|

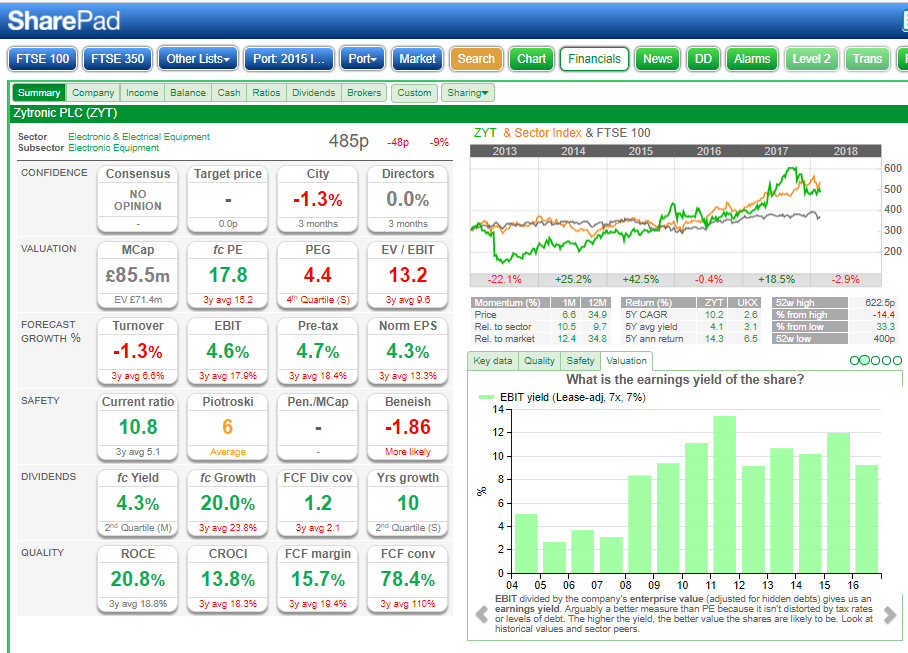

Voyager RNS Log WC 18/02/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Monday 19/02/2018: Dart Group: DTG: Mkt Cap £964m: RNS Trading Update: Current Financial Year (FY18) Due to the continued success of our growing Leisure Travel business and a more normalised pricing environment after the heavy discounting in the market over the past year, the Board now expects Group underlying profit before taxation([1]) for the year ending 31 March 2018 to be materially ahead of current market expectations. The Group will publish its Preliminary Results for the year ending 31 March 2018 on 12 July 2018. Next Financial Year (FY19) The Group continues to develop and build its businesses. Looking ahead to the year ending 31 March 2019, forward bookings in our Leisure Travel business for summer 2018 are presently satisfactory. We also remain encouraged by the performance of our two new operating bases at London Stansted and Birmingham airports. Our Distribution & Logistics business, Fowler Welch, continues to focus on growing its revenue pipeline and developing existing and new business opportunities. It is still early in the leisure travel booking cycle and we remain cautious on pricing. However, given the satisfactory forward bookings and the execution of our growth strategy, the Board currently expects the Group's trading performance for the year ending 31 March 2019 to be broadly in line with the current financial year. My View: well nothing to dislike there and I would say that materially means in the order of maybe as much as 10% higher than market expectations. Some investors may be a touch phased by the comments looking into FY commencing April 2018 and whilst the forward booking process does offer some visibility, we have yet to enter Q1 of 2018/19 as yet. Therefore to my mind, the comments are absolutely fine and I am pleased to continue my association with DTG that goes back to about the 200p level a few years ago: I will continue to hold. Tuesday 20/02/2018: Bodycote: BOY: Mkt Cap £1.8b: RNS Re Long Term Safran Agreement BODYCOTE ENTERS INTO AGREEMENT WITH SAFRAN LONG-TERM CONTRACT FOR MANUFACTURING SERVICES Bodycote, the world's largest provider of heat treatment and specialist thermal processing services, today announced that the company has entered into a long-term agreement with Safran, an international high-technology group and tier-1 supplier of systems and equipment in the Aerospace market. Bodycote's global network will support the agreement, operating initially from strategically located facilities in France and Belgium. Under the agreement, Bodycote will provide manufacturing services which include thermal spray coatings, electron beam welding, hot isostatic pressing (HIP), heat treatment and others to Safran companies and their key strategic first-tier suppliers. Bodycote's processes and technologies are used to prolong the working life of critical components and provide in-service protection from factors such as abrasion, temperature and wear. The agreement ensures that manufacturing requirements will be met by a quality-focused supplier to support the growth in Safran's civil aerospace programs. These programs include but are not limited to CFM LEAP for Safran Aircraft Engines, helicopter engine programs for Safran Helicopter Engines and landing gear systems for Safran Landing Systems. Bodycote's international network of thermal processing and other specialist services offers security and mitigates risk in the supply chain. My View: whilst accepting that it’s not the sort of RNS that can offer any quantification in terms of revenues or profit, it’s nevertheless an encouraging announcement from BOY. I like Bodycote and have considered them to be a quality outfit for many years: decent returns of capital, decent FCF, no debt and a quality supplier. Very boring and steady but that’s nice in my opinion, who needs excitement! Happy to continue to hold. Wednesday 21/02/2018 No RNS Relevant to Portfolio Thursday 22/02/2018: Zytronic: ZYT: Mkt Cap £85m: RNS AGM Trading Update: Further to the outlook statement given in the preliminary results announcement, current revenues and profits over the first four months of this financial year remain broadly in line with the equivalent period last year. " The Outlook t the time of the interims on 12/12/2017 said: The current year has started with orders, revenues and trading along similar levels to that of the prior year, which, together with our strong balance sheet and cash generation, provides a sound base for further growth in dividends and shareholder value. The focus on growth this year will be from expansion in local sales representation in the USA and the Far East, and we shall keep shareholders updated on the progress, and any material developments, over the course of the year. My View: It was rather fond “thank you and goodbye for now” departure from ZYT at the opening bell as at best it looks like the progress in revenues and profits have plateaued for ZYT and the stock looks to be ex-growth. Note that ZYT was one of my major holdings up to October 2017 but the price seemed to really rise overly much in my view reflecting over expectation amongst investors. When I initially bought ZYT it could rightly be described as a high-quality growth business. Now whilst I still see ZYT as a quality business it is now appearing to have lost that growth label and whilst it had bags of cash on the balance sheet it’s valuation now looks a little toppy for a small cap dividend paying stock that maybe carries too much risk at the current time, especially as a very significant percentage of its revenues, come from four main customers. So, at the opening bell, I sold my last batch having done some heavy slicing in October 17. ZYT has done very well for me since my original purchase a few year ago and I was happy to both top up along the way and also continually reinvest my dividends but the statement “current revenues and profits over the first four months of this financial year remain broadly in line with the equivalent period last year” is in my opinion a mild profits warning. Lovely company and I may well return someday but for now, it’s protection of profits and capital. Coincidentally, taking the “at the opening bell” sale price and the XD to come matched the previous day’s close price; the benefits of early trading following a somewhat disappointing RNS! Note, take a look at the data below from the excellent SharePad and whilst there is still a lot to like, together with recent RNS announcements it suggests to me that growth may have stalled.  Thursday 22/02/2018: D4t4: Mkt Cap £51m: RNS Regarding New Contract Wins D4t4 Solutions Plc (AIM: D4T4), the AIM-listed data solutions provider, is pleased to report a number of new contract wins in key vertical sectors for its Data Management and Data Collection business areas. Following the release of D4t4's half year results to 30 September 2017 and the Company's contract wins announcement on 27 December 2017, the Company has recently converted a number of further significant opportunities from its strong pipeline of potential business. My View: At the end of November 2017, I sold the majority, about 80%, of my D4t4. I just did not like the comment in the half year results with a real bias to H2 with H1 being disappointing. I felt there just seemed to be too much uncertainty in the company and maybe I had got this one wrong so for me it was best to take a manageable loss and preserve capital. However, I still retain a fairly small position with D4t4 and the news flow couple with director buying is enough to encourage me to continue to hold my remaining shares. Within this RNS there is no financial quantification of what the contracts mean to H2, remember H1 was poor with "better things to come in H2" and I find that somewhat disappointing. To my mind after a rather poor set of interims back in November 2017, they really should have taken the opportunity to update investors on H2 expectations. Friday 23/02/2018 No Significant RNS for Portfolio Shares.  Glad I An Not There: sadly this weeks award goes to an absolute beacon of reliability from my days as a little lad in short trousers. At that time the AA was an absolute pillar of service & reliability, I used to dream of becoming an "AA motorcycle hero when I group up”. Well just like another fond childhood memory, Hornby trains, how things change. In June 2014 the AA was the subject of an IPO and had a very decent start on the markets with its share price appreciating by about 70% in the subsequent year. Despite good returns on capital, I could never be persuaded to invest simply to that enormous red flag of massive debt; to my sceptical mind, it was a flotation destined to make others rich but not the shareholders in the long run. The debt pile was always totally horrid whichever way you look at it: Net Debt to EBITDA over 7, debt to EV of over 75% which goes up to 85% when you take into account the large pension deficit. At the time of writing these notes and taking into account the reduced market cap following the profits warning, the debt to EV has gone to an astonishing 83%. On 21/02/2018 the AA released an RNS Strategy Review which was in effect a profits warning and a fairly massive reduction in the dividend. In itself the dividend cut is understandable but in terms of the overall debt, a mere drop in the ocean. I have no idea if the AA will survive without raising capital but overall, it’s not a place I would choose to be. Having said that, I should qualify my views on debt by saying that an easily manageable debt situation is fine but to my mind, the AA debt is simply crippling. Will AA service, will Hornby survive or will they follow the fate of that other iconic memory for my childhood, Jamboree Bags! I also not that the unfortunate Neil Woodford is a major shareholder in AA. Now, without doubt, Woodford is a decent investor but like all investors, continued success is simply not guaranteed and when one of his shares runs into problems it's simply difficult to impossible for him to discharge his holding in the way that the average private investor may do. Just one of the advantages us private investors have over the big boys. Incidentally, anybody who wants to do a follow up by looking in the rearview mirror with TalkTalk and my approach to getting out on less than good news may find the share price graph of TalkTalk interesting in reaction to poor news: “profits weighted towards H2”, “Cyber attack” etc offering plenty of opportunities to sell since mid 2015 and avoid the stepwise car crash of the share price. It was stock I held for quite a while and whilst selling a little early late in 2014, took some very decent profits. Had I been a holder in mid-2015, I would have long since fled. Why did I sell when I did? Well as a customer, when things went wrong I had really dreadfully frustrating service from the overseas “I must go through my checklist” customer service desk; as an investor the dropping down in returns on capital; overall losing conviction in the business. Protection of capital is paramount; if in doubt, get out “We can't control the winds - but we can adjust our sails”.  Finally, for this week, you may find of interest the following link to an article in the Guardian about restaurants and the crowded marketplace: www.theguardian.com/lifeandstyle/2018/feb/22/casual-dining-crunch-jamies-italian-strada-byron-struggling Personally, I have totally withdrawn from investing in any food or pub chains several months ago. They have been decent enough to me in the past but we are at a time of rising basic wages for staff (a good thing for the low paid staff), incredibly tight margins and near saturation of the marketplace. Maybe one to return to another day but for now, they won't enter my portfolio. Whatever you are doing this weekend, try to stay warm as we have it appears a very cold front coming in from the East; oh how I look forward to sitting on my cold plastic seat at Kenilworth Road on Saturday. Happy investing.

0 Comments

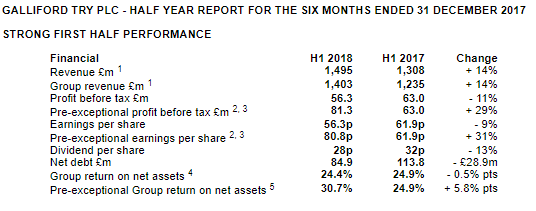

Voyager RNS Log WC 11/02/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Well, the markets have certainly had their touch of volatility over this last couple of weeks as we have gone through what appears to be an expected correction. I often feel that the random movement of Mr Market is rather like a very drunk man trying to make his way home. He lurches from side to side, sometimes he even goes backwards or dangerously drifts into the road but despite all of these random lurches, he eventually goes in the right direction. Anyway, enough of this and onto this weeks review: Monday 12/02/2017: XP Power: XPP: Mkt Cap: £608m: RNS Regarding US Tax Changes: The recently enacted Tax Cuts and Jobs Act in the United States is expected (subject to audit) to result in a non-cash tax credit in 2017 relating to the revaluation of US deferred tax balances of circa GBP5.2m, based on the net deferred tax liability at the end of 2017. This credit is as a result of the reduction in the federal tax rate from 35% to 21% and will be excluded from adjusted earnings. The Company has also received notice that claims relating to the Development and Expansion Incentive (DEI) in Singapore have been accepted by the Inland Revenue Authority of Singapore resulting in a circa GBP1.3m refund of Corporation Tax paid in 2015 and 2016. This will also be excluded from adjusted earnings. We will continue to work through the full impact of these changes but expect the Company's future effective adjusted tax rate to be in the range 15-17% depending on regional mix of profits. My View: I have been a fan of XPP for quite some time and bought my first batch in early 2016 and have enjoyed a superb share price ride since that time. The shares got a touch of a boost from this tax gift on an RNS with the US & Singapore at a combined value of £6.5m. Now whilst the company is still evaluating the effects of this good fortune, they state that the Company's future effective adjusted tax rate to be in the range 15-17%, which to me can only be good news and may just lift some brokers forecasts a touch. As I say, nice company and I will continue to hold. Tuesday 13/02/2018: RWS Holdings: RWS: Mkt Cap £1.2b: RNS AGN & Trading Update: The current financial year has started well as we continue to build on this record performance, with our Patent Translation & Filing, newly formed Life Sciences, and Information divisions all contributing in line with our expectations. "In addition, RWS acquired Moravia on 3 November 2017 for a cash consideration of US$320 million. Moravia is one of the leading providers of technology enabled localisation services to some of the largest technology companies in the world. Its acquisition enhances RWS' global presence, adding operations in the Czech Republic, USA, Japan, China, Argentina, Hungary and Ireland; provides further geographic and currency diversification; and adds an additional profitable, cash generative division of scale to the Group. Current Trading and Outlook The Group has performed in line with the Board's expectations in the first quarter of the current financial year. Our focus now is upon the integration of Moravia together with the successful exploitation of the opportunities provided by our recent acquisitions. "Notwithstanding US exchange rate headwinds, the Board is confident of further substantial progress in 2018 as RWS consolidates its global leading positions in its chosen sectors. My View: well that’s a sound enough trading update for the first quarter of RWS’s financial year & let’s remember this is Q1 so a long way to go in the current FY. I guess some punters will be continually expecting to see “ahead of” trading update but in real life, this does not happen so expect there could be a minor sell by punters which may create another buying opportunity. Note I recently topped up at an attractive price on one of the dips early last week as the market had a little shakedown. In my opinion, a quality business that I am happy to continue to hold for a long time and top up when decent opportunities are presented. Wednesday 14/02/2018: Galliford Try: GFRD: Mkt Cap: £800m: RNS Half Year Report 14 FEBRUARY 2018 GALLIFORD TRY PLC - HALF YEAR REPORT FOR THE SIX MONTHS ENDED 31 DECEMBER 2017  INTERIM DIVIDEND The Group has brought forward plans to increase dividend cover to 2.0x pre-exceptional earnings. Reflecting this, and the Group's strong underlying performance during the half year to 31 December 2017, the directors have declared an interim dividend of 28.0p per share (H1 2017: 32.0p) which will be paid on 6 April 2018 to shareholders on the register at close of business on 16 March 2018. We then move on to the CLLN legacy: Financial position Galliford Try continues to operate well within its financial covenants. However, the compulsory liquidation of Carillion plc ("Carillion") has placed additional financial obligations on the Group arising principally from the joint venture with Carillion and Balfour Beatty plc on the Aberdeen Western Peripheral Route contract ("AWPR"). The over-run costs on AWPR, compounded by the compulsory liquidation of Carillion have increased the Group's total cash commitments on the project by in excess of £150m. The Group continues to make good progress in resolving both AWPR, the construction of which is expected to complete during summer 2018, and other legacy contracts. The Group no longer undertakes fixed price, all risk major projects of this nature, and has improved its tendering and project selection processes. The Group has sufficient financial resources to meet its obligations, including the estimated impact of Carillion's liquidation. However, this would involve diverting capital away from the Linden Homes and Partnerships & Regeneration businesses, thereby reducing their ability to capitalise on the material growth opportunities these businesses would otherwise be well positioned to exploit. Capital Raising Galliford Try therefore intends to raise £150m of new equity capital in the coming weeks to strengthen further the Group's balance sheet and ensure that the Group's businesses can continue to pursue their respective growth opportunities that were set out in the "Strategy to 2021" announced in February 2017 (the "2021 Strategy"). My View: Looking at the numbers you could argue that they look reasonable but then we come to the sting; the poisoned challis gifted by the CLLN joint venture which has necessitated a capital raising and inevitable dilution of about 15-20% for shareholders. We also have a dividend cut which is to my mind, not a particularly big issue compared to the CLLN legacy. At the time of writing these notes, the shares are some 50% down from their February to March price range. All of those who employed a trailing stop loss as an alarm call may well have got out as I did on the day of the CLLN news. I thought that was a sensible move selling at 1250p and it preserved my capital from a considerable further fall. However, I got my reentry into a fairly smallish position at 980 wrong last week as I incorrectly judged that the CLLN was built into the share price despite my reasoning of caution with my original sale (see Voyager RNS WC 21/1/18). Never mind, an unfortunately timed purchase but thankfully only a small position; it happens, don’t waste time justifying a wrong one, simply sell at the bell and move on. Had the RNSs been more positive, I would have considered adding more but simply too much risk for now in my opinion. I know some investors will think deeply and justify themselves for remaining faithful from that good 1550p share price 10-11 months ago and I accept that investment styles differ. However, as ever, capital preservation is paramount in my mind. Thursday 15/02/2018: NewRiver REIT: NRR: RNS Acquisition of two retail parks for GBP26.5 million representing a blended yield of 9% NewRiver is pleased to announce that it has completed the acquisition of two retail parks for a combined consideration of GBP26.5 million, representing an initial yield of 8.9% and a capital value of just GBP141 per sq ft. Both retail parks have good occupier demand and present NewRiver, as a specialist retail asset manager, with the opportunity to add value through a variety of identified active asset management initiatives. The Rishworth Centre and Railway Street Retail Park, Dewsbury The Valegate Retail Park, Cardiff Allan Lockhart, Property Director commented: "These acquisitions are in line with our strategy of acquiring fundamentally good quality assets with untapped enhancement opportunities which NewRiver is well placed to exploit as an active and specialist retail asset manager. We are confident of significantly improving the retailer profile and the sustainability and quality of underlying cash flows so that these assets will deliver attractive returns for our shareholders. Importantly we have retained our capital discipline on entry price, acquiring these assets at a blended yield of 9%." My View: this is one of the stocks I hold within my high yield portfolio and from what I can understand, it seems like another decent acquisition bt the competent management team at NRR. Just checking my records and I see that I first purchased NRR quite some time ago in fact back in mid-2013; I am happy to continue to hold and reinvest the generous dividends. Friday 16/02/2018: I am afraid I have an early start and will be away from home before the RNS flow so will catch up on anything significant in next weeks Voyager. Glad I Am Not There: well this week lets have a look at UP Global Sourcing Holdings plc, UPGS, an IPO at the start of March 2017 & it appears a top tip from a subscription service tipsheet or at least so I am told. Now I should say that I simply do not do IPOs: been there, done that, got the T-Shirt or correctly got out with what’s left of the T-Shirt. Absolutely years since I have done one as they are just not my style as I like proven track record companies that have been tested by the financial markets; each to their own and all that. Also, although the intention of these comments is not to knock the business concept, it’s not a business model that appeals to me. Anyway, UPGS issued a profits warning on Monday 12/02/2018 that say the shares fall by an astonishing 45% an absolute horror for investors. The horror story began to unfold last year with a first profits warning on 11/09/2017 just six months after coming to market; an absolutely horrid place for holders to be especially after such a short space of time on the market and really does question the business in total (model & management credibility). However, I digress as I just wanted to use this as a reference example to a couple of items a continually bang on about. Firstly, are experts really experts i.e. tipsters are like all of us in that they don’t get it right every time. Secondly, although you may not have got it right with your tip/purchase, the important thing for me is what action you take when bad news hits and believe me, sooner or later it will hit a stock within your portfolio. With rapid action in mind, look at the graph below and consider how investors on the day of the first profits warning back in September, may have escaped by selling at close to the opening bell maybe a 25% loss or worst case as much as a 50% loss with the share closing down at 104p having closed at 210p on the previous trading day. Well, that was bad but further procrastination over the next five months would see another 50% wiped off that already beaten up 104p. On the trading day before this Monday’s profits warning, the share price closed at 61p and on the day of the warning fell sharply to around 40p where if you were lucky, you may have been able to get. By the close, on the day of the second warning, the share price had hit 32p i.e. a 48% drop on the day. Will there be continual drift? Will investors see value in the business at these levels? I honestly don’t know the answer to either question but what I do know is that the smarter investor who exited on the day of the original profits warning on 11/09/2017 would despite the original pain, be so much better off than the investor who remained blindly loyal to their original investment decision. A lovely example of what I feel are combined capital destroyers: not acting on a profits warning and the application of wealth destroying procrastination.  This weekend I have a Hatters free as our game at Coventry has to be rescheduled due to their continued progress in the FA Cup. I may well pop on a train and go to watch Cambridge United at home and that will at least give me a good excuse to call into that wonderful backstreet pub, The Cambridge Blue with its massive range of well kept real ales.

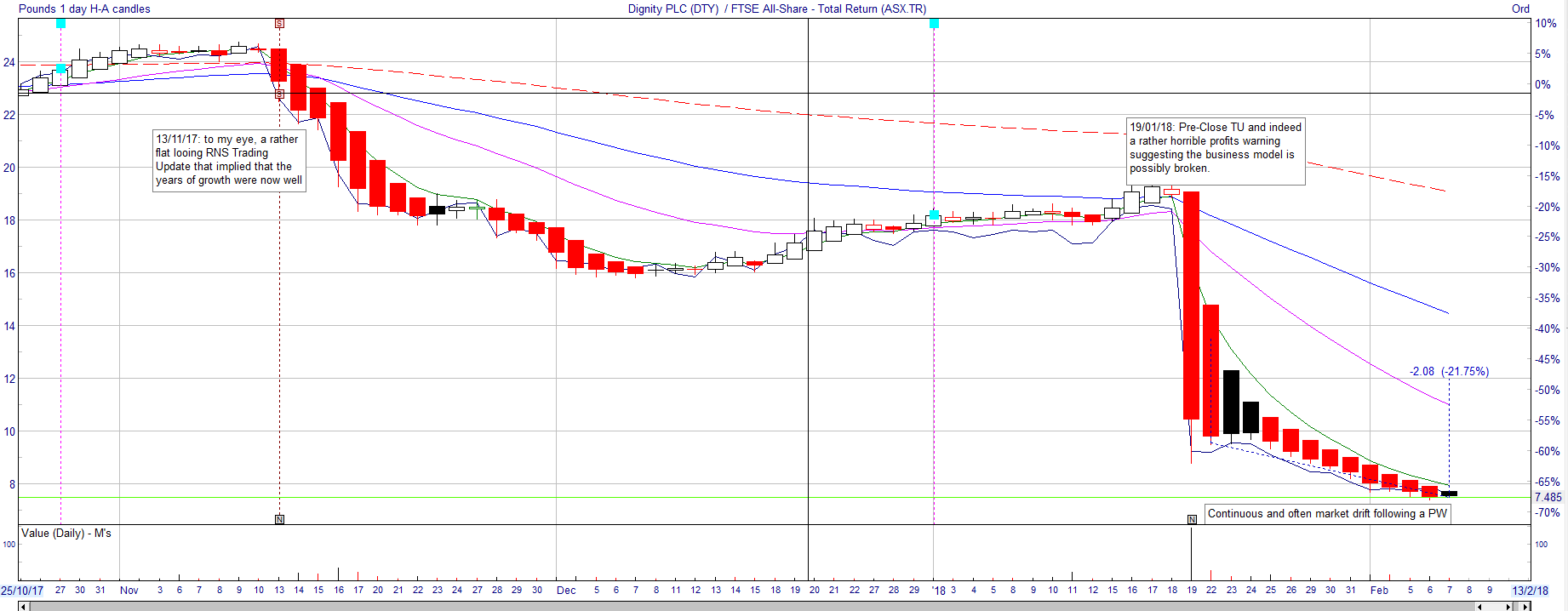

Whatever you are doing, have a good weekend and happy investing. Voyager RNS Log WC 04/02/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Oh, how I dislike February, such a dreadfully cold month; this year I just keep asking myself why have I not flown off to somewhere warmer? I have tried Oz on a couple occasions as a winter retreat but the trouble is down under that if you venture to the warmer parts such as Queensland then swimming is the sea is a definite no as something either wants to eat you or do irreparable harm to you. Yet if you head to Victoria or Southern Australia where the water is just too cold for box-jellyfish or crocodiles and certainly too cold for a southern softie like me. I shall have to have a think for winter 2019, maybe SE Asia, maybe Barbados or a bit closer to home, the Canaries. Mind you if Murder In Paradise is anything to go by, visitors drop like flies in the Carabian so who in their right mind would go there or even closer to home, be foolish enough to set foot in Midsomer. Just how would you get travel insurance for such places? Probably me just thinking a little too deeply. As I have written before on this site, I generally pay no attention to market noise and definitely don’t check price progress anything remotely like daily as I prefer to be RNS driven. However, with storm clouds forming in the USA and falling markets on Friday & Monday, I did a little trimming back on a small number of positions that had maybe become a little stretched, taking profits on FDEV and a few small company IT’s focused on Japan and the UK. Just risk mitigation on the fringes of the overall portfolio where things had become a little stretched. In this column in the past, I have mentioned that I took out all of my original costs for the purchase of KWS which due to its meteoric rise since my tranches purchased, maybe, I thought I might de-risk a little further and sell a few more? However, I then discovered that the considerable holding I have retained are all in my dealing account and not in the tax-free environment. What a wally I am, the CGT is already bulging for 2017/18 and any further sale would just add a horrible 20% gift to that gruesome chancellor bloke, yes the very one who scuppered our £5k tax-free income on share dividends. Looks like I will become a long-term supporter of KWS and eek them away over the next couple of years; long live Mecanno and the fat-finger, or maybe more correctly her, the blind eye syndrome. Oh well, all the KWS are running for free, so who knows! Following Tuesdays sell-off that was hitting the markets worldwide, I decided to do a little shopping and repurchased some GFRD for >20% lower than I had sold in mid-January and also added to my special situations holdings in RWS as they drifted south to what looked a rather bargain price for a quality company, and also topped up on Spectra Systems who issued a couple of ahead of expectations RNSs recently. Yes, there are risks with GFRD contract implications with Carillion but with a dividend of almost 10% which subject to change, is covered by FCF, it’s worth adding to the high yield portfolio. Interestingly on Twitter this week there have been a few views expressed on the use of stop losses; some folk use them whilst some folk don’t. I guess it’s whatever you feel more comfortable with and indeed to a large extent, the quality of the company in terms of its sound accounting practices, debt, realistic market prospects and momentum. Personally, as I have said many times before, taking steps to avoid the destruction of one's capital tied up with a falling share price is simply fundamental to the way I invest. With a stop loss, for a smaller cap company, which for me is £50m to £250m, I usually start with a 20% stop loss that then trails as the SP hopefully increases and as I reach good profits, then I reduce the trigger back to say 12%. If the trigger is hit, I don’t automatically sell but seriously reappraise the investment asking myself “if I did not already own this stock, would I purchase it today with the information currently at hand”? If the answer is yes, then I continue to hold and maybe even take the opportunity to top up; if it’s no, then of course I sell. I have friends and acquaintances who have steadfastly refused to listen to the alarm bells ringing. Is it because they would still buy the share today, maybe because they are terribly loyal or could it be can’t bring themselves to so crucially admit that they got that purchase wrong. Staying with a company that has hit you for a 40% loss requires a 66% gain for break even, a 50% loss requires a 100% gain and an 80% loss a five-fold appreciation in the share price to break even. For me, the answer is easy and you can always go back in such as in the case of GFRD mentioned a couple of paragraphs above, and repurchase again and often at a better price but as ever, each to their own. Looking at the end of last week and going through this week, are we heading for a crash or simply a market correction? Well, I don’t forecast these things and in truth, the “experts” don’t either. The experts are expert only and that’s one thing is looking in the rearview mirror and telling you where you have been but don't have the slightest clue about where we are headed. Where would they be without retrospect? Although in no way a prediction, I rather suspect that the current sell-off is just a correction as markets have really got a touch ahead of themselves and so slide back; it happens and is simply part of stock market investing. Recent examples of corrections are there to see: January 2014, August 2015, January 2016 and of course Brexit. Here we have in my view just got way overstretched in terms of the likes of the Dow Jones so maybe a fall back of as much of 12-15% could happen; yet as I say, predictions hold little value. When markets get maybe a little overvalued, I start to assess each RNS even closer and gradually, if it seems the prudent thing to do, cut reduce some positions i.e. my pre Christmas reductions in ZYT, BVXP, SMWH and KWS. I still hold these stocks but have just taken out some rather decent profits. The rest of the time I tend to ride the turbulence in a slightly more buoyant de-risked boat and hopefully pick up buying opportunities from the cash pile as I see fit. I should also say that after being a freebie, or is that tightfisted, member of ShareSoc, I took out a paying membership this week. Simply can't argue with what these guys do and I am very happy to support their efforts and who knows, I may well turn up at the odd meeting or two. Blimey, I am rabbiting on a bit this week. Let’s get down to discussing any RNSs that have an impact on the portfolio: Monday 05/02/2018: No RNS of interest to the portfolio Tuesday 06/02/2018: Amino Technologies: AMO: Mkt Cap: £140m: Final Results:   Notes (1)Adjusted Gross Profit is a non-GAAP measure and is defined as gross profit before exceptional items (2)Adjusted EBITDA is a non-GAAP measure and is defined as earnings before interest, taxation, depreciation, amortisation, other operating income, exceptional items and share-based payment charges (3)Adjusted profit before tax, adjusted operating profit and adjusted earnings per share are non-GAAP measures and exclude amortisation of acquired intangibles, other operating income, exceptional items and share-based payment charges (4)Adjusted cash generated from operations excludes cash from exceptional items Keith Todd CBE, Non-Executive Chairman, said: "2017 was another year of progress for Amino with strong profit growth and cash generation. We have continued to innovate and steer through the changing customer landscape whilst building a broad product portfolio and customer proposition. Revenue for the year at GBP75.3m was broadly the same as the previous year (FY 2016: GBP75.2m). Profitability was in line with market expectations, with adjusted operating profit(1) of GBP11.1m representing a 9% increase over the prior year (FY 2016: GBP10.2m). Operating profit was 228% higher at GBP9.5m (FY 2016: GBP2.9m) as there were minimal acquisition related costs in the year. The Company's ability to generate cash remains strong with the year-end cash position ahead of market expectations at GBP13.0m (30 November 2016: GBP6.2m). We have large addressable markets and our recent investment in software, services and the emerging Android TV opportunity, coupled with a strong backlog and pipeline, supports our confidence in 2018 and beyond." Outlook Amino has made a promising start to 2018 and has a solid order book and sales pipeline visibility to the end of the year, with a return to our normal seasonality in terms of a stronger second half financial performance. With this positive momentum and clear portfolio and positioning, the Board expects the Company to deliver sustainable profitable growth in the coming year My View: the results look to be bang on target, being in line with market expectations, the dividend was raised by a nice 10% to give a handy yield of about 3.5%. Also, that dividend is amply covered by FCF. The brokers forecasts for 2018 suggest that the company should continue to grow albeit not at the stella rate that would attract the more adventurous investors. The outlook statement reads well enough to me and whilst accepting the risks associated with an AIM technology stock, I rather like the company and it has done quite well for me, I will continue to hold. Also nice to see the CFO, Mark Carlisle, dipping his hand into his pocket to buy an initial position of 5000 shares which is about time as he has been in post since August 2016. I always take notice of CFO/FD share purchases or sales. Tuesday 06/02/2018: Frontier Developments: FDEV: Mkt Cap £495m: Interims I will only cover this one very briefly as it exited the portfolio at the start of the week as I did a little derisking. FDEV was one of my special situations and did ok for me over the few months I have held the stock but with the USA having a wobble on Friday last and that continuing into the Monday, I decided that it was time to manage risk and sell as to my mind the valuation was looking very stretched with absolutely no room for disappointment. The results did not look that stunning to me with minimal increase in turnover and a gradually declining operating margin. Anybody who knows me will be aware of the disdain I have for the PE ratio but I have to admit that a projected PE of 55 is a touch stretched. Maybe I am getting overly cautious but as I am locked into Mecanno KWS for the foreseeable future for tax implications, there is only so much risk I want to carry and anyway, I can always come back at a later date. Wednesday 07/02/2018: No RNS of interest to the portfolio Thursday 08/02/2018: On The Beach: OTB: Mkt Cap £653m: RNS AGM Trading Update AGM Trading Update On the Beach Group plc (LSE: OTB.L), the UK's leading online retailer for beach holidays, today issues the following trading update for the four months to 31 January 2018, in advance of its Annual General Meeting to be held today. The international sites in Sweden and Norway have continued to show strong growth YOY and the Group will shortly launch its international proposition, http://www.ebeach, into its third market, Denmark. The Group continues to increase its investment in talent and technology while building its exclusive supply position and growing awareness across all brands. The Board believes the full benefits of these investments and the incremental marketing investment in the Sunshine.co.uk brand will continue to flow through in the remainder of this financial year. The Group will report Interim Results for the six months to 31 March 2018 on 10 May 2018. Simon Cooper, Chief Executive of On the Beach Group plc, commented: "The first four months of the new financial year has delivered another solid period of growth for the On the Beach, Sunshine and ebeach brands. Our strategy of investing in our brands, talent and technology to drive growth has delivered performance in line with the Board's expectations, with consumers attracted to our wide range of value for money beach holidays. Our third nationwide television advertising campaign started on Christmas Day and has helped drive this strong performance as our brand awareness continues to grow. The Board remains confident in the Group's outlook and will continue to evaluate opportunities to enhance its market share position." My View: I remain comfortable with OTB and appreciate the inline update which encouragingly demonstrates growth and also expansion into other countries to grab a slice of the online holiday market. A very good company in my opinion and I shall continue to hold Glad I Am Not There: well, it’s a place I was there at one time but sold out of Gattaca over 12 months ago once again to preserve capital and manage risk. Back in the late 90’s, a very experienced and well-read investor told me that if a company changes its name then that may well tell you something about the competence of the management of that company especially if that name is just plain stupid. Look at Compel back in the late 1999/2000, Norwich Union, Consignia in the mid-2000’s: now it’s not always the kiss of death and sometimes has no detrimental effect, simply a wise warning to keep a guarded eye open. So, enter Gattaca (GATC) previously known by the name of Matchtech and historically quite a decent business and one which I have pleasingly owned on a couple of occasions. Well, guys that totally ridiculous name change just did not work and as well as failing to give a reasonable account of the reasoning for that chosen name, you have managed to cock-up quite alarmingly and on Wednesday at 2:30 pm issued the following Trading Update/profits warming in an RNS: Taking a more prudent assessment of the economic outlook, we have tempered our expectations for growth in H2 and consequently, we are undertaking a review of our cost base, so as to identify savings, some of which will be achieved in H2. Notwithstanding these savings, profits before tax excluding non-recurring costs are now expected to be in the order of 15% below the Board's previous expectations. The management at Gattaca have steered the share price of the business from well over 600p in 2014 to today's price of just north of 200p; possibly Calamity may have been a better choice of name. Oh yes, the yield which could draw in the casual unsuspecting punter who fails to dig a little deeper, suggests it is now about 10% and will in my opinion, surely be severely cut as there is just not enough FCF to anywhere near cover the payment. Indeed the TU does make reference to the dividend in: In light of the revised full year expectations the Board has decided to reset the rate of dividend in order to restore a more sustainable dividend cover ratio, to enable the pay down of debt, and to reflect a more normalised yield. The Board intends to set the dividend cover at approximately 2x (2017 1x). My view is that the dividend will be reset with reference to the current valuation to be in the order of 4% which is quite a hit for current shareholders. Very glad I don’t hold any GATC and as a final thought, I really mistrust a company that chooses to issue such an announcement significantly later than 7:00 am; this one was released at 2:30 pm, simply poor in my opinion. I last purchased GATC at 322p in October 2016 and sold my holding on2/2/2017 on reading their TU that looked anything but inspiring; I simply asked my self “would I buy this share today knowing what I know now? The answer was a full and rapid NO and the stock was immediately sold, including the stock I had purchased a year or so earlier, for a total loss of around 15%. Not great but at least I was protecting my capital and this approach to capital protection is fundamental to me. Note, I applied the same logic with DTY when they issued what I perceived to be a warning bell; back in November I wrote: DTY a stock I sold at the bell on 13/11/2017 when they released a trading statement I just did not like; not a disastrous statement but nevertheless one that just did not make me feel in the slightest comfortable. I did have a medium sized position in the stock and thankfully escaped relatively unscathed: if in doubt, get out! Now I said relatively unscathed in my Voyager report back in November and checking the numbers, it was a manageable loss of 9%. The shares were, of course, hit by a rather horrible profits warning on 19/01/2018 and fell by a further 50%. Yet another point that I regularly bang on about is that if you are caught up in a profits warning, and believe me it happens to us all, my action is to immediately sell at the opening bell. Investors who failed to do this with DTY having been hit with that awful 50% drop already, would have seen their remaining capital hit by a further 25% in the following couple of weeks: I have written about my handling of profits warnings back in 2016 and since that time, Ed Crofts team have also written a very thorough mini-book on the subject which reaches the same conclusion: SELL on a PW as in the coming weeks and months the stock is most likely to continue to drift south.  Finally, let,s add another green one that in my opinion is just so true:

Overconfidence can be a killer and I suspect after the sweet spot of 2017 that many PIs will feel they are very good investors. However, a strength for an investor is to remain very self-critical and examine the downside at least as much as you enthuse about the possible upside. This weekend I travel to the UK City Of Culture, Stevenage. Actually, I am quite thankful to the New Towns Act planners as they have actually created a town that manages to make my old hometown of Luton, look marginally attractive and that does take some doing believe me. The football ground itself is totally unappealing and the stewarding just about the most inhospitable and incompetent I have come across. The things I do in the cause of football! Whatever you are doing, I wish you a good weekend and definitely feel very envious of those investors residing in warmer climates. As ever, happy investing! Voyager RNS Log WC 28/01/2018

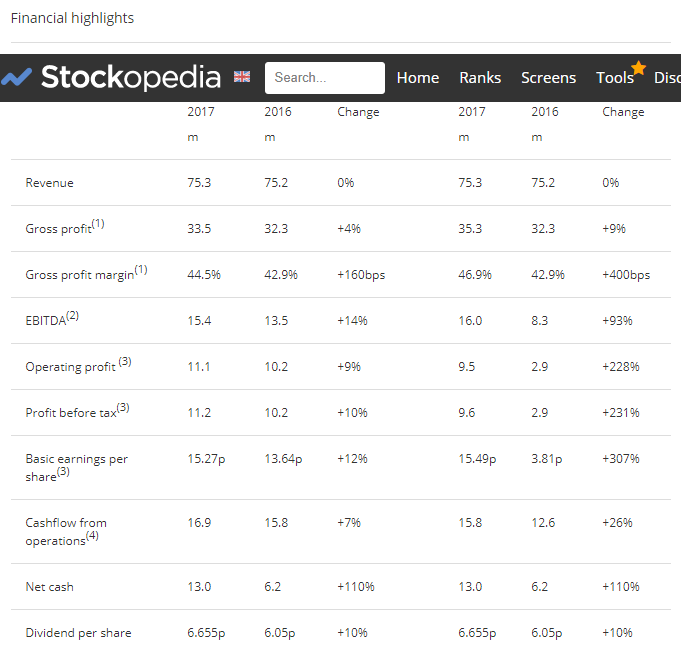

As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. A fairly short report this week and to be quite honest, that’s rather nice in a way as it makes life so easy and hopefully one can let time and quality tick along together and work their slow magic provided Mr Market is not in a terribly bad mood for weeks or months. I have to say that I am not a great share price watcher and if a stock is not the subject of an RNS, then a week could easily drift by between me looking at prices. Having said that, I always have a sort of alarm for non-noise movement but the serious reactions are usually RNS driven hence my focus on what’s going on with a business rather than what mood the punters are in. Actually, for clarity in sharing my rambling thoughts, I am adding a key for the colouring of text: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. So, let’s have a look at any RNS affecting shares within the portfolio: Well Monday, Tuesday and Wednesday came and went very quietly without any price action RNS for any of the portfolio shares. Thursday 01/02/2018: Keywords Studios (KWS): Mkt Cap £918m: RNS offering a trading update: Full year trading update Strong financial performance- strengthening our market leading position The Board is pleased to announce that it expects revenues to be not less than EUR150m (FY16: EUR96.6m) and adjusted PBT* of at least EUR22.5m (FY16: EUR14.9m), both of which are comfortably ahead of consensus market expectations. Strong organic growth remains a feature of the Group's performance and this has been supplemented by acquisitions as the Group continues to deliver on its strategy in order to become the "go to" supplier of technical services to the global video games industry. The Group is now comprised of seven globally managed service lines operating from 42 production studios in 20 countries, compared to four service lines operating from five production studios in five countries at the time of our IPO in July 2013. During the year, we welcomed eleven businesses into the Group across all its existing service lines as well as its newly established Engineering service line. 2017 saw two of the Group's largest acquisitions to date, VMC and Sperasoft, which have further strengthened our service offerings and client penetration and extended our geographic reach and access to talent. Sperasoft enabled our entry into Co-Development, in which multiple services including game programming and art creation are delivered holistically in the game development phase, whilst VMC has bolstered our Engineering capabilities. These significant acquisitions represent yet further steps in the pursuit of our strategy and we are pleased with how smoothly they are being integrated with the rest of the Group. The Group has invested net cash of EUR89.1m in the acquisitions described above, funded by the Group's strong cash generation, available debt facilities and a successful GBP75m equity placing in October 2017. The placing further demonstrated the support of our existing shareholders as well as enhancing our shareholder base through the addition of a number of new institutional investors. Following these acquisitions, the Group had EUR30.5m in cash at the year end and had utilised EUR18.3m of its EUR35m rolling credit facility, which leaves the Group well placed to complete further selective acquisitions in 2018. My View: I continue to rather like my favourite Meccano company as it continues to grow both organically and by acquisition. Certainly, I look forward to the final results both this year and next year to get a feel for the year on year appreciation of the financial performance. As mentioned in earlier RNS Voyager notes a few months back I sold some shares in KWS equivalent in value to my cumulative purchases I had made over the past couple of years. The shares having so markedly increased in value means that the holding I still have remains as one of my highest portfolio percentages by retained value of stock. I see no reason to reduce my holding but due to its high valuation in conventional terms, I will keep a close watch on this special situation as if and when the markets turn sour, it could potentially be hit rather hard. Thursday 01/02/2108: Spectra Systems (SPSY): Mkt Cap: £46m: RNS Trading Update Trading Update This announcement contains inside information for the purposes of Article 7 of Regulation 596/2014. Spectra Systems Corporation, a leader in machine-readable high-speed banknote authentication and brand protection technologies, announces that it received confirmation yesterday from its licensee for covert materials supplied to 18 central banks that the royalty component of the licensee's payments will be higher than previously expected for 2017. As a result, Spectra estimates that its profits for the year ended 31 December 2017 will exceed market expectations. My View: well like KWS, one of my special situations and I gave the following thoughts on SPSY a couple of reports back in mid-January when they released the good news about Licencing Revenues and Revised expectations: “simply put, how beautiful as the work has been put in, the product delivered and it’s now almost as simple as counting the cash as it arrives from the customer. It’s not a big company and usually, I draw a line about having any more than one investment below a Market cap of £50m as such stocks can be very illiquid when you want to make an exit and sometimes only quote to very small normal market size. However, I really took a like to this one last October and nabbed a few for my special situations portfolio. Incidentally, for those who like the highly regarded Stock Ranks (SR) approach pioneered by Ed Croft’s Stockopedia team, SPCS has an excellent SR of a 95 and nicely gaining momentum. I am happy to continue to hold and should there be a little pull-back, which I expect there to be, add a few more”. This TU nicely gives both confirmation and faith to continue to hold for hopefully further gains. Friday 02/02/2018: No RNS for shares within portfolio. Time for a Glad I Am Not There: that unbelievable crowd at Utilitywise (UTW) still can’t agree with the auditors/advisors what constitutes revenue recognition and dealing in the shares has now been temporarily suspended on AIM until such time that the accounts for the FY ending 31st July 2017 may be agreed and published. If UTW can’t really publish with market confidence what their revenue was then, however, can an investor make a serious investment judgement on the stock? Certainly, this one has been flagged as a major risk for a couple of years now and was I believe, first highlighted by the excellent Paul Scott as a serious risk when the share price was far higher than it’s current suspension price of 40p. Investors have had a lot of time to assess their position in this business over the last couple of years and I really hope that the majority of private investors managed to get away some time ago. If ever I remotely suspect something dodgy in a companies accounting practice, then I simply get out. Staying on that theme, Purple Bricks (PURP) put out an odd RNS on Friday 02/02/2018 contesting the findings of the Jefferies research report in which Jefferies rather questioned the validity of some of the PURP figures. It’s not a share that has seriously tempted me as I really don’t feel I could ascribe any valuation to the share with its share price rather built of management projections and hope of things to come. PURP is to me a rather odd one and this mornings RNS attacking a research note simply increases my resolve to steer well clear of the business; maybe I am missing a wonderful opportunity but I just don’t fancy the risk. After last weeks away win for the Hatters at Grimsby, I penned an article titled “A Tale of Einstein & Chips By The Seaside”. It’s not only in football that suffers from what Einstein quoted “insanity is doing the same failing thing again and again and expecting a different result”; you see one of our perennial underperformers that the manager insists is “really good” failed yet again and actually got sent off after 30 minutes. As ever, have a good weekend and happy investing. Voyager RNS Log WC 21/01/2018

After the hectic last week of many RNSs from the portfolio, this week started quite sedately with nothing to report for either Monday or Tuesday; I honestly don’t mind a little quiet once in a while as it gives you time to both reflect and get on with other things in life. In terms of new investments, I have been wrestling with my conscience about not buying shares in Israeli companies. Am I unreasonably biased? Well after various historic dabbles with investments in Israeli companies I generally have not been left with a taste trust or confidence. So, I asked myself why was I considering breaking a rule and buying into Taptica? Well it would surely be on the grounds of what I term as a special situation i.e a business where something possibly game-changing is really happening, good RNS stories etc. with a nice “ahead of expectations trading update in early January: could I overcome my bias? Well the answer which was possibly influenced by the excellent McMafia on BBC was “don’t, at least not just yet”; just can't get that comfy feeling. No, I am afraid my “no-go” countries which include the bulk of Africa, Russia, Israel & China plus a few others, remain as they were. I know fellow investors will quote companies that have done well but equally from those countries I could quote Emblaze, Telit, Putin’s RusPetro, Stella Diamonds in Africa and various Chinese AIM rubbish; just why put your cash at risk? I have been adding a few bits & bobs to the portfolio in the last few days but these have been in the form of Investment Trusts, an area of investment I have been very keen on for many many years. I will have to get my bum into gear at some time in the next quarter and do an article dedicated to investment trusts and my approach to these terrifically underrated investment vehicles. Well, that’s enough rambling on, let’s have a look at this week’s RNSs that are relevant to companies within the Whittler universe. As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. Monday 22nd January 2018: No RNSs for whittler stocks Tuesday 23rd January 2018: No RNSs for whittler stocks Wednesday 24th January 2018: Bodycote: BOY: Mkt Cap £1880m: RNS BODYCOTE CONFIRMS EUROPEAN EXPANSION IN HOT ISOSTATIC PRESSING NEW MEGA-HIP VESSEL SCHEDULED FOR 2018 DELIVERY Bodycote is pleased to announce that its Sint Niklaas, Belgium, Hot Isostatic Pressing (HIP) location will take delivery of a new "Mega-HIP" unit which will be operational by the end of 2018. The new high pressure, high temperature Mega-HIP is Nadcap capable to meet the growing demand of the European aerospace market over the next five years and beyond. This investment will significantly increase Bodycote's Nadcap HIP capacity globally, in addition to the substantial increase in Nadcap capacity which Bodycote completed in 2017. These recent investments highlight Bodycote's commitment to expand its global HIP capacity to meet market requirements. In addition to aerospace, Bodycote HIP serves clients around the world in markets as diverse as medical, power generation, marine, nuclear, automotive and electronics with both HIP services and its Powdermet(R) technologies. The recently launched Powdermet(R) technologies incorporate new, patent-pending techniques that combine 3D printing with well-established net shape and near net shape (NNS) techniques. This new hybrid technology dramatically reduces the manufacturing time and production cost of a part compared to producing the same part using 3D printing alone. My View: well not exactly shooting from the HIP, the announcement looks positive for Bodycote and on another day may well have added a couple of pence to the share price but Mr Market was not in his best mood on Wednesday; no real issues in my opinion just uninteresting market noise taking the markets down a touch. I think that BOY is a lovely quality business and the share price itself had appreciated by about 18% since the middle of December. Until there is a recession, I am just going to sit on my hands with BOY and hopefully let the quality continue to play out. Wednesday 24th January 2018: WH Smith: SMWH: Market Cap £2340m: RNS Trading Update The Group delivered a good performance in the period with total sales flat year on year and like-for-like sales down 1% for the 20 weeks. Total sales in Travel were up 7% with like-for-like sales up 3%. We have continued to see good sales growth across all of our key channels and gross margin continues to grow in line with plan driven by category mix management. Our store opening programme in the UK is on track and we expect to open around 15 new units this year. Our new large airport stores in Gatwick and Stansted opened in the period and are performing well with good feedback from both landlords and customers. Our International business continues to grow and we now have 249 units open, including 2 of the 10 units we have won in Changi Airport, Singapore. We expect all 10 units there to be open this spring. In High Street, total sales were down 5% with like-for-like sales down 4%, in line with expectations. Gross margin was up year on year although slightly less than anticipated, in part reflecting the lower sales of high margin spoof humour books compared to the same period last year when humour books had a particularly strong performance. However, we continue with our cost efficiency programme and now expect full year cost savings to be in the region of GBP12m, slightly ahead of target. My View: well not exactly a trading update from my favourite boring business that will get the punters excited but the real interest in the business for me is the Travel which in 2016 weighed in with 66% of the groups PBT and rose to 69% of group PBT in 2017. According to the TU, travel is continuing to grow both by expansion and like-for-like in 2018. Overall, I am happy to continue to hold. Thursday 25th January 2018: No RNSs for whittler stocks. A nice chance to start a slow cooker large batch of Bolognese; if you take care with the selection of the ingredients, the quality really comes given time in the slow cooker; a bit like investing really! Friday 26th January 2018: No RNSs for whittler stocks Well, that’s a very short RNS log this week but it at least gives one a chance to draw breath after such a lot of scribbling last week. I am quite glad I ditched Galliford Try last week as the Carillion news broke; that swift action really protected my capital as since the sale the price has drifted down a further 12% as I write. I should say that I think GFRD is a very decent company and in all probability, I will return to invest in GFRD again but for now, I simply protect my capital. In my opinion, two fairly simple rules apply in this case:

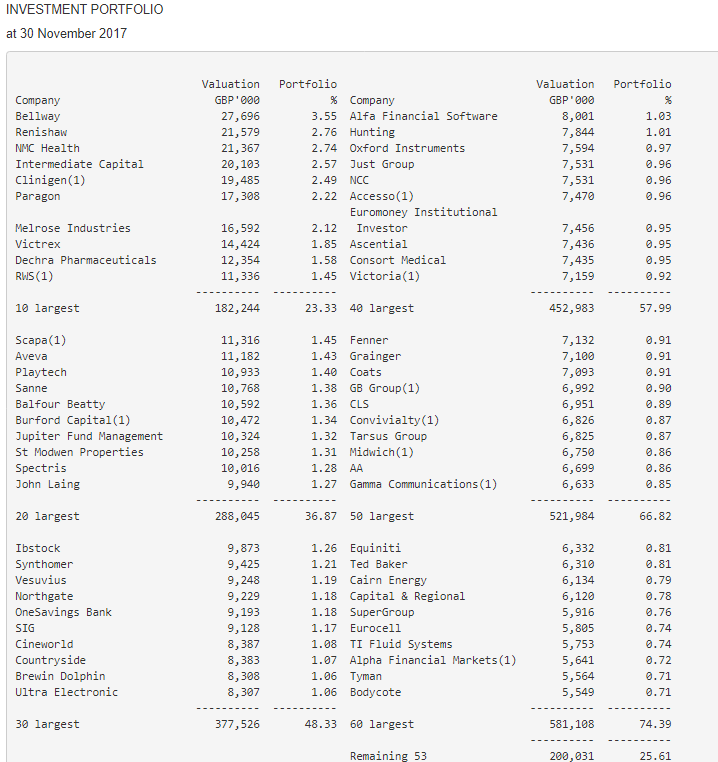

On to next couple of weeks and we may well see a trading update from OTB, maybe JE., KWS and results pencilled in for FDEV & AMO. This weekend my incurable hattersitis take me to the delights of Cleethorpes where the Grimsby ground is situated with just about every old iron girder corroding nicely is the salty atmosphere. What a dog of a journey it is but needs must etc. Whilst I am not the greatest fan of fish & chips, even I have to say they are a bit special up there so I guess I will be digging into some. I hope you have a good weekend and should you find the time to read something really interesting, then over I slow cup of coffee, I would highly recommend a read of Terry Smith’s Annual Letter To Investors published a few days ago; a great read in my opinion. Happy investing. Voyager RNS Log WC 14/01/2018 This week has proved to be quiet a busy week after the lull over the festive season and things are picking up pace now including the arrival of those blasted new years resolvers in the pool at 6:30 am; are they a blasted nuisance or am I just getting grumpy towards them. Hang on, I have always been grumpy to such transient creatures but never mind a couple of really hard frosts by early February usually sees them retiring back to the comfort of the duvet for another 11 months. For me, the pattern stays the same every working day with a swift mile in the pool followed by initial interrogation on the iPhone of portfolio RNS’s; hopefully seeing no bad news then on with the day. I have always found that ploughing length after length in the pool gives me a great quiet time to think things through. When I was part of the rat race it used to be work issues, now it’s more about writing footy or investment stuff or another passion, good quality food. I absolutely hate the world of convenience food; whoops, did I mention I own shares in Just Eat; no moral fibre me! Anyway, enough of this Jeremy Clarkson stuff, what’s been going on in the markets relevant to shares within the portfolio? As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. Monday 15th January 2018: Spectra Systems (SPSY): Mkt Cap £39m: RNS: Licensing Agreement and Supply Agreement + Revised Expectations Licensing Agreement and Supply Agreement Spectra Systems Corporation, a leader in machine-readable high-speed banknote authentication and brand protection technologies, is delighted to announce that it executed on Friday an exclusive, worldwide, licensing agreement for one of its existing products which is in use by 18 central banks through an existing licensee, a major supplier of banknotes worldwide. The licensing agreement will extend the rights to the underlying technology, which has been in use since 2003, in perpetuity and generate $11.2 million in royalty payments over the next five years. The payments will be settled in eleven equally spaced payments. In addition, Spectra also executed a Material Supply Agreement with the same licensee to provide them with covert materials exclusively for a period of ten years at reduced rates relative to the current agreement. The Board anticipates that the supply of material, which does not incorporate minimum quantities, will generate a total revenue of approximately $1.5 million -$2.0 million over the next five years. It is estimated however that the combined licence and supplied material sales will generate a contribution per annum from this product through 2023 which is approximately 2.7 times that of the current agreement, based on the minimum purchase requirements in that agreement and experienced in certain recent years. Based on the execution of these agreements, Spectra is expecting that both its revenue and particularly its profit before taxes for the year ending 31 December 2018 will significantly exceed market expectations. My View: simply put, how beautiful as the work has been put in, the product delivered and it’s now almost as simple as counting the cash as it arrives from the customer. It’s not a big company and usually, I draw a line about having any more than one investment below a Market cap of £50m as such stocks can be very illiquid when you want to make an exit and sometimes only quote to very small normal market size. However, I really took a like to this one last October and nabbed a few for my special situations portfolio. Incidentally, for those who like the highly regarded Stock Ranks (SR) approach pioneered by Ed Croft’s Stockopedia team, SPCS has an excellent SR of a 95 and nicely gaining momentum. I am happy to continue to hold and should there be a little pull-back, which I expect there to be, add a few more. Monday 15th January 2018: Bodycote (BOY): Mkt Cap £1882m: RNS Us Tax Legislation & Trading Update US Tax Legislation Bodycote notes the enactment of the Tax Cuts and Jobs Act in the United States on 22 December 2017 reducing the statutory rate of US Federal corporate income tax to 21%. Whilst work is ongoing to review the full future impact of this new US tax legislation on the Group, it is expected to give rise to a significant non-cash tax credit for the Group in the year ended 31 December 2017 as a result of the revaluation of US net deferred tax liabilities. Subject to final audit and confirmation of final tax computations, the effect of this one-off revaluation of US net deferred tax liabilities is expected to add c. 5p to EPS for 2017. Trading Update Bodycote also announces that trading in the final quarter of 2017 was better than anticipated and the Board now expects full year 2017 headline operating profit to be towards the upper end of market expectations (company compiled analysts' estimates range: GBP117 million - GBP126 million). Bodycote intends to announce Full Year Results on Tuesday 6 March 2018. My View: well any regular readers of this RNS log will know that I rather rate this high-quality business. Maybe it’s not the most exciting beast on the market, even possibly a touch boring but we now know that profits will be towards the top end of expectations and when you look at the range quoted above, that looks rather good to me. Again what a nice SR of 88, can’t be bad and I am very happy to continue to hold. Monday 15th January 2018: Looking in another area we see the very sad news about Carillion a share that was valued at way over 300p for many years and now suspended at 14p and in what appears to be a terminal stare. The numbers have looked poor for a couple of years now yet I suspect some may have been sucked in by the generous and unsustainable dividend that has nowhere near been covered by FCF for the majority of recent years along with debts. This had a knock-on effect to a company within my portfolio: Galliford Try (GFRD) who mid-morning following the collapse of CLLN, put out the following RNS: Joint Venture with Carillion plc Galliford Try plc (the "Group") notes the announcement by Carillion plc this morning. The Group is in joint venture with Carillion and Balfour Beatty on the 550 million Aberdeen Western Peripheral Route contract. The terms of the contract are such that the remaining joint venture members, Balfour Beatty and Galliford Try, are obliged to complete the contract. Our current estimate of the additional cash contribution outstanding from Carillion to complete the project is 60-80 million, of which any shortfall will be funded equally between the joint venture members. The companies will discuss the position urgently with the Official Receiver of Carillion and Transport Scotland, to minimise any impact on the project. My View: firstly on CLLN where for investors caught up in the debacle one can only have limited sympathy as the signs were there for all if they cared to read the newsflow and look at the numbers. Yet the knock-on goes across many, many small businesses caught up in the web of subcontracting for the giant Carillion that CLLN lived within. Contractor business viability, jobs pensions all very sad stuff. Rather like being on a rowing boat being towed along by the Titanic; my sympathies to all innocent parties involved. Then we come to the knock-on effect for the likes of GFRD (Mkt Cap £970m) working with CLLN on major joint ventures. This casts a fair doubt on what hit there may be to GFRD’s bottom line this year and possibly also next year and it’s a doubt and risk I did not feel comfortable in carrying so an unemotional exit as soon as the GFRD RNS hit the market; funds intact and in fact exiting with a few % profit but, more importantly, reducing risk of further downside. Whilst on the subject of CLLN, just a thought: Very predictably, history does repeat itself and we can learn from the past if we choose to do so. Any readers remember the collapse of the once £1bn valued company Jarvis back in 2010? There are lessons there and again with CLLN; the tipsters being so terribly wrong and the toxicity of unsustainable debt. I remember in the days when I used to look at what the experts had to say, the absolute number of well-followed experts who recommended Jarvis as a super stock “super stock”, one to hold forever. Yes, right: such things inspired the article I published in July 2017 about the “share detectives” titled Watching The Detectives. Tuesday 16/01/2018: International Greetings: IGR: Mkt Cap £259m: RNS Trading Update Strong trading delivers earnings upgrade IG Design Group plc, one of the world's leading designers, innovators and manufacturers of gift packaging, greetings, stationery, creative play products and giftware, announces an update for the third quarter, which covers the Group's Christmas trading period to 31 December 2017. The Group is pleased to report that following the positive performance reported over the first six months ending 30 September 2017, trading has continued to be strong up to and throughout the Christmas period. In line with the strategy to further diversify the business, the Group expects to deliver record revenues in FY18 with the continued expansion of its global footprint outside the UK which the Board expects will account for over 70% of sales by destination. All regions are on track to achieve year on year revenue and profit growth and we are therefore pleased to upgrade the Group's full year performance with diluted earnings per share(1) expected to be ahead of current market expectations and delivering strong year-on-year growth. We continue to see strong cash conversion across the Group and expect average leverage for FY18 to follow the progress made in recent years and be significantly below an average of two times. Latest initiatives highlighted in our Half Year Results Announcement remain on track to drive future revenues in FY19 and beyond. Additionally, as a result of the level of the Group's US earnings the Board expects earnings per share to benefit in FY19 and beyond from the recent US tax legislation changes. Furthermore, the US tax rate change is expected to translate into lower tax payments, thereby enhancing the cash generation of the Group. My View: simply what’s not to like? As I said last week in this log, my view on this quality business has not changed since I commented on the interim results at the end of November 2017 and in fact are even more positive taking into account the quality acquisitions and a touch of tax generosity from our mate Trump. I am happy to continue to hold the investment which has delivered a return of well over 100% for me in the last 18 months. Personally, I think this very sound well-managed business will gain further investor support after this RNS and in my opinion, continue to appreciate in value. Again a very decent SR but I won’t quote numbers as I don’t want to offend Ed as I have already quoted two CRs above. Wednesday 17/01/2018: RNS: Henderson Smaller Cos Investment Trust: HSL: Mkt Cap £672m: Half-year Report. I do like good quality investment trusts and HSL is, in my opinion, a high quality IT delivering year on year, in fact, the half-year report shows that for the 5 years to 30/11/17 the share price appreciated by 159% and by 304% in 10 years. Not exactly sluggish and by far outperforming the FT All Share TR and that’s why I use it as one of my benchmarks to judge my own performance. Below I have included a listing of the 60 largest holdings in the HSL investment trust and whilst there is the odd dud, it contains a lot of quality stocks: again a demonstration of the benefits of a basket of stocks: see an earlier blog I did about me being a basket case. Just click/tap on the listing to enlarge the view.