The Investment Journey Of A Private Investor

All private investors that at some time consciously took an investment on the stock markets did so as the start of an investment journey. For many that journey would have ended fairly quickly having suffered a series of poor investment decisions and for others, a little success probably kindled a spark of enthusiasm to go a little further on that investment journey. This series, broken down into to time period chapters, describes my own journey starting rather unknowingly with an early awakening in 1989 to the present day; or more correctly updated every three or so years.

Contents:

Introduction

Chapter 1

Chapter 2

Chapter 3

Chapter 1

Chapter 2

Chapter 3

Introduction: Every Journey Begins With A Single Step: Lao Tzu

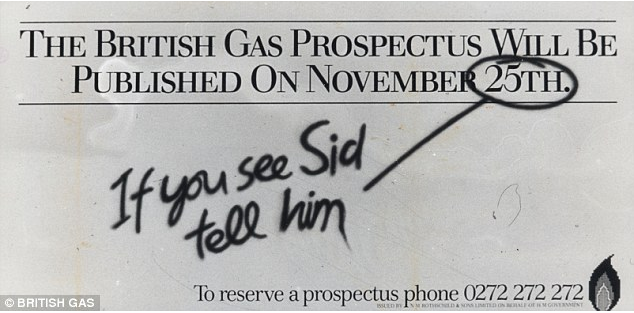

Chapter 1: Simple Beginnings: Have You Seen Sid?

For many ordinary members of the public, it was really the first time they had been actively encouraged to own shares in a company. The "tell Sid" advertising campaign prompted many thousands of people to buy shares in British Gas. The “have you told Sid” promotion to raise public awareness of the privatisation of gas in the UK was absolutely inescapable and for many people the first real time they had directly owned part of a business; being a shareowner.

Like so many, privatisation was my first exposure to the world of share ownership and indeed the great publicity campaign that the accompanied the ongoing process. I had joined Anglian Water at the time of the formation of the water companies in 1974; that in itself was a grand place for a relatively young chap to be. The company was incredibly supportive I worked through part-time study to complete my professional qualifications in science and become a Graduate of The Royal Society of Chemistry. What I did not realise at the time was that this lad who joined the very large analytical laboratory service of this new business at the very first run of the career ladder would be fortunate enough to eventually spend twenty years managing one of the largest analytical services in East Anglia: you just never know how things will turn out! It was Anglian Water that introduced me to the racy world of the stock market as the company went through the privatisation process.

Lots of publicity work took place within each of the companies heading down the road to the stock market and my own company was no exception with political figures involved in high profile publicity events. Just to name drop a touch, well why not, I gave tours of our scientific process to the very charming Lord Hesketh of motor racing fame and also Michael Howard a man destined to become a leader of the Conservative party; I have to say I took to one of these individuals much more easily than the other.

As was common with all businesses about to be privatised, employees were offered preferential terms to take part in the privatisation issue and quite honestly it was a no brainier. The company was duly floated, nice phrase for a water company, on the stock market and the flotation price of £2-40 closing its first day’s trading, in 1989, some 15% up: I had become a shareholder, I was excited and my investment journey had begun. In those early days, I had not the slightest idea that the stock market would play such a large role in my future. Following the listing of the various energy, water company’s etc people who worked within the newly floated businesses were regularly offered share-save schemes. These basically allowed staff to buy shares in the business at a previously discounted rate and via monthly contributions from their salary over periods of 3, 5 and 7 years. To me, it sounded just too good to be true and I filled my boots as they say over the years building us a considerable holding in the business: I had become a fully fledged investor.

There was no stopping me now from investing within my comfort zone and I took part in lots of other privatisations going on the time and became what is now known as a stag, buying shares in these newly privatised industries and with the exception of my own business, selling them relatively quickly and making some easy money. I decided I really liked this privatisation stuff, well at least in term of making me a wealthier chap. What I did not know at the time was that although it was fine making a very nice fast buck in staging, the real money and wealth would come to those with patience who took the very generous dividends and reinvested them the purchase of additional stock.

My investment journey had begun and I felt quite pleased with myself: my lovely shares were rapidly increasing in value and paying very handsome dividends. Yes, I really liked this investment lark; what could possibly go wrong?

Like so many, privatisation was my first exposure to the world of share ownership and indeed the great publicity campaign that the accompanied the ongoing process. I had joined Anglian Water at the time of the formation of the water companies in 1974; that in itself was a grand place for a relatively young chap to be. The company was incredibly supportive I worked through part-time study to complete my professional qualifications in science and become a Graduate of The Royal Society of Chemistry. What I did not realise at the time was that this lad who joined the very large analytical laboratory service of this new business at the very first run of the career ladder would be fortunate enough to eventually spend twenty years managing one of the largest analytical services in East Anglia: you just never know how things will turn out! It was Anglian Water that introduced me to the racy world of the stock market as the company went through the privatisation process.

Lots of publicity work took place within each of the companies heading down the road to the stock market and my own company was no exception with political figures involved in high profile publicity events. Just to name drop a touch, well why not, I gave tours of our scientific process to the very charming Lord Hesketh of motor racing fame and also Michael Howard a man destined to become a leader of the Conservative party; I have to say I took to one of these individuals much more easily than the other.

As was common with all businesses about to be privatised, employees were offered preferential terms to take part in the privatisation issue and quite honestly it was a no brainier. The company was duly floated, nice phrase for a water company, on the stock market and the flotation price of £2-40 closing its first day’s trading, in 1989, some 15% up: I had become a shareholder, I was excited and my investment journey had begun. In those early days, I had not the slightest idea that the stock market would play such a large role in my future. Following the listing of the various energy, water company’s etc people who worked within the newly floated businesses were regularly offered share-save schemes. These basically allowed staff to buy shares in the business at a previously discounted rate and via monthly contributions from their salary over periods of 3, 5 and 7 years. To me, it sounded just too good to be true and I filled my boots as they say over the years building us a considerable holding in the business: I had become a fully fledged investor.

There was no stopping me now from investing within my comfort zone and I took part in lots of other privatisations going on the time and became what is now known as a stag, buying shares in these newly privatised industries and with the exception of my own business, selling them relatively quickly and making some easy money. I decided I really liked this privatisation stuff, well at least in term of making me a wealthier chap. What I did not know at the time was that although it was fine making a very nice fast buck in staging, the real money and wealth would come to those with patience who took the very generous dividends and reinvested them the purchase of additional stock.

My investment journey had begun and I felt quite pleased with myself: my lovely shares were rapidly increasing in value and paying very handsome dividends. Yes, I really liked this investment lark; what could possibly go wrong?

Chapter 2: Hitting a Zero Then Meeting a Hero

Well, the first steps in my investment journey had really gone well with the easy stuff of buying shares in the utility company I worked for. I had also branched out just a tad, and bought into some investment trusts run by Edinburgh fund managers and that gave me a buzz in terms of doing something a little more myself rather than just taking the safe pickings from utility flotations. The next logical step of the journey was, of course, to really become a big boy and buy some shares in individual companies but how would I select them. Possibly via tips in newspapers or via tip sheets. In the end, it was a combination of tip sheet and the papers with the first purchase being a house-builder that was rapidly acquired by a larger player for a premium; nice, I thought!

I started to read a penny share tip sheet that suggested two really hot companies to get into were Azur; a ladies fashion company and also the British Taxpayers Association; both traded on the OFEX market. The write up for each seemed to be very convincing and the fact that you needed to subscribe to the penny share publication to obtain these privileged hot tips, gave me the confidence to buy both. I was naive of course and the collective investment soon proved to be a bit of a disaster; I learnt that such very junior markets were not for me: lots of promise of jam tomorrow but as my old granny used to tell me, “tomorrow may never come”.

I started to read a penny share tip sheet that suggested two really hot companies to get into were Azur; a ladies fashion company and also the British Taxpayers Association; both traded on the OFEX market. The write up for each seemed to be very convincing and the fact that you needed to subscribe to the penny share publication to obtain these privileged hot tips, gave me the confidence to buy both. I was naive of course and the collective investment soon proved to be a bit of a disaster; I learnt that such very junior markets were not for me: lots of promise of jam tomorrow but as my old granny used to tell me, “tomorrow may never come”.

Bound just to be a temporary setback I convinced myself and boldly strode onwards. With just basic research of the Helphire prospectus and the confidence of reading in the press the high regard of the management of the business, one the first day of trading in late 1997 I purchased some Helphire shares. Within a few weeks, I was handsomely in profit; this share price just kept going up and up; obviously one for me to hold onto; no intention of selling these boys quickly!

Following Jim’s well-reasoned guidance and understanding a little more of the financial criteria, I bought another two stocks: Blacks Leisure and DCS. Both of these stocks rapidly began to motor and I was a very happy investor. Wow, this was really good stuff and as I was feeling absolutely fabulous, I bought another growth stock; Harvey Nichols. Unfortunately, Harvey Nichols failed to move in my favour but the good point was that I was rapidly developing the realisation that even with reasoned share selection, it’s the performance of the collective basket of shares in your portfolio that determines joy or sorrow.

Some of my colleagues at Anglian Water, flushed with the success of AW share ownership, were also becoming impatient to dip their toe into the stock market pool and decided it would be a good idea to form an investment club. Our meetings were held in a pub in Cambridge: it was rather nice and very social. The format was for at least one potential purchase to be nominated, followed by a discussion of merits and voting. For our first purchase, I nominated Helphire, telling the group of my very wise decision to buy and boasting that I was already 20% up on the deal. My powers of persuasion came to little as the vote, went in favour of the nomination of a wiser sage within the club who had been investing for many years. Our sage wanted us to stay local within Cambridge and buy shares in Ionica a telecommunications company in Cambridge. The club was good fun but after Ionica, despite our unrelenting loyalty and refusing to sell, went bust, the investment club became less active. The investment club continued for a couple of years but the realisation to some members that they may actually lose money severely dampened their enthusiasm for the venture.

Undaunted and possibly bolstered by my already growing experience of share success and failure, I confidently continued on my investment journey. I say confidently, although I was honest enough with myself to realise that the dramatic Helphire success, which by this time had trebled in value, owed much more to luck than my prowess as a stock picker: of course, when I did regale the story of my success, it was all down to my smart decision making. I decided I really needed to build my knowledge on what may make a good investable company over a poor company. I continued with various tip sheet publications: The Analyst, Technivest, Quantum Leap and others came within my radar but I never really felt comfortable with either their reasoning or that fact that the share price was usually up by about 15% directly on the Monday morning following publication. I continued to plough through newspapers and then stumbled upon a couple of columnists that struck the right note with me: Jim Slater writing in the Mail on Sunday and Paul Kavanagh in the Sunday Times. I did not realise it at the time but these two guys would have a considerable impact on my investment journey as we headed towards the turn of the century.

Undaunted and possibly bolstered by my already growing experience of share success and failure, I confidently continued on my investment journey. I say confidently, although I was honest enough with myself to realise that the dramatic Helphire success, which by this time had trebled in value, owed much more to luck than my prowess as a stock picker: of course, when I did regale the story of my success, it was all down to my smart decision making. I decided I really needed to build my knowledge on what may make a good investable company over a poor company. I continued with various tip sheet publications: The Analyst, Technivest, Quantum Leap and others came within my radar but I never really felt comfortable with either their reasoning or that fact that the share price was usually up by about 15% directly on the Monday morning following publication. I continued to plough through newspapers and then stumbled upon a couple of columnists that struck the right note with me: Jim Slater writing in the Mail on Sunday and Paul Kavanagh in the Sunday Times. I did not realise it at the time but these two guys would have a considerable impact on my investment journey as we headed towards the turn of the century.

I was becoming very impressed with the work of Jim Slater and bought his incredibly well-written book “The Zulu Principle”. The reasoning within the book was to my mind so very sound, understandable and convincing. Within my salaried employment I was managing a budget of £10 million pounds and dealing with accountants on a very frequent basis and maybe my confidence with financial budgets made the book all the more appealing. Jim mentioned such sensible things as a reasonable valuation for the expectation of future growth in earnings, the relative strength of the share price, the non fudging of profits and returns on capital: all aspects that would become hard coded within my thinking.

Following Jim’s well-reasoned guidance and understanding a little more of the financial criteria, I bought another two stocks: Blacks Leisure and DCS. Both of these stocks rapidly began to motor and I was a very happy investor. Wow, this was really good stuff and as I was feeling absolutely fabulous, I bought another growth stock; Harvey Nichols. Unfortunately, Harvey Nichols failed to move in my favour but the good point was that I was rapidly developing the realisation that even with reasoned share selection, it’s the performance of the collective basket of shares in your portfolio that determines joy or sorrow.

Following Jim’s well-reasoned guidance and understanding a little more of the financial criteria, I bought another two stocks: Blacks Leisure and DCS. Both of these stocks rapidly began to motor and I was a very happy investor. Wow, this was really good stuff and as I was feeling absolutely fabulous, I bought another growth stock; Harvey Nichols. Unfortunately, Harvey Nichols failed to move in my favour but the good point was that I was rapidly developing the realisation that even with reasoned share selection, it’s the performance of the collective basket of shares in your portfolio that determines joy or sorrow.

My thirst for knowledge started to take up more and more of my time as I read various investment books including What works on Wall Street, Beating the Dow but I was so impressed with Jim Slater’s works that I followed up his association with Company REFS and took out a subscription. At the time the publication consisted of the equivalent of a couple or more telephone directory size catalogues; they were heavy beasts as they mounted up and pre-computing took a massive amount of time to sort. The good thing was, however, that absolutely superb financial data had become available to joe public but at a cost. So for me, the post service became a source of not only data but the contract notes for my share trading. The trading commissions themselves could easily eat a hole in your portfolio value as at least one broker I was using at the time had a charge of £45 per transaction; nothing like the £5 for any amount that we are spoilt with today.

I started to attend various meetings & lectures in London, particularly ones involving lucky Jim; they were really so informative. I also remember attending one hosted by the owner of the Analyst tip sheet where it was explained to the audience that JJB sports was a share that you should plan to hold for life; although I held JJB at the time, I found the “hold for life part” a touch difficult to follow & indeed my scepticism was proven to be correct some years later.

The internet was now coming of age but to get on-line at work back in 1997 was something of a challenge: whatever did the directors think we were going to do with such access. It became clear that I needed to buy my own PC for home use and I invested £2000 in a start of the art 4GB hard drive, 64mb RAM monster with a 15-inch screen; now we are flying with my dial-up internet connection!

This was my first PC and it could hook up to the internet! Now getting online; wow was I lucky, all of this information on free bulletin boards written by people who were obviously in the know yet willing to share their wealth of knowledge to all: welcome to the world of ramping.

Overall I was a happy chap, I was learning all the time about share selection and making money. I used to have many coffee break discussions with Gordon who had the contract to maintain the power facilities in the labs. Gordon was a very keen investor but each coffee conversation started with his cursing of Adil Nadir and Polly Peck; Gordon had suffered a particularly bad experience in that area. Anyway, on this particular morning, Gordon said “my broker has been trying to push me in the direction of Fibrenet, reckons technology is the next hot thing”, “what do you think Bill”?

This was my first PC and it could hook up to the internet! Now getting online; wow was I lucky, all of this information on free bulletin boards written by people who were obviously in the know yet willing to share their wealth of knowledge to all: welcome to the world of ramping.

Overall I was a happy chap, I was learning all the time about share selection and making money. I used to have many coffee break discussions with Gordon who had the contract to maintain the power facilities in the labs. Gordon was a very keen investor but each coffee conversation started with his cursing of Adil Nadir and Polly Peck; Gordon had suffered a particularly bad experience in that area. Anyway, on this particular morning, Gordon said “my broker has been trying to push me in the direction of Fibrenet, reckons technology is the next hot thing”, “what do you think Bill”?

Hmm now there is a thought; I will really have to look into this one but nest not hang around as the price is flying away!

Chapter 3: Technology Stocks: The Only way Is Up!

The investment landscape started to change rapidly in the late 90’s and whilst I had had a very good run in Blacks Leisure, JJB, MSB International, and Severfield Reeve as the prices started to fall back I took my profits and also booked slight loss on Harvey Nichols: all stocks that had been identified via Jim Slater’s methods. In those relatively early days, I would only be running around 6 to 8 stocks in my portfolio. It’s a crazy feeling because at the time I was beating myself up for having made only a 60% profit on this basket of shares. I thought to myself “if I had been smarter and sold at the top my gains would have been way over 100% for no more than 18 months of investment. Thankfully, I don’t think that way anymore and can live very comfortably with myself in the knowledge that I will probably never be able to purchase at the bottom and sell at the top. However, I did take quite some more years investing before I could leave my remorse of not selling closer to the top behind me.

I now had a fair amount of cash sitting in my PEP/ISA and only a couple of stocks including DCS which I kept holding as Jim Slater kept writing so enthusiastically about it. I then started thinking of those Fibernet shares that Gordon our electrical contractor, had been mentioning and decided that it was time to try something else and take a much closer look at IT shares. I had some good knowledge of IT companies as my own company had outsourced the provision of all IT services to a third party, our IT partner, on an amazingly expensive contract; I really could not believe the costs we were paying and all because our own in-house IT expertise was allegedly not up to the job.

I now had a fair amount of cash sitting in my PEP/ISA and only a couple of stocks including DCS which I kept holding as Jim Slater kept writing so enthusiastically about it. I then started thinking of those Fibernet shares that Gordon our electrical contractor, had been mentioning and decided that it was time to try something else and take a much closer look at IT shares. I had some good knowledge of IT companies as my own company had outsourced the provision of all IT services to a third party, our IT partner, on an amazingly expensive contract; I really could not believe the costs we were paying and all because our own in-house IT expertise was allegedly not up to the job.

At this time, I was also attending meeting after meeting with our IT outsource company as they preached their version of the Y2K commercial opportunity, apologies, I mean the millennium bug. We were all doomed to perish when the clock struck midnight on 31st December 1999 unless our consultant IT partners determined each piece of IT kit was safe: just for clarity, I am talking about fairly straightforward analytical instrumentation not aeroplanes. I started to get the feeling that IT service companies had discovered a money tree, a very lucrative investment opportunities & sadly as all of our IT expertise who may have been able to question some of the wisdom had been transferred to the consultants; we were there for the taking, like shooting fish in a barrel.

Yes, the technology world was rapidly impacting on the stock markets: respectability and excitement could easily be demonstrated by a company if it had the magical .com after it’s name or business plan. Within no time at all Technology and internet stocks had become the new Klondike Gold Rush

Once it became clear to investors and speculators that the internet had created a wholly new and untapped international market, IPOs of internet companies started to follow each other in rapid succession. It seemed to me that the business plan of some of these companies was based on little more than just an idea on the back of a fag packet with a flashy vision and obligatory mission statement. The excitement over the commercial possibilities of the internet was so big that every idea which sounded viable could fairly easily receive millions of pounds worth of funding. The basic principles of investment theory with regard to understanding when a business would turn a profit if ever, were ignored in many cases, as investors were afraid to miss out on the next big hit. They were willing to invest large sums in these companies many of which had more of an idea rather than a feasible plan. The survival of most of these companies depended on the rapid expansion of its customer base, which in most cases meant huge initial losses. Try as I did at the time, I just could not get a “must have” feeling about pure internet play stocks and never invested in one as such.

However, I became very much in tune with any form of technology business that seemed, at least to me, to have a tangible product to offer: IT consultancy, outsourcing of IT services, procurement, software developers etc. I became totally hooked; you could say I was an IT junkie. During the late 90’s conventional wisdom went out of the window; who wants to invest in a company that actually makes something; paying dividends is boring. Good old reliable Mickey Clark on the BBC’s Wake Up to Money used bemoan the markets “who wants to but smoke-stack companies, you know the ones who make something and pay a dividend”?

Not to be missed was Paul Kavanagh’s very readable column in the Sunday Times started to heavily feature plausible technology stocks: Sunday mornings had become very interesting. Many such investment articles in almost all publications caught the IT mood of the time as the technology bubble formed. As I said, I was far from immune to this technology fever and my portfolio had just about abandoned the previous Zulu style principles and climbed aboard for the tech ride. My portfolio now became fully invested in a whole range of technology stocks: Anite, Comino, Dataflex, Diagonal, Financial Objectives, Kewill, Logica, London Bridge Software, MMT Computing, Merant, NSB Retail Systems, Plasmon, Royal Blue, Redstone, Staffware & Triad. What was that dinosaur term of diversification all about? I had become a complete technology junkie, not a very relaxed junkie but nevertheless a junkie.

Once it became clear to investors and speculators that the internet had created a wholly new and untapped international market, IPOs of internet companies started to follow each other in rapid succession. It seemed to me that the business plan of some of these companies was based on little more than just an idea on the back of a fag packet with a flashy vision and obligatory mission statement. The excitement over the commercial possibilities of the internet was so big that every idea which sounded viable could fairly easily receive millions of pounds worth of funding. The basic principles of investment theory with regard to understanding when a business would turn a profit if ever, were ignored in many cases, as investors were afraid to miss out on the next big hit. They were willing to invest large sums in these companies many of which had more of an idea rather than a feasible plan. The survival of most of these companies depended on the rapid expansion of its customer base, which in most cases meant huge initial losses. Try as I did at the time, I just could not get a “must have” feeling about pure internet play stocks and never invested in one as such.

However, I became very much in tune with any form of technology business that seemed, at least to me, to have a tangible product to offer: IT consultancy, outsourcing of IT services, procurement, software developers etc. I became totally hooked; you could say I was an IT junkie. During the late 90’s conventional wisdom went out of the window; who wants to invest in a company that actually makes something; paying dividends is boring. Good old reliable Mickey Clark on the BBC’s Wake Up to Money used bemoan the markets “who wants to but smoke-stack companies, you know the ones who make something and pay a dividend”?

Not to be missed was Paul Kavanagh’s very readable column in the Sunday Times started to heavily feature plausible technology stocks: Sunday mornings had become very interesting. Many such investment articles in almost all publications caught the IT mood of the time as the technology bubble formed. As I said, I was far from immune to this technology fever and my portfolio had just about abandoned the previous Zulu style principles and climbed aboard for the tech ride. My portfolio now became fully invested in a whole range of technology stocks: Anite, Comino, Dataflex, Diagonal, Financial Objectives, Kewill, Logica, London Bridge Software, MMT Computing, Merant, NSB Retail Systems, Plasmon, Royal Blue, Redstone, Staffware & Triad. What was that dinosaur term of diversification all about? I had become a complete technology junkie, not a very relaxed junkie but nevertheless a junkie.

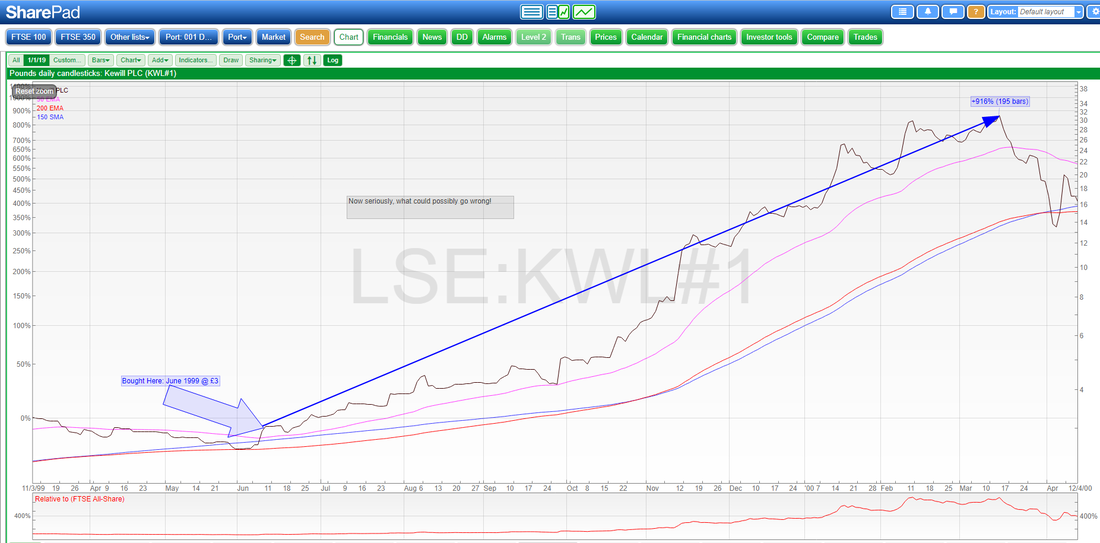

The world had become just unreal; a couple of months could go by and a stock could be up 50% or 100% and in some cases rise almost in a logarithmic fashion. The rate of price rise of these technology stocks was phenomenal: I bought Kewill for just over £3 in June 1999 and eight months later it had risen to over £28 “wow, my stocks were going through the roof”.

Footnote: there is just so much to say about this .COM/Technology bubble that it carries over into the next chapter.

Footnote: there is just so much to say about this .COM/Technology bubble that it carries over into the next chapter.

Chapter 4: Technology & .COM Stocks: Rolling Over The Cliff

A we reached the end of 1999, the paper profits were just becoming unreal and investors were buying into the idea that this one way trip would go on and on: you even had people in well-paid jobs that had become totally seduced by the technology/.COM story and had given up employment to become full-time investors; fortunately I never really got that feeling. The Sunday Times carried a regular feature entitled The Diary of a Day Trader featuring a chap who had quit his secure job during the .COM boom to become a full-time trader working from home. The Diary of a Day Trader was a must-read feature, chronicling the ups and downs of the journey of John Urbanek. Even people who had not bought a share in their entire lives were talking about the column on a Monday morning at work. The column was beautifully honest, “warts and all” and as time went by it was obvious that the new trading life was becoming very tough. Interestingly in his final column, he wrote "I am not throwing in the towel and will continue as a day trader, although somewhat older and wiser than when I started almost two years ago. I would not necessarily recommend that readers follow my lead. It is not an easy life – nor is it an easy way to make money"; Wise words that may he headed by any investor and as I recall there were many less fortunate folk who found the glorious new .COM road would not be paved with gold forever. For my part, I was becoming increasingly nervous at the altitude that my technology stocks were reaching but felt almost powerless to climb off the roundabout, it was surreal; the intoxication just overwhelming.

As the clock struck midnight on new-year’s eve 1999, I was at work completing the tape backup for our valuable laboratory information system, wondering what I was doing there on a new years eve playing service to what I perceived as the Y2K scam. I was also wondering just for long this gold rush could continue. Thankfully the drive home in the early hours of the first of 1st January 2000 proved uneventful; the traffic lights were all still working and as yet no aeroplanes had fallen from the sky: the millennium bug had been beaten; civilisation and the planet saved!

Note: apologies to any IT types involved in valid IT work to beat the Y2K bug; it's just that so much of the analytical kit that had to be certified as Y2K compliant presented almost zero risk.

As the clock struck midnight on new-year’s eve 1999, I was at work completing the tape backup for our valuable laboratory information system, wondering what I was doing there on a new years eve playing service to what I perceived as the Y2K scam. I was also wondering just for long this gold rush could continue. Thankfully the drive home in the early hours of the first of 1st January 2000 proved uneventful; the traffic lights were all still working and as yet no aeroplanes had fallen from the sky: the millennium bug had been beaten; civilisation and the planet saved!

Note: apologies to any IT types involved in valid IT work to beat the Y2K bug; it's just that so much of the analytical kit that had to be certified as Y2K compliant presented almost zero risk.

As for the question of how long this technology gold rush could continue, the answer came along in early 2000 with to my mind a watershed of the .COM bubble in the flotation of Last Minute.com. Lastminute.com floated at a SP of 380p and rose to over 500p in the first hour of trading; the demand was massive and the average punter was allocated 35 shares; what a crazy world. The company had a phenomenal valuation: the magic roundabout built on the edge of the cliff had to grind to a halt and that’s exactly what happened in March 2000. A friend, Bob and I were talking about the madness of the dot.com thirst and the departure from reality with the lastminute.com floatation; little did we know at the time that this was the signal for the end of the technology boom. What followed is now well-documented history as the decline in share price of these briefly loved stocks was about as fast as their rapid rise. Fortunately in the most part, I got out part way through the tumble down the cliff and whilst I had in today’s terms made very healthy gains, they were nowhere near as high as they appeared to be when we were at the top of the cliff. I sold, sold and sold until again my portfolio just had a couple of stocks remaining including a few Redstone’s; how could a company that sponsored the Wales Rugby team be anything but worthy? Yes, that Redstone reasoning of myself seeing the reassurance of a company sponsoring a national side was totally misplaced.

The main part of the decline or fall off the cliff took part over something like an eight week period commencing March 2000, with many IT stocks losing around 80% of their value. In fact, Lastminute.com continued falling for some months to come until it had lost 96% of the valuation it had reached on its first day of trading. For sure, anybody who invested during the late 90’s and early 2000’s will never forget those turbulent days.

Early 2001 became a time to reflect. What would I do now? I had made good profits so far on my journey and learnt a lot. Sadly not everybody was learning as they might; I had investment friends who continued to stay loyal to their technology stocks and refused to sell, living in a world of self-denial. My good friend Bob said to me “Fibernet touched £30 not so long ago and mark my words, it will get back there soon, this fall is only a temporary setback”: to his credit Bob was a very loyal chap he went all the way to the top with his stocks and for the most part stayed loyal all the way to the bottom!

Early 2001 became a time to reflect. What would I do now? I had made good profits so far on my journey and learnt a lot. Sadly not everybody was learning as they might; I had investment friends who continued to stay loyal to their technology stocks and refused to sell, living in a world of self-denial. My good friend Bob said to me “Fibernet touched £30 not so long ago and mark my words, it will get back there soon, this fall is only a temporary setback”: to his credit Bob was a very loyal chap he went all the way to the top with his stocks and for the most part stayed loyal all the way to the bottom!

It was definitely time to sit on my hands, protect a reasonable cash pile and take some time to think; what was this diversification stuff I once thought worthwhile. After my experiences to date, I felt comfortable in that I was learning all the time and probably after the .COM bubble burst I was becoming a touch more cautious but where would I go from here I wondered. What stocks may be a touch more predictable and safe? Hang on, those ex-building societies look interesting and pay a safe dividend and then, of course, there is always the banks; you can’t get much safer than that!

Chapter 5: From Wilderness To Recovery

As I came away from the eventual .COM carnage I started to realise that overall I had done reasonably well from that particular episode. I exited that couple of years with appreciably more funds than when I had entered but still felt that self-critical nagging that if only I had sold some of those high fliers earlier; maybe even got out at the top. As it happens I had learnt from my earlier experiences that once a good thing starts to come to an end, get out. On reflection although I had made good money, I had not been that clever at all: I had really been a member of the herd running into IT stocks as if nothing else existed and in truth setting aside my earlier learning of trying to find and analyse growth companies that actually turned in profits year after year: it was time to head back to that base.

Just how bad did things get once the Technology-.Com bubble burst? Well as you can see from the chart below the FTSE100 fell by a whopping 50% before recovery set in.

Just how bad did things get once the Technology-.Com bubble burst? Well as you can see from the chart below the FTSE100 fell by a whopping 50% before recovery set in.

So my approach from late 2000 was to revert back to trying to identify Zulu type growth companies but this time around it just did not seem so easy; it’s a simple fact that when the market is in a depressed mood even apparent high-quality businesses are held back. I was finding it a real battle to make much of an impact against a background of a steadily declining FTSE 100 that gradually fell from a high of about 6950 at the start of 2000 to a low point of 3300 in early 2003: times were tough and I was being ever cautious and sat on a fair cash-pile. From 2000 to 2002 I did not really make any significant money from the overall basket of stocks that I held; investment life was difficult as the FTSE ground out it’s slow yet relentless path to the eventual bottom. I suppose that I was managing to “hold my own” was down to much greater care than in the .COM herd time. Yet, I still kept beating myself up: hey, I was this kiddie who could do 40% a year in the late 90’s, why won’t it happen now? Yes, I know, on reflection plain delusion of an investor who had become accustomed to making easy money during the last half of the 1990’s. Incidentally during 2000 to 2002 was one of my busiest times in my working life, coupled with the fact that I had moved home into a very old building that became a restoration project, meant that I just did not have much time to meddle. The lack of trading in itself became a real lesson i.e. if you have done some decent research, limited risk by going for quality, then the best friend may well be time in the market. Also at this time funds were needed on the restoration project; the complete re-thatching of a large roof is a jaw-dropping cost but I guess that was a wise use of some of my previous market gains.

That dreaded herd mentality was definitely something I wanted to try and avoid in the future if at all possible. My stock purchases at this time were mostly those with potential for growth but also supplemented by ones that paid a decent yield hopefully to protect the downside and of course the majority of my detective/screening work would be via my trusty Company REFS which thankfully became available in a CD form. There were a few gems that I picked up in 2001/02 as VP at 92p, Wolverhampton & Dudley at an equivalent of just over a pound in today’s money, Fisher(James) and Clarkson both at under £2. Just to give a flavour, my ISA & PEP accounts, yes they were separate in those days also included Hardy & Hanson, Greene King, Scottish & Newcastle, Prudential, Scottish Power, Azlan, Dairy Crest and Vodafone. Not a massive number of stocks but many of which I held onto for a few years and mostly rewarded my loyalty by becoming real stars which is more than I can say for Vodafone post the costly Mannesmann acquisition; the Vodafone performance proved a real drag on the overall portfolio. My mindset wanted to control risk in my ISA/PEP world and do the more risky stuff within my trading account; the logic being that at least I could recoup a percentage of the sillies via CGT offset.

In addition to the continued retracement after the .Com bubble there were, of course, worries when our old buddy Sadam had squirrelled away copious amounts of what became known as WMD. Thankfully, at least for investors, the Iraq question came to something of an end in early 2003 when we had the invasion of Iraq and Baghdad bounce. What a lovely time that was as we moved away from the cliff edge and into a beautiful incline FTSE 100 & FTSE 250 that would last for about five years.

The portfolio was chugging along really decently, no 40% years but the pot was larger and making really respectable gains. Frustratingly over the period from 2003 to 2007, although the returns were good they were at times struggling to keep pace with the FTSE 250 which was racing away as the markets recovered. Was I meddling too much or over trading? Maybe accepting a larger portion of risk with some AIM stocks: would I have been better off avoiding risky AIM stocks, just buying quality growth stocks and sitting on my fiddling hands? The answer is I don’t really think I will ever know for definite but I suspect the sitting on hands bit would have won the day.

As work quietened down a touch and the heavy time demanding house renovation eased, I had more time available, more time to research REFS for quality & growth; that was good but conversely, I also had the time to again chase a few story stocks in my dealing (non-ISA) accounts. The stocks making me profits after 2003 was quality stuff such as VP, Fisher, Clarkson, SDL, AMEC, Peacock, loads of breweries; I probably held stock in the majority of breweries at various times when I think back and let’s not forget banks and insurance companies. Yet it was the silly adventurous purchases mainly on AIM that kept my acceptable enough performance below that of the run-away FTSE 250. I was probably spending too much time reading about “hot stocks” on bulletin boards, a hot tip in IC or some other publication. Remember the “next big thing” types, the likes of Aerobox, Accident Exchange Group, Inion, Media Square, Bioprogress ; the inventors of the dissolvable colostomy bag, I mean can you imagine!. Still, I did learn valuable lessons from my BB experiences and just vowed never to get sucked in again by those claiming to be ITK; I was also bolting on to my armoury the knowledge that debt can be a killer to a small business.

Although this list of small nibbles into adventurous “next big thing” AIM stocks did not help portfolio progress they were mainly either cut at a 20% loss or sold on the first profits warning; to my mind valuable lessons that remain bolted onto mindset from that time onwards. Incidentally, a lesson for every investor to my mind is to have a decent number of reasonably diversified companies and concentrate on the overall basket performance. If you have to “gamble around the edges” then do this with a very limited percentage of your overall pot outside of your tax-free account; better still, if you need that style of excitement take up bungee jumping, glider flying or some other less dangerous pastime.

Within my “day job”, my own company, whose performance I never counted within my percentage returns as that was simply my good fortune of being in the right place at the right time, was bought out for almost £16 in 2006 by a consortium of Canadian and Australian insurance/pension companies. I was a very happy man as I had studiously taken up almost to the limit, every share-save offer with prices ranging from £2 to £6: I was just gob-smacked by the eventual return of funds. Totally no skill involved apart from the discipline of maintaining the continual drip feed purchase of AWG shares at an advantageous price and very importantly, the passage of time, in fact, lots & lots of time.

By mid 2007 the whole investment world was buzzing along cheerfully enough for me as I was close to being fully invested not solely in growth stocks but also in those lovely safe financial institutions namely the large unexciting insurance companies plus various banks including the newly listed ex-building society types; what lovely safe dividends these boys paid; I thought at the time what could possibly go wrong to rock this steady little investment world that I enjoyed?

Epilogue: Learning Points as at December 2007

Memo to myself in late 2007: Learning Points so far that I would do well to remember but being as fallible as the next person, would almost certainly temporarily forget from time to time:

The portfolio was chugging along really decently, no 40% years but the pot was larger and making really respectable gains. Frustratingly over the period from 2003 to 2007, although the returns were good they were at times struggling to keep pace with the FTSE 250 which was racing away as the markets recovered. Was I meddling too much or over trading? Maybe accepting a larger portion of risk with some AIM stocks: would I have been better off avoiding risky AIM stocks, just buying quality growth stocks and sitting on my fiddling hands? The answer is I don’t really think I will ever know for definite but I suspect the sitting on hands bit would have won the day.

As work quietened down a touch and the heavy time demanding house renovation eased, I had more time available, more time to research REFS for quality & growth; that was good but conversely, I also had the time to again chase a few story stocks in my dealing (non-ISA) accounts. The stocks making me profits after 2003 was quality stuff such as VP, Fisher, Clarkson, SDL, AMEC, Peacock, loads of breweries; I probably held stock in the majority of breweries at various times when I think back and let’s not forget banks and insurance companies. Yet it was the silly adventurous purchases mainly on AIM that kept my acceptable enough performance below that of the run-away FTSE 250. I was probably spending too much time reading about “hot stocks” on bulletin boards, a hot tip in IC or some other publication. Remember the “next big thing” types, the likes of Aerobox, Accident Exchange Group, Inion, Media Square, Bioprogress ; the inventors of the dissolvable colostomy bag, I mean can you imagine!. Still, I did learn valuable lessons from my BB experiences and just vowed never to get sucked in again by those claiming to be ITK; I was also bolting on to my armoury the knowledge that debt can be a killer to a small business.

Although this list of small nibbles into adventurous “next big thing” AIM stocks did not help portfolio progress they were mainly either cut at a 20% loss or sold on the first profits warning; to my mind valuable lessons that remain bolted onto mindset from that time onwards. Incidentally, a lesson for every investor to my mind is to have a decent number of reasonably diversified companies and concentrate on the overall basket performance. If you have to “gamble around the edges” then do this with a very limited percentage of your overall pot outside of your tax-free account; better still, if you need that style of excitement take up bungee jumping, glider flying or some other less dangerous pastime.

Within my “day job”, my own company, whose performance I never counted within my percentage returns as that was simply my good fortune of being in the right place at the right time, was bought out for almost £16 in 2006 by a consortium of Canadian and Australian insurance/pension companies. I was a very happy man as I had studiously taken up almost to the limit, every share-save offer with prices ranging from £2 to £6: I was just gob-smacked by the eventual return of funds. Totally no skill involved apart from the discipline of maintaining the continual drip feed purchase of AWG shares at an advantageous price and very importantly, the passage of time, in fact, lots & lots of time.

By mid 2007 the whole investment world was buzzing along cheerfully enough for me as I was close to being fully invested not solely in growth stocks but also in those lovely safe financial institutions namely the large unexciting insurance companies plus various banks including the newly listed ex-building society types; what lovely safe dividends these boys paid; I thought at the time what could possibly go wrong to rock this steady little investment world that I enjoyed?

Epilogue: Learning Points as at December 2007

Memo to myself in late 2007: Learning Points so far that I would do well to remember but being as fallible as the next person, would almost certainly temporarily forget from time to time:

- Avoid bulletin board experts, they just simply claim to have the inside track knowledge and they invariably do not: it's all too often ramp-pump & dump.

- Invest in quality data to aid your investment decisions: my thirst included Sharescope (I think it’s fair to say I was one of their earliest customers), Company Refs and SharelockHolmes.

- Concentrate of quality and stocks that are already displaying the signs of being winners: increasing turnover, increasing profits, reasonable margin and a touch of momentum.

- Try to only invest in companies that carry manageable or preferably no debt; screen out the others.

- Look for companies that make decent returns on capital; ROCE

- Try to avoid businesses with a touch of creative profit creation: CPS preferably greater than EPS; Cash-flow is just so important & a touch more difficult to manipulate.

- Try to have at least some degree of diversification across a few sectors and market caps.

- Be a bit less critical of yourself as it’s almost a certainty that you will never get in at the bottom or sell at the top; don’t beat yourself up trying.

- Have an exit plan for a stock; it’s all too easy to buy but selling requires a different discipline. For me, it was a 20% stop loss at this time or some knowledge that the original attraction for the investment had changed. You simply have to manage the downside risk.

- Desperately try not to form an emotional attachment to a stock it has no emotion or feelings & can’t love you back; a Labrador can whilst a dog of a stock can’t.

- If I you have to invest in anything that could be described as a story stock, a blue sky punt etc then don’t do this within your valuable PEP/ISA tax-free pot.

Chapter 6: The Financial Crisis & Toxic Debt

Well, things had been chugging along well enough since the Iraq invasion back in early 2003 and by the end of 2007, the portfolio was looking in a very healthy state. I was really enjoying my investment life almost more so than my professional life. I was employed by an excellent company, essentially the same company for over thirty years. I had grown within that company, my career flourished and I had in truth been far more successful than my humble ambitions ever warranted. However, as with all big companies, there is forever a need of the various CEO’s to own a cultural change within a business. In truth, many such changes are simply the previous sets just repackaged and delivered by another group of consultants. Now I am not saying this is necessarily something that would put anybody off within a business but in my case, I felt like I had been on the roundabout too long and the desire to jump through the same or similar hoops was simply diminishing. I decided that I needed to accelerate my AVC contributions vastly and laid a plan to retire early from science no later than 2011 and become essentially a full-time investor. Heavens, just think I could still be employed in what is still honestly a wonderful company but I just do not miss the performing tricks part of company culture one bit.

Well, the plan was set in place and the finances carefully arranged; the stock market had been kind to me but as we reached the end of 2007 a few little dark clouds started to appear on the distant horizon; namely chatter about banks in the USA made loans to citizens that were unlikely to be paid. The area of main concern was sub-prime mortgages if effect the banks were making loans to people who did not stand a realistic chance of coping with that loan. Alfie, a colleague who dabbled in shares and was rather like an Italian version of Private Frazer from Dad’s Army, came bounding into my office to tell me “toxic debt mate, I tell you it’s really bad, really bad”: what is it this toxic debt stuff Alf, I asked, “don’t know mate, but I tell you it is really bad” replied Alfie. That conversation was typical of the time as we rapidly entered a period when everybody used the term toxic debt and fast became a financial expert. However, in common with all experts associated with the financial world at the time, nobody really had a clue about what was wrong, who it affected or indeed the eventual magnitude of that effect.

One of the first UK banks to have the jitters was Northern Rock. Foolishly to me at the time it looked a bargain and I added a few into my ISA only to sell them nine days later for a 30% loss after the news reported massive queues of customers wanting to withdraw their cash from the bank despite the government pledge to guarantee savings up to £80k . Had I waited a short while longer, my loss would have been greater than 85%; decisive swift action or luck, I don’t know but at least my loss had been limited. It felt like a Groundhog Day moment, "Déjà vu all over again", surely the market declining pattern of early 2000 was not about to be repeated; no, surely not!

Well, the plan was set in place and the finances carefully arranged; the stock market had been kind to me but as we reached the end of 2007 a few little dark clouds started to appear on the distant horizon; namely chatter about banks in the USA made loans to citizens that were unlikely to be paid. The area of main concern was sub-prime mortgages if effect the banks were making loans to people who did not stand a realistic chance of coping with that loan. Alfie, a colleague who dabbled in shares and was rather like an Italian version of Private Frazer from Dad’s Army, came bounding into my office to tell me “toxic debt mate, I tell you it’s really bad, really bad”: what is it this toxic debt stuff Alf, I asked, “don’t know mate, but I tell you it is really bad” replied Alfie. That conversation was typical of the time as we rapidly entered a period when everybody used the term toxic debt and fast became a financial expert. However, in common with all experts associated with the financial world at the time, nobody really had a clue about what was wrong, who it affected or indeed the eventual magnitude of that effect.

One of the first UK banks to have the jitters was Northern Rock. Foolishly to me at the time it looked a bargain and I added a few into my ISA only to sell them nine days later for a 30% loss after the news reported massive queues of customers wanting to withdraw their cash from the bank despite the government pledge to guarantee savings up to £80k . Had I waited a short while longer, my loss would have been greater than 85%; decisive swift action or luck, I don’t know but at least my loss had been limited. It felt like a Groundhog Day moment, "Déjà vu all over again", surely the market declining pattern of early 2000 was not about to be repeated; no, surely not!