to be announced. My View: firstly I wish companies would spell check in a better way as even a word blind dyslexic such as me can spot errors; that’s disappointing. I took profits of a recovery stock The Restaurant Group and bought back into IQE today having previously made some very decent profit on my sale of IQE earlier in the year. In fact, my association with IQE goes way back some 8 years but sadly I took time away from IQE for some of that time and missed the rise form the 20’s to the 70’s but at least I re-entered to catch a nice special situation that went on a charge through just about all of 2017 (half of that charge was better than no ride at all). Since that time and my sale in the 140’s, the share price has drifted down significantly after periods of ramping and negative ramping/excessive shorting in the investment community. I thought that the AGM statement was positive enough for me to buy back into what I tend to classify as a special situation stock. It’s not without risk but does contain a substantial amount of promise. From what I can see, the AGM statement has also been received well by the brokers. Tuesday 05/06/2018: No RNS of impact to Voyager Wednesday 06/06/2018: Amino: AMO: Mkt Cap £149m: Trading Update: SEE AMO Notes above & sale of 50% of holding. Thursday 07/06/2018: Ramsdens: RFX: Mkt Cap £57zm: Final Results:  My View: maybe I should start by saying that morally I don’t usually invest in the likes of pawnbrokers, loan-shark companies, tobacco companies, cheap booze companies etc as the exploitation of the less affluent is not something that I choose to profit from. However, I just about convinced myself that RFX was only partly a pawnbroker, conscience somewhat cleared, and therefore in recent weeks have been steadily building up a position in RFX with an average buy price of 188p. I like the financial numbers and ratios and indeed I see that Stockopdeia has given it a stock rank of 91. I should say apologies for the limited notes here as my office time is very limited this week; simply suffice to say that I see RFX as a decent quality business progressing well and it’s first set of full results since joining AIM look impressive to me. Indeed, I was very taken by these results which fractionally beat expectations (I think they are only covered by one broker but anyway, so the expectation does suffer from bias) and took a further slice of RFX and it now replaces AMO in the top 10 list. The strength in the numbers comes from their FX service, up 26% to £11.3m & Jewellery which was up 35% to £8m. The EBIT margin looks encouraging according to my rough fag-packet increasing from 13.2% in 2017 to around 15.8% in 2018. Friday 08/06/2018: Games Workshop: GAW: Mkt Cap £986m: RNS Trading Update: TRADING UPDATE ON CLOSE OF FINANCIAL YEAR ENDED 3 JUNE 2018 Games Workshop is pleased to announce that the sales and profit growth, which was discussed in the trading update released on 4 May 2018, has continued in the period to the end of the financial year. Sales growth has been across all sales channels. We expect the Group's sales for the 53 weeks to 3 June 2018 to be approximately £219 million and the Group's profit before tax to be at not less than £74 million. Royalties receivable from licensing are c. £10 million. In recognition of our staff's contribution to these results, we paid during the year a bonus amounting in total to £5 million. This was paid equally to each member of staff. My View: it looks a very decent trading update to me and I particularly like the bonus arrangement for all staff sharing in a £5m pot; that to my mind is excellent and really get employees feeling that they are more than just a servant to the company. The end of year figures look bang on the brokers and that leads me to a couple of thoughts: Firstly with a company doing as well as GAW and approaching a market cap of £1b I would have thought that more brokers would commence coverage of GAW. Secondly given the very positive newsflow from GAW including the introduction of new offerings and the royalties stream of income, I would think the forecasts would be moved upwards a touch for 2019 as at present the broker suggests a drop of 5% in revenue and a drop of 22% in pre-tax profit.  Interesting times; I am happy to continue to hold and may add further on future share price weakness as profit taking sets in.

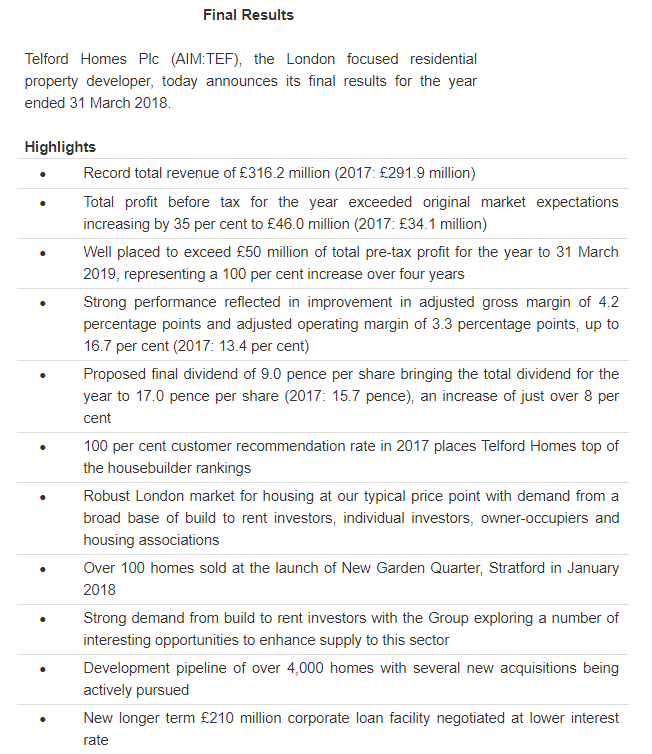

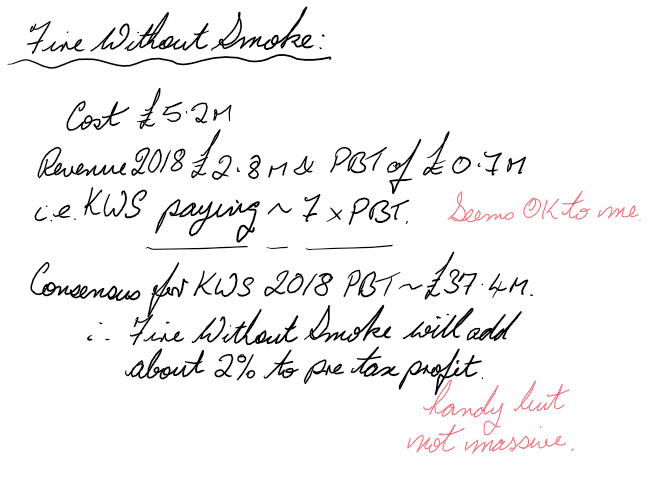

Whats On the horizon next week: Results: Finals from IG Design Group: IGR on 11/6/18 & Finals from Norcros on 14/06/18. Oh yes, also maybe AIR on 11/06/2018 if they complete the accounts worked then return from suspension. Possible Trading Updates? BOO & SOM. This weekend I intend to enjoy a nice family BBQ, fillet steaks marinated in kampot pepper/Lime/olive oil & chicken marinated in ginger/garlic/lime/soy sauce all cooked over charcoal and maybe washed down with a little red! Whatever your plans, enjoy the summer while it lasts! Happy investing; catch you all next week Voyager RNS Log WC 25/05/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Only a short week with the bank holiday and a very quiet one at least to start with as there was very little RNS news on Tuesday apart from the market jitters as Italy and Spain struggle with their economies and the thankless individuals collectively called politicians struggle with a way forward. In truth, I have never been a political animal and feel fairly convinced that I could have found a way to prosper even in the likes of Albania in the 90’s. Anyway. Let’s hope Mr Market does not become overly upset over the next couple of months but if he does, I have a very healthy reserve that may be called on should any anomalies be chucked up for the better quality companies. Conversely, rubbish will be rubbish no matter what the market is doing. Onto this week's log: Monday 28/05/2018: Bank Hol, Markets Closed: Tuesday 29/05/2018: No RNSs relevant to Voyager portfolio. Wednesday 30/05/2018: Telford Homes: TEF: Mkt Cap £346m: Finals RNS:  Total profit before tax in the year to 31 March 2018 increased by nearly 35 per cent to £46.0 million (2017: £34.1 million) [1], ahead of original market expectations. This strong performance was reflected in an improvement in our adjusted gross margin of 4.2 percentage points and a 3.3 percentage point increase in our adjusted operating margin, up to 16.7 per cent (2017: 13.4 per cent). The margin improvements are partly due to the mix of developments that completed during the period but also a combination of other factors, particularly some prudent estimates for build cost inflation that were not realised. I am also delighted that we have been able to declare a final dividend of 9.0 pence per share, making a total of 17.0 pence per share for the year, an increase of 8.3 per cent compared with the previous year (2017: 15.7 pence). We expect to continue to pay at least one third of our annual earnings to shareholders in dividends. Outlook Telford Homes has delivered significant profit growth over the last three years with total profit before tax increasing from just over £25 million in 2015 to £46 million in 2018. Furthermore, we are well placed to achieve our stated goal of exceeding £50 million of total pre-tax profit for the year to 31 March 2019 which will represent a 100 percent increase over four years. Having arrived at this point in a short period of time the challenge now is to establish the business consistently delivering over £50 million of profit every year and furthermore to generate and sustain the next significant growth period. Without the advent of build to rent we would not have been able to achieve consistency of profits and would instead have fluctuated around an overall upward trend. Our industry is very capital intensive and the business would have required sustained injections of new capital just to maintain the profit levels achieved in the last few years on an ongoing basis. However our increasing success in the build to rent sector means we expect to consistently deliver profit in excess of £50 million over the next three years predicated on a certain level of new build to rent business. We also expect to set a platform for delivering the next significant phase of profit growth in the medium to longer term. The level of build to rent business we are able to secure will be crucial to achieving our ambitions and to outperforming them if the opportunity arises. The strength of our position and our ability to capitalise on the exciting possibilities ahead are a result of the hard work and dedication of the whole Telford Homes team. I am exceptionally proud of the customer recommendation and employee satisfaction scores we achieved last year and I am confident there is a relationship between them. I look forward to us building on the solid foundation we have created for Telford Homes both in the year ahead and beyond. My View: another very sound set of results from TEF which as I have said before, is my favourite stock in this sector as it’s simply geographically concentrated in the right place, London where there is a massive shortage of reasonably priced housing & the rental investment is flourishing; a large part of TEF work is in the buy to rent segment where they carry out the entire process to completion before handing over to large investor landlords. I just can’t really see that need, which makes this stock low risk, ever really going away. I see TEF as a very well managed business that manages expectations and simply delivers almost constantly at the top end of those expectations or even above them. For fellow TEF investors, here is a link to a video where Jon Di-Stefano, TEF CEO, and his FD talk through the results: Video: www.brrmedia.co.uk/broadcasts/5b06e7139e3d657120be37ee/telford-homes-full-year-results I view TEF as a very long-term hold and that I am happy to continue to treasure within the portfolio and likely add further on any share price weakness in the following months. Yes, it is an incredibly boring stock & not one for the “get rich quick mob” but I can’t help but like boring predictable stocks. Wednesday 30/05/2018: Bodycote: BOY: Mkt Cap £1770m: AGM Trading Update RNS: Trading Update Current trading Group revenue for the four months ended 30 April 2018 was £243m, 7% higher than the same period last year and 10% higher at constant currency. On a divisional basis, ADE revenues were up 5% to £94m (up 10% at constant currency), while AGI revenues were up 9% to £149m (up 10% at constant currency). Within the overall Group result, Specialist Technologies' revenues grew 12% at constant currency. The following review of the Group's markets quotes all movements based on growth against the same period in 2017, at constant currency. Car and light truck revenues grew 8%, with continued strong growth in Emerging Markets and good growth in Western Europe, while North American revenues were down slightly. Civil aerospace revenues grew 4%, held back by restrained demand in France stemming from capacity shortfalls in the aerospace industry supply chains. Overall growth of energy revenues was 24%, with continued strong growth in onshore North American revenues, as well as early indications of an upturn in Western Europe oil & gas revenues. Large frame industrial gas turbine (IGT) revenues were down in North America in line with the cut backs in IGT production announced by the OEMs at the end of 2017. In Western Europe, the IGT declines were more than offset by the increase in business from the new Long Term Agreement with Doncasters. General industrial revenues were 11% higher with good growth across all geographies. Margins have continued to improve although the profit drop-through from incremental sales has been partially offset by increased investment in business development. Financial position Net cash as at 30 April 2018 was £45m compared to £40m at 31 December 2017, reflecting continued strong underlying cash generation in light of the typical working capital outflows in the first few months of the year. The Board will pay a final dividend of 12.1p per share and the special dividend of 25.0p per share on 1 June 2018, at a total cost of £71m. Summary and Outlook We have seen robust growth in the first four months of the year in spite of the foreign currency headwind. At this early stage, and notwithstanding the Group's limited visibility, the Board now expects full year revenue to be higher than previously expected and headline operating profit to be slightly ahead of current analysts' consensus. My View: it seems to me that revenues are up some way more than forecasts & the fag packet looks quite encouraging:  All in all, quite an upbeat trading update from one of my top 10 holdings: it will never be the most exciting company but to my mind, a portfolio loaded with such steady well-managed companies would not be a bad portfolio. Wednesday 30/05/2018: Keywords Studios: KWS: Mkt Cap £1080m: Acquisition of Fire Without Smoke RNS: Strengthening the Group's Art Services Line Keywords Studios, the international technical services provider to the global video games industry, today announces that it has acquired Fire Without Smoke Ltd ("Fire Without Smoke") for a total consideration of up to £5.2m from the founders Will O'Connor, Michael David Thomson and others (the "Sellers"). Headquartered in London and with a studio in Montreal, Fire Without Smoke provides a full suite of creative and marketing services to game publishers and developers, creating assets such as game trailers, marketing art and materials for esports events, and providing marketing consultancy and general design services to the video game industry. Founded in 2013 and now with [40] staff between London and Montréal, Fire Without Smoke works with major game publishers such as Sony, Square Enix, Riot Games, Deep Silver, Sega, Capcom and Ubisoft. For the year ending 31 May 2018, Fire Without Smoke is expected to have revenues of £2.8m and adjusted profits before tax of £0.7m. Under the terms of the acquisition Keywords is paying a consideration comprised of £3.85m in cash, £0.5m of which is deferred until the first anniversary of acquisition and subject to certain performance targets, and the issue of 77,006 new ordinary shares in Keywords, which will be issued to the Sellers on the first anniversary of the acquisition and will then be subject to orderly market provisions for a further 12 months. My View: yet another deal by KWS as it builds its global offering: a quick fag packet calculation:  From what I can gather, two brokers have today have raised their price target for KWS to £21. I don’t place much faith in brokers price targets but anyway, that implies about a 20% upside from where we stand now. The Outlook statement that accompanied the finals on the 09/04/18 was very positive yet the shares may well drift a touch ahead of the next trading update which I expect to see around the end of July/beginning of August. Overall, I am happy to continue to hold this rather exciting company but as ever, the managing of all of these acquisitions does worry me a tad.

Thursday 31/05/2018: Air Partner: AIR: Mkt Cap £52m: RNS Finals for 2017: Temporary suspension of share trading Further to the Company's announcements of 11 April and 25 May 2018, the Board of Air Partner has agreed with Deloitte LLP, the Company's auditor, that the Company will not be in a position to publish its annual audited accounts for the year ended 31 January 2018 by close of business on 31 May 2018. The Company is working together with Deloitte LLP to finalise the audit and expects the audited accounts will be published no later than Monday 11 June 2018. Accordingly, the Board has requested that trading in the Company's ordinary shares on the London Stock Exchange be suspended with immediate effect pending publication of the audited accounts, following which the Company will request the suspension be lifted. This unforeseen delay is a result of the volume of work required to complete the accounting review and its impact on the financial year audit and the prior year restatements. It is in no way related to the Company's current trading, cash flow, banking arrangements or any underlying issue. Peter Saunders, Non-Executive Chairman of Air Partner, said: "The delay to the publication of our full year accounts, and the resultant trading suspension, is extremely frustrating and hugely disappointing for all connected with Air Partner. However, it is a reflection of the volume of work, which began 7 weeks ago, to conclude a transparent, thorough, and exhaustive internal review and audit. This delay is not related to the Company's current trading, cash flow, banking arrangements or any underlying issue. We thank our shareholders for their continued patience and support." My View: I did up until early April this year have a fairly chunky holding in AIR and they were very considerably up on my original investment that is until that RNS about their “accounting oversight”. On the first sniff of doubt i.e. that early April RNS, I immediately sold. In truth, it was a still a very profitable investment and as the share price continued to head downwards, my sale turned out to be a wise move. An RNS “things are not so bad” was released a couple of weeks later and I reentered at a new but very small starter position using a portion of my profits from the earlier holding; in fact the smallest position by some way in the portfolio. The reason I bought this fresh starter position was that I felt there was a real possibility that the accounts issue was historic in nature and a release of the promised results would once again confirm confidence in the business with the promise that things were under control. We then have two RNS’s the most recent one being 25th May (only 5 days ago) confirming that the year-end results would be issued on 31st May. So, after my swim, I got onto my iPhone & SharePad to have a quick look at the results but nothing there @ 7:15 but nothing; ok, I will ditch what I have as soon as the market opens, I decided. Whoops, hardly finished towelling myself dry when we have an RNS from AIR telling us that the shares are temporarily suspended but hey, everything is fine as “delay is not related to the Company's current trading or cash flow etc”. Now, it may well be that the delay is simply getting sustainable security and closure of the accounting issue or alternatively the audit may have found a few more unfortunate accounting issues when they lifted a few carpets around the place. Either way, I feel the company has really lost some trust and credibility which they may possibly have avoided had they more astutely funded the audit into the “anomaly”. Once they return from suspension I will likely sell the few I own. Friday 01/06/2018: No RNSs relevant to Voyager portfolio. Can’t help myself: A New Purchase: An addition to the portfolio: Purchase of Softcat: SCT: a FTSE 250 stock of £1.3b Mkt Cap. Bought at 724p. Briefly what I like about Softcat:

Softcat plc ("Softcat", or the "Company"), a leading UK provider of IT infrastructure products and services, today releases a trading update for the quarter ended 30 April 2018 ("the Period"). The Company has continued to trade well across all segments during the Period, maintaining momentum from the first half and reflecting further successful execution of its strategy. Market conditions and customer demand have both remained strong. Outlook The Board is confident that the Company will deliver full year results that are ahead of expectations. Glad I Am Not There ( GINT): I should say these are not “clever dick” notes just simply an attempt to help investors learn from their mistakes and let's face it, we all make mistakes and I am probably a graduate of the University of errors: the crucial point is what we learn from those mistakes. Photo-me International: PHTM: For investors, a very disappointing update and as PHTM say, Japan hasn't performed as expected. The outlook says “below current market expectations”. The stock was really bashed by the market falling about 25% and then fell again on the following day. Simply horrible things profits warnings but to my mind, every investor should have a plan of how they deal with them and that’s most certainly not burying your head in the sand. PHTM simply just one of those stocks that never really hit the spot for me i.e. I just never got what PHTM was about with its mix of photo booths and laundrettes seemed to be in something of a 1990’s time warp. I just was never overly impressed by the management sales pitch or presentations to investors. Whilst I agree they have no net debt and indeed have cash on the books, that very generous dividend of 7.7% has not been covered by FCF since 2014 and whilst they intend to pay that dividend this year, it looks to be in for a cut in the future. Note: the conventional dividend cover of eps/dps suggests all is well but looking at the free cash flow suggests otherwise and has done for a few years. Thankfully due to my overall feel for the stock and the quality of the cover, it just never tempted me to buy. Whats On the horizon next week: I can’t see much pencilled in for next week but expect to hear a trading update accompanying the Somero AGM and suspect a trading update will come from Amino (AMO) & Dart (DTG). Have a good weekend & as ever, happy investing; catch you all next week. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed