|

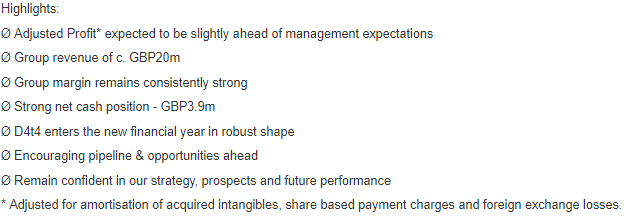

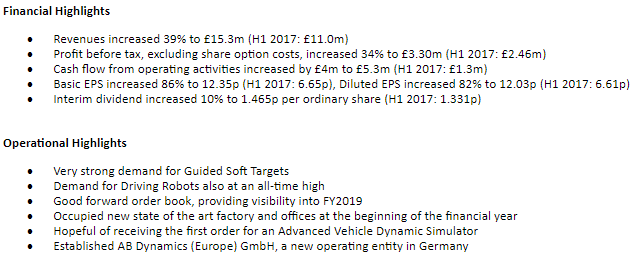

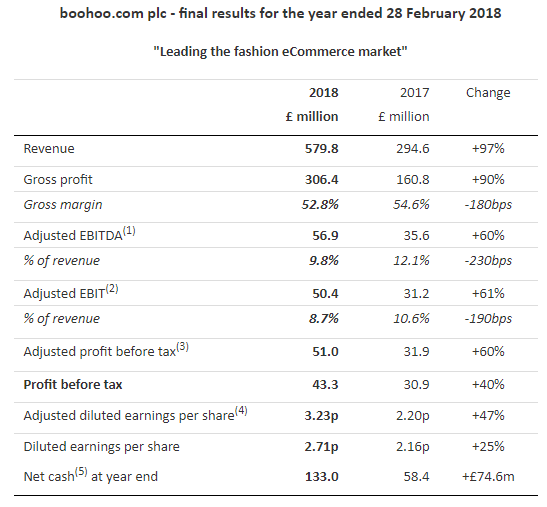

Voyager RNS Log WC 22/04/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Starting with a Green: what I would say about these notes are that they are honestly and simply my interpretation of the newsflow RNS issued by companies within the Voyager portfolio. If I think something is encouraging, then I will say so. Equally, if I feel a company has temporarily gone off the rails, again I will say so as honestly as I can. Oh, what a Saturday at Carlisle as the Hatters gained promotion into League 1; such joy. I absolutely love the passion in football, the emotions, the highs, the lows and also having a couple of beers with friends and local supporters on my travels. I think that something like this actually helps an individual as an investor as in my case the drainage of the emotional side of my brain with sport leaves no emotion for stocks which is a good thing in my opinion. Stocks are simply vehicles that after hopefully diligent research, will in maybe half of the purchases, react well whereas those that appear as one of my less worthy decisions are jettisoned with barely the shrug of a shoulder. Why am I such a fan of RNSs? Well, simply they are my rapid window into what is happening within the business. Companies provide so much valuable information and whilst you have to sometimes dig through the director speak clutter & CFO “adjustments”, it’s not that hard to do and all there for free without the personalised interpretation of a journalist. Also RNS’s are great as with a bit of sifting you get as close as you can to the real vibration of what’s going on in the business. Why is this important? Well for absolutely years now I have been banging on about “investment noise” you know the stuff we see in newspapers, investment magazines, social media etc: there is just so much of it these days that bombards the PI with advice and tips. I honestly feel that PI’s should Do All They Can To Tune Out The Noise it simply a distraction; apologies for shouting! To supplement the RNS service, the private investor has the opportunity if they so choose, to attend AGMs, exhibitors, ShareSoc events etc to talk to the directors of a business. However, just a cautionary word that such events would be absolutely invaluable if the senior directors were all fitted with polygraphs calibrated to detect fibs and misalignment of claimed prospects with reality; it’s just the odd few fibs as sometimes CEO can just become blinded by their tunnel vision, so, take care as you can't naively believe everything you are told. Having said that, once you are comfortable with the honesty and integrity of a companies directors such as Somero, then really listen to what they have to say. This week we have Mello 2018 but that is not what I would define as noise; it’s much more sound educational mentoring from well-respected investors who are speaking at the event. Incidentally, a great deal of the mentoring I received back in the late 90’s early 2000’s was from one of the smartest investors I have known, Jim Slater and believe me, this type of learning is invaluable. Before we go onto this weeks RNS review, I will reiterate possibly the most important lesson I have learnt in 30 years of investing and I will do it in the form of a straight copy & paste from the 2017/18 review article on the blog page of this site:  Onto the RNS news flow: Monday 23/04/2018: D4t4: Mkt Cap £50m: Year End Trading Update RNS:  My View: A fair bit of waffle in the TU in my opinion and whilst in overall terms things look reasonably decent, I note that that the revenue is seen as £20m compared to analysts expectations of £23m: something to keep an eye on and this combined with a touch of profit-taking probably depressed the share price by a few %. We of course have the almost obligatory adjustments profits to paint the rosiest of pictures which is downright annoying when the adjustments include share-based payments; is not that a company cost i.e directors total remuneration package? The TU is mo more than reasonable in my view but for now I am tempted to continue to hold. Also, a quick move early on Monday morning to close my AA spread bet for a nice profit. Tuesday 24/04/2018: RWS: Mkt Cap £1254m: RNS Trading Update: Half Year Trading Statement RWS Holdings plc ("RWS", "the Group"), one of the world's leading language, intellectual property support services and localisation providers, today provides an update on trading for the half year ended 31 March 2018 ("the first half"), ahead of the announcement of its half year results on 7 June 2018. Trading & Financial Update RWS has performed well during the first half, albeit has faced significant exchange rate headwinds as flagged in our AGM statement in February 2018. Notwithstanding these headwinds, the business has achieved revenues of GBP139.6 million for the first half, compared to GBP76.6 million in the first half of 2017, broadly in line with our expectations. The Group expects to achieve Adjusted PBT of at least GBP30.0 million in the first half on a constant currency basis, broadly in line with our expectations for the full year which continue to anticipate a second half weighting. However, the average exchange rate for the first half was $1.37: GBP1, compared to an average of $1.24: GBP1 during the prior year, meaning that we expect the Group to achieve Adjusted PBT of at least GBP28.3 million including the currency effect. The Board will continue to monitor exchange rates over the remainder of the year. However, if the current rates prevail, we would expect a profit outcome slightly below market consensus. This first half saw a steady performance from our Patent Translation & Filing division, following its record performance in 2017, reflecting a strong contribution from our Worldfile product offering and good growth in our Chinese operations. Patent Information continued to perform well (+11%*) and Language Solutions has seen the benefits of last year's restructuring (+11%*). We also saw an excellent first half from our Life Sciences division (+9%*). The successful integration of our two US acquisitions in the space, LUZ (acquired in February 2017) and CTi (acquired in November 2015), has delivered very positive results and enabled the division to grow revenue with several key customers. Our acquisition of Moravia, which completed in November 2017 for a cash consideration of US$320 million, has brought the Group a leading European provider of technology-enabled localisation services to some of the largest technology companies in the world. The acquisition enhances RWS's global presence, adding operations in the Czech Republic, USA, Japan, China, Argentina and Ireland; provides further geographic diversification; and adds an additional profitable, cash generative division of scale to the Group. Since acquisition, Moravia has continued to grow its relationships with its existing major technology clients; however, with over 95% of its revenue in USD and the majority of the cost base in Euro/CZK, the business has seen foreign exchange headwinds. In addition, its performance has been held back by a lower volume of activity than expected from a few clients. Despite this, we are encouraged by Moravia's first half client wins and its pipeline of new opportunities. The integration process is proceeding well and, in particular, a higher level of synergies has been identified which will deliver additional annualised cost savings. My View: well quite a few things that make me feel uncomfortable as follows: albeit has faced significant exchange rate headwinds: Normally I am not overly bothered with exchange considerations especially if I intend to hold a stock for a long time but it just concerns me that this is the very first thing mentioned in the trading update: possibly to divert us and buy a little time. achieved revenues of GBP139.6 million for the first half, compared to GBP76.6 million in the first half of 2017, broadly in line with our expectations: Now that’s director speak to say income will be at the bottom of analysts expectations or in my words let’s say likely not to meet market expectations in turnover. Adjusted PBT of at least GBP30.0 million in the first half on a constant currency basis, broadly in line with our expectations for the full year: Again, that’s director speak to say profits will be at the bottom of analysts expectations or in my words let’s say an almost mild profits warning. Maybe not such as issue if the share traded on a PE of let’s say below 15. Then the RNS goes on to give a further little warning: However, if the current rates prevail, we would expect a profit outcome slightly below market consensus. So, profits in the second half of the year could not be a little less than needed to meet today's TU which in itself is a mild profits warning. Then we have: In addition Moravia, its performance has been held back by a lower volume of activity than expected from a few clients. So, another possible pothole to rock the cart if things don’t improve in the second half of the year. Finally on my don’t like list, based on this TU, RWS is, in my opinion, going to have to motor ahead rather fast and have a good H2 in order to reach brokers consensus forecasts. All in all, whilst I accept that RWS is a quality business, it may have temporarily be having a little wobble, maybe a touch of indigestion after swallowing Moravia, which leads to uncertainty and with a share that is highly rated in PE terms, that just does not give the market's confidence. I did a very quick “first impression” of the TU on the iPhone whilst drying off after the morning swim (it was only 0725 in the morning and it caught me with my knickers down if you follow; my changing room reading of the RNS); got home before the market open to dig a little more and as is normal for me in these circumstances decided to sell as early as I could. Overall, I got a decent price and took a fall of 11% on last nights price. As I always say, you are not going to get all of your stocks going in the desired direction and that’s just not within your control but you can manage downside risk by jettisoning a stock from the portfolio, in this case the Voyager, when risk is identified. Tuesday 24/04/2018: AB Dynamics: ABDP: Mkt Cap £178m: RNS is about:  Tony Best, Chairman of AB Dynamics, commented: "We are pleased to report on an excellent start to the current financial year based on a strong commercial performance. We have built a good forward order book, both for the remainder of 2018 and into next year which gives us confidence in meeting market expectations. The Group continues to invest in its people, products and facilities, and we now have 130 employees, an increase of 41% over the last year. We continue to evolve our structure to support a large and growing installed base of equipment and systems across the world, whilst also ensuring we carry on delivering the innovative new products and services that our customers expect. During the period, we established a new operating entity in Germany which will provide improved customer support and a local engineering resource. The Board is pleased to announce the increased dividend to shareholders of 1.465p per ordinary share that is supported by the strength of our business and future prospects." Tony Best went on to say: We are pleased to report that the forward order book provides a sales pipeline for the remainder of this financial year and into the next and we look forward to the full year with confidence. My View: a very sound set of results with revenue up by 39% and PBT up by 34%. Oh yes, once again we have the adjustments for the dreaded “share option costs” this is really part of the remuneration package which is simply part of the cost of running the business so should be accounted for within Cost Of Sales. Apart from that, nothing I can see there to cause concern in fact quite the opposite, they instil confidence. If you strip out the share options costs from H1 for 2017 & H1 for 2018, we have operating profit @ H1 increasing from £1.6m in 2017 to £2.9m in H1 of 2018 which is a very appreciable rise. Doing a quick fag packet set of calculations based on the half-year results and the broker's consensus full year, these are very good H1 results and I rather expect that they will comfortably beat the current consensus forecast for 2018. An innovative quality company delivering a very good ROCE and high-profit margin. In my opinion, it’s making splendid progress and I am very happy to continue to hold plus I will be looking to add further should we see a price dip in the coming weeks. Wednesday25/04/2018: Persimmon: PSN: Mkt Cap £8.3b: Trading Update RNS: Persimmon plc ("the Group") announces the following trading update covering the period from 1 January 2018 to date, ahead of its Annual General Meeting ("AGM") which is being held at 12.00 noon today. Since the start of the year has been encouraging with the Group's total enquiry levels running c. 13% ahead of the prior year. The Group's forward sales position remains very strong with total forward sales revenue, including legal completions taken to date in 2018, of £2.76 billion, being c.8% higher than last year (2017: £2.56 billion). As announced on 27 February 2018, additional payments under the Plan of 125p per share will be paid over the next three years in late March/early April each year. The first of these additional payments of £389 million, was paid to shareholders as an interim dividend on 29 March 2018. At the same time the Board recommended that the scheduled return of 110p per share, or c. £345 million, will be paid to shareholders on 2 July 2018 as a final dividend. With the scheduled payment on 2 July 2018, the total value of the capital returned by that date of £2.22 billion will be £1.36 billion greater than that originally planned at launch in 2012. The additional payments over the next three years will bring the total value of the Plan to £13.00 per share, more than double the £6.20 per share original commitment made by the Board in 2012. The total value of the Plan is now c. £4.07 billion. My View: listed above are a few selected snippets from the trading update and whilst accepting that PSN operates in a cyclical market, that direction on that market still favours the patient shareholder. Absolutely no complaints from me with a near 100% return on a generous slice of PSN tucked away into my ISA immediately after that surreal Brexit referendum in mid-2016. Can’t see any reason not to continue to hold at the moment. However, I feel that the proposed £75m bonus even if it is to be offered in shares to the CEO, is simply outrageous but I suppose that when it rains gold from the skies, the hard working CEO’s put their buckets out to catch the free gold. Anyway, maybe the greedy grabbers won't get the buckets of gold, after all, see link: www.moneymarketing.co.uk/aberdeen-standard-votes-excessive-pay-persimmon/ Wednesday25/04/2018: Boohoo: EPIC: Mkt Cap £1775m: Final Results RNS:  Outlook and guidance

Trading in the first few weeks of the 2019 financial year has made a strong start. Group revenue growth for the next financial year (FY19) is expected to be 35% to 40% with adjusted EBITDA margin between 9% to 10% and capital expenditure of £50 to £60 million. Looking beyond the current year we will continue to lead the market on value, service and proposition in all our key geographies. Whilst this will require a continued investment in people and infrastructure, we believe that the benefits of our investments in marketing and warehouse automation will generate economies of scale to allow us to drive sales growth of at least 25%, whilst maintaining a 10% EBITDA margin. My View: As a previous holder who enjoyed a comfortable profit albeit maybe an overly early exit on BOO in the past, as I wrote last week after much deliberation waiting to re-enter as the price continued to fall, I bought again last week well aware that there was a risk involved just one week ahead of the year-end results. The Free Cash Flow (FCF) has increased from £5.4m for 2017 to £29.8m for 2018 whilst the ROCE still hovers around 30%: it all spells out as a quality business very much enjoying its moment in the sun. The results have been well received by the market and I am sure that as this one is such a darling of private investors having been championed by the very worthy Paul Scott in the past; there will be some relieved investors today. I am happy enough and will continue to hold. Thursday 26/04/2018: Taylor Wimpey: TW.: Mkt Cap £6.3b: Trading Update RNS: UK current trading The underlying housing market has remained stable in the first four months of 2018, with continued good accessibility to mortgages at competitive rates. During the first few weeks of March, the poor weather conditions had a noticeable impact on sales and build rates but activity has since recovered. Solid consumer demand continues to drive a healthy sales rate against a very strong comparator. Average private sales for the year to date were 0.85 per outlet per week (2017 equivalent period: 0.93) in line with our expectations. Cancellation rates remained low at 13% (2017 equivalent period: 10%). As at 22 April 2018, our total order book value stood at approximately £2,155 million (2017 week 16: £2,210 million). This represents 9,050 homes (2017 week 16: 9,219 homes), excluding legal completions to date. My View: a rather uninspiring update I felt and decided it was time to take profits so sold on the morning of the RNS; whilst my sale was some way off the top of the market price of 210p back in early January, the fact is that in a long career of investing I reckon I have only sold at the top on a handful of occasions: Never feel you are clever enough to buy at the bottom and sell at the top; it just doesn’t happen apart from the “smart crew” on bullectin boards & we all believe them don’t we! TW was one that has earnt its keep in the high-yield portfolio (that massively unexciting stuff) delivering a return of over 15% in the year but I felt that the update may lead to some drift and really time to move on as I have plenty of housebuilder exposure in a PSN & also the TEF a company as I rate as the most exciting in that sector. Friday 27/04/2018: Air partner: AIR: Appointment of Interim CFO RNS: Air Partner PLC is delighted to announce the appointment of Chris Mann as Interim Chief Financial Officer. Chris is a chartered accountant who has worked in finance positions at senior level within a range of listed and private companies, most recently with KONE Corporation and Gatwick Airport Limited. Chris will remain with the Company until a permanent Chief Financial Officer is appointed in due course. He will not be a director of the Company, nor a member of the Board. My View: decent move and an apparent safe pair of hands to draw a line under the previous accounting issues and hopefully swiftly move on. Whats On the horizon next week: To be honest, next week looks a little dull and I can’t see any Voyager companies with H1 or H2 results pencilled in or for that matter and trading updates that coincide with the same period as last year. This weekend sees the Hatters final League 2 home match for hopefully some years and then it’s onto League 1 for next season. Strangely in football, I have always had this theory that clubs get promoted to reach an equilibrium between competence and incompetence so let's see what next season brings. Certainly, there will be lots of different town & cities to visit and for me, that’s all part of a great day out. I am already looking forward to the Stadium of Light in Sunderland which will give me an excuse to call into Hartlepool for a couple of swift ones in that superb real ale bar called The Rat race. Happy investing; catch you all next week

1 Comment

Voyager RNS Log WC 15/04/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. I see that early in the week that Tim Martin, the very unique character and chairman of Wetherspoons decided it was time to pull the plug on his companies involvement with social media; good for him I say. I appreciate Tim’s reason were other than my comments that follow but I really feel that the likes of Facebook messaging and telling the local burglar that you are out for the night partying, has a lot to answer for. A couple of months ago in a really fine pub in Rydal Cumbria, a family of four, parents plus two young teenagers and also a rather nice dog, came in for a bar meal. The parents tried to start a sibling inclusive conversation but the two teenagers remained totally glued to their smartphones and the only conversation that came from their lips the entire time they were there was a “yes” when asked if they would like ice cream for dessert. The dog who did not have a clue about smartphones or Facebook was very social: what a world! Where has conversation gone? Is it just in cyberspace? I quick thought on last weeks benchmark blog: just to be clear, I certainly don’t mean tracking an index or fund but really just my encouragement for private investors to continuously try improve their investing by looking at what the quality boys do and over say 5 years. If they are continually ahead of you and you simply can’t change your habits and importantly assuming you invest to increase your wealth, then think about giving up and asking a successful manager to look after your pot. On to this week's log: Monday 16/04/2018: No RNSs relating to Voyager holdings: Tuesday 17/04/2018: No RNSs relating to Voyager holdings: Wednesday 18/04/2018: IG Design: IGR: Mkt Cap £275: AIM Market: RNS is about: Increasing revenue and improved margins driving strong growth IG Design Group plc, one of the world's leading designers, innovators and manufacturers of gift packaging, greetings, stationery, creative play products and giftware, announces a trading update in relation to the year ended 31 March 2018. The Group's trading accelerated in the second half of the year with all regions delivering strong revenue growth and increased profits. As a result the Board anticipates a full year of overall progress and financial performance in line with management expectations. The Company's results for the full year to 31 March 2018 will be announced on 11 June 2018. Highlights - The Group's gross and net margins have increased driven by strong performances across all of the Company's global operations, with the previously flagged cost headwinds having been effectively mitigated - Net cash ended the financial year positive, after having completed the acquisition of Biscay Greetings in Australia, the disposal of part of the Hirwaun site in the UK and with record levels of capital expenditure invested during the year - Average leverage during the year is expected to have been below 1.5 x EBITDA (FY17, 2.3x EBITDA) - The Board remains committed to its progressive dividend policy and is considering increasing the Company's earnings pay-out ratio in future periods, to reflect both the improved financial performance of the Group and the positive outlook of the Directors. My View: IGR is one of my major holdings as there is just so much I like about the company: The company is run by competent management who understand their market. Senior directors have a good level of share ownership. IGR makes real profits increasing year on year. The company makes decent returns on capital. The dividends whilst being a touch mean as the company has invested should appreciate in the future according to management. The newsflow from IGR continues to be very encouraging. The table below from SharePad gives a nice summary of some key numbers as we stand and the key ratios which already look interesting will be updates when the finals are published in June.  Taking a look at risk: Just need to keep an eye on net debt over the coming months. For those who like the security of a high Stock Rank, IGR comes in at an impressive 85. All in all, I am happy to retain my holding and may be tempted to but a few more on a share price dip. Having said that, I see this stock as a nice quality steady growth company that will appreciate over time; I doubt it will move like a rocket but that will do nicely for me. An interesting PI video recorded on Monday this week (PI World offer an excellent service): www.piworld.co.uk/2018/04/18/ig-design-group-igr-investor-presentation-april-2018/ Wednesday 18/04/2018: Telford Homes: TEF: Mkt Cap £320m: AIM Market Stock: RNS Trading Update: TEF tells us that they have had a “Strong performance reflected in circa three percentage point improvement in gross and operating margins”; all sounds rather good to me. Incidentally, the comparative table shows why I rate TEF so highly compared to other more popular building stocks:  My View: whilst this housebuilder has done nothing like the return that my other builder PSN which has kindly given over 100% return, TEF has more than earnt it’s keep in the portfolio yet seems to be somewhat overlooked by the markets despite having a first-rate management in charge. \for those who like Stock Ranks, Telford scores an impressive 89. Until the cyclical housing downturn kicks in, which it will, of course, one day, I am happy to hold this niche builder who concentrates on the chronic housing shortage in London. Wednesday 18/04/2018: Bodycote: BOY: Mkt Cap £320m: FTSE 250 Stock: RNS Contract win to supply Rolls-Royce: Bodycote, the world's largest provider of heat treatment and specialist thermal processing services, announces that it has signed a 15-year contract with Rolls-Royce's Civil Aerospace business. The contract is expected to be worth over GBP160 million in incremental revenues over the 15-year period. Sales will ramp up over the next five years. My View: yes another one of my exceedingly boring companies but as readers will know, I simply love boring companies. A decent and encouraging contract win to supply Rolls-Royce with over £160m over a 15 year period. Now in terms of turnover, the current BOY turnover is around £690m so that’s a pleasing but not massively significant £10m or so a year but it all helps. Thursday 09/04/2018: D4t4: Mkt Cap £55m: RNS Press Release: Essentially the statement is about encouraging progress with Celebrus. The RNS came out at 09:00 and the share price responded immediately adding a further 5%. Not much more to say really but looking rather decent and I look forward to their year-end results. Friday 20/04/2018: Bonmarche:BON: Mkt Cap £45m: RNS Trading Update For Year Ending 31/06/2018: The Company is pleased to confirm that, reflecting the good progress achieved during the financial year, the FY18 profit before tax will be in line with the Board's expectations. Online sales maintained the strong growth seen throughout the financial year, against comparatives that became more difficult in the fourth quarter. Store sales performance was disappointing, reflecting the issues more widely reported in the clothing market. Whilst total sales for the year therefore declined slightly, the gross margin percentage was resilient. The lower headline gross margin that had been anticipated due to adverse FX movements, was largely mitigated through tight stock control and improvements to the loyalty scheme, which led to lower discounting. There were also significant overhead cost savings, delivered through improved operational efficiency and reduced, but more effective, marketing expenditure. Helen Connolly, Chief Executive Officer of Bonmarché, said: "As anticipated, trading conditions in the final quarter of our financial year remained challenging and, against this backdrop, I am pleased that we have delivered an increase in the FY18 profit before tax compared to last year. "Whilst we expect the market to remain difficult, our focus will be on continuing to improve our proposition to customers through a number of self-help initiatives, which we expect to drive further progress for the business during the new financial year. My View: At BON and in common with a lot of other retailers, the high street continues to experience fairly tough times. However, I think that Helen Connolly is doing a good job at BON since her arrival. The interesting part is the continuous percentage increase in LFL sales of the online offering yet against this we have to balance that online was accounting for about 10% of total turnover at the half-year report; if on-line contributed say 30% of total sales then I would feel much more positive about the stock. This is in truth only a very small position for me and bought in May last year as a recovery situation and it may well be one that I have got wrong even though it’s just about cost neutral with that generous 8% yield. Probably time to move on with this one; you can’t win them all! Other Thoughts On Previously Held Stock: I thought I would offer a few comments on stocks where I sold once I saw bad news breaking, each of these companies has released an RNS during this week: Galliford Try: GFRD: Not really an RNS but those mean chaps Peel Hunt has reduced their price target for Galliford Try down to 1165p even by my standards that’s a touch mean and over a £ less than I got in my sale following the RNS on 15/01/2018 informing up about their Carillion liability. Now whilst GFRD does not tick the boxes as a buy for me at moment, I rather think that Peel Hunt are a touch pessimistic long term. A decent company in their in my opinion but maybe I am being overly sentimental having had a long association with them back to the time they were under £3. I reckon that in the medium term GFRD will be fine: I do not currently hold a position either long or short in GFRD but do feel slightly tempted as I can see a 20% total return on these over the next 12 months. SPRP: A couple of years back I sold my holding in SPRP on the morning of their trading statement on 18/04/2016 relating to battery issues and have never been tempted back since. The RNS of 19/04/2018 “The Company continues to take legal advice, and is in communication with BRK, with regard to the Termination for Breach Notice, the allegations made by BRK and its position. The Company disputes the allegations made by BRK. A further announcement will be made in due course. The gross book value of the disputed stock of unsold BRK products was GBP4.3m as at 31 March 2018. Whilst discussions with BRK continue, the Company is unable to confirm the expected date for release of its audited final results for the year ended 31 December 2017. A further announcement will be made in due course. The Company announces that in late January 2018, it entered into a committed 3 year revolving credit facility with HSBC Bank plc for GBP7.0 million to fund the Company's working capital. On 29 March 2018, the Company drew down GBP3.0 million of this facility”. Apart from the destruction of investors wealth, this situation as SPRP is really looking a bit of a muddy mess with simply insufficient clarity as to what is really going on. In addition, sadly, I simply don’t think that the management are strategically that switched on; simple as that. In order to invest in a business, I have to have confidence in the management and SPRP don’t really give me that confidence; I don’t think they cook the books but as I say, they just strike me as strategically naive and rather accident prone. However, having said that, if I were an investor, I would dig into the detail a touch in order to reassure myself that the high Capex/D&A ratio is sound and not a cause for concern; as I am not an investor in SPRP, I can’t be bothered to dig. Just to add to the lack of confidence, the group finance director resigned with immediate effect in March; see the 5th March RNS: it always worries me when I see the poor old CFO or CEO for that matter, leaving with immediate effect; walking the plank to be fed to the sharks! Also they have just drawn down on a £3m debt facility with the banks which I can’t quite understand as the most recent accounts claim to have something like £10m cash available on the books!! They really need to explain to shareholders the cash position in my opinion. With SPRP, it may all be perfectly innocent and part of the grand strategic plan & will no doubt be made a touch clearer in a future RNS. Incidentally investors will have a chance to put a few relevant questions to SPRP at Mellor next week. I do not hold a position either long or short in SPRP. Gattaca: GATC: If you forgive the expression, “when you smell a rat, get out” and sadly this has been the case for the perennial destroyer of investors capital and again I see it as a case of poor strategic management. You may remember that they were originally under the sensible name of Matchtech and whilst under that name their share price rose from 240p in early 2013 to 640p a mere eighteen months later. Then it seems that management simply lost it sadly at a time when others in their sector continued to prosper. They probably paid vast sums to some image consultants to advise them in making that dreadful name change to Gattaca; just what the heck does that name mean? I sold my shares back in 2016 when I just simply no longer felt I had confidence in the management of GATC; since that time the share price has constantly dwindled down to Thursday mornings 145p. As I always say, if in doubt, get out. Note: investors had plenty of red flags including the immediate resignation of the CEO in early February and a sale at that time would have at least protected an investors capital a touch more than today's share price. I do not hold a position either long or short in GATC. Finally, an RNS from another incredibly boring business but this time one I sold back in early 2017 when the share price just about tripled my original investment yet there was still a little more to come but that’s investing! The company in question is Trifast: TRI and again a very well managed business but at the time, I felt that its valuation was becoming maybe a bit stretched yet since I sold it has put on another 20%, so what do I know? On Thursday they released an encouraging RNS “slightly ahead of expectations”. TRI still ticks a lot of boxes for me as it is a class act but I doubt I would return unless that really did something about that measly dividend of 1.4%. Also this week, I have been busy topping up Somero (SOM), buying back into a previous “profits taken holding” BOO and actually purchasing a share from the past that at one time did very well for me, Restaurant Group (RTN) plus taking a spread bet in AA; you may remember I wrote about the sad demise of AA a couple of months ago. So why am I buying into these two losers you may well ask (in fact, I may well be asking myself that question in a few months time, plenty of time to get egg on my face). In the case of RTN, since the finals on 07/3/18 the CEO and CFO have been buying very significant numbers of shares; £170k worth between them, the still generous dividend looks to be covered by FCF although this could be cut should they need more capital (might be a sensible move). Finally, the chart looked rather compelling and I bought in on Monday:   In the case of the AA, I opened a spread bet on Monday: again really significant CEO & CFO purchases of shares in recent days again at a combined value of £170k. Once again the chart was looking rather compelling:  Whats On the horizon next week:

Results: AIR, ABDP & BOO (I have just taken a modest position in BOO after the rather the >40% fall in share price over the last 6 months: will I regret it?). AGMs with TU’s from PSN & TW. Ex-Dividend: LGEN & PMP This week I have been just a bit to busy enjoying the nice weather and revamping a few items in the garden; so, sadly no walking in the lakes. Instead, I will head for Cumbria, Carlisle, leaving home about 5:00 am on Saturday morning to catch the 06:40 direct service to Carlisle. A win for the Hatters will see us back in League 1 but in truth, we only need two points from the remaining three games and that’s IF the other hopefuls each win their final three games: I reckon we are nearly there! Have a great weekend and enjoy our summer which usually lasts for about five days! Happy investing; catch you all next week Voyager RNS Log WC 08/04/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Oh, What A Noisy World! Twitter: I do like Twitter and it’s a great place to keep in touch with fellow investors but without care, it can become very hungry on one’s time. On the pro side you can get very rapidly the thoughts of other respected investors but on the con side, unless you really manage your Twitter time well, you could get sucked into a black hole of noise. It’s something that I have become increasingly conscious of these last few months. In some respects, the time reading on Twitter may well be a compliment to the very readable comments made by other investors and certainly, the links often posted are first class. However, like most things in life its quality of information rather than quantity that counts: with shares you can easily sieve characteristics to get to the stocks that may be of interest to you but with Twitter with those that you follow, there are no real shortcuts; well at least not any that I am aware of. Thankfully some of the most respected successful investors are relatively infrequent Tweeters and when they do tweet you really take notice of what they have to say. It's really just an observation and one that runs alongside the drum I have been beating for years now about cutting the market noise. Incidentally, the idea about market noise first came to me many years ago whilst flying to Australia. The plane was an old QANTAS beast and noisy as hell until I put on my “oh so flashy” noise reducing headphones: bliss, I could think again as I deliberated Sharescope on my laptop. That’s when I thought how great it would be to cut out market noise and that’s what I do with a passion these days; I honestly can't recall the last time I bought IC magazine or similar; not knocking them but they just simply add to the noise. For me, decision making within investing is about the financial numbers & ratios, the RNS flow from the companies that make it to the Voyager universe and a mandatory need to have as far as we can tell, a credible CEO & CFO running each particular business. On the other hand, I do read the comments of some of the thoughts of a number of very astute investors on the Twitter and also regular articles posted by excellent commentators including such as Paul Scott (Stockopedia), Phil Oakley & Richard Beddard (both on SharePad): these guys actually try to educate the private investor with relatively infrequent but quality analysis. It’s then up to the individual investor if they choose to be spoon-fed or learn from mentors and make their own investment decisions. As for managing my time on Twitter, I now try to limit myself 15 minutes in the morning and 15 minutes in the evening or at least that’s what I try to do until somebody includes a useful link that I simply can’t resist reading: blast, there I go again, time ticks away with Twitter. Anyway, let's have a look at what’s being going on in the Voyager Universe this week. Monday 09/04/2018: Keywords Studios: KWS: Mkt Cap £1060m: RNS’s are about:

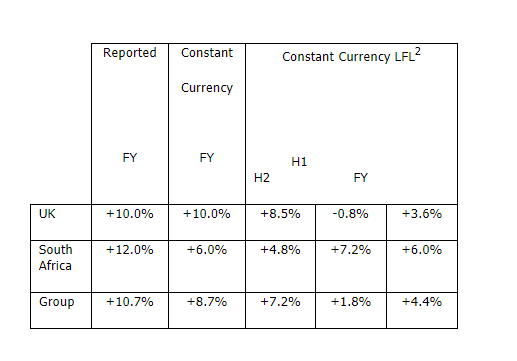

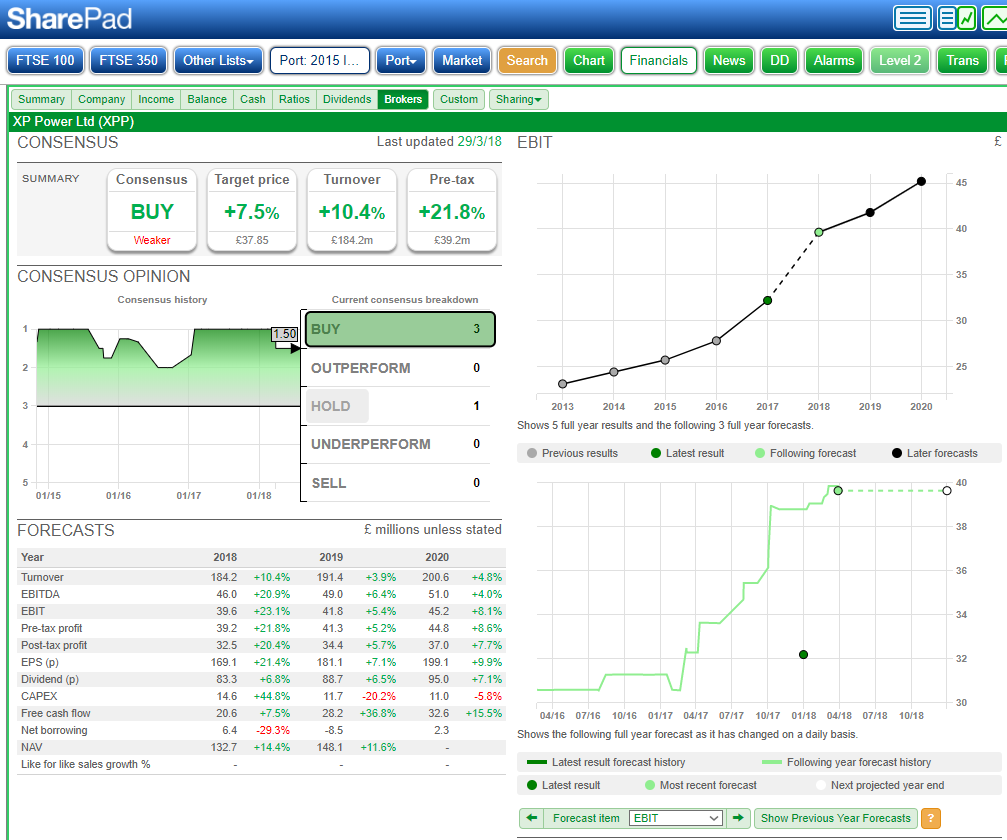

Financial overview: Group revenue (including effect of acquisitions) increased by 57% to €151.4m (2016: €96.6m) Adjusted EBITDA* up 57% to €26.3m (2016: €16.7m), representing a margin of 17.4% (2016: 17.3%) Adjusted profit before tax* increased by 55% to €23.0m (2016: €14.9m) Adjusted basic earnings per share* up by 52% to 31.18c (2016: 20.59c) Adjusted operating cash generation** increase of 48% to €21.9m (2016: €14.8m) Net cash*** of €11.1m (2016: €8.7m) Final dividend of 0.98p (2016: 0.89p); 10% increase in total dividend to 1.46p per share (2016: 1.33p) My View: the numbers themselves are right at the top end of the revised market expectations; the revisions being made when KWS provided a strong trading statement back in early February this year. There are of course lots of adjustments but this is inevitable with a company growing at the rate that KWS and continually making bolt-on acquisitions but nevertheless the numbers are highly impressive. The market, which is incidentally highly fragmented, for the work that KWS offer is simply huge and the CEO Andrew Day, estimates this to be $5 Billion; that’s some market and KWSX is now becoming recognised as a “go to” provider for many of the requirements of this huge market. Incidentally, it’s well worth a look at the results presentation that KWS did on Pi World this Monday, Link: www.piworld.co.uk/2018/04/09/keywords-studios-kws-fy-results-presentation-9th-april-2018/ Regular readers will know that I first bought into KWS back in mid-2016 when the shares were just over £3 and did make several top-ups as the “beating expectations” RNSs kept flowing. I eventually reached a point where the percentage of KWS in my portfolio was becoming a touch sill and that together with my ongoing thoughts about the risks associated with managing so many acquisitions, lead me to sell some shares in kws to the value of my original investment: just simple risk mitigation. However, due to the continual upward trajectory, despite my top-slicing, KWS remains as one of my most significant stocks by percentage value shares within the Voyager. At the moment, I am happy to continue to hold and hopefully sleep well. Tuesday 10/04/2018: D4t4: D4t4: Mkt Cap £50m: RNS Trading Update & Contract Wins: The Company is in the process of its year-end close and intends to provide a more detailed update on financial performance on 23 April 2018, in advance of this, the Directors are confident that the revenue and adjusted* profit before tax will be ahead of the comparatives for the year ended 31 March 2017. Details of the recently converted opportunities are as follows: Data Management: · A major multi-year contract with a global US headquartered financial institution for our Private Cloud Data Analytics solution. Data Collection: · A new contract for our Celebrus data collection software with a Taiwanese bank. · An extension of a global contract in the financial services sector with the addition of a new data collection channel using our Celebrus data collection software. · A capacity extension contract for our Celebrus data collection software with a major online retailer in the UK. · A capacity and functionality extension contract for our Celebrus data collection software with a major online retailer in the UK. · A capacity extension contract for our Celebrus data collection software with a major European retailer. · A new contract for our Celebrus data collection software with a major Japanese car manufacturer who will be utilising our GDPR compliance functionality. *Adjusted for amortisation of acquired intangibles, share based payment charges and foreign exchange losses. My View: I did write a few months back that when D4t4 released that ”results will be weighted to the second half of the year” RNS, that I greatly reduced by holding again simply as risk mitigation. Well, although I am fairly ruthless in jettisoning a risk to the portfolio, once I feel confident about better news then I am happy to either but back in or consider increasing my holding. I thought that this RNS was both reassuring about this year’s prospects and the new contract wins certainly add more confidence in going forward. The one thing I did not like about the RNS was the vague wording “profit before tax will be ahead of the comparatives for the year ended 31 March 2017”. Just why not say we will meet market expectations and save the poor investor some legwork in terms of chasing back through historis reports? All in all, I am happy as I bought back my previously sold stock at a lower price than I had sold them for and the share price looks to be appreciating nicely: happy enough with that one. Wednesday 11/04/2018: Norcros: NXR: Mkt Cap £150m: RNS Trading Update: Group underlying operating profit for the year is expected to be in line with the Board's expectations. Group revenue for the year is expected to be in the region of £300m (2017: £271.2m), 10.7% higher than the prior year on a reported basis, 8.7% higher on a constant currency basis, and 4.4% higher on a constant currency like for like basis2.  UK revenue for the year was 10.0% higher than the prior year reflecting in part the first time contribution from Merlyn which was acquired on 23 November 2017. Merlyn has been seamlessly integrated into the Group and performed in line with the Board's expectations. On a like for like basis2, UK revenue was 3.6% higher than the prior year. Second half UK LFL revenue declined by 0.8% compared to the 8.5% growth seen in the first half. This was largely due to lower retail revenues at Johnson Tiles and a tough comparative period last year. Johnson Tiles apart, H2 UK LFL revenue was 8.4% higher (H1 +11.4%). Our South African business again delivered strong revenue growth despite a challenging market environment, 6.0% higher than the prior year on a constant currency basis and 12.0% higher on a reported basis, continuing the sustained progress of recent years. Reorganisation - Johnson Tiles UK In 2017 we implemented a restructuring at Johnson Tiles UK designed to improve its operating performance and increase manufacturing flexibility. Notwithstanding the benefits of this restructuring the business remains loss making as market conditions experienced in the second half proved more challenging than expected. As a result, the Board has implemented a further restructuring programme which will involve the loss of up to 50 jobs. This will result in a charge of around £2.1m, to be treated as an exceptional item and recognised in the financial year ended 31 March 2018 with the subsequent cash outflow occurring in the first half of 2018/19. Annualised savings are expected to be at least £2m. Financial position Closing year end net debt is expected to be around £48m (2017: £23.2m), in line with the Board's expectations. Pro forma Net Debt to EBITDA is expected to be circa 1.3x, in line with the guidance at the time of the Merlyn acquisition. My View: I greatly reduced my position in NXR which formed part of an Income portfolio, towards the end of February (see earlier blog notes). I still like the company and it had indeed delivered all one could ask for in a high yield portfolio but I felt as the market continued to be blinded by the pension issues that it was time to take a 50% or thereabouts top slice. Incidentally, those pension issues as I write so often, are simply not a serious issue as the pension fund is closed to new entrants and the average age of members in now in the early 80’s. I am happy to hold my remaining share and trust the issues that have held the company back at Johnson Tiles will be sorted shortly. I always feel for employees that are to be made redundant, I have done enough of that “breaking the bad news” in my career but a quick fag packet look at the numbers suggests that the staff will be treated reasonably well. Without doubt whilst the accountants who run NXR may be described as a safe pair of hands, their RNSs and presentations are as dull as dishwater completely lacking in inspiration but I will nevertheless hold my reduced holding for now. Wednesday 11/04/2018: Air Partner: AIR: Mkt Cap £47m: RNS FURTHER UPDATE ON ACCOUNTING REVIEW: Our review has made good progress, and is ongoing. At this stage, we believe that the total cumulative impact arising between the financial years ended 31 July 2011 and 31 January 2018 will not exceed £4m. The final amount will be confirmed to the market after completion of the review. In accordance with accounting practice, amounts relating to prior periods will be recorded as restatements of comparative financial information. Any amount attributable to any period will be treated as a non-cash item. On the advice of its advisers, considering the work required to restate appropriate historic accounts and complete the full year audit, the Company believes it prudent to reschedule the announcement of its full year results for year ended 31 January 2018 from 26th April 2018 to 31 May 2018. The RNS then goes on to reassure by After appropriate restatements, the Board expects that the Company will have sufficient distributable reserves to pay dividends. The Board intends to recommend that the final dividend payable for the year ended 31st January 2018 will be 3.8 pence per share. The Board further wishes to take this opportunity to reaffirm its ongoing commitment to its dividend policy, which targets cover of between 1.5 and 2.0 times underlying earnings per share. On 6th February 2018, the company announced, "underlying pre-tax profit for the financial year ended 31 January 2018 is expected to be not less than £6.4m". Prior to adjustment for any expense attributable to the period arising from this matter, this statement remains valid. The Group currently maintains a strong balance sheet with over £8.6m of its own cash at the end of March 2018. Any one off costs and fees associated with the review will be expensed in the financial year ended 31st January 2019 and clearly identified as such. Whilst our review is ongoing, we will not comment on rumour or speculation, and shareholders should expect official statements to be issued to recognised Regulatory Information Service providers as appropriate, ensuring full compliance with regulatory obligations. My View: well that’s quite a reassuring update from AIR and to a large extent dispels some of the market fears that AIR could become another CVR. In my view AIR was nothing like the CVR situation; with AIR somebody in the accounts department has been let’s say irresponsible with bad practice remaining undetected and whilst this is a worry, this RNS does clear the air ( I like that, clear the air). Last week I wrote in this journal that I sold all of my AIR at the opening and took my profits as the stock carried too much risk and could easily drop appreciably further and of course, it certainly did and indeed so much further than I expected and more than probably justified. Early on the day of this latest reassuring RNS, I bought back into AIR at a price very significantly cheaper than I had sold them at last week. I now see AIR as a special situation with, given time, an attractive upside but with a touch more risk that most of the other stocks within my portfolio. My view is that whilst even at the best of times the share price is prone to turbulence, this stock has potential given time for a maybe 25-40% upside. Note: although I do sell with a rather ruthless unemotional streak, and this is done in order to protect capital, I am very open to returning to that stock once the risk has diminished: recent in 2018 include PMP, D4t4 & AIR. For me, it’s all a question about acknowledging the risk, mitigating that risk and NEVER being too proud to either sell or repurchase once the situation has changed and the stock risk altered. Thursday 12/04/2018: WH Smith: SMWH: Mkt Cap £2180m: RNS Interim Results: The figures tend to show in my opinion that SMWH is possibly treading water a little this last six months:  My View: well after a very good association with SMWH which had delivered my a splendid return from one of my favourite “most boring” companies, it’s time to bid the stock farewell and bank the profits. It’s a lovely company and the travel section is still progressing well but the attractions in terms of ROCE/CROIC remain, I see limited upside and indeed by trailing stop loss has been pinging little messages to me since mid-February. For me, it’s time for now to bank the profits. Friday13/04/2018: XP Power: XPP: Mkt Cap £677m: RNS Trading Update: The Company has made a good start to the new financial year as the strong order intake reported in 2017 continued into 2018. Order intake in the first quarter of 2018 was £51.2 million (2017: £47.0 million), 9% ahead of Q1 2017 on a reported basis or 19% ahead in constant currency. On a “like for like” basis, removing currency effects and the impact of the Comdel acquisition, orders increased by 12%. Group revenue for the three months to 31 March 2018 was £46.6 million (2017: £39.6 million), 18% ahead of Q1 2017 on a reported basis, or 28% ahead in constant currency. On a “like for like” basis revenue increased by 17%. The Book to Bill ratio, which tracks the relationship between orders received and completed sales and is an indicator of future revenue growth, was 1.10 for the first quarter. Financial Position Net debt was £6.8 million at 31 March 2018 compared with £9.0 million at 31 December 2017. Dividend The Board has declared a dividend for the first quarter of 16 pence per share, a 7% increase over the prior year, which will be paid on 11 July 2018 to shareholders on the register at 15 June 2018 (2017: 15 pence per share). Outlook The momentum seen in 2017 has continued into the first quarter of 2018 and we are encouraged by the continued strong order intake experienced across the business and the book to bill level gives us confidence for the future. The Board’s expectations for the Company’s full-year performance remain unchanged. My View: A solid trading update from XPP and let’s remember this is for the first quarter of 2018 so you are quite unlikely to get “ahead of expectations” predictions for the full year at this stage. I have held XPP for a couple of years now and it has been a fine performer in the portfolio. I really do like the company as they offer so many of the attributes that I seek in a solid business: of course, like most stocks it is not without risk but with good management at the helm, you get a comfortable feel. For information the brokers forecasts are shown below; I see Stockopedia also allocates an attractive stock rank of 87 to XPP.  Friday13/04/2018: Air Partner: AIR: RNS Directorate Change: Following the announcement of Air Partner's intention to restate certain historic results, the Company today announces that the Chief Financial Officer, Neil Morris, has offered his resignation to the Board of Air Partner. This has been accepted, with effect from today. Neil will remain available to the Company to contribute to the ongoing review, in respect of which, there is no further update from the RNS released on Wednesday. The Company is reviewing candidates for the position of Interim Chief Financial Officer that are available immediately. Air Partner will be engaging an external recruitment consultancy to assist in the search process for a permanent Chief Financial Officer. My View: Well, no an unexpected announcement but nevertheless a touch cold as we don’t even have a “we would like to thank Neil….” In the statement and it makes it fairly clear that no internal candidates will be considered. I would think there will be a whole lot of changes in the finance department at AIR. Whats On the horizon next week: Let’s start with Sunday when I hope to do blog on the Voyager performance in FY 2017/18; it will be a fairly high-level overview in terms did the Voyager bear the benchmarks applied. I can’t see any results pencilled in for next week but would have thought that we could possibly see some Trading Updates from RWS, TEF, IGR & BON shortly. This weekend the stumbling Hatters have the opportunity to lurch a little closer to promotion when we take on Crewe at Kenilworth Road. I had better mention next week's game now as although I have a train ticket booked that gets me into Carlisle at mid-morning well ahead of the 3pm kickoff, I might just waste the ticket and take a couple of days around Grasmere before heading off to Carlisle; I will take a late decision on that one. If it is a few days walking in the Lakes then I may have to sacrifice next weeks voyager. Happy investing; catch you all next week Voyager RNS Log WC 01/04/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. This week a different introduction by saying that I am a mistrusting individual when it comes to the business culture of certain countries of the world; can’t see me ever changing that mistrust but should I just occasionally break my rule? I have a geographic deep mistrust with companies domiciled in certain countries and whilst I have absolutely nothing against the good folk of China, Israel, Russia or the wonderful African continent, I just don’t need to take the risk in terms of investing in such companies. I have to have faith in the accounting practices and honest news release of companies and unfortunately, countries as described in the areas above, simply do not give me that faith. Yes, I will miss out of some investments but simply put, I just don’t have the appetite for that kind of risk; I have to feel that I can trust the integrity of the directors of a company. In an investment club many years ago, we got our fingers burned with GEO Interactive Media/Emblaze; I personally had a fortuitously profitable but I consider lucky escape with Telit Communication when my some & mirrors digging raised some real concerns. I would suggest that any investor might find it worthwhile putting together some form of defence to guard against the “smoke & mirrors” merchants of the investment universe. Enough ranting about my mistrust of management, yet to be fair, if you don’t have that basic trust of the management practices on any business and that includes wherever they are domiciled, however can you either invest or remain invested? Anyway, on to this week's Voyager RNS. Tuesday 03/04/2018: Air Partner: AIR: Mkt Cap £60m: RNS is about accounting issues: YEAR END UPDATE The Board of Air Partner has identified, during the course of its year-end review process, an issue predominantly relating to its accounting for receivables and deferred income. Following preliminary investigations, the issue principally relates to the collection of receivables from customers and accounting for uncollected amounts since financial year 2010/11. Certain uncollected receivables were inappropriately offset against deferred income rather than being expensed to the income statement in the appropriate financial year. This is a non-cash item and has no bearing on the Company's cash balances. Whilst the investigation continues, the Board presently understands that the cumulative amount between financial year ended 31 July 2011 and the financial year ended 31 January 2018 is approximately £3.3 million and a significant proportion of this relates back to 2011. At no point was a customer, operator or supplier impacted or disadvantaged. Further, the Group continues to maintain a strong net cash position. My View: As ever when such news breaks, I carry out a very rapid risk evaluation and 95% of the time sell as soon to the opening bell as I can. In this case, I asked myself a few fundamental questions about management of AIR particularly as the RNS seems to have been rushed out without the management at AIR really knowing the full extent of the problem “Whilst the investigation continues”: Do I still have sufficient trust in the management of the business to have my capital invested? The answer was of course no; simply how can I with them having not just once but systematically made such an accounting error. Indeed will senior managers & directors bonuses that may have been paid in relation to such “profits”, be repaid? Will the ongoing investigations reveal more unfortunate errors? The answer is I don’t know but what I do know is that a risk that further unfortunate errors could be identified which could lead to considerable further downside and that risk does not sit easily with me. In such circumstances, I ask myself the very simple question: “If I did not hold this stock already, would I buy today given what the situation is now”? Again for me, the answer is NO. I originally bought AIR at just over 70p and have enjoyed decent dividends and a steady if sometimes choppy appreciation in share price but at the moment the stock simply carries too much risk to be comfortably retained within the portfolio and has been jettisoned and a very decent profit banked. As it turns out I got a very much better price by selling early than if I had waited until later in the day or indeed the next day or two when the shares fell another 20%. I did not sell at the top or anywhere close to it but that’s fine with me as it's been a capital benefit to the portfolio. I know that some investors are a little loath to sell on such news and worry about sunk dealing charges and whilst that may have been a worry with the silly dealing charges of 20 years ago, many brokers only charge a tiny £5 commission on a trade. I shall not bore folk with my whittling on about procrastination… Wednesday 04/04/2018: No RNS relevant to the Voyager portfolio but as retail appears to be under so much pressure, I decided to cash in my holding in Newriver Reit. Overall, it’s done ok for me but with the gradual demise of retail and the shopping experience moving so much to either the internet or tightening household purse strings, I just saw upside as not favourably balancing the potential downside. So it was a fond goodbye to an old friend from 2013 and time to move on. I have to say that in the past four months I have done considerable top-slicing of some positions that had just got a little too frothy; in hindsight, that was most definitely the right thing to do but the cash pile is now becoming a touch heavy. As ever, patience will be exercised in selection, execution and selling. However, it is becoming increasingly more difficult to identify good FCF/Returns on Capital stocks at attractive prices but I had to bite the bullet in late March and make a very late entry into Games Workshop as it dipped to the £22 mark. Do you know how many times over the last couple of years I have identified GAW as having so many characteristics that I look for in a stock yet my prejudice in terms of identifying with the business, prevented me from buying in early 2017. Never mind, maybe better late than never! Thursday 05/04/2018: No RNS relevant to the Voyager portfolio but I do keep running the rule over BOO; a share I sold for some decent profits and just keep questioning myself if it is still overvalued or getting into “buy back in” territory? I see a broker this week has placed a price target for what it’s worth, of 125p as they still feel the stock is overvalued at the mid 140’s: time will tell. I will simply keep on the watch list for now. I also set some time aside on Thursday evening to simply review over the last seven years records my “when there is a doubt get out” culture and quite honestly the picture is overwhelmingly positive. I would say that stock selection by whatever your chosen method may say on average give you a 50% or 60% win rate. Without a doubt in my view the crucial factor that differentiates the good performance from the average performance is how you actually manage those stocks that don’t perform: I could write a book about it! What saddens me is when private investors continually go into denial with an attitude of “it will come good, I am sure”. A massive character strength in investing is to acknowledge a not so bright prospect and move on. Friday 06/04/2018: No RNS relevant to the Voyager portfolio; lovely as I have some project work to get on with outdoors in the garden. Whats On the horizon next week: Two portfolio companies have reporting dates next week; one an exciting company and the other one an incredibly boring company; there is nothing with boring companies, I love them! 09/04/2018: Keywords Studios: Finals 12/04/2018: WH Smith: Half Year Finally, with the financial year closing, it’s time to calculate an allocation of profits to my two selected charities and pleasingly this FY has proved to be a very good investment return for me and therefore for my charities, Shelter & Prostate Cancer UK. Have a good weekend & catch you next week. Happy investing. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed