|

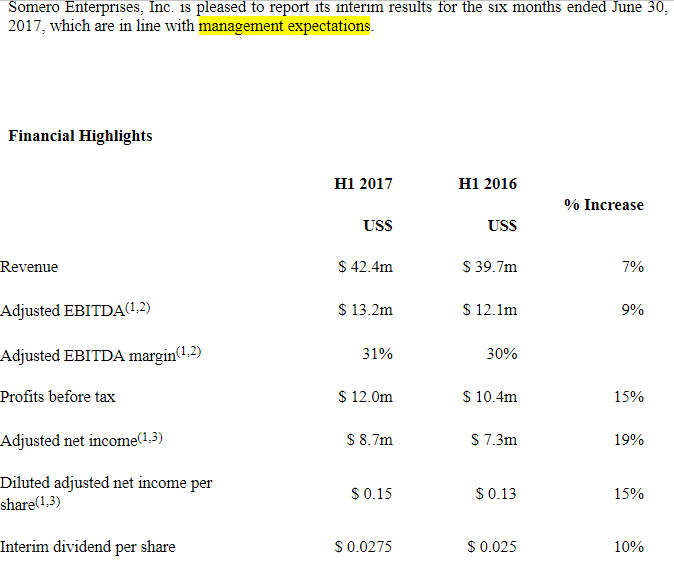

Week 9 of The Voyager RNS Log: Week Commencing 03/09/2017 Firstly a bit of sampling the product from Cake at the Lincoln Patisserie Valerie: I dropped in ahead of the Hatters game with Lincoln City and as I detest cakes as such we decided to go for Eggs Royale & Eggs Benedict: the food was good & also the coffee was good but the establishment looked a little tired to be honest and maybe a tad on the expensive side. The city of Lincoln around the Cathedral was buzzing with tourists but sadly not this branch of Patisserie Valerie; lots of unoccupied tables. It did concern me a touch when I also noticed that a queue was forming from people actually trying to get into a local patisserie/coffee shop. Then pre-match I met up with some friends and their partners for a couple of pre-match beers and the discussion got around to my visit to Patisserie Valerie. The conclusion based on their visits in other towns was that the offerings were priced a touch high for acceptable quality. After a few days consideration, on Wednesday morning I jettisoned my holding in CAKE for a total return of around 20%: live market research at its best! Note: see my notes on Fulham Shore. Monday 04/09/2017: Bioventix: BVXP: Market Cap £130m: RNS Trading Update: and what a splendidly boring update it was: Trading Update Bioventix plc (BVXP), a UK company specialising in the development and commercial supply of high-affinity monoclonal antibodies for application in clinical diagnostics, announces a trading update. The Board is pleased to report that revenues for the financial year ended 30 June 2017 are expected to be marginally in excess of £7M (2015/16: £5.5M). Since the cost-base of the Company continues to follow a similar shallow trajectory as in previous years, both revenues and profits before tax are expected to be ahead of market expectations for the year ended 30 June 2017. Now I say boring as the seductive words “ahead of market expectations” appear so often in BVXP trading updates. I have quite a long relationship with BVXP going back to 2014 and have added on a few occasions since my 700p purchase three years ago: in fact, looking at my records, the last top up was at around 1900p at the end of July. BVXP is now one of my top 5 holdings in terms of portfolio value. Really what a lovely solid business this is with a relatively low-cost base and totally superb ROCE & CROCI. My View: This is a total gem of a company, in fact, it’s the type of company that you so rarely come across: I intend to continue to hold and will consider further top ups in the future. Tuesday 05/09/2017: IQE: Market Cap £240m: Interim results: A lot of punters and indeed some investors had great hopes that these results would maybe contain the Apple word; hardly a sound reason for investing; best stick to the transformational nature of the business in my opinion. Possibly the numbers quoted in the interims are not as key as the rather wordy commentary which is where I pitch my attention: Dr Drew Nelson, IQE Chief Executive, said: "The compound semiconductor industry is moving through an inflection point. Many of the key innovations that are taking place in the technology world would not be possible without the advanced properties of compound semiconductor materials. Indeed, compound semiconductors are the fundamental enabler of innovations such as 3D sensing, biometric sensors, electric and autonomous vehicles, high speed wireless and optical communications, and advanced manufacturing. "IQE has developed an unparalleled breath (SW, I think they meant breadth) of materials IP, which position it to prosper from the inflection that is taking place in our industry. Our broad portfolio of IP is a powerful competitive advantage which is enabling us to differentiate ourselves in the marketplace. The strength of our IP has enabled us to broaden our direct engagement with OEMs from single points of engagement a few years ago, to multiple programmes enabling a number of next generation mass market technologies. "IQE's outlook has never looked better. The broad range of customer engagements across multiple technologies and multiple end markets, provide a clear path to increase revenue diversity and accelerate growth over the coming months and years ahead. The breadth and depth of customer engagement underpins the Board's confidence in approving the capacity expansion plan, which provides a flexible and cost effective route to significantly scaling up in our business over the next few years" My View: I don’t see IQE as a punt and maybe that’s because after such a great few months the shares will stop their rise and consolidate particularly as the punters get bored. With many shares, investment is a long haul game and I see this with IQE. I would suggest that it will go on over the 1-3 years to be a fairly exciting growth business and maybe fall to a predator as others have done in the area of the market. Initially, after these results, the shares lurched down into the low 120’s as those with great expectations and little patience bailed out but then bounced. I will be patient and happily, as I am well into profit, continue to hold: maybe the punters have temporarily left and the investors remain? Wednesday 06/09/2017: Somero: SOM: Market Cap £160m: Interim Results:  My View: although I have had a great relationship, but not love, with this stock since the early days of 2014 and greatly respect the SOM management, three things continue to make me feel that the superb share price rise over the last three years is just slowing down a touch: The stock is simply due to its sector, cyclical in nature. Although undoubtedly a high quality business it’s moat is really built on excellent customer service; the technology is not patented and an abundance of copies are available in China. The hoped for market penetration in China has not materialised. As mentioned in an earlier RNS log, I still retain a reasonable holding in SOM but had previously decided to take some money off the table at just over 300p. A lovely company but in my opinion during the summer it was, time for me to bank some substantial profits and reduce my holding. I still maintain a holding in the quality business. Wednesday 06/09/2017: Fulham Shore: FUL: AGM & Trading Update The Update Reads: We are currently building two more Franco Manca pizzeria, in London and in Bristol, which are due to open later this autumn. The Group continues to anticipate opening 15 new restaurants in the current financial year, in line with expectations (10 have been opened so far, the latest two being Franca Manca Oxford and The Real Greek Dulwich Village). However, given an increased availability of sites for sale due to the well-publicised pressures on other restaurant operators, we have decided to review our opening pipeline and to seek to improve terms with landlords of new sites we had already identified. This may delay some of our openings to later in this financial year. In March 2017, the Company announced that it was reviewing the progress of its third business, a single franchise of the Bukowski Grill. In order to simplify operations and focus on the Group's core brands, Fulham Shore has taken the decision to sell its Bukowski franchise and site in D'Arblay Street, Soho. A further update will be announced in due course. Current trading Despite hitting our Group targets for the first quarter of this financial year, during the holiday season in July and August the Group has seen a slowdown in trade, primarily from our restaurants in London suburbs. We believe this is a sector-wide trading pattern and not unique to our brands. In addition to this slowdown in revenue growth, as previously indicated, the Group is experiencing a higher fixed cost element to support its increased level of operations, especially in The Real Greek. As a result of these two factors, the Board expects that, while Headline EBITDA (as defined in the Company's accounts) for FY18 will be significantly higher than that achieved in FY17, it is likely to be less than current market expectations. My View: lovely business in terms of product, tried it myself, but it’s in a very crowded market place and despite its differential, it has not been able to withstand the overall pressures felt by the restaurant sector in recent months. In common with my usual approach to a profits warning this stock was sold by 08:10. The original tiny purchase (much less than 0.5% of folio) I made in FUL was always going to be a touch of a risk and really demanded continued roll out and increasing returns. As the company has hit a bit of a bump in the road, as shown by the curtailed expansion programme and profits warning, the action for me was to sell at the opening bell. I appreciate that after this RNS some directors bought what on the face of it seems like substantial numbers of shares. However, they held such a vast number of shares already; it was like taking a £5 note from a cash machine to top up your wallet already containing £2000 in notes if you get my drift. Wednesday 06/09/2017: Severfield: SFR: Market Cap £204m: AGM Trading Update Current trading and outlook The Group's trading performance and financial position remains in line with management expectations and the outlook for the year ending 31 March 2018 remains unchanged. As a result of the current phasing of contract works, the results for the full year are expected to be more first half weighted than in the prior year. My View: The wording of the trading update heavily suggests to me that the contract income & profits are now slowing down after that very rosy place SFR enjoyed over the past 12 months. On 25/11/2016 SFR in an RNS declared that the company’s order book was trading ahead of expectations. On Wednesday 06/09/2017 the TU tells us that the results are to be more weighted to H1 than H2. The implication is that in previous years H2 was greater than H1 so do I smell a “things are slowing down guys” message. So, it’s straight out with the fag packet calculation: I have not smoked for over 30 years but affectionately hold on to that fag packet term as most of my bookies odds on the gee-gees were calculated in that way. The H1 & H2 over the last couple of years looks like: Rev PBT Ratio (H2-H1)/H1 H1 2005 97.4 3.0 H2 2015 201.5 8.3 1.77 H1 2016 117.1 4.8 H2 2016 239.4 13.2 1.75 H1 2017 118.2 8.1 H2 2017 262.2 19.8 1.44 For 2018 > 1.O?? As suggested by latest RNS: H1 weighted more than H2 My early conclusion was that revenue and PBT have now peaked and are indeed slowing down: just my take on the numbers but that’s what investment is about, opinions. I sold very close to 08:10 hrs this morning: still a good company but the original attraction has now diminished. Wednesday 06/09/2017: ULS Technology: ULS Market Cap£77m: New Conveyancing Service: ULS Technology plc (AIM:ULS), the provider of online B2B platforms for the UK conveyancing and financial intermediary markets, announces the launch of a new conveyancing service developed for the mortgage lender Magellan Homeloans ("Magellan"). My View: I purchased ULS back in April 2017 after an encouraging trading update and to be honest it was never more than a momentum play and although it has served me well over this 6 month period I was happy to take my 15% profit and move on. As often is the case with these small cap AIM stocks, the sale had to be done in a couple of chunks in order to get a “non-blind” price that I felt comfortable with. Thursday 07/09/2017: Dart Group: DTG: Market Cap £765m AGM Trading Update: Annual General Meeting Statement At the Company's Annual General Meeting later today, Philip Meeson, Executive Chairman, will make the following statement: "The satisfactory start to the financial year as reported in our Preliminary Results Statement of 13 July 2017 has continued, with Leisure Travel bookings growing in line with our 41% summer 2017 seat capacity increase. Demand for our higher margin package holiday products remains strong and holiday customer numbers as a proportion of total departing customers have increased slightly. It is particularly encouraging to report that our new London Stansted and Birmingham Airport operating bases are already proving popular, with over 1.3m passengers booked to fly with Jet2.com this summer, of which close to 50% have chosen a package holiday with Jet2holidays. Continued progress is being made at Fowler Welch, our Distribution & Logistics business. Despite our airline ticket yields being lower than those achieved in summer 2016, overall the Board expects the Group to meet current market expectations of underlying profit before taxation for the year ending 31 March 2018 and will provide a further trading update on publication of its interim results on 16 November 2017." My View: this is an old favourite and one that I have written about on a number of occasions and a fine example of “maybe you have not missed the boat”; well plane in this case! I honestly thought that this one had got away from me a few years ago when the price hit 200p but it has prospered for me very nicely as the company has grown. Today’s “meet expectations” update looks fine to me although when I read the RNS on the iPhone whilst sitting in a humid pool changing room, I did wonder if the market would go negative on the lower ticket yield line. I will continue to hold. Thursday 07/09/2017: Frontier Dev: FDEV:Market Cap £420m: Final Results This was a new purchase for me this week and comes into my special situations category: I have already benefited in this area with KWS and so felt quite comfortable in buying into FDEV. Anyway, the RNS reads very well and below I have included the rather meteoric financial numbers:  What a lovely set of results they are but why include the * note to explain EBITDA? The outlook, I have included the full text as it’s rather exciting and worth a read, goes on to say: Current Trading and Outlook The Board have been encouraged by trading since the year end (31 May 2017). The number of players of Frontier's games continues to grow. In August 2017, Planet Coaster, which launched in November 2016, passed 1 million cumulative franchise units, and Elite Dangerous, which launched in December 2014, exceeded 2.75 million franchise units. We have further expanded the addressable audience for Elite Dangerous by launching on PlayStation 4 in June 2017. During the summer Planet Coaster and Elite Dangerous participated in successful price promotions on our major distribution channels with the Steam & Xbox Summer Sale events. These events were in turn supported by major updates for each game as we followed our strategy of continuing to further enhance the experiences the delivery. We launched our first in-game Paid Downloadable Content (PDLC) for Planet Coaster in July 2017, and announced that Elite Dangerous 2.4 'The Return' will be released in September 2017 which supports the on-going story arc related to Thargoids, the franchise's first alien species. In August 2017 we announced that our third franchise, Jurassic World Evolution, will launch in summer 2018 on PC, PlayStation 4 and Xbox One simultaneously. In 2015, Universal Pictures' Jurassic World became one of the biggest blockbusters in cinema history, grossing more than $1.67 billion at the global box office on its way to becoming the third-highest-grossing film of all time. Jurassic World Evolution will launch in the year that Universal Pictures' celebrates the 25th anniversary of the original Jurassic Park film, and the next chapter of the franchise Jurassic World: Fallen Kingdom will be in theatres June 2018. We anticipate that the next step-up in our financial performance will be delivered by the launch of Jurassic World Evolution in summer 2018. The Board currently expect that the majority of initial revenues from this new franchise will fall into the financial year ending 31 May 2019, as the Jurassic World: Fallen Kingdom movie is released in June 2018. The Board therefore anticipates that trading in the current financial year, the twelve months ending 31 May 2018, will principally be based on sales from the Elite Dangerous and Planet Coaster franchises. The Board is excited about the growth opportunities ahead in the coming years, as existing franchises continue to be strengthened and new franchises are developed and launched. Frontier is developing, evolving and investing in our people, organisational structure and facilities to effectively create, develop, market and sell even more distinct franchises aimed at different audience segments to achieve the Company's ambition to create a self-publishing multi-franchise success story. My View: personally I simply can’t stand video games or anything similar: stick cricket is about my limit! However, you don’t have to like the products to invest in something: I have no real need for laser flat concrete (SOM) but the company is attractive. This is what I classify in my in my terms as a special situation with the potential for exciting growth over the next few years: yes, it has its associated risks of fashion and competition but for now its an interesting addition to the portfolio. Friday 08/09/2017: No RNSs for companies within Portfolio However, I do note another profits warning from SafeStyle: SFE. I have never held the shares but did write a cautionary note about them being a householder discretionary purchase in the RNS Log of 21/072017 when they first warned on profits. Probably a decent company but you do need that element of housholder/consumer confidence and spare dosh so in my view, not one for now. RNSs for a couple of shares I held relatively recently and took profits. Firstly G4M which had become rather overheated for my taste and I sold at 800p in early June to take a very, very healthy almost silly profit. Anyway, they issued a trading update on 05/09/2017. Myself, I just felt the share price had got somewhat ahead of itself but nevertheless have kept an eye on the shares since as I am keen to see how sales are developing in Europe & the rest of the world as the UK stuff seemed to be slowing down a tad. Today’s update shows that the UK has a sales increase of 31% (is that bad?) compared to the same period in 2106 and that Europe & Rest of the World (ROW) has shot up by some 70%. I would suggest that in a year’s time that Europe and ROW will be in line or ahead of UK sales. So my feelings are that I will keep a close eye on this one and definitely be looking to buy back in on a pull back. Secondly, my old friend Cambria Automobiles: CAMB issued a trading update on Tuesday 05/09/2017 which was a touch cautious with sales of new cars under some pressure due to consumer confidence and the weak pound affecting imported cars. Now I should say that in my view Camb are a well managed class act albeit in a very low margin business. The nature of their business is cyclical and linked very much to consumer confidence and that confidence has been in something of a decline since the shares hit around 90p some 18 months ago. CAMB have been very kind to me having sold the stock back in January 2016 and like any quality business I owned stock in, I keep a watchful eye on their performance. I am sure I will buy back in sometime but I don’t feel that time is here just yet. Glad I’m Not There (a sort of reverse take on the old Judith Chalmers holiday programme briefly mentioning a dog of the week that thankfully I don’t own). Well one I was there this week although an overall decent company with good management is Fulham Shore; see RNS notes above. As I say just about every week in this Voyager RNS Log, your next profits warning may be just around the corner; simply part of the life of a private investor no matter how clever or careful you try to be. You can mitigate the risk of profits warning by going for what I perceive as quality but even then, you will get bitten by a PW now and again. The trick is to act according to your plan, whatever that may be, and don’t beat yourself up; accept that PWs happen! Take a look at the Telegraph article on Neil Woodford’s apology to investors after his “fortnight from hell”: http://www.telegraph.co.uk/business/2017/09/06/neil-woodford-right-criticised-sorry/?WT.mc_id=tmg_share_tw Maybe the nomination for the Glad I’m Not There award this week should be Interquest Q: ITQ, who have been right royally shafted their faithful and long suffering shareholders. On Wednesday they announced that they will effectively be suspended from AIM on 09/09/2017 following their dismissal of their nominated adviser and broker Panmure Gordon. When will they return? So, the long suffering shareholders saw the stock fall by 22% on the day of the RNS. In fact the shares have fallen 67% in the last 15 months. On the fact of it you may get the impression that this is simply terrible and incompetent management of the business: indeed it is but sadly it’s far worse that that. It appears that the owner & some fellow directors, who failed in an attempt to buyout the company some time ago, have rather engineered this situation that will lead to the companies expulsion from AIM; I wonder who will be the beneficiary of that expulsion, certainly not the shareholders. It is the sort of behaviour that gets AIM an often unjustified bad reputation. Yes, there are some dodgy businesses listed on AIM & I have written about some of them recently. However, let’s not lose sight of the fact that AIM contains some very wonderful well managed companies and a significant percentage of my capital is invested in them. I did actually write a blog article “Surviving On The Hostile Planet AIM” back in back in August 2016: http://stockwhittler.weebly.com/blog/archives/08-2016 Over the next couple of weeks the RNS log may possibly take a bit of a breather as I am taking what I feel is a well earned break for a few days in Kyrenia; I always manage a break around this time of year. I will try to get a Voyager RNS Log out next Thursday and then maybe some awfully brief ramblings the following week with a return to normality at the end of the month. Next week: the only planned RNS I can see scheduled within the folio is GFRD finals on 13/09/2017. However, there may be further news on RGB takeover and who knows what trading updates may arrive: as ever, always remember that the next profits warning may just be around the corner. Have a good weekend and as ever, happy investing.

1 Comment

Edwin

9/11/2017 01:00:29 pm

Great update and insight. You may be right about CAKE. I'm not convinced about subjective thoughts overriding accounts though. Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed