|

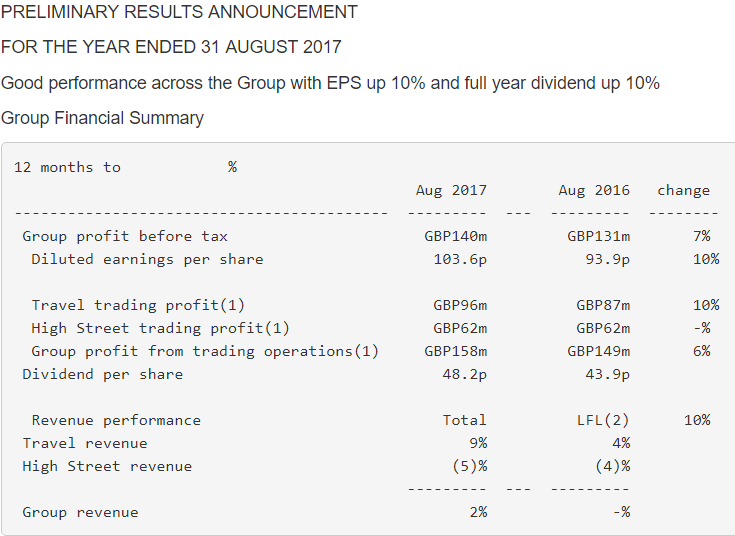

Voyager RNS Log WC 08/10/2017 Note: as ever nothing I write here is in any way a recommendation; well apart from the superb meze. Just view this as me meandering through my thought process concerning various regulatory announcements and sharing my views. It has been quite a busy week but in terms of the portfolio, the composition apart from reinvested dividends has remained constant without any transactions taking place. My thoughts on the various RNSs relevant to companies that I hold are: Monday 09/10/2017: XP Power: XPP: Market Cap £596m Trading Update: I did comment on XPPs acquisition of Condel last week and in a pleasant start to this week we have an excellent “ahead of its previous expectations” Trading Update. Trading Trading in the third quarter has been robust. Revenues for the nine months ended 30 September 2017 increased by 34% over the prior year to £123.9 million (2016: £92.6 million). In constant currency the increase in revenues was 21%. Order intake for the nine months ended 30 September 2017 was strong at £137.5 million (2016: £95.8 million) which was 44% higher than the prior year. In constant currency this was an increase of 30%. Our third quarter order intake was £44.1 million (2016: £34.2 million). The momentum in our order intake is encouraging, particularly the continued growth we are experiencing in our North American markets. Outlook We are encouraged by another quarter of strong order intake with our end markets remaining buoyant. The Group believes it is continuing to take market share as its portfolio of industry-leading power technology products is increasingly designed-in to new equipment by our target customers. These design wins will translate into orders as our customers’ projects move to production phase over the coming years. The Board now anticipates the Group’s performance for the full year will be ahead of its previous expectations outlined at the time of the Group’s interim results on 31 July 2017. My View: well, how can I be anything but happy with that RNS: I am happy to continue holding. Tuesday 10/10/2017: Revolution Bars: RBG: Market Cap £100m: a string of put up the money, no we will not, swipes between RBG and Deltec that culminated with Deltec declaring that they would not be making a cash offer for RBG; hardly a surprise in my opinion as Deltec was debt ridden and did not have the cash. So it’s back to the 203p which I won’t grumble about as it gives me a fortunate 70% profit on stock I repurchased as a special situation recovery stock; I was simply lucky: right place at the right time etc. Note: on Thursday, Stonegate in an RNS, indicated that their bid price for RBG would remain at 203p. Wednesday 11/10/2017: Telford Homes: TEF: Market Cap £308m: Trading Update: reads well enough to me: The Group's reported profits in any given period are driven by the number of open market completions achieved and there were far fewer of these in the first half of the year than the number expected in the second half. This is purely down to development timings which are all on track and in accordance with the original programmes but do not fall equally across the year. Completions of individual properties are proceeding exactly as planned with no unexpected delays. As a result of the imbalance of completions across the year pre-tax profit for H1 2018 will be significantly lower than H2 2018 and also lower than the corresponding period last year but will be entirely in line with expectations. The interim dividend is proposed to increase in accordance with the anticipated full year profit growth. The Group is on track to deliver full year profit before tax in excess of £40 million in accordance with market expectations and the Board's longer term positive outlook is unchanged. My View: I feel that Telford are an impressive company that without fuss simply gets on with the or business plan and monotonously delivers: just the sort of company I lIke to own. The table below reproduced from SharePad, compares five housebuilders that I either own or have owned over the last 18 months. As you can see from the table, Telford has many attractions and in my view is the housebuilder I would choose to own if I were limited to holding just one stock in this particular sector.  Thursday 12/10/2017: Norcros: NXR: Market Cap: £103m: Trading Update: Oh how nice to read an NXR release update where even the dull accountants take a positive note. The thrust of the TU is overall good progress and in-line. Group revenue and underlying operating profit(1) in the first half is expected to be in line with the Board's expectations. Group revenue for the first half is expected to be approximately GBP144.9m (2016: GBP128.8m), 12.5% higher than the prior year and 7.1% higher on a constant currency basis. The growth reflects a robust performance in our UK business and continued growth in our South African business. My View: I still think this is an astonishingly undervalued business whose share price has been held back by the perception the market has over its pension deficit. NXR have also done very well in reducing debt from £27.5m in 2016 to £21m in 2017. I did a write up on NXR at the time of the AGM at the end of July when I commented that in my view Mr Market is being far too pessimistic about that pension deficit which is well managed and has a very high average age per member. Thursday 12/10/2017: WH Smith: SMWH: Market Cap £228m: Preliminary Results:  Stephen Clarke, Group Chief Executive, commented:

"We have delivered a good performance across the Group. "The Travel business continues to perform well with strong revenue growth, up 9% in the year. For the first time, revenue in Travel has overtaken High Street and Travel is now the largest part of the Group in both revenue and profit. Profit in Travel is up 10% to GBP96m, now over 60% of Group trading profit. "During our 225(th) anniversary year, we were delighted to open our 225(th) international store and now have 233 stores open. We have won 273 stores across 25 countries, including new stores in Singapore and Rome. "The High Street business performed well - matching the particularly strong profit performance from last year. Our investment in new product design continues to drive stationery revenue and we have been pleased with the success of the recently launched Tom Fletcher Kids Book Club. "The Board has proposed a 10% increase in the final dividend and we have today announced a further share buyback of up to GBP50m reflecting the Group's cash generation and our confidence in the future prospects of the Group. "This performance is only possible through the hard work and commitment of our 14,000 colleagues across the business and I am grateful for their continued support. "Looking ahead, we will focus on profitable growth, cash generation and new opportunities to profitably invest in the future. While the economic environment remains uncertain, we are well positioned for the current year and beyond." (1) Group profit from trading operations and High Street and Travel trading profit are stated after directly attributable share-based payment and pension service charges and before unallocated costs, finance costs and taxation. See Note 3 to the financial statements and Glossary on page 31 for an explanation of the definition and purpose of the Group's alternative performance measures. (2) Like-for-like sales are calculated on stores with a similar selling space that have been open for more than a year (constant currency basis) My View: well anybody who follows my writings will know that SMWH is truly one of my favourite investments; incredibly boring and they just deliver. It’s interesting to see that the continued growth of the travel offering which has been a huge success: when was the last time I did not have to queue at a Smiths at either a motorway service station or airport? Maybe market research at it's best! Despite the 35% rise in SP since the start of 2017, I am happy to continue to hold. Thursday 12/10/2017: Just Eat: JE. Market Cap: £477m RNS regarding Hungryhouse merger:- CMA provisionally clears Just Eat / Hungryhouse merger Just Eat plc (LSE: JE) welcomes today's announcement from the CMA that it has provisionally cleared the company's acquisition of Hungryhouse. We are pleased that the CMA has provisionally concluded that this transaction does not lessen competition. We look forward to continuing to deploy our technology and expertise to help more independent restaurants develop and grow their businesses, while offering an even better service to consumers. My View: The market seems to like the news and the shares kicked on over 6%. Admittedly not my usual style of purchase being on such a stretched valuation but I will console myself by calling it a “special situation”. Friday 13/10/2017: no RNSs of mote involving shares within my portfolios Glad I Am Not Here: well I of course always like to think that things will turn out well for shareholders and particularly so with the case of AIM stocks where generically the universe is a tougher place if one does not take care. This week we had the rather astonishing announcement from Mytrah Energy informing the market that the chairman had taken an “unauthorised loan” from the company to purchase a property; just how did that escape corporate governance from a business that is loss making and with terrible cash flow? Now I do honestly believe that on AIM there are some really excellent well managed companies that are very worthy of an investment, in fact over a third of my portfolio is invested in AIM companies but they are ones where I have trust in the management of the company. Just a case of being diligent and doing research plus the all important risk assessment. Having said that, remember that the next profits warning is maybe just around the corner; simply the nature of investment particularly in small companies. Another qualifier for the Glad I Am Not Here weekly award is Character Group: CCT. Now this is a share I have owned a couple of times over the years and and on Wednesday they were firstly a little naughty with a late RNS offering the markets a trading update at 08:00 a touch late in the day for my liking and really just unacceptable; I mean did the accountant break the news to the CEO over the morning bowl of corn flakes? Actually, that’s a reasonable scenario as they are a serial profits warner; sorry, I will get my coat! The RNS tells us that “At this early stage of the Group's new financial year the Board consider that, based on the latest sales and market data available to them, the Group's performance for the year ending 31 August 2018 is now expected to be significantly below current market estimates. Nevertheless, the Directors believe this to be a temporary downturn and that the Group anticipates returning to its previous growth pattern during the second half of the 2018 calendar year, and this ultimately is expected to be reflected in the financial performance for the year ending 31 August 2019”. Now for my part, I began to lose confidence in management, again, with some trading updates and also a video presentation the company did; the whole thing just started to appear to be a risk in my opinion and I sold in January 2017 for a smidgen on an overall gain. As I always say, once you doubt something about a company it’s simply time to go; I may not always be right but it’s a question of comfort and managing perceived risk. It’s just a question for the individual investor and what you feel comfortable with. For example, some discomfort sales over the last four years in addition to CCT have been SAL, SHOE, SPRP, PMP, TCM & TRAK. With it’s strong balance sheet, I suspect CCT will go on and do what it usually does i.e. a mix of good progress sprinkled with the occasional profits warning. Next Week: I expect to see trading updates from ZYT & AMO early next week and in fact the market has been racing ahead a touch with ZYT so obviously, some investors feel there is good news to come but for my part, I am much more cautious with small-cap companies. Sometimes the order book can be lumpy and disappoint so let’s wait and see. We also have the finals from BVXP which has enjoyed an incredible increase in share price of over 100% in 2017. Have a great weekend and as ever, happy investing

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed