|

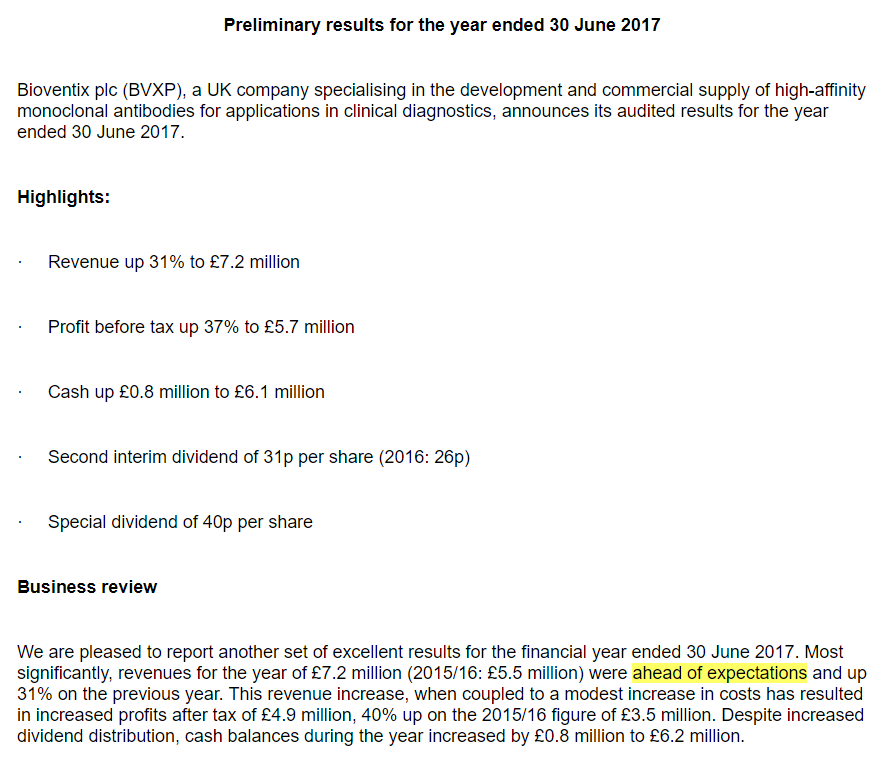

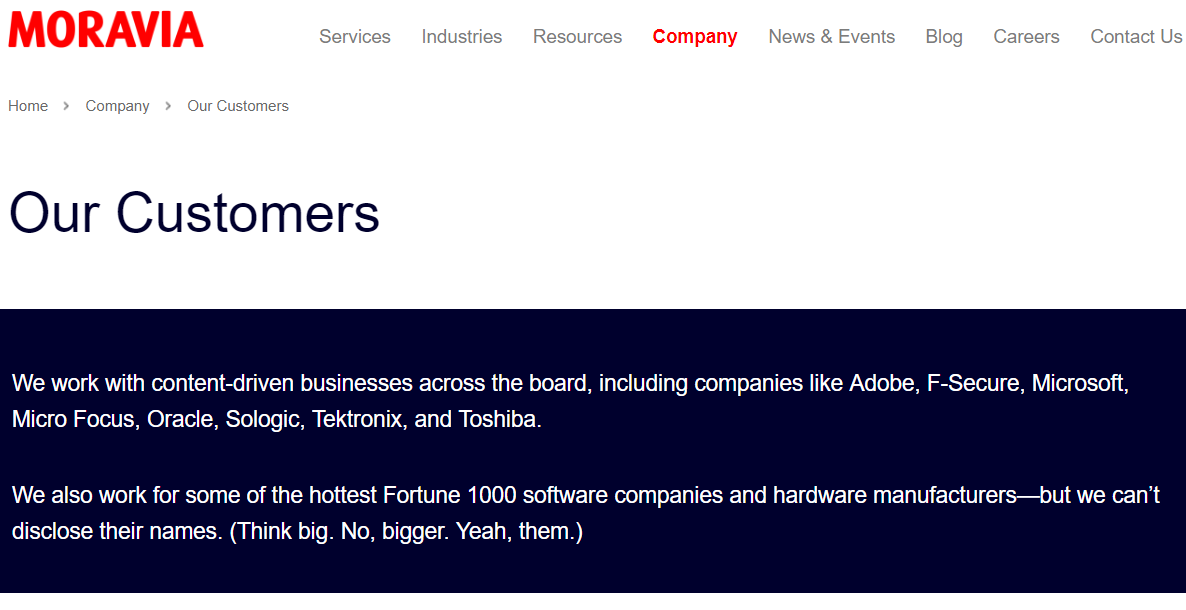

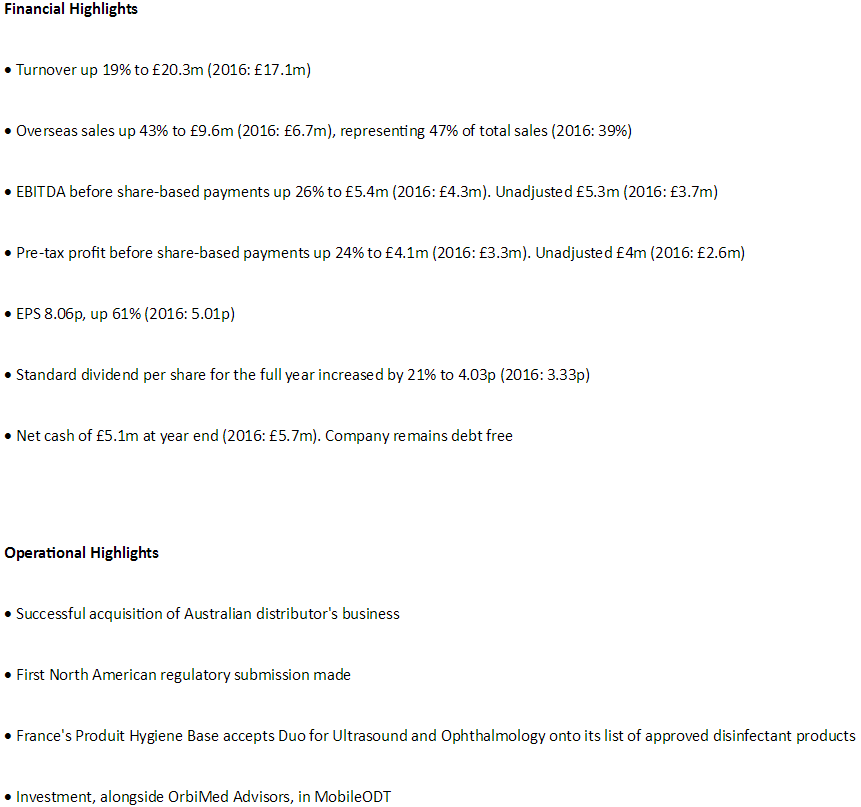

Well what a touch of good fortune this week as I received a letter from The International Postcode Online Lottery informing me that I had won £725,000. Now that is doubly fortunate as having never bought a ticket in the first place to actually win is simply amazing. I must call the telephone number on the letter and arrange to pay the few £000’s in order for my win to be released. Honestly, I sincerely hope that nobody falls for such a scam. Anyway, back to my whittling; a little bit of activity for the portfolio this week as I added a new holding, RWS Holdings; see notes below for Wednesday 18/10/2017. I also did a hefty top slice of Bioventix as well as some Zytronic. Both of these companies, BVXP & ZYT, are included in this log. Some of the proceeds of these sales were used to add further to my ITV holding which I have been continuing to add to since mid-September. I should say that I am now getting a touch concerned about the general Midas feel that investors have; should I feel that concern? Well, I have written before about the need to exercise some caution and remember that in a bull market valuations and indeed cult stocks can become terribly stretched like a stressed piece of elastic as the price of these Klondike microclimate stocks detaches from reality. Examples can be seen all over the place including a couple I write about in this note; e.g. although Tristel is a great business does it comfortably warrant such a high rating based on “things to come”? I am also evaluating the return of BOO to the portfolio, a stock I previously took profits in albeit a touch early, but yet again, the great business that it obviously is, does it really warrant such a sky-high valuation. Sorry, I simply don't have the answers but that does not preclude me from viewing the Klondike with caution. Monday 16/10/2017: Bioventix: BVXP: Final results for the year ending 30/06/2017:  Pleasingly a 40p special dividend has also been declared which added to the collective routine dividends of 51p for this year gives 91p which amazingly is equivalent to 13% of my purchase price of BVXP. As ever, the CEO, Peter Harrison, is very balanced with his comments: The revenues resulting from the success of the Siemens troponin project will be important in replacing approximately £1 million of NT proBNP sales that will be lost from the 2017/18 accounts due to the termination of a specific technology license. Conclusion We are delighted to be able to report such positive news for the current year. For the financial year 2017/18, our challenge will be to make up for the approximately £1 million of lost sales mentioned above with revenues from the newly launched Siemens troponin project and modest growth from additional vitamin D antibody sales and royalties. Beyond that, growth in the period 2018/2020 will be linked to our troponin project and the success of Siemens in their product launches around the world. We continue our research activities as we look to seed additional projects that will germinate in the period 2020/2030 creating additional shareholder value. My View: BVXP have performed exceptionally well in the three years that I have held them and Peter Harrison always modestly and conservatively looks at the future usually under promising yet overperforming. They have had an exceptional last three months with a 50% rise in the share price and as may be expected, this has drifted back a touch since the finals. Just to balance the risk of the touch of uncertainty over take up of new diagnostics, I have top sliced the shares up to 175% of my original investment. That leaves me still with a decent sized chunk "riding for free" and as an investor, I am very happy to continue to hold this reduced amount for the long term. Some of the proceeds have been used to purchase further ITV shares to add to my current holding. Monday/Tuesday/Wednesday: The daily news from RBG regarding their proposed takeover by Stonegate plus the “leaving with immediate effect” RNS about the CEO. Now before I go any further, I should declare that I no longer have financial interest in RBG having evaluated the “Stonegate Ultimatum”, I sold last Friday at 200p and booked a very tidy profit. Stonegate, I believe really backed themselves into a corner with their “Final Offer” and in effect scuppered any chance of solely increasing their offer above 203p as they have to abide by the Takeover Panel rules. The proxy votes and investors votes were not sufficient to get above the 75% YES threshold and so the deal was off. Now after selling I kept an eye on the RNS flow and saw that sadly some investors either don’t understand takeover panel rules or simply can’t add up even after the proxy results were reported on the Monday before the Tuesday shareholders vote, it was blindingly obvious that the 75% threshold just mathematically could not be reached in favour of Stonegate. Finally, as a non-invested bystander, I did smirk a touch when the news was announced on Wednesday 18/10/2017 that the CEO was leaving with immediate effect and the post to be temporarily covered by the chairman. They seem to have this type of misfortune at Revolving Door Group, sorry RBG as they lose CFO’s and a CEO. Anyway, due to the tight profit margins and type of business it is (I detest Vodka), I simply thank RBG for the short ride and wish them and all current shareholders all the best and to be honest, I reckon they will eventually do ok. Wednesday 18/10/2017: RWS Holding: RWS: Market Cap £1263m. Three RNSs this morning. Firstly the proposed acquisition of Moravia: RWS Holdings plc, a world leading provider of intellectual property support services (patent translations, international patent filing solutions and searches), commercial translations and linguistic validation, today announces that it has entered into an agreement (the "Acquisition Agreement") to acquire the entire issued share capital of Moravia US Holding Company, Inc. and Moravia Lux Holding Company S.à r.l. (together "Moravia"), a leading provider of technology-enabled localisation services, from Moravia Holdings II, LLC (the "Acquisition") for a cash consideration of US$320m (the "Consideration") plus working capital and certain other adjustments and transaction costs. The Consideration, adjustments and transaction costs are intended to be funded by a c.£185m (before expenses) cash placing of new ordinary shares in the capital of the Company (the "Placing"), details of which have been announced by the Company separately today, and a new US$160m term loan which will refinance the Group's existing facility (the "New Facility"). The Board believes that the Acquisition has a compelling strategic and financial rationale as it: Brings to the Group a highly successful business with a strong track record of profitable and cash generative growth: Long term relationships with some of the largest publicly traded technology companies in the world Has increased revenues by a CAGR of 26.0% from US$100.3m in 2014 to US$159.2m in 2016 and adjusted EBITDA by a CAGR of 52.6% from US$11.6m in 2014 to US$27.1m in 2016 Creates a third RWS division of scale with significant growth prospects: Growth opportunities include increasing share of wallet with its long-standing clients, winning new clients, introducing complementary solutions and growing new verticals and geographies Will operate as an autonomous division, replicating the successful creation of a Life Sciences division through the Group's acquisitions of CTi and LUZ, giving the Group three divisions of scale in attractive global markets, all with strong track records of profitable, cash generative growth Further diversifies RWS, as it is expected to represent approximately one third of the enlarged group's profits, and strengthens its global operational base Provides significant additional market opportunities for both companies due to their complementary business activities, geographies and client base, including the potential cross-selling of patent translation services to Moravia's intellectual property-rich clients Brings a strong, well established management team to the Group Is at an attractive valuation for one of the few major localisation providers focussed on the high growth technology sector in a highly fragmented market Is expected to be highly and immediately earnings enhancing for RWS shareholders Secondly, we have an RNS telling the market about a placing of 45,000,000 shares with institutions in order to fund the acquisition. Finally, later in the morning an RNS informing the markets of the success of the placing at 425p: sadly PIs have been overlooked from consideration, it seems the larger a company gets the less it treasures its PIs. My View: quite an interesting one for me this as I dithered on a purchase following their excellent trading update of 03/10/2017 “adjusted profit before tax (before amortisation of intangibles, share option costs and exceptional acquisition costs) is also expected to have performed strongly and ahead of market expectations”. Luckily the acquisition and placing announcements of 18/10/2017 gave me a second opportunity to climb on board at a reasonable price. My “fag packet” calculations very much agree with the RWS statement that this deal should be very & immediately earnings enhancing for shareholders but that’s not all, a quick scan around the Moravia web site reveals a tantalising list of customers:  Is RWS expensive? Well, readers will know that I am just not at all impressed by the ubiquitous “Arfer Daley” PE, I much prefer to base my comfort on ROCE, CROCI and free cash flow and RWS scores highly in these areas. So, on board now and look forward to the ride which I hope will be a long one. Thursday 19/10/2017: On The Beach: OTB: Market Cap: £587m: 2017 Full Year Trading Update “Strong H2 revenue growth across all markets” The Group has traded well in the year with adjusted PBT performance expected to be in line with Board expectations. UK revenue growth for the year was 17% on the back of a strong H2 performance with growth of 26%. Excluding the acquisition of Sunshine.co.uk Limited, UK revenue growth was 14%, with H2 revenue up 21%, with continued progression in UK EBITDA margin compared to 2016. The Group experienced significant growth for the majority of the key summer trading period, despite some softness in the weeks that followed the Barcelona terrorist attack in August and we have exited the financial year with strong forward momentum. My View: looks fine to me and although reference is made to the Monarch failure, I can’t visualise that this will be more than a small blip on the one year figures. Overall I am happy to continue to hold. Thursday 19/10/2017: Tristel: TSTL: Market Cap: £126m: Final results for year ending 30/06/2017 and I have screenshot the headline numbers below:  Well, the year ended 30/06/2017 look very good with the company heading in the right direction so no complaints there. However, I really would encourage Tristel to clearly include an outlook statement rather than leave the investor to glean what may be going on from the residual text published: sorry TSTL not good enough. Maybe the lack of an outlook is down to the delay/uncertainty with the North American venture? Well ok, be open and simply include a note in the phantom outlook statement.

My View: well I have had my reporting rant so what do I really feel about this business that I first took a fairly sizable stake some years ago when the price was 69p and that holding was then sold for 124p when a RNS gave me concerns about greedy share based payments and slowing down sales in the UK. Indeed at the time, the market was not overly impressed and the shares drifted over the next five months from a high of 145p to 90p. In the rising 90’s I re-entered the stock and then top sliced at 200p; wise or not, it was simply becoming too dominant a position within the portfolio and for risk management, I cut it back a touch. Overall, historically the company has been one of my favourites but what about the future? Firstly the stock does have great expectations built into the price which itself has appreciated by 90% since the turn of the start of the year and some 40% since July. Balancing that we have to consider that if regulatory approval is gained for North America then despite what appears to be a high rating, the stock should nicely continue to increase in value. On the other hand, I note some investors consider the stock to be expensive and should there be further USA delay or even a refusal, then the share price could easily be under severe pressure. On balance, I will continue to hold my remaining shares although I have to say that I appreciate the comfort of having banked very good profits on this one. Finally, if I did not already hold some TSTL, would I see TSTL as a compelling buy? I have to be brutally honest with myself and say no. Thursday 19/10/2017: Zytronic: ZYT: Market Cap: £96m: Trading Statement: The Board of Zytronic is pleased to provide the following pre-close statement ahead of announcement of the Group's results for the year ended 30 September 2017, which is expected to take place in December 2017. Revenues have continued to show good progress over the prior period, and results are expected to be in line with market expectations. My View: simply looks fine to me and despite my top slice this week, I am very happy to continue to hold a decent slice of ZYT which has handsomely delivered for me since my initial purchase in early 2015. I did have a scan round the quotes from other PIs and saw some remarks such as “an uninspiring trading update” but there you go, ZYT can't be expected to be “ahead of expectations” all of the time. I have seen an argument run to say that the valuation on a PE of 20 is historically on the expensive side but you know what, I think that the placing of an over reliance on the PE alone is simply misleading. For starters, if you strip out the cash that ZYT holds this PE comes down quite nicely. Now to my preferred measures: ROCE, CROCI, free cash flow & FCF conversion and I see a real quality business and it’s up to the individual investor to decide if the current share price offers reasonable value. The risk; well with reliance on a limited numbers of customers there is a risk of hitting a bump in the road. Personally, I decided that for a relatively small company ZYT had due to its success, really pulled it's weight & some more since the start of 2017 and that a top slice would be a prudent measure (Note: I am beginning to sound like Gordon Brown in saying prudent, HELP!) The remaining chunk, I am happy with and will continue to hold. Thursday 19/10/2017: Keyword Studios: KWS: Market Cap: £780m: Well, I was beginning to worry having not read of an acquisition by KWS for a few weeks but those needless worries have been set aside by the announcement of the acquisition of d3t ( you know this all gets a bit confusing as I already hold D4t4 but what’s in a name?); anyway the RNS for KWS: Keywords Studios, the international technical services provider to the global video games industry, today announces that it has acquired d3t ltd ("d3t"), for a total consideration of £3 million from the founders Jamie Campbell and Stephen Powell and others (the "Sellers"). Based in the North West of England, between Liverpool and Manchester, d3t delivers premium quality outsourced software development services for video game developers and publishers internationally. The acquisition of d3t is in line with Keywords Studios' strategy to grow organically and by acquisition as it selectively consolidates the highly fragmented market for video game services. d3t brings additional skills, client relationships and geographic reach to Keywords, extending the strength and scale of its recently established Engineering service line. Founded in 2011 and now employing 44 staff, d3t is an award-winning software development company with capabilities including HD re-mastering, porting, optimisation, rendering and game systems development. Over the course of the last six years they have delivered consistent high quality across dozens of projects for clients such as SEGA, Codemasters, Sony XDev and the BBC. Jamie Campbell and Stephen Powell, along with the rest of d3t team, will remain with the business. In the year ended 31st of July 2017, d3t achieved revenues of £2.8 million and an underlying adjusted pre-tax profit of £0.4 million. Under the terms of the acquisition Keywords is paying a consideration comprised of £2.4m in cash and the issue of 42,368 new ordinary shares in Keywords, which will be subject to a two-year lock in period. Giacomo Duranti, Chief Operating Officer, commented: "The acquisition of d3t complements our recent acquisition GameSim's capabilities to extend the services, scale and geographical presence of our Engineering offering. With increasing demand in the video games industry for reliable, high-quality outsourced software engineering services, we are building a strong offering to support our clients globally. My View: As I wrote a couple of weeks back, I still have a very significant holding in KWS that I am essentially running for free having taken out the value of my original investment in the business; it still remains one of my major holdings. The share dilution and cost of the acquisition are fairly insignificant so it’s really a question of bedding the new business in and continued delivery; something that KWS appears to be rather good at. I try to imagine how this gaming Mecano company that bolts on so many acquisitions manages the growing empire and that’s my only concern with the stock. Personally, I absolutely detest all gaming, it just does not relax me but that could possibly be because I am totally crap at it; give me the full TV series of Breaking Bad any-day! However, investment is not about one’s personal preference, it’s about attractive and hopefully sound companies and KWS continues to meet my selection criteria. To be honest, I think I may be holding this company for many years to come. Friday 20/10/2017: IQE: IQE: Market Cap: £940m: RNS regarding the under-payment of US Tax due to an unfortunate third party accountancy firms regrettable ignorance: Settlement of Prior Years Taxes: The Group recently engaged the services of an international tax firm to assist with a routine US tax filing for the year ended 2016. Unexpectedly, this exercise has identified taxes due in the US relating to the profits of an overseas subsidiary for the years ending 2013, 2014, 2015 and 2016, which follow the acquisition of the epitaxy business of Kopin in January 2013. This firm has estimated the tax due as approx. £4.2m, and is in the process of calculating the actual amount, which may take up to 4 weeks. IQE immediately initiated the payment of the estimated amount to the relevant tax authority, and will adjust any over/under payment in due course. On the advice of this firm, IQE has also accrued interest due of up to £0.4m. As a result of a Group re-organisation initiated in September 2016, but unrelated directly to this previously advised tax treatment, it is believed that no similar tax liability arises in 2017. The wildly optimistic line which I think is total fantasy is that IQE feels that they can claim full recompense from a local tax advisory service for the issue. In my opinion, that's daft. Whilst they may be able to gain some claw back on fees, the US taxes are clearly owed by IQE and not down to the activity of the third party accountancy firm. IQE is clearly extremely disappointed with the previous professional advice received and will be pursuing full recompense as a matter of priority with the previous advisors. I guess the reassuring part is a hint on current trading: The Group has enjoyed a strong Q3 with continuing growth driven largely by the ongoing strong VCSEL ramp in support of a highly significant mass market consumer application, and the new Foundry expansion remains on course to open in H1 2018. As a result, the Board remains confident the Group is on track to deliver full year expectations, including that of net debt. My View: lots of the figures may well be brushed away as exceptional items and at least the company has been responsible in highlighting the issue and also giving a flavour of current trading. Glad I am not there: well on a few occasions as I pen these notes I have and will continue to declare that I hold or held a “Glad I am not here” as they occur. Let’s face it, I am most definitely not clever enough to invest only in companies that never have issued bad news or profit warnings. This week the flavour is slightly different with RWS which did not treat it’s PIs that well with the placing and that hit current shareholders, particularly as they were not included in the offer. However, I bought straight into RWS on the day of the acquisition & placing announcements but at the same time feel for those PIs treated a tad shoddily by the lack of consideration by RWS. I suppose those PIs were important to RWS at one stage but just like stepping stones on a stream, they become less significant when the company has grown and crossed that once challenging stream: sad but a fact of investment life. This weekend my football travels continue to watch the table topping Hatters (yes that's right, table topping) at Crawley. I will make the fairly easy journey by train and have a couple of pints of decent ale in the Brewery Shades Inn before the game. Whatever you are doing, I hope you have a great weekend & as ever, happy investing.

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed