|

Voyager RNS Log WC 01/10/2017 Well, quite a lot to talk about this week on the portfolio front with a number of announcements that made interesting reading after ploughing a steady mile in the pool. Strange how we all have some “addictive” pursuit; just could not imagine the early mornings without a nice calming pool in front of me. Just as a general comment and maybe a take care reminder; the markets we currently trade in are probably at one of their easier moods than I have generally experienced over the last 30 years of investing and I fear that there are many investors out there who have never experience a bear market or serious correction. It seems that the world and his brother are making 20%, 30% etc at present and that does genuinely please me but do remember that the music will not keep playing forever: just a reminder that “everybody is a winner in bull markets” and they simply don’t continue forever and careful stock selection of quality businesses is to my mind essential. A couple of Whittler Rules:

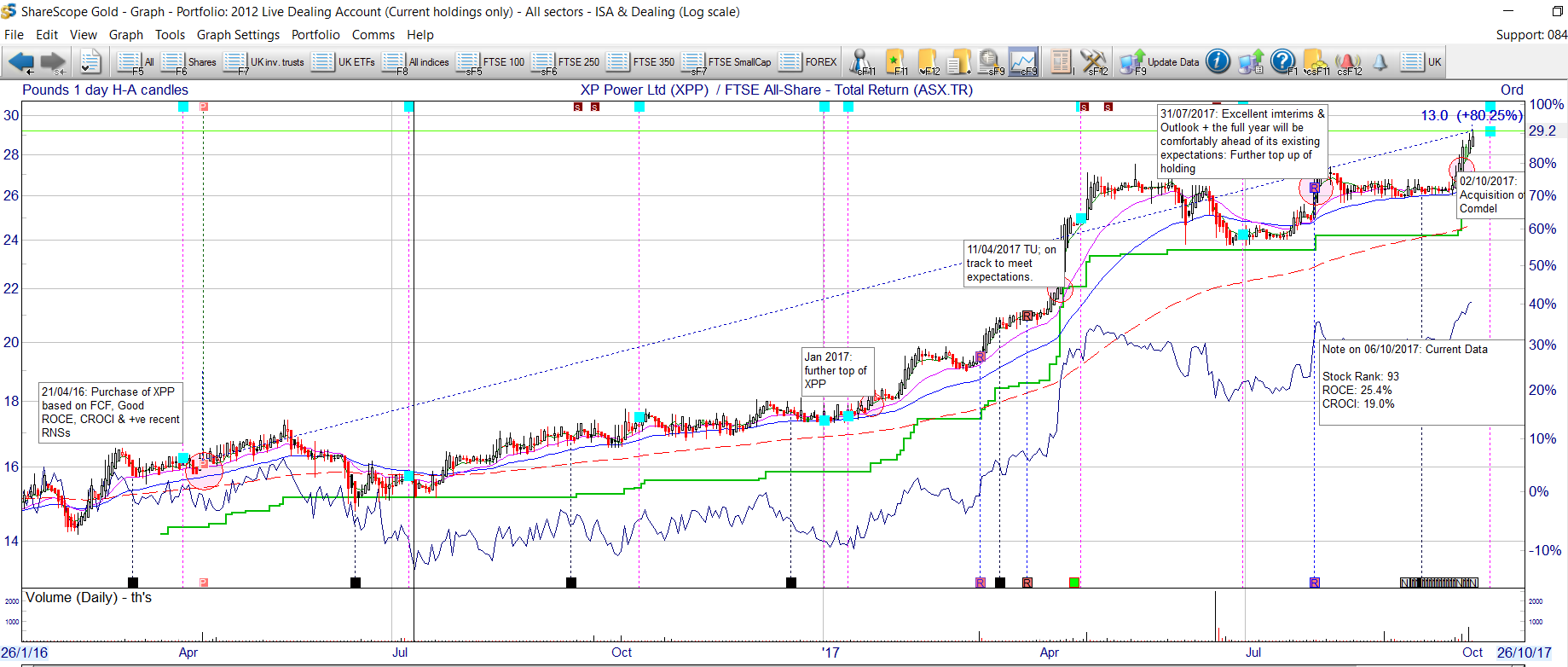

Anyway the universe/folio RNSs: Monday 02/10/2017: XP Power: XPP: Mkt Cap. £546m: RNS Regarding their acquisition of Condel Inc.: The RNS reads: XP Power, a world-leading developer and manufacturer of critical power control solutions for the electronics industry, announces that it has acquired the business and assets of Comdel Inc. ("Comdel"), a designer and manufacturer of radio frequency ("RF") power supplies (the "Acquisition"). Total consideration of US$23.0 million (GBP17.0 million) was paid in cash on completion. The Acquisition is on a debt and cash free basis and was funded with a new revolving credit facility of US$40.0 million with a US$20.0 million additional accordion option. The new facility is in place to assist the company's inorganic growth strategy. Comdel is based in Massachusetts, USA, and supplies the industrial and technology sectors with a range of standard, modified and custom high power RF power conversion products. Comdel typically supplies RF power supplies to the semiconductor, thin film, photovoltaics, and induction heating industries. In the fiscal year ended 31 December 2016, Comdel recorded sales of US$16.5 million (GBP13.0 million), profit before tax of $1.8 million (GBP1.4 million) and had gross assets at the year end of $10.9 million (GBP8.5 million). The Acquisition is expected to be enhancing to the Company's earnings per share in 2018*. My View: Looks a decent acquisition to me and will hopefully boost XPP growth prospect over the coming years. Is XPP expensive? Well even on the ubiquitous and often manipulated PE ratio, not terribly expensive for a company experiencing attractive growth in my opinion. As ever, I look to the returns on capital which are very attractive and confirm my view that I am very happy to continue to hold. In fact, I am a little niggled with myself as although I have made various top-ups over the last 18 months, I really should have been more committed to my “fag-packet calculations” that kept shouting to me to make a further significant purchase. I reckon we all have the gift of wisdom after the event! Click on chart to enlarge:  Monday 02/10/2017: On The Beach: OTB: Mkt Cap: £526m: an RNS statement regarding Monarch Airlines: On the Beach Group plc, (LSE: OTB), the UK's leading online retailer for beach holidays, notes the recent announcements by the Monarch group and the Civil Aviation Authority that Monarch Airlines Ltd and other companies in the Monarch group have entered administration. On the Beach is contacting customers that are currently in resort to assist with their return travel and also those customers booked to fly with Monarch Airlines in the coming weeks and months. The Group has Scheduled Airline Failure Insurance in place which covers the failure of Monarch Airlines Ltd including monies paid to Monarch Airlines Ltd and also the costs to repatriate customers currently in resort. The Board anticipates that there will be a one-off exceptional cash cost associated with helping customers to organise alternative travel arrangements or providing refunds and will update shareholders in due course. The Group has no exposure to Monarch Holidays Ltd bookings as it only offered Monarch Airlines Ltd seat-only flight options on its website. My View: this sort of thing happens in the travel industry and with the pressure on airfares it will undoubtedly happen again maybe not to OTB but certainly elsewhere. I take a fairly relaxed view to this event and will continue to hold my current position. Tuesday 03/10/2017: Revolution Bars Group: RBG: Mkt Cap: £105m: Results For Year Ended 31/07/2017. The results in truth mean very little as RBG is the subject of an agreed takeover by Stonegate at a price of 203p; that price may of course rattle up a little if Deltic who are ponderously carrying out due diligence on RBG, come in with a higher offer before 5pm on 10/10/2017 the deadline set by The Takeover Panel. Of course, there is always the possibility that a third potential bidder may enter the contest and for that reason, I am happy to stay invested with the comfort that the Stonegate 203p is near as money in the bank. Readers may recall that earlier in the year following the announcement that the second FD was to depart RGB having only been in post a handful of months, I took this as a major red flag warning banner and immediately sold my holding. An extract from my RNS Log of 04/08/2017 reads I originally bought into RBG in January this year but following an announcement that the second CFO in a few months had declared he was leaving the business I sold my entire holding; 2 x CFO’s leaving in a short space of time just did not sit well with me. A few months later, May 2017, RBG duly issued a profits warning and the shares were absolutely caned eventually bottoming at about 50% of the pre-profits warning price in early July: hardly surprising as management credibility had declined and with it the trust of many investors. On Tuesday last week, RBG issued a very reassuring trading statement and it appeared the new CFO had brought a bit of sanity and reassurance to the business. I pondered for a couple of days and then bought back in on Friday afternoon. Back to the RBG Results: The results do reveal an accounting mess at RBG before the time of the current FD: Our results Our reported results show good progress against the prior period, with sales growth of +9.2% and even stronger growth in adjusted EBITDA*** at +16.0% against the restated figure for the prior period. We consider adjusted EBITDA*** to be the key measure that best represents the business' underlying performance as it excludes exceptional items and bar opening costs that are a function of the timing of the new venue development programme rather than the underlying trade. Last year's adjusted EBITDA*** has been restated from GBP15.6m to GBP13.0m. Operating profit was GBP3.7m (2016 Restated*: GBP5.3m) but this was after charging exceptional items of GBP4.4m (2016 Restated*: GBP1.4m). During the year, there was significant change within our finance team. This included the Chief Financial Officer, Sean Curran, and the Group Financial Controller, who had both been with the business for over ten years, both leaving the Group. Chris Chambers replaced Sean in the autumn of 2016 but resigned shortly thereafter in February 2017. Mike Foster joined the business in March 2017, initially as interim Finance Director, before being appointed to the Board and as the Group's Chief Financial Officer in early June 2017. Our Finance and IT teams play a critical role in providing the systems and reporting to facilitate running an efficient business. Significant IT developments have been undertaken in the year to support the Sales, Operations and People Development teams. Our Finance team has had much to contend with in the last year and it is now very clear that our accounting systems and processes were in need of upgrading. Improvements have been made, and will continue to be made, in this area to provide a more robust financial infrastructure and in so doing bring additional benefits. My View: All in all a bit of a financial reporting muddle at RBG and it’s just as well in my opinion that another company looks like taking them over albeit at a probable bargain price just north of 200p. Reference Note: Note: now just to reiterate, I do NOT OFFER ADVICE on specific shares but merely share my rationale and methodology of investing, However, I have over the years built up a series of Whittler Rules that sit on my office wall. In the case of RBG at the time of my initial exit as two FDs sought other opportunities, the rules that applied, again as on my office wall, were:

Tuesday 03/10/2017: AB Dynamics: ABDP: Mkt Cap £114m: Pre-Close Trading Update: The Group has performed well in 2017 and the Board expects revenue and profit before tax (excluding share option charges and latest IFRS 15 adjustments) to be slightly ahead of analysts' forecasts. The Board has chosen early adoption of IFRS 15, from 1 March 2017, and this is expected to lead to a reduction in the level of reported revenue for the year to 31 August 2017, but with no consequential impact on profit before tax. Despite the adoption of IFRS 15, it is anticipated that reported revenue will nevertheless remain in-line with current market expectations. My View: I like ABDP and it’s rewarded me nicely since my couple of batches purchased in June & July of 2016 following a fall back in the previous high flight path of the stock. Within the update are the pleasingly reassuring words that the PBT will be slightly ahead of analysts expectations: much nicer wording than management expectations as after all, what are management expectations! Is the share expensive? Well, I personally think not given its niche state of its business and forecast profits growth over the next couple of years. Also the returns on capital, ROCE & CROCI have been historically high and look like staying that way. Probably one I will hold for quite some time to come. Wednesday 04/10/2017: No RNS relating to a share within my universe or portfolio. Thursday 05/10/2017: Only one RNS of serious note for the portfolio in that Deltec came out with a very wordy RNS essentially suggesting a non-cash takeover/merger of Deltec & RBG. I guess this one may drag on for a while and hopefully may either flush out an improved bif from Stonegate or suck in another bidder who may see the RBG offering being undervalued at a touch over 200p. I think I will just sit on my hands and not get overly excited until the end game is a touch closer. Friday 06/10/2017: No RNS relating to a share within my universe or portfolio. Glad I Am Not Here: well, its a fairly sad one this week for holders of Accrol Group: ACRL with an apparently disastrous announcement that the shares are to be suspended with the likelihood that much of the forecast profits for this year will be flushed down the pan along with the companies tissues that they manufacture. You could go on with the puns but in truth it’s simply not a happy position for investors who bought into ACRL when It was listed on AIM not that many months ago. I have to say that I very rarely invest in IPOs and take the view that I would rather have a decent look at the minimum of a few months listed trading and numbers to anywhere near give me an acceptable degree of comfort. An added deterrent for the ACRL float was the enticement of a fat yield in order to get investors on-board. Were there any warning signs? Well, I would say there was one that would not sit well with me and that is the RNS dated 07/09/2017: giving a TU and the announcement of the appointment of a new CEO: the RNS reads: Accrol Group Holdings plc (the "Company" or "Accrol"), the AIM-listed leading independent tissue converter, announces that Gareth Jenkins has been appointed as Chief Executive Officer with effect from 11 September 2017. Gareth joins the Company having spent 24 years at DS Smith plc, one of Europe's leading packaging companies manufacturing corrugated solutions for the retail, FMCG and industrial markets. He spent the last four years as Managing Director of the UK & Ireland packaging division and has extensive strategy, commercial, M&A and operational experience, gained in both the UK and in Europe. Gareth will replace Steve Crossley, who is leaving the Company and stepping down from the Board with immediate effect to pursue other interests. My view: That sort of statement does set the warning bells ringing very loudly especially as there was absolutely no hint of Steve Crossley's "unplanned" departure in the year end results RNS published just 8 weeks earlier. Had I have been an investor I would have very rapidly sought significant reassurance that all was well or otherwise: see my notes in red above "rules on the wall". I should also add that I steer away from companies that promised large dividends that are nowhere bear covered by FCF & also carry debt. Next Week: we have preliminary results for my favourite boring company WH Smith and I hope there is zero excitement and my boredom may continue. SMWH are up over 25% so far this year and I have to say have done me proud over the years. I also suspect we may see a trading update from Amino: AMO next week. Have a good weekend and as ever, happy investing.

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed