|

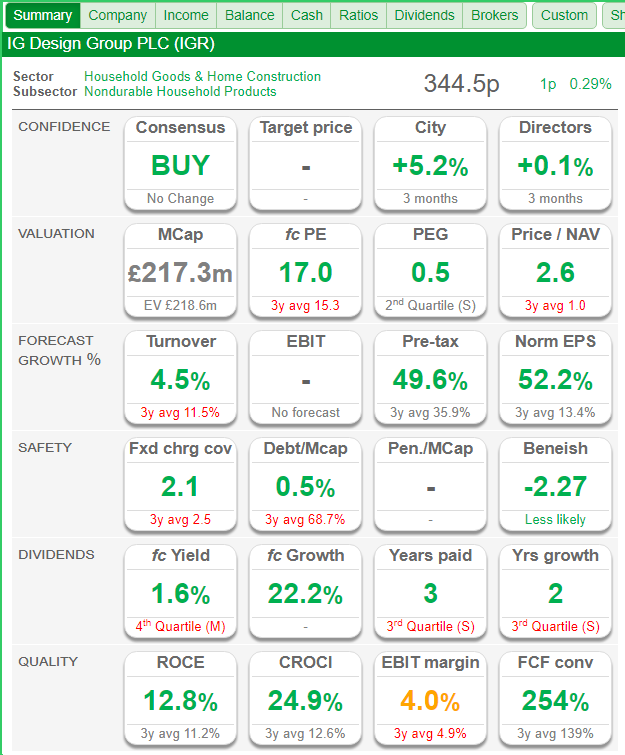

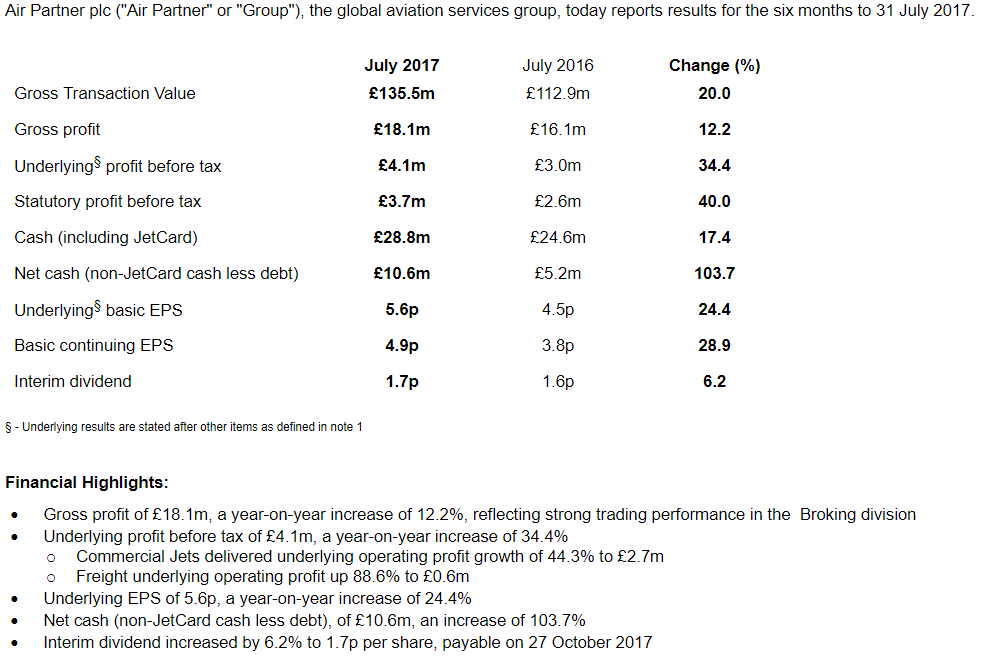

The Voyager RNS Log: Week Commencing 24/09/2017 Note: as ever nothing I write here is in any way a recommendation; well apart from the superb meze. Just view this as me meandering through my thought process concerning various regulatory announcements and sharing my views. Well having returned from my routine September visit to my favourite restaurants in Kyrenia; I just love authentic meze. However, it’s nice to get back behind the keyboard; and so refreshing not to even look at share prices over the last couple of weeks but just kept an eye on RNSs via a distinctly awful wifi and costly 3G. I have to say that Erdogan’s antics are likely to prevent me from flying via Istanbul again; can you believe four baggage x-rays, a compulsory change of plane and a body search with swab tests on my IT kit just to get back home; Erdogan seems a total paranoid madman. Anyway, a couple of RNSs to catch up on before I touch on this week’s events. Firstly: Tuesday 19/09/2017: Keyword Studios: KWS: Half Year Report and once again another very solid picture of growth emerges with adjusted profits up some 60% and adjusted eps up 55%. Note: the nature of the adjustment is integration expenses of EUR0.5m (H1 2016: EUR0.7m), share option charges of EUR0.4m (H1 2016: EUR0.3m), amortisation of intangibles of EUR1.2m (H1 2016: EUR0.6m) and foreign currency loss of EUR1.96m (H1 2016: EUR1.77m). Now adjustments are without doubt a pain in the bum for us private investors so what does the profits growth look like when stripping back these adjustments? Well, to my “fag packet calculation” it looks pretty blooming good. Has the share price got a touch ahead of itself? Well, that’s the perennial question with all growth stocks that prove popular with investors and see their share price appreciation in such a dynamic way. In my case KWS has appreciated about 4 to 5 fold since my original batches purchased and to mitigate a touch, especially as KWS was becoming a touch heavy in the portfolio, I sold some shares that covered my entire initial investments value thus leaving a very significant amount of stock riding “for free” within the folio. Hang on, “riding for free”, what a silly concept/quote that I remember seeing in share tip sheets in the late 90’s. Whatever does it mean? Whoopee, a profits warning but that won’t hurt me as they are riding for free! My View: I am very happy to continue to hold what seems to be an ever-increasing weighting in my portfolio even after the recent sale of my original investment in £. Incidentally, surprisingly I managed to sell that part holding at the top of the market; now that does not happen often! Is the share currently expensive? Well, difficult one to answer after such a great run but the measures I like, ROCE, CROCI, Free Cash Flow Conversion look so attractive as does the forecast growth rate in eps. Another aspect that attracts me is the huge addressable market where gaming companies outsource such services as those offered by KWS. Also, KWS appears to have a good reputation with its customers, an impressive client list and confidence in the continual expansion of the business. I personally see this one as a 3-5 year hold in which you have to acknowledge the risks associated with such an acquisitive company but worth “sensibly” tucking away in my opinion. Thursday 21/09/2017: Revolution Bars: RBG: RNS ruling from takeover Panel ruling that Ranimul, the parent company of Deltic the other bidder competing with Stonegate for the acquisition of RBG, must announce by 5 pm on 10/10/2017 if they intend to make an offer for RBG. Interesting times and I feel a rather happy investor. Thursday 21/09/2017: IG Design Group: IGR: RNS Re: Acquisition of a leading Australian greetings card business: In the year to 30 June 2017 the business generated sales of AUD13.4m with an operating profit before tax of AUD2.9m. The total transaction and restructuring costs are estimated to be AUD0.6m (GBP0.4m) which will be treated as exceptional costs. While of negligible impact to underlying earnings in 2017/18 due to the timing of completion, the acquisition will be earnings accretive from the next financial year underpinned by synergies in sourcing, design and logistics net of amortization of intangible assets. My View: anybody who reads my various notes about IGR will no doubt already be aware that I consider this to be a well-managed business that has delivered in recent years. Is it expensive or not? Well, you may well know that I just don’t have much faith in easily manipulated PE values preferring to consider returns on capital invested whilst looking for an attractive entry point. In this case we have a decent CROCI and IGR nicely converts profits into cash. Overall I am happy to happily hold IGR which has doubled my original investment over the last 18 months. Dashboard from the excellent SharePad:  Monday 25/09/2017 to Wednesday 27/09/2017: only a few routing RNSs for stocks within the Whittler universe/portfolio. Thursday 28/09/2017: Air Partner AIR: Interim Results and to my eye a very good set of interims with the headlines shown below:  So with the numbers, all looks to be very encouraging as is the outlook statement: Outlook: The new financial year has started well and we are making good headway against our strategic objectives. Trading since the period end has remained solid. We enter the second half with continued confidence that our expectations for the remainder of the year will be met, whilst the final quarter of the financial year can be the most challenging. We have built a strong platform from which to continue to grow the business. Our long-term objective to create a more equal balance between our two divisions, Broking and Consulting & Training, will deliver higher quality and increasingly visible earnings to our shareholders and will further align us to the needs of our global customer base, enabling us to continue to provide exceptional service and value. One part to keep an eye on in the next update/results will be the progress with Clockwork research which has had a challenging first half since it’s recent acquisition by AIR: At the end of 2016, we acquired fatigue management consultancy, Clockwork Research. First half trading has been challenging, but with a good pipeline of projects we are confident in the longer-term prospects for the business. We have undertaken work to further strengthen this pipeline and leverage the Baines Simmons offering. An encouraging example of the cross selling opportunities that have arisen following acquisition, is that Clockwork Research is now carrying out work within the rotary sector with a Baines Simmons client. On the same day as the interims, AIR announced that it had paid £3m to acquire SafeSkys Limited: On 27 September 2017 Air Partner plc acquired the entire share capital of SafeSkys Limited for a total net of consideration of £3.0m, obtaining control of the company on that date. SafeSkys Limited is a leading environmental and air traffic control services provider to UK and international airports. The acquisition has been funded from the Group's cash resources. Due to the proximity of the transaction to the reporting date, the purchase price allocation accounting has not been finalised. Details of the acquisition accounting will be provided in the annual report for the year ending 31 January 2018. The acquisition of SafeSkyes was itself the subject of a separate RNS on 28/09/2017: Air Partner plc ("Air Partner"), the global aviation services group, is pleased to announce the acquisition of SafeSkys Limited ("SafeSkys"), a leading Environmental and Air Traffic Control services provider to UK & International airports. The acquisition has been funded from Air Partner's existing cash resources, aligns to Air Partner's long-term strategy and objectives, and is expected to be earnings enhancing in its first full year of ownership. SafeSkys reported revenue of c. £1.8m for the year ended 31 July 2016. SafeSkys was founded in 1993 by Richard Barber, and over the past 24 years of his ownership, has grown to be recognised as a leading provider of Environmental and Air Traffic Control services working across 16 civilian and military airports in the UK, employing over 80 trained staff working every day onsite at the customer airport. Hopefully we will have some more details provided about this acquisition at the time of the finals and certainly AIR must be confident having paid £3m for a company with a current turnover of £1.8m; digging around at companies house I also gleaned some information from the latest accounts for 2016, SafeSkys have net assets of £637k which included £223k of cash. From what I can deduce from the SafeSkys site, they seem to operate almost as an agency style of operation so extrapolating the 80 staff to the £1.8m turnover can give a duff figure of salary estimate per employee.  Friday 29/09/2017: no RNS significant to stocks within the Whittler universe/portfolio.

My View: a very decent set of interims accompanied by the interesting acquisition of SafeSkys all make the company look very attractive to my eye and I will continue to hold plus may be tempted to make further additions on the inevitable turbulence that AIR encounters on its flight path to hopeful continued success (hell, that was a cheesy line Whittler). I have been invested in Air Partner since mid-2015 and have made a series of top ups since that time. Happy to say that the investment, which also provides a healthy >4% dividend, is working rather well for me. Not quite in the Glad I am not here category but nevertheless, a share a keep a dubious eye on having once held and sold after becoming a touch concerned about the management of the business (issues with tied in suppliers & market understanding), is Sprue Aegis: SPRP who posted their half year report on Monday 25/09/2017. Strange in a way because I suspect that SPRP is overall a decent enough business. However, I still feel concerned about the allocation of revenue to capex which just seems to increase all the time and is running at 6 to 7 times the D&A. The allocation of costs to capex is just a touch worrying when compared to both the D&A & EBIT: maybe it’s fine but if I were a shareholder I would dig a lot deeper just to make sure I was comfortable. However, as I am no longer a shareholder, I will leave that one there and dig around elsewhere: whoops, I mean studiously investigate elsewhere. Glad I’m Not There (a sort of reverse take on the old Judith Chalmers holiday programme briefly mentioning a dog of the week that thankfully I don’t own). Congratulations to multi-award winner Telit Communications whose shareholders either need nerves of steel or a bottle of gin! On Thursday 28/09/2017 an RNS suggested that the smoke generator may have run out of fuel and the mirrors developing cracks. The announcement advises of some downward revisions of forecasts and also an advance waiver for any potential breach of a covenant; thankfully I don’t hold TCM neither do I like gin! Finally, what a nice bunch of people private investors can be; well that’s certainly my view of the large number I have come across over the many years I have been investing. I remember that for years I just did not like the Twitter style of social media and indeed only ever used Twitter at the time to see how depressing the Hatters team news would be: I should explain that Twitter carries football team lineup news at around an hour before kick off when I am enjoying a pre-match pint. Strange but how wrong I turned out to be because about three years ago I started using the little tweeting birdie to exchange a few thoughts on shares. Amazingly this opened a whole new world of Twitter buddies, blogs etc; all in all really enjoyable. Last weekend, although I did not attend as away on holiday, one of those dubious ringleaders, Wheeliedealer; a top bloke incidentally, organised a summer bash which was attended by many from quite considerable distances even the frozen north of Scotland and a few outside of the UK. What a superb community or indeed set of communities there are available out there for us private private investors with the likes of sensible types on Twitter, ShareSoc & events such as those organised by David Stredder, Of course we also have such excellent writers such as Phil Oakley on SharePad/Sharescope and of course the unique style of Stockopedia’s Paul Scott plus the great Conkers Corner. There is plenty of good stuff out there for the open-minded PI to learn from if they so choose. Next week: we have preliminary results from Revolution Bars Group, there may be a trading update from Amino Technologies but I suspect that will be the week after; the same applies to Zytronic where I expect to see a trading update within the next 2-3 weeks. Have a great weekend and as ever, happy investing.

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed