|

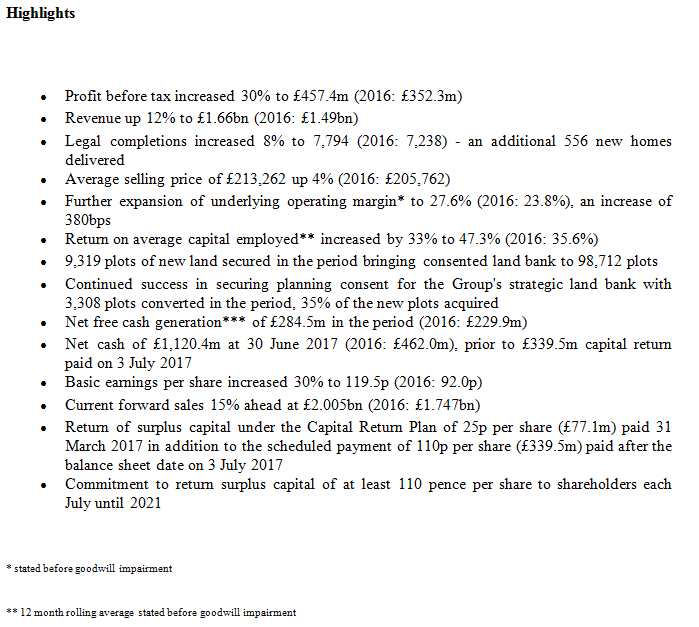

Week No 7 of The Voyager RNS Log: Week commencing 20/08/2017 Monday 21/08/2017: No RNS of interest to the portfolio or Whittler universe. Tuesday 22/98/2017: RNS Persimmon:PSN: Half Year Results As has been the case with the majority of housebuilders over the last few years, a very decent strong set of results backed up by a lengthy and confident outlook statement:  Persimmon is a share that I have held on three occasions over the last 15 years. I consider PSN to be a quality business but due to its product, housing, being closely linked to the mood of the economy, house builders prosperity is cyclical in nature. On the other hand, when the mood of the economy is positive, it offers excellent returns on capital, great free cash flow and makes handsome returns to investors in the form of dividends and return of capital/special dividends. I have to say that about 20 months ago I had really become obesely overweight housebuilders in the ISA portfolio. The attractions were simply just too good to ignore and they had done marvellously well for me but in January 2016 I rather trimmed the sector thinking that would be enough of a ride for the time-being. However, Brexit presented such wonderful opportunities and I took the plunge once again including a fairly medium folio % in Persimmon at slightly over £14: what could possibly go wrong? Well thankfully nothing did go wrong and the shares prospered well including some very generous returns of cash & dividends all of which have been reinvested in further purchases of PSN. That medium sized holding has now developed into a reasonably significant holding.

My View: PSN is a quality business, yes it’s cyclical in nature but provided you keep a close eye on momentum & the housing market in general, I don’t consider it overly as a risk. I will continue to hold. Wednesday 23/08/2017: No RNS of interest to the portfolio or Whittler universe. Thursday 24/08/2017: Revolution Bars Group:RBG: What an interesting morning with a couple of RNSs one from Stonegate confirming, as I suspected, that they will be going ahead with an agreed takeover of RBG but at a modestly increased price of 203p; the indicative price in the earlier RNS a couple of weeks back was 200p. Then our friends Deltic determinedly release their RNS acknowledging the 203p from Stonegate but at the same time declare their intention to evaluate a cash offer for RBG and very interestingly go on to say that RBG has given them access to the accounts: Wow, do I detect a bidding war? Who knows? We will just have to wait and see. My View: My investment strategy is roughly based on about 75% of stocks qualifying via return on capital ROCE/CROCI & free cash flow matrices but the remaining roughly 25% is on what I classify as special situations: probably similar to a whole number of other private investors. In terms of special situations, they could be what I consider to be value plays or possibly a company where something “game changing” is happening. Over the years I have done quite well with these special situations and a couple of recent examples are Lavendon and Waterman. Now just to be clear, with these special situations I only go for what I consider to be good quality yet undervalued businesses and most definitely not value traps or dividend seduction whores where the dividend is paid out of anything but free cash flow. To that recent list, I can now add RBG as I consider the 203p from Stonegate as money in the bank and I can’t see the price falling below that level now. So my intention is to simply hold on and await developments from Deltic to see if a better offer is made for RBG and then if Stonegate really want their bid on the cheap to continue, see what they can come up with; I am in no rush. Friday 25/08/2017: Air Partner: AIR: A very solid trading update:- PRE-CLOSE TRADING STATEMENT Air Partner has made a strong start to the year with underlying pre-tax profit for the first half of the financial year expected to be not less than GBP4.0m, which compares to GBP3.0m reported in the same period last year. The Group retains a strong net cash position. Our Broking division, comprising Aircraft Charter and Remarketing, has performed well across all product lines during the first half, while the Consulting & Training division is delivering solid results with an encouraging pipeline of opportunities to be secured in the second half of the financial year. In line with our growth strategy, the Board continues to assess investment opportunities, both organic and acquisition, to enhance or extend the services and capabilities we offer our customers around the world, and to strengthen and advance our market position. We are on a journey of transformation, with the clear objective to become a more balanced business, with two market leading divisions - Broking and Consulting & Training - providing exceptional service and value to our customers globally and delivering high quality and increasingly visible earnings to our shareholders. Outlook The Board is pleased with the strong start to the year and remains comfortable with its expectations for the full year. As we always state, in the world of aviation, and most especially in the global charter industry, it is prudent to be ever cautious and vigilant. The global charter business has always been, and will continue to be, a volatile industry, and against this backdrop we will manage the business for the long term, with a very clear strategy of alignment to the needs of our global customer base. My View: I am very happy to hold my present position in AIR which is now up by around 70% since my original purchase. In addition I have made a series of top up purchases during 2017 including some positive rebalancing with AIR in the Tinker folio. I am a very happy holder whilst at the same time appreciating the potential volatility within this market as outlined honestly in the trading statement. Sad one of the week has to be Dixons Carphone PLC in which I have not held a position for over 18 months. I have such fond memories of Dixons/Dixons Carphone having bought them for what was a ridiculously low price back in 2013 as they were starting to once again get their act together; finally selling them in January 2016 following some RNS releases that indicated that the superb growth in profits was tailing off. It’s quite comforting in a way reading the 24/08/2017 RNS and finding out that I am not alone in being slow to trade my smartphone up to the next super smart model that can do all sorts of things that are unlikely to really interest me. As it stands my iPhone 6s needs a recharge every day; it does not seem so long ago that my Nokia could last a week on a single charge but there again, that was what it said on the side, a phone. I really like a lot of the things a smartphone can do; excellent camera & the super 4G but this RNS maybe suggests that the customer’s appetite is almost satisfied. Fourth Week of New section: Glad I’m Not There (a sort of reverse take on the old Judith Chalmers holiday programme briefly mentioning a dog of the week that thankfully I don’t own). This weeks star prize has to go to a high market cap company, Provident Financial (PFG) a FTSE 100 business: note I have never held either a long or short position in PFG. Oh morally how worthy they are of copping a nasty one. Sorry to go off on a rant but I absolutely deplore such businesses that make their money by exploiting those in desperate need of a loan when such facilities are unavailable because of credit rating etc via banks. These unfortunate often poor customers of PFG need help and not financial exploitation in a similar but possibly less dramatic way to pay day loan companies. On Wednesday PFG issued an RNS and put it this way, “if Carlsberg did profits warnings….”. It was simply a dreadful profits warning and had all the dreadful elements of profits collapsing along with the new strategy for the business, the CEO departing and the dividend being scrapped. Honestly, it could not happen to a more deserving bunch of bums. For me, such a business involving what is politely called “sub-prime lender” is totally uninvestable on ethical grounds and there is absolutely no chance I would ever want to own the shares; I like to make money but not by supporting the exploitation of the poor. I probably come across as a raving socialist but to be truthful I am much more of a capitalist with a conscience. In terms of profit warnings, investors would have had an opportunity to seek the exit door on 20/06/2017 when a slightly veiled profits warning was issued and the share price fell by 18%. Investors would then have had a few more days to sell at around the £24/£25 mark before the usual post-PW gradual decline set in. On PW day, 23/08/2017, the share price fell astonishingly by over 60%. Will it recover? Well, quite honestly I don’t care as it would always sit way up on my bargepole list. Incidentally, I found it rather sad that Woodford wrote a note on the day of the profits warning almost excusing himself from the hurt that it would cause investors in his underperforming fund; a little humility would perhaps have been a touch more appropriate. Finally, something I learned many years ago; Procrastination is, in my opinion, the worst enemy for a private investor following a profits warning and remember no matter how good an investor you are, you WILL suffer the occasional profits warning; that’s a simple stocks investing truth. Do have a great weekend and as ever, happy investing.

0 Comments

Week No 6 of The Voyager RNS Log: Week commencing 13/08/2017

Monday 14th August 2017: Firstly one in which I don't hold a position at all; neither long or short. RNS from Telit: TCM: Mkt Cap: £168m but sadly for holders subject to violent gravitational pull. The RNS informs the market that the crook of a CEO has departed the company and that allegations made about the company's accounts are incorrect and that all is well. Well, that’s ok then but hang on, how come that in just 48 hours since the market closed Telit suddenly find out that their CEO is a fraudster? Also, the interim CEO is the CFO i.e. the chap who was responsible for signing off the accounts so he is hardly likely to say that he produced a set of smoke and mirror accounts to fool the market, is he? Now somewhat surprisingly the share price did not tank in fact, it went up a few points by the end of the day and thereby offering investors rather than gamblers the chance to jump ship. My View: When I have the slightest suspicion that I doubt the trustworthiness of management or something is potentially wrong with the management of a company, I honestly don’t waste time in heading for the exit. That’s what I did back in June 2016 when I stumbled on the likelihood that TCM had been creating alleged profits by diverting essentially opex costs to capex. Just turning back to last weeks profits warning, those who acted fast on the day of the profits warning would have been able to exit at around 190p-200p rather than the close price of 150p: a strategy I employ is to sell on a profits warning as early as I can and I usually have business done by about 08:10 unless I am swanning around somewhere far-away enjoying myself. As soon as there is any doubt in my belief in the management or a PW, then I sell immediately: I just can’t see the sense in not preserving one's capital. I feel it always pays to remember that bad directors don’t readily become good directors and poor company culture is so difficult and slow to change. In the case of TCM with the various announcements from the company and investigative work from a couple of highly respected researchers, I take the view that to hold the shares is really simply a gamble something akin to running through a gunpowder factory in the dark carrying a candle: you may reach the other side and be declared as brave yet other outcomes are certainly less favourable. I honestly don’t mean to offend investors who decide to remain faithful to TCM; simply a case of me writing about my approach to such situations. Incidentally, I do not hold either a long or short position in TCM: shorting seems a touch alien to my mindset. Tuesday 15/08/2017: Revolution Bars Group: RBG: two RNSs today involving RBF. Firstly at 07:00 one from Deltec Group informing the market that they had approached RBG about a possible takeover of RBG but the RBG board did not wish to pursue further. Secondly, one from RBG giving their view on the Deltec approach and their reasoning for not feeling the approach would be in the best interest of shareholders. Also at the same time, RBG confirmed that they are still working with Stonegate as they discuss a possible bid at 200p. My View: It seems to me that RBG is now firmly in play and will either be taken out by Stonegate or another predator and I would not be at all surprised if it were to be at a higher price than 200p. I will sit tight on my fortuitous purchase of RBG and await developments. Wednesday 16/08/2017: No RNS of interest to the portfolio or Whittler universe. Thursday 17/08/2017: No RNS of interest to the portfolio or Whittler universe. Friday: No RNS of interest to the portfolio or Whittler universe. Third Week of New section: Glad I’m Not There (a sort of reverse take on the old Judith Chalmers holiday programme briefly mentioning a dog of the week that thankfully I don’t own). This week’s major Glad I’m Not Here award goes for the second consecutive week to Telit Communications: TCM if only for the comment about the shamed CEO that they published on Monday: “It is a source of considerable anger to the Board that the historical indictment against Oozi Cats was never disclosed to them or previous members of the Board and that they have only been made aware of its existence through third parties”. I have to say that statement did amuse me a touch, just what did they expect a fraudster to do? Another worthy contender for the award is Ashley (Laura): ALY: a serial disappointer and another profits warning this week. The generous looking “unreal” dividend that has not been covered by FCF for years and in recent months there have been boardroom changes plus senior management resignations. This weeks RNS contains the award winning paragraph “The results will show an exceptional GBP2.8m impairment charge due to the revaluation of a freehold property owned by the Group. In addition, and as previously disclosed, trading conditions have continued to be demanding. The Board of the Company therefore expect net pre-tax profits for the year ended 30 June 2017 will now be materially below market expectations”. Just what are demanding trading conditions? Does it mean difficult, overpriced or simply customers not living in a time warp? Next week: The only scheduled RNS I have in the diary is for one of those beautiful Brexit bargains Persimmon: PSN with full year results on 22/08/2017 although I suspect we will get a trading update from the superb Bioventix in the next few days. Fingers crossed for nothing nasty from elsewhere but if it happens, it happens! As I always say part of the deal we sign up to as investors is that even with best due diligence sobriety reminds us that the next profits warning is probably just around the corner. Have a good weekend; catch you next week. Week No 5 of The Voyager RNS Log: Week commencing 06/08/2017

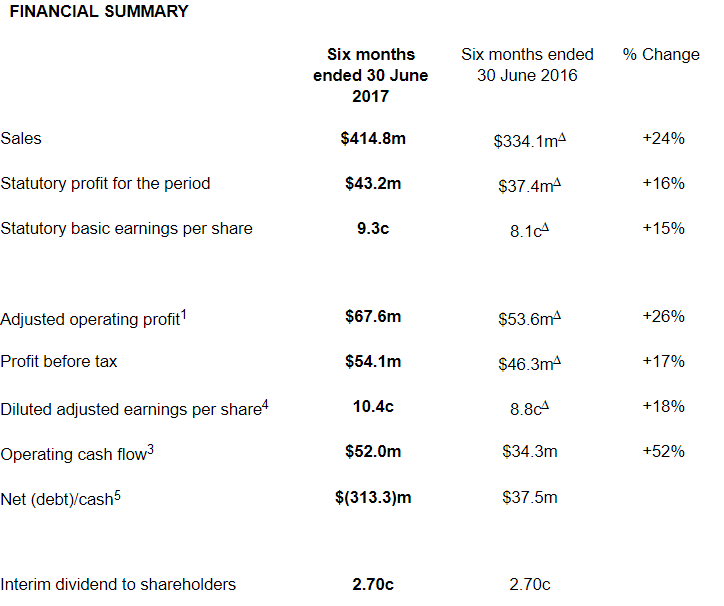

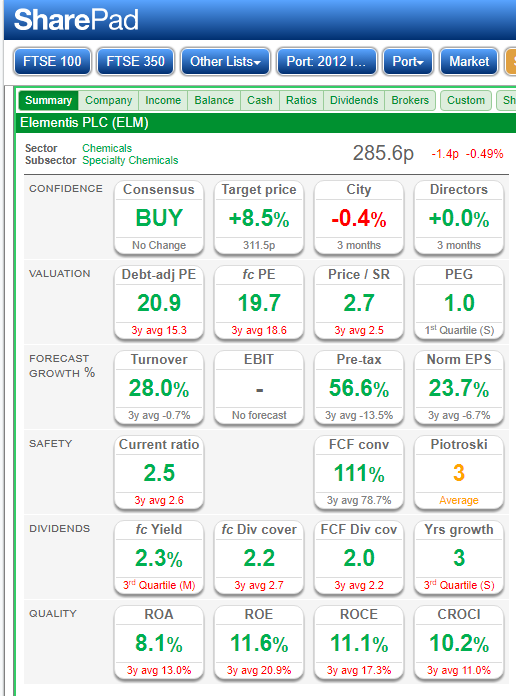

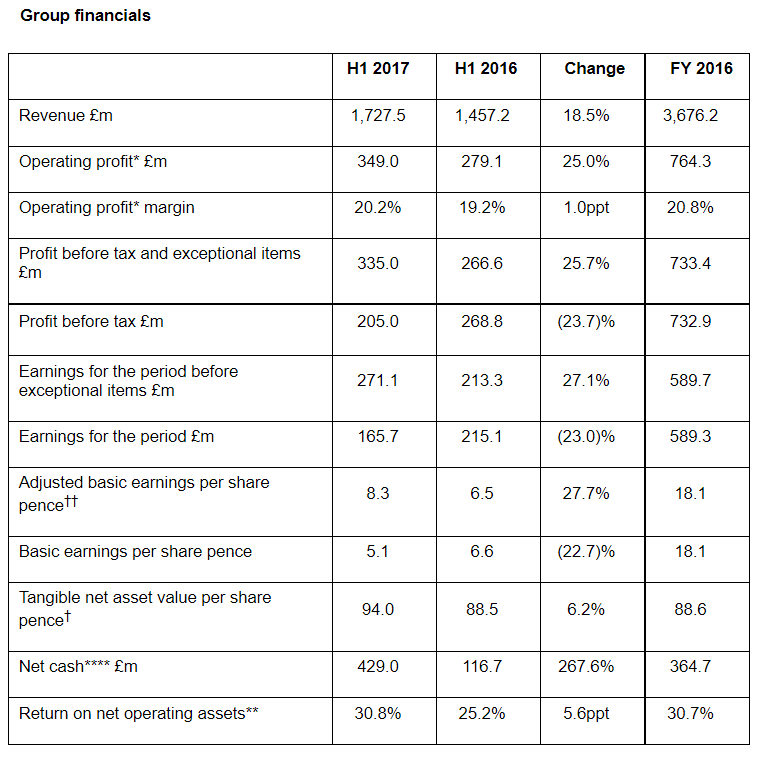

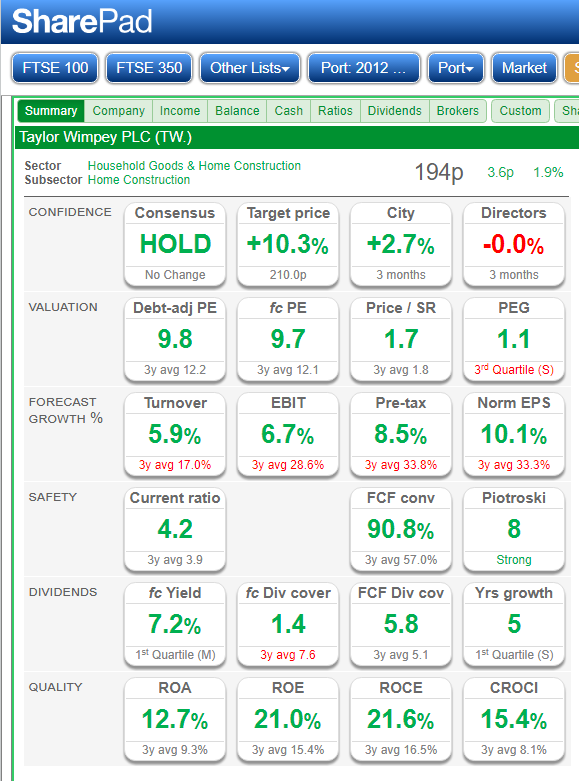

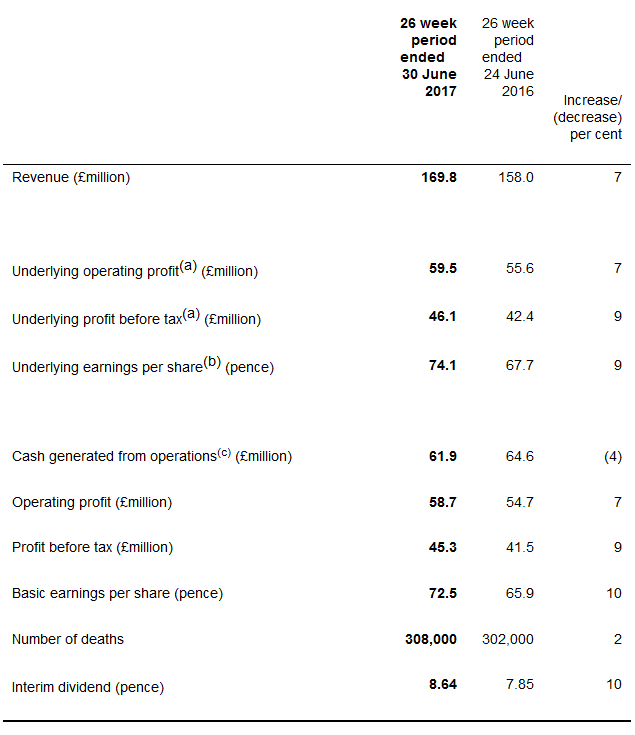

Note: straight lifts from each RNS are in italics and my scribbling in normal text. Monday 07/08/2016: No RNS for stocks held within the Portfolio Tuesday 08/08/2017: No RNS for stocks held within the Portfolio Wednesday 09/08/2017: Legal & General: LGEN: Half Year Results The results make decent if boring reading with the headlines of: financial highlights: OPERATING PROFIT up 27% to £988M (H1 2016: £777m) Profit after tax UP 43% to £952m (H1 2016: £667m) Earnings per share up 41% to 15.94P (H1 2016: 11.27p) Interim dividend3 of 4.30p per share (H1 2016: 4.00p) Net release From operations for Retained business4 up 6% to £724m (H1 2016: £681m) return on equity5 of 26.7% (H1 2016: 20.6%) SOLVENCY II SURPLUS6 INCREASED BY £1.0BN TO £6.7BN (FY 2016: £5.7BN) SOLVENCY II COVERAGE RATIO6 OF 186% (FY 2016: 171%) H1 2017 Results include base mortality release7 of £126m My View: well what can I say about one of my Brexit bargains that has given me a return of 55% since. Includes a nice safe yield of over 5% & intend to hold until I need the capital for something more attractive. Why did I not fill the wheelbarrow at the time! Wednesday 09/08/2017: AB Dynamics: ABDP: RNS informing the markets of directorate changes with CEO Tim Rogers announcing that it was his intention to step down at the end of 2017 plus some strengthening of the board with a couple of new appointments. The following link to an interview with Tim Rogers detailing the changes is worth a listen to: http://www.directorstalk.net/interview-ab-dynamics-ceo-stepping-largest-order-ever/ Thursday 10/08/2017: AB Dynamics once again: ABDP: another RNS from ABDP and one worth taking note of as the culture of the board is not to bombard the market with insignificant minor announcements: Significant Contract for Driving Robots AB Dynamics plc (AIM: ABDP) the designer, manufacturer and supplier of advanced testing systems and measurement products to the global automotive industry, is pleased to announce that it has received its largest ever order for driving robots. The order has been received from the China Automotive Technology and Research Center (CATARC), a leading Chinese research organisation based in Tianjin. AB Dynamics is a longstanding supplier to CATARC, which has previously bought a number of driving robots, a Guided Soft Target and a Suspension Parameter Measurement Machine from the UK-based automotive testing specialist. The new order allows CATARC to expand its track-based testing capabilities to include the latest China-NCAP test protocols and to perform a wide range of other international standard tests as required by its clients. CATARC is the leading organisation in China for the testing of Intelligent and Connected Vehicles and has already invested nearly 100 million yuan in its track-based testing and simulation capabilities. Tim Rogers, CEO of AB Dynamics, commented: "We were delighted to receive this strategically-important order from one of our key Chinese customers. CATARC is a benchmark in the Chinese car industry and we appreciate the confidence that it has placed in AB Dynamics and its products. With the new suite of driving robots and the Guided Soft Target which will be delivered later in 2017, CATARC has positioned itself as a major player in global vehicle safety testing business. "AB Dynamics has focused on offering a comprehensive suite of test equipment covering lab-based and test track which works together in synergy. Customers appreciate the fact that our products have been designed from the outset to work together seamlessly." My View: I don't think the board changes are anything to worry about and seem to be well planned and nothing knee jerk about them so seems fine with me. As for the significant contract for driving robotics it can only be good news for the company but no indication is given in monetary terms as to its positive impact on ABDP. Myself, I am happy to hold my initial post Brexit shock wave purchase and the couple of follow up top ups I have made having enjoyed a super return over the last 12 months. Friday 11/08/2017: no announcements relevant to the shares within the portfolio or universe of interest. Second Week of New section: Glad I’m Not There (a sort of reverse take on the old Judith Chalmers holiday programme briefly mentioning a dog of the week that thankfully I don’t own). This week’s major Glad I’m Not Here award is oh so worthy of the award: Telit Communications: TCM. Oh, what a calamitous week the Israeli IT company has had. Firstly on Monday, they published their half year results. In a nutshell the smoke & mirrors Profit Before Tax came in at a loss of $6.7m compared to a “profit” of $4.2m in H1 last year. The company tried to offer some reassuring words which did not thrill the market sufficiently to stop the share price falling by 41%. Two days later an RNS announced that the CEO was taking extended leave following fraud allegations relating to his past pre-TCM days and the share price took another dip on the day; this time by another 33%. The CEO had the great slice of luck to have sold a few million shares at close to the top of the market at around the 350p mark; yes, that was indeed a stroke of good fortune as some 10 weeks later the shares trade at around a third of that sale price. So after trousering a handsome return, the CEO takes an extended leave of absence from the company whilst an investigation takes place. Of course, I am not suggesting anything was improper; just simply commenting that the CEO had excellent timing in executing that sale. Now I should say that I have been incredibly mistrusting of TCM for a long time now and even blogged about them in the first half of 2016. My concern being that I really suspected they were capitalising routine “running the business” costs and therefore greatly inflating profits; indeed, I questioned if they had ever really made a real profit had the accounts been of a less aggressive nature. Who knows, this may even be a turning point for the company once they have reviewed their accounting policy but it’s not one where I wish to risk my hard earned dosh on. I did write about my concerns here, on BB’s and also Twitter but these days I am much guarded with my comments after the abuse I received on certain BB’s when I wrote a few years ago about the unsustainability of the Tesco model, poor and declining ROCE, insufficient FCF to cover dividend payments etc. It received a similar response concerning a similar fragility with the Morrison Supermarket chain. To be honest I changed my BB name and these days hardly post on such sites at all; who needs the abuse of fools when all you are doing is trying to very gently point out a potentially serious financial situation with a business; such is life! As for TCM, the excellent Paul Scott has tried to point out his concerns surround in the accounts over the last year or two and now the “sheriff of AIM” Tom Winnifrith has given his damning views of the business. I do hope that PIs managed to look after themselves; personally I only held the shares for 9 days back in the first half of 2016 when further checking of the numbers revealed that I had been a tad lazy on my due diligence and because of the capitalisation of costs issue I sold at once miraculously making a small %: simply a slice of luck in my case when I really deserved a kick in the arse for not taking sufficient care with my research on that one. I have been running a Smoke & Mirrors screen (SMS) for about 18 months now and it’s quite a dynamic screen that I refine on a regular basis. The screen flags up companies that I need to take real in depth look at should they somehow enter my investment universe. Even today, the SMS flags up shares that are extremely popular with PIs that I talk to. However, apart from throwing in the odd direct question, I learnt my lesson on the BBs as I don’t want to offend fold or create any bitterness. Maybe all PIs should have their own SMC or a system of flagging “take extra care”. Incidentally, Israeli companies are just about to join avoid list along current residents Africa, China & Russia. Ok, I know that many PIs may have done well in companies based in these continents or countries but to my way of thinking the risk of corruption is simply too high and these geographic locations are best avoided. Next Week looks like being a fairly quiet week for the portfolio with no announcements scheduled. Heck, that’s bound to tease out a profits warning; after all, I always say a profits warning is just around the corner; let’s wait and see. Well, that’s it for this weeks RNS log: it's off to the Barnet game tomorrow following the Hatters. The ground is set in a nice open spacious park but unfortunately does not have a decent pub within miles. Happy Investing & have a good weekend. Week No 4 of The Voyager RNS Log Note: straight lifts from each RNS are in italics and my scribbling in normal text. Monday 31/07/2017: XPP: Market Cap £529m: Interim Results. The interims read very well:  Adjusted for intangibles amortisation of £0.1 million (1H 2016: £0.1 million), £2.8 million (1H 2016: £0.1 million) of advisory and aborted acquisitions costs and £0.8 million (1H 2016: Nil) tax deduction related to the aborted acquisitions. The Outlook in the XPP statement also makes very positive noises providing reassurance and promise of more growth to come: “We have made a very strong start to 2017 and the momentum experienced in the second half of 2016 has accelerated in the first half of the current year. We had a strong book-to-bill ratio in the first half of 2017 of 1.16 and a customer order book of £70.9 million. We are confident that our new product releases and design wins over the last few years are supporting our revenue growth. While we remain conscious of potential macroeconomic challenges, the combination of these factors means that the Board now anticipates the Group’s performance for the full year will be comfortably ahead of its existing expectations”. “The Group has a strong balance sheet which places us in an excellent position to make selective acquisitions to further broaden our product offering and engineering capabilities. We believe we are now well along the path to achieving our vision of becoming the first choice power solutions provider to our existing and target customer base”. The figures do use the suspect word “adjusted” but the notes gives a degree of explanation up front and I would say no reasons for concern there. Again up-front, the script does explain openly the positive effect that the decrease in the value in the pound has had for the business “Approximately 81% of our revenues are denominated in US Dollars and the translation of these revenues into Sterling for reporting purposes has had a beneficial effect. However, the majority of our cost of sales and a large proportion of our operating expenses are also denominated in US Dollars for which the translation into Sterling has a negative impact, thereby significantly dampening any effect on the operating margin”. I did a write up about the purchase of XPP back in April 2016 and at the time I was fairly optimistic about the company's prospects & indeed it turned out to be a decent purchase plus also offers a very decent yield that is comfortably covered by FCF.   Incidentally, there is an interim results presentation involving Duncan Penny CEO of XPP and Jonathan Rhodes FID; well worth a watch on the XPP web site. My View: I liked the company when I purchased into it in April 2016 and still like the company. I also like the degree of clarity in the way the results are presented. Where do we go from here? Well, I suspect there will be some broker upgrades to follow which in the medium term should keep a touch of a tail wind with the shares; I may consider a top up shortly as I just adore expressions such as comfortably ahead of its existing expectations. 31/07/2017: Revolution Bars Group: RBG: Market Cap £88m but subject to significant daily change!: Statement Re: Possible Offer. A bit surreal this one and worth a note I suspect from myself. I originally bought into RBG in January this year but following an announcement that the second CFO in a few months had declared he was leaving the business I sold my entire holding; 2 x CFO’s leaving in a short space of time just did not sit well with me. A few months later, May 2017, RBG duly issued a profits warning and the shares were absolutely caned eventually bottoming at about 50% of the pre-profits warning price in early July: hardly surprising as management credibility had declined and with it the trust on many investors. On Tuesday last week, RBG issued a very reassuring trading statement and it appeared the new CFO had brought a bit of sanity and reassurance to the business. I pondered for a couple of days and then bought back in on Friday afternoon. The reason behind the purchase was simply the prospect of recovery of the share price. Now I should say that I would think that 80% or more of my stock purchases are based on seeking strong cash-flow accompanied by impressive ROCE/CROCI but I also do purchase what may be termed as value positions/recovery situations and simply by good fortune, these can become the subject of a bid: seen recently with my Lavendon & Waterman holdings. I think with LVD & WTM it was a case of being patient waiting for recovery and pleasingly they were eventually the subject of successful takeovers. In the case of RBG it was again waiting for recover as the new CFO got to grips with the finances and I expected this could yield results in maybe 12 months: the possible bid coming in on Monday 31/07/2017 was purely really good fortune on my part and I take little credit for that potential windfall, sometimes Lady Luck smiles on you but you can bet your boots that that same Lady Luck will balance things out at some time in the future and give me a kick up the rear. Incidentally, other shares that I hold that currently sit under the value/waiting for recovery umbrella are BON, BT, GFRD, ITV & NXR. Sell or hold at the moment on a potential offer; always a bit of a quandary for an investor that one: will the potential bidder Stonegate after looking at the books walk away? I honestly don’t think so Stonegate is a very smart animal totally specialised in this sector having made some smart buys over the years: most will have heard of Yates & Slug & Lettuce (oh God, that’s just brought back to me the memory of SFI that completely fell off the bar stool in 2002). So I think it’s closer to being a nearly done deal than most investors think yet maybe another 10% may be added to the offer or an alternative bid come in as personally, I think that Stonegate sees a bargain at 200p especially with their hand at the tiller. Whilst I admire investors who bought in the recent trough and have decided to sell; then well done on making an excellent return. However, I intend to hold on to my shares in RBG for yet a while. I should say what a dreadfully strange time it was for RBG to issue that potential offer RNS, 16:22: why not simply wait until the markets opened the next day? Still not to worry the good news added a touch of extra vigour to my tedious task of making mushroom risotto that evening; lovely food especially with a touch of white wine and calvados but all that stirring! The celebratory drink of the evening was peppermint tea; Monday to Friday are “dry days” for a few months. Finally, on the subject of RBG, I have to say that the excellent article by Paul Scott following the TU helped push the buy button. Incidentally, on roll-outs, there have been some first class articles by Paul on the more bullish side and Phil Oakley on the more “take care” side of roll outs: two first class commentators in my view. Tuesday 01/08/2017: Elementis: ELM: Market Cap: £1,370m: Interim Results: all fairly positive but maybe the excitement in ELM has slowed for a while after enjoying a 50% rise from July 16 to Mid February 17. The shares are taking a breather now having been fairly locked within a trading range for the past 5 or 6 months. Overall doing OK and will remain as part of the 3YL portfolio.   The outlook statement reads: Outlook-on track to grow operating profit across all three segments in 2017. My View: a decent solid business with an unexceptional yield that is very well covered by FCF: for now I won’t be adding any more. Tuesday 01/08/2017: Taylor Wimpey: TW.: Market Cap £6,347m. The interim results are to my eye good with headlines presented as:  Note: the decline in PBT of £130m due to an exceptional item involving leasehold review: a paragraph reads: Within the AGM trading update in April we published the conclusions of our leasehold review, and announced that we would make a provision, before tax, of £130 million in the first half accounts, which we continue to believe is an appropriate estimate. We expect the cash outflow to be spread over a number of years. The process of negotiation with the owners of the freeholds to these leasehold properties is on-going, and is proceeding in line with our expectations, and we continue to keep customers updated on the progress of these discussions.  My View: overall a decent set of results and the previously announced leasehold revision of £130m has now been included as an exceptions cost in the interims. There is also pleasingly a special dividend announced again for next year with more cash being returned to shareholders. I was very overweight in housebuilders and took some very pleasant profits to reduce overweight sector exposure. However, in the aftermath of Brexit, the seduction of the sector was just too great for me to resist and I became a little obese but not grossly obese as I had previously been before selling some house builders in January 2016. Incidentally, I am always relaxed about having a bias to a few sectors that I consider to be going through favourable times and don’t really see a weighting across the major sectors as an imperative. Wednesday 02/08/2017: Dignity: DTY: Market Cap: £1278m: Quite a decent set of results in my view although comments such as an x% increase in the number of deaths do give one a spooky feeling. I suppose the DTY RNSs would go into overdrive with a touch of plague hitting our shores! Anyway, back to the results:  Non-GAAP measures The Board believes that whilst statutory reporting measures provide a useful indication of the financial performance of the Group, additional insight is gained by excluding certain non-recurring or non-trading transactions. These measures are defined as follows: (a) Underlying profit is calculated as profit excluding profit (or loss) on sale of fixed assets and external transaction costs. (b) Underlying earnings per share is calculated as profit on ordinary activities after taxation, before profit (or loss) on sale of fixed assets, external transaction costs and exceptional items (all net of tax), divided by the weighted average number of Ordinary Shares in issue in the period. See note 2. (c) Cash generated from operations excludes external transaction costs. Following a very strong start to the year, with the number of deaths seven per cent higher than last year in the first quarter, the half year concluded with the number of deaths two per cent higher than the same period in 2016. The Group's results for the first half of 2017 were in line with the Board's expectations with underlying operating profits increasing seven per cent to £59.5 million (2016: £55.6 million). Outlook: The Group continues to expect the number of deaths in 2017 to be slightly lower than in 2016. Our financial expectations for the full year remain positive and unchanged. I suppose a balanced portfolio could be along the lines of Tristel to as the first line of defence to kill the bugs followed by GSK to treat you if the bugs get through and finally Dignity to “look after you” should the grim reaper get his evil way! My View: overall a decent set of numbers but I somehow feel the best years of profits growth are behind DTY and they eventually will have to address the rather stingy dividend in order to make the shares a touch more attractive. Having said that, the business will always have customers; it’s not the sort of service to simply die away. Wednesday 02/08/2017: AdEPT Telecom: ADT: Market Cap: £80m: £7.3m BGF funding and Atomwide acquisition. Interesting acquisition in my view; the RNS part relating to the acquisition of Atomwide goes on to say “The Board of AdEPT also announces that it has signed an agreement with effect from 1 August 2017 to acquire the entire issued share capital of Atomwide a well-established UK based specialist provider of IT services to the education sector ("the Acquisition")”. The note goes on to say that the acquisition is expected to be earnings enhancing from completion (one would hope so!), Atomwide hold the IPR for their education applications and that’s nearly 80% of Atomwide revenues and gross margin are from recurring products and services. My View: will, of course, have to keep an eye on debt with ADT as well as the rather volatile nature of the share price but overall it looks like decent progress for ADT. The share has performed reasonably well for me in the last 12 months haven appreciated by just over 30% but I don’t think I will add further just yet. Thursday 03/08/2017: No RNS of interest to my portfolio or immediate watch list Friday 04/08/2017: Keywords Studios: KWS: Acquisition(s) of La Marque Rose SARL, Asrec SAS and the subsidiary companies of holding company, Dune Media SAS. I have to say I was getting a touch worried about KWS as they had not announced an acquisition for a few weeks but that was put right today. My View: to be fair to KWS, the bolt on businesses do look interesting and if KWS can manage and softly integrate whilst keeping the flair of the added companies, then the future could indeed look very promising. I have to say there is never a dull moment on the journey with KWS: I will continue to hold. New section: Glad I’m Not There ( a sort of reverse take on the old Judith Chalmers holiday programme briefly mentioning a dog of the week that thankfully I don’t own), surely a candidate for dog of the week has to be Real Food Group with it’s screwed up RNS announcements and it’s smoke & mirrors accounting. The increase in Capex/D&A ratio would have rang alarm bells with me and at the very least necessitated some in depth digging to get a feel for it’s validity. I do run a smoke and mirrors (S&M) screen to try to pick up rapidly such points; they may well be perfectly valid but at least the S&M screen directs me to have a look. Another candidate for the dog of the week may have been Utilitywise, UTW, but I somehow think that the announcement this week covering changes in accounting practices may draw something of a close to some of the obvious suspicions surrounding UTW. Strangely the company did sneak into the outer reaches of my universe but got rapidly defragmented due to its dodgy accounting practices and the revolving door of changes in the boardroom: it always makes me worry when a CFO leaves in order to pursue other career opportunities. Still not one for me I am afraid. Next Week: all I can see scheduled at the moment are interims from LGEN, oh what a beautiful Brexit bargain that was. So, hopefully, an easy week on the keys and not necessitating an overindulgence with the peppermint tea. In between that, we have the start of the football season; the real stuff & not that Premier League nonsense. So, it’s off to my beloved Kenilworth Road on Saturday ”the theatre of dreams” but sadly not recently ones with many happy endings. Have a good weekend. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed