|

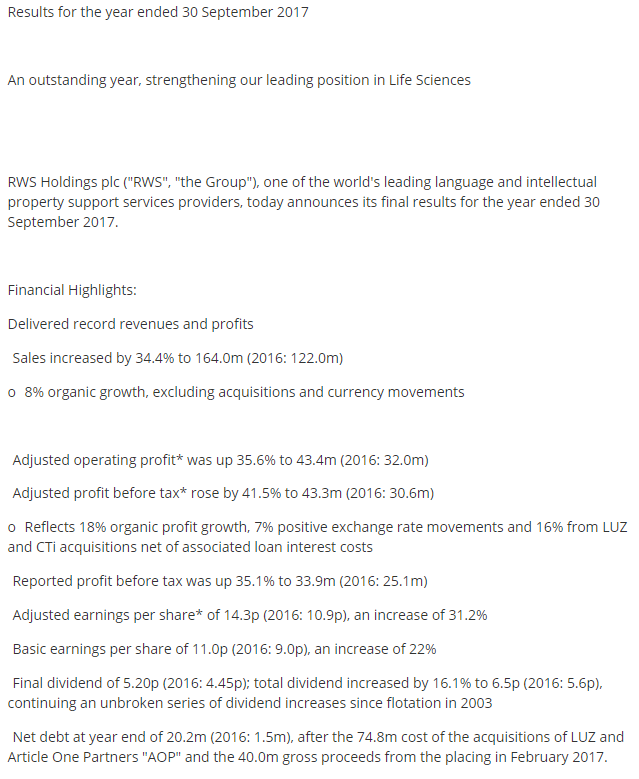

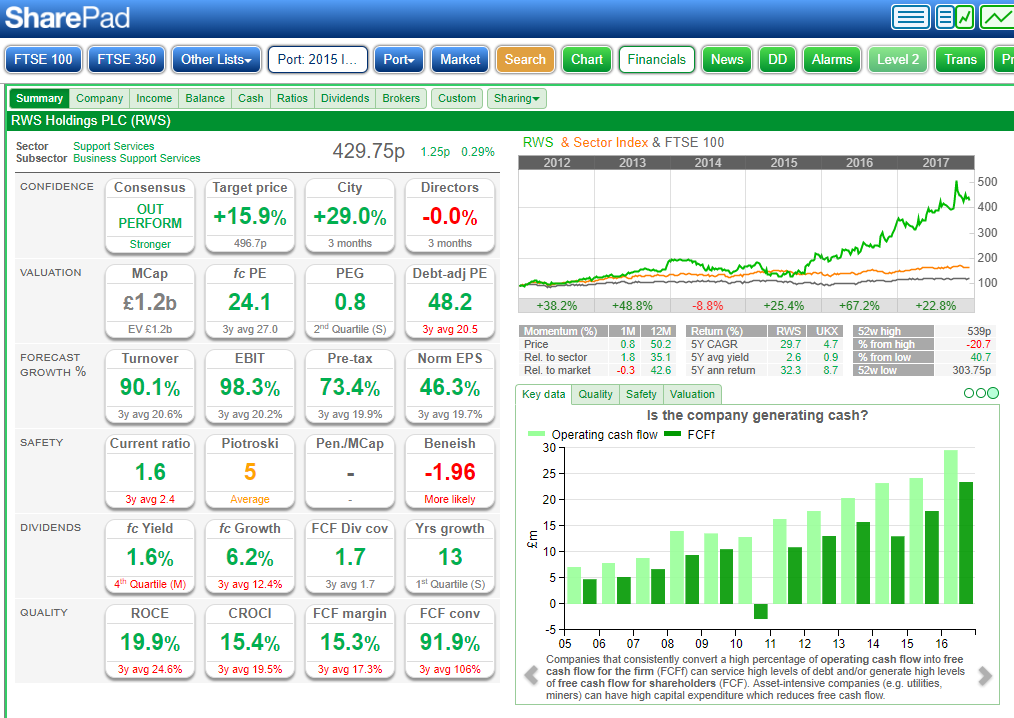

Voyager RNS Log WC 10/12/2017 After the motherboard failure, I had on my last self-build PC, can’t complain as it was 9 years old and starting to groan just a little, I am now a happy IT man again having purchased a really splendid Microsoft Surface Tablet/Notebook as a backup to my new desktop PC. I just love having SSD HDs as you can be on the net within about 15 seconds of starting up. Yes, I know apple/android systems (I also have both) can be almost instant but with Apple, they are absolute control freaks you constantly feel they are just letting you use their devices out of sheer goodwill. Whilst Android has those little battery eating androids gobbling up battery power when you are not looking. Anyway, ShareScope is such a vital part of my armoury, I have to have a .exe environment to operate it hence Windows 10. I must admit these days I find myself continuously using SharePad/ShareScope and tend to neglect my Stockopedia, another excellent tool; just happens that way for me. Anyway, enough IT type whittling, let’s have a look at recent RNS activity within the Portfolio. This week I am including a short update for last week which thankfully was rather quiet and gave me much needed breathing space to complete the membership transfer on the Ltfcfool, a new discussion forum for Hatters fans; yes, I know you have to be a long-suffering fool to be a Hatters fan: an incurable affliction that renders the sufferer way beyond help. Tuesday 5th December 2017: Amino Technologies: AMO: Mkt Cap £134m: Trading Update Trading Update and Notice of Results Profit and margins in line with market expectations Amino Technologies plc (LSE AIM: AMO), the Cambridge-based provider of digital entertainment solutions for IPTV, Internet TV and in-home multimedia distribution, today provides the following trading update for the year ended 30 November 2017. The Group expects to report a full year performance that demonstrates continued customer traction for its IP / cloud video software solutions and devices, despite industry-wide memory cost headwinds. Gross profit and adjusted profit before tax are expected to be in line with market expectations, whilst revenue is expected to be similar to the previous financial year due to product mix. The Company's cash position at 30 November 2017 was GBP13.0m (30 November 2016: GBP6.2m) as a result of good operating cash conversion. Commenting on today's announcement, Keith Todd CBE, Non-Executive Chairman said: "I am encouraged by Amino's strong operational performance with good profit margins and excellent cash generation. As we continue to deliver momentum and scale, we are seeing growing traction for our software solutions and new product lines. We enter 2018 with a solid backlog and an excellent pipeline which provide us with confidence for the year ahead and beyond." The Company will announce its full year results on 6 February 2018. My View: I am comfortable enough with this in-line trading update; no nasty shocks and on track to deliver market expectations. The shares are not on a demanding valuation with a PE 13.9 which falls by about 10% when you take into account the good cash position. Brokers forecast an eps growth of around 25% and the shares offer an attractive yield of 3.6%. Stockopedia stock ranks system also indicates AMO as attractive with an SR of 91. Looking my preferred selection criteria of return on capital (ROCE & CROCI) & FCF; all of which look attractive, I am happy to continue to hold this interesting technology company. Wednesday 6th December 2017: RWS Holdings: RWS: Market Cap £1.2b: Final Results:  Outlook: The Group has made a strong start in the first two months of the new financial year, in line with our expectations that we will continue to build upon the record levels established in 2017 RWS now possesses an outstanding global platform, which will enable it to develop sales opportunities in multiple geographies, with a complete range of language management services and technology offerings. My View: Good progress with the promise of more to come including the transformational acquisition of Moravia. I think a lot of investors see RWS as an expensive stock on a PE of 23 but I prefer to focus on the very attractive returns of capital (ROCE & CROCI), ability to generate FCF and its impressive eps forecast growth rate of 46%. Data from SharePad shown below:

Tuesday 12th December 2017: Zytronic: ZYT: Market Cap: £82m: Final Results: Preliminary Results for the year ended 30 September 2017 (audited) Zytronic plc, a leading specialist manufacturer of touch sensors, announces its preliminary results for the year ended 30 September 2017. Overview Significant improvement in Group trading profits to 5.4m (2016: 4.3m) Strong cash generation from operating activities of 4.7m (2016: 5.6m) Final dividend increased by 39% to 15.2p (2016: 10.96p), bringing total dividends for the year to 19.0p (2016: 14.41p), up 32% year-on-year and the fourth successive year of double-digit dividend growth Touch sensor units sold increased to 138,000 units (2016: 130,000 units) with large sensors > 30" increasing to 18,000 units (2016: 14,000) Basic earnings per share increased to 29.0p (2016: 26.6p) Commenting on the outlook, Chairman, Tudor Davies said: "The current year has started with orders, revenues and trading along similar levels to that of the prior year which together with our strong balance sheet and cash generation provides a sound base for further growth in dividends and shareholder value." My View: Zytronic is another of my smaller companies that I have held for a reasonable length of time, about three years and whilst containing the risks that many small companies are exposed to including a reliance of a fairly small group of clients, they are in my view a quality outfit. However, having said that, they are not one that may appeal to the investor in a rush as witnessed by the short-termism that drove the share price up to well over 600p ahead of the October trading update. At that time I decided that nice as ZYT is, that it had become a tad overheated and top sliced about 30% of my holding to watch the shares gradually drop back to around 500p. I just do not understand the impatience of some “fast buck” investors; that approach just does not do it for my watchful but more patient temperament. So how do the results look? Well, eps marginally beat brokers forecasts at 29p and the dividend has significantly increased, up by 39%. Additionally, ZYT seems to be awash with cash. Chuck in the forecast yield of 4.5%, my favoured ROCE/CROCI and ZYT’s ability to generate free cash flow and that leaves me as a happy yet patient holder. As for growth, that’s a little conservative in terms of the outlook from the company but in fairness, they have tended to be anything but boastful in the past. Wednesday 13th December 2017: Keyword Studios: KWS: Market Cap £912m: Acquisition of Sperasoft Services Extended into Co-Development, expanding Engineering Service Line Entry into Eastern Europe Keywords Studios, the international technical services provider to the global video games industry, today announces that it has acquired Sperasoft Inc and Sperasoft Studio LLC (together, "Sperasoft"), for a total consideration of $27 million from the founders Igor Efremov, Alexei Kudriashov and Mark Rizzo (the "Sellers"). Headquartered in Santa Clara, California, Sperasoft provides game development, art creation and software engineering services to video game developers and publishers around the world from its production studios in St Petersburg and Volgograd, Russia and Krakow, Poland. Over the years, Sperasoft has delivered consistent high quality work for its clients including Electronic Arts, Ubisoft, Warner Bros and Riot Games. For instance, the company is proud of the recent work of its St Petersburg studio, which worked alongside five of Ubisoft's internal studios to develop Assassin's Creed: Origins, which launched to critical acclaim on 27th October 2017. The acquisition of Sperasoft is in line with Keywords Studios' strategy to grow organically and by acquisition as it selectively consolidates the highly fragmented market for video game services. Sperasoft adds considerable expertise and scale to Keywords new and growing Engineering Services business and adds additional scale to the Art creation business. In joining the Group, Sperasoft also provides Keywords with production centres and supporting management in Russia and Poland which are important locations for video game services talent across all of Keywords service lines. Sperasoft has grown steadily over the years increasing revenues from $10.4m in 2015 to $16m in 2016. It is anticipated to grow to approximately $20m for the year ending 31 December 2017. The underlying adjusted EBITDA for 2017 is expected to be approximately $2m. Under the terms of the acquisition, which is expected to be earnings enhancing in the first year, Keywords is paying a total consideration of $27m. This is being satisfied by $22m in cash, $1.0m of which is deferred until the first anniversary of the acquisition, funded from the Group's existing resources. The remainder is being satisfied by the issue of 260,049 new ordinary shares in Keywords, which will be issued to the Sellers on the first anniversary of the acquisition and will then be subject to orderly market provisions for a further 12 months. Friday 15th December 2017: Keyword Solution and another acquisition: LOLA Keywords Studios, the international technical services provider to the global video games industry, today announces that it has acquired the assets and business of Localizadora Latam SC ("LOLA") for a total consideration of up to US$1.03m from its founders, Alejandro González and Luis Daniel Ramírez. Based in Mexico City, LOLA provides Latin American Spanish dubbing, localisation and sound design services for the video game, film and television markets, with clients including Warner Bros and Ubisoft. Founded in 2013, LOLA has built a reputation for quality and Keywords Studios currently uses the services of LOLA to complement those of its wholly owned local voice recording studio, Kite Team Mexico. Following the acquisition, Keywords' existing Kite Team operations in Mexico City will be integrated with those of LOLA to create the market leading provider of services for Latin American Spanish localised video games. LOLA had revenues of US$1.2m in 2016. In the year to 31 December 2017 the company is expected to maintain this performance, with an estimated normalised PBT of US$250,000. Approximately 40% of its revenues relate to work subcontracted from Keywords Studios. Under the terms of the acquisition Keywords is paying a consideration comprised of US$480,000 in cash and the issue of 10,106 new ordinary shares in Keywords, which will be subject to a one-year lock in period. Keywords will pay a further amount of up to $350,000 in cash over the next 2 years dependent on LOLA achieving certain performance targets. My View: Sperasoft this is the second largest acquisition made by my favourite Mecanno company KWS and involves the inclusion of 400 technical types onto the companies books. KWS is really becoming a sizable business and has considerably grown since I first purchased the stock. The second acquisition of the week seems a logical low risk bolt on of LOLA a company that KWS know very well as they subcontract work to them. I doubt Lola will cause the sort of surprises that Ray Davies of the excellent Links sang about back in 1970. Yes, by conventional measures the shares do look expensive hovering at around the 1500p mark but then again I thought that by conventional measures they looked expensive when I first bought at just over 300p. As mentioned before in this series of Voyager notes, I did top slice these on the first of September 17 taking out in terms of capital, my entire original spend. That still leaves me with a significant investment in KWS that essentially I run for free. Looking at the conventional PE we have a dizzy value of around 50 for PE but equally an exceptional forecast eps growth rate of over 40% plus my usual comfort blanket of very attractive returns on capital. I remain a happy holder but nevertheless one that is very aware that one of the spinning plates, in terms of managing the acquisition could easily crash to the floor. Investors may find the article form the Evening Standard of interest: https://www.standard.co.uk/business/stateside-swoop-for-keywords-in-27m-raid-on-assassin-s-creed-firm-a3718511.html Glad I Am Not There (GINT): well, it’s a fairly big one in terms of market capitalisation in Saga and in fact a company I bought shares in at the IPO at about 185p and sold a couple of years later for a total return of about 10%. No moans from me there as 10% is I agree not impressive but within an overall basket of shares it does no harm the bottom line. I should say that I do like the Saga way of doing business; they appear very professional to me and I certainly use their platinum credit card rather than cash abroad. Yet Saga has been hit by the collapse of Monarch Airlines and have allowed for a one-off hit of £2m to cover the financial fallout. In my view, although it qualifies for a GINT, I think the overall business is good and expect it to make a recovery from the current depressed share price that sits around the 125p mark. This weekend I travel to the football ground owned by the new age traveller Dale Vince a man famous for his green energy credentials and I have to say well done to him; admirable stuff. The Forest Green FC ground is up the top a great big hill in Nailsworth. It’s not only the location that makes the place interesting, the locally brewed beer is good and the club has a strict vegetarian policy in the very welcoming pub, The Green Man, that forms part of the stadium. Not your usual terrible football food offering at this ground where quite palatable veggie burgers are the order of the day. Whatever you are doing this weekend, have a good one and don’t spend too much time looking for the mythical Santa Rally of the markets; I never really bought totally into that one.

0 Comments

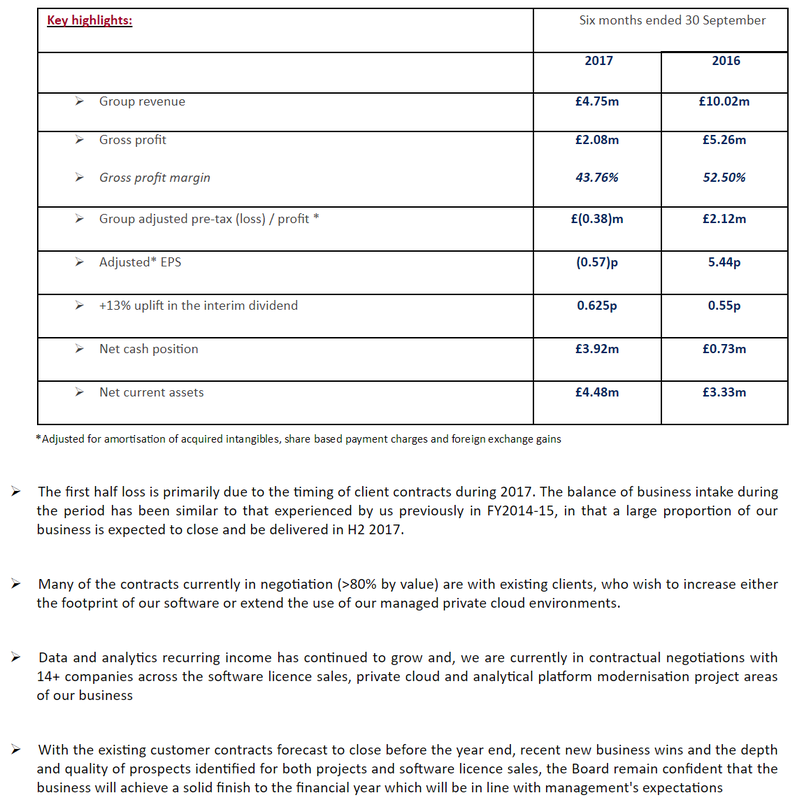

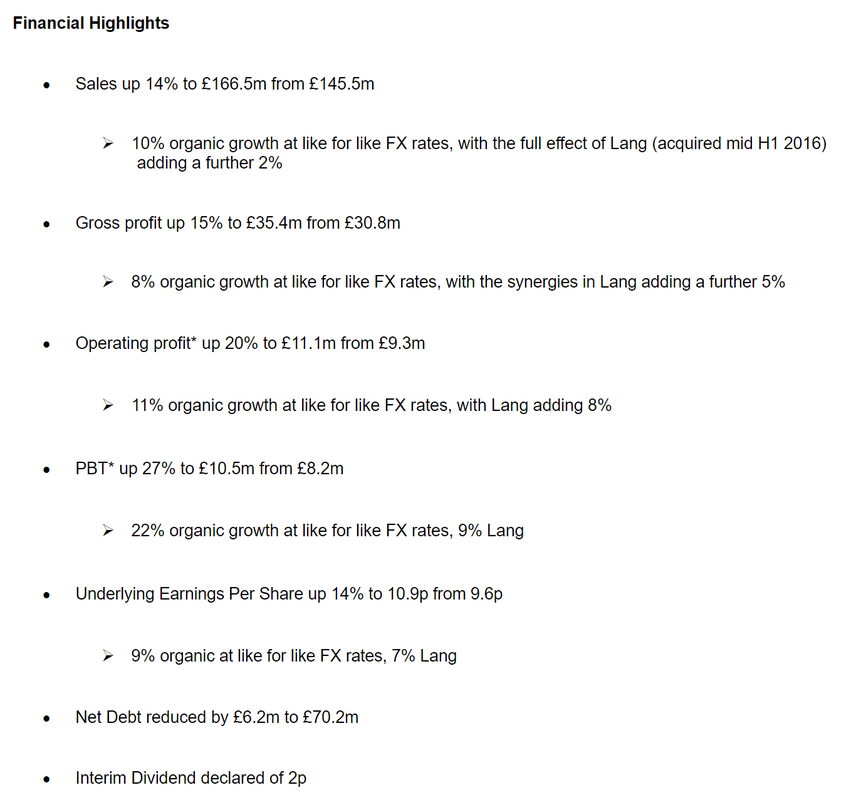

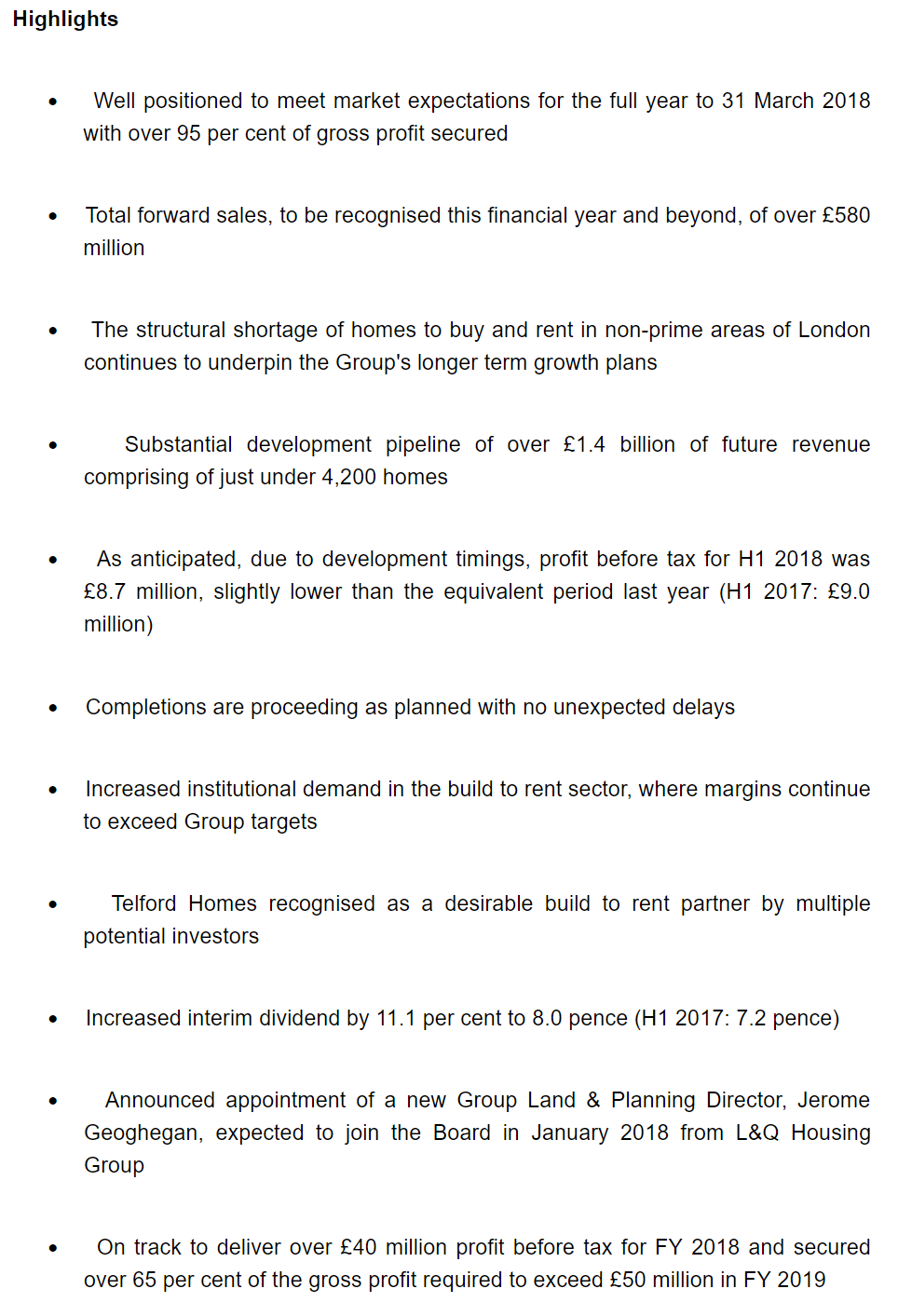

Voyager RNS Log WC 26/11/2017 Oh dear, the perils of train travel. My weekend trip to Crewe for the Hatters game had to be abandoned at Birmingham New Street station as the train arrived over two hours late due to a broken rail north of Leicester. So instead of football, I retrieved what I could from the day by visiting the Birmingham Frankfurt Xmas market; beer & bratwurst. The beer was nice but the sadly the bratwurst had all of the culinary delights you would expect from an emulsified pig. Still, such is life: now how about the RNSs that affect stocks within the portfolio over this week? Monday 27th November 2017: No RNSs for shares held within the portfolio. Tuesday 28th November 2017: D4t4: Mkt Cap £51m Interim Results "As experienced in some previous years a higher proportion of our business is expected to close and be delivered in H2 2017. Despite a lower first half due primarily to a change in the timing of contract awards by comparison to the same period last year, the Board remains confident of achieving management expectations for the full year based on recent business wins and the depth and quality of the prospects pipeline."  The first half loss is primarily due to the timing of client contracts during 2017. The balance of business intake during the period has been similar to that experienced by us previously in FY2014-15, in that a large proportion of our business is expected to close and be delivered in H2 2017. Ø Many of the contracts currently in negotiation (>80% by value) are with existing clients, who wish to increase either the footprint of our software or extend the use of our managed private cloud environments. Ø Data and analytics recurring income has continued to grow and, we are currently in contractual negotiations with 14+ companies across the software licence sales, private cloud and analytical platform modernisation project areas of our business Ø With the existing customer contracts forecast to close before the year end, recent new business wins and the depth and quality of prospects identified for both projects and software licence sales, the Board remain confident that the business will achieve a solid finish to the financial year which will be in line with management's expectations My View: the loss in the first half of the year is a touch disappointing but of more of concern to me is the lack of a real feeling of confidence with the visibility of sales. Phrases such as “business (completion of orders) is expected to close and be delivered in H2 2017 “and “we are currently in contractual negotiations with 14+ companies” just don’t give me enough of a good feel or reassurance to continue to hold all of my position in D4t4 and I therefore, have carried out a very unemotional sale of 70% of my holding for a manageable 12% loss. Despite fairly significant director buying post interims, I feel there is just too much uncertainty for my comfort and have now greatly reduced my position. Tuesday 28th November 2017: IG Design (IGR): Mkt Cap £260m formerly known as International Greetings. Interim Results:  Outlook Whilst cost headwinds are undoubtedly stronger than ever, our businesses are well positioned to combat these. A full order book and a strong performance in the first half of the year provides confidence that the Group is fully on track to meet full year market expectations for profit and other key underlying metrics. My View: Punters got overly excited about IGR and unsustainably drove the price up by almost 10% just a couple of days before the interims. On the day of the interims, the shares dropped back due to probably a bit of profit taking and the gamblers waking up to a very good but steadily growing company that will not make them rich overnight: get rich quick is definitely not my style if investing; it only happens in Hollywood movies and the lottery. The results are in my opinion very good with increasing sales, increasing profit and organic growth supplemented by additional growth from the acquisition of the business Lang. Decent returns on capital and good cash flow/free cash flow; my kind of business and one that has given me handsome return since re-entering the stock at less than 180p in early April 2016. The closing price on 30/11/17 was 414p. A Happy investor who will continue to hold. Wednesday 29/11/2017: Telford Homes: TEF: Market Cap: £314m: Interim Results.  Outlook We are firmly on track to deliver profit before tax in excess of £40 million for the year to 31 March 2018, in line with market expectations, having secured over 95 per cent of anticipated gross profit. We have also already secured over 65 per cent of the gross profit required to exceed £50 million of profit before tax in the year to 31 March 2019. My View: Usually a phrase such as 2nd half weighted/H2 weighted rather concern me but not in the case of Telford a very well managed business that continues to deliver and to my mind is the most attractive of the builders based upon current valuations and it’s good prospects. I will continue to hold. Thursday 30/11/2017: On The Beach: OTB: Mkt Cap: £580m: Preliminary Results:  Current trading and outlook

The first quarter of our financial year (calendar Q4) is historically the quietest trading period for the Group. The low cost carrier summer 2018 seat release came earlier than last year and in part helped to offset the disruption caused by the Monarch Airlines Limited failure and repeated flight cancellations borne out of air traffic control and pilot strikes. On many of the routes from regional departure points where Monarch had a higher proportion of the flight capacity we are already seeing replacement capacity being positioned. In calendar Q4 last year sales for summer 2017 were impacted by the tour operator currency hedge and the Western Mediterranean hotel price inflation. Neither of these headwinds have been prevalent in the start to FY18. In addition to this, consumer appetite for and capacity travelling to destinations in the Eastern Mediterranean are strongly up year on year and against this backdrop the Board is pleased to report that current performance is in line with expectations and believes the business is well positioned for the key trading period that commences in late December and continues into Q1 2018. My View: A sound set of results for OTB having good returns on capital and usually very decent cash flow, reinvesting in the business and continuing to grow at a good rate: Revenue up 17.2%, PBT up 25% & basic eps up by 25%. I do rate OTB and they have done well for me and I rather expect they will continue to deliver. My only real criticism is one directed at myself as unfortunately, I dithered little too long back in the Autumn of 2016 before buying into OTB after having a good look at both the numbers and the quality of the product on offer on their website. I like the business and will continue to hold. Glad I Am Not There (GINT): well so as not to be overly modest, how about a place where I was, D4t4; can’t get them all right but what I can do is mitigate risk and sell a large percentage of my holding. I am afraid one of the inherent risks of investing in small cap companies is often the visibility of earnings. Note, I am not condemning D4t4 but simply limiting my potential risk exposure. No football travel for me this weekend as the dreaded BBC have switched the Hatters game away to Gateshead in the FA Cup to a Sunday 2 pm kick-off and logistics just prohibit that one for me. In truth, I am a southern softie these days despite my folks hailing from Wallsend in the frozen north. Whatever you are doing, have a great weekend. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed