|

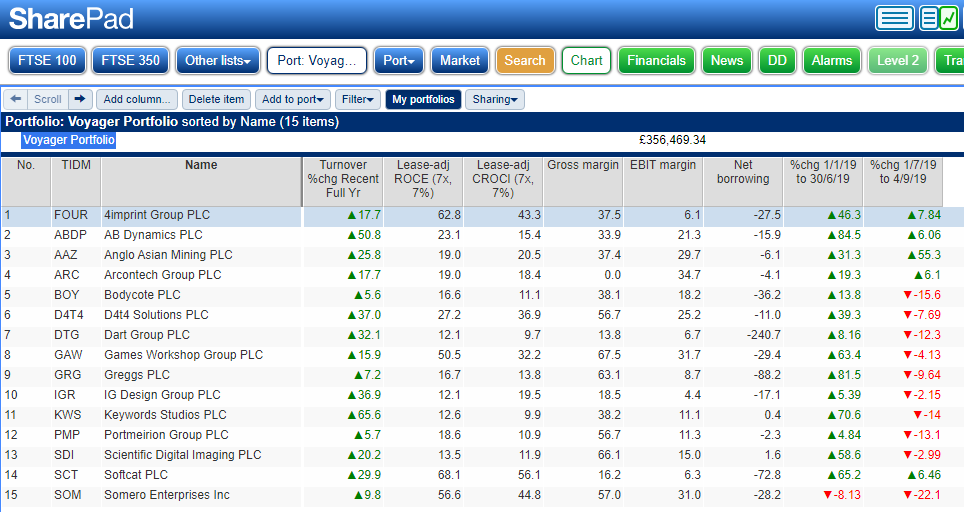

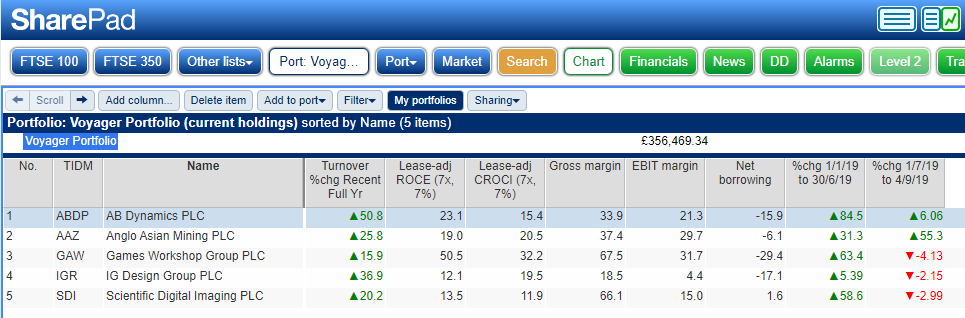

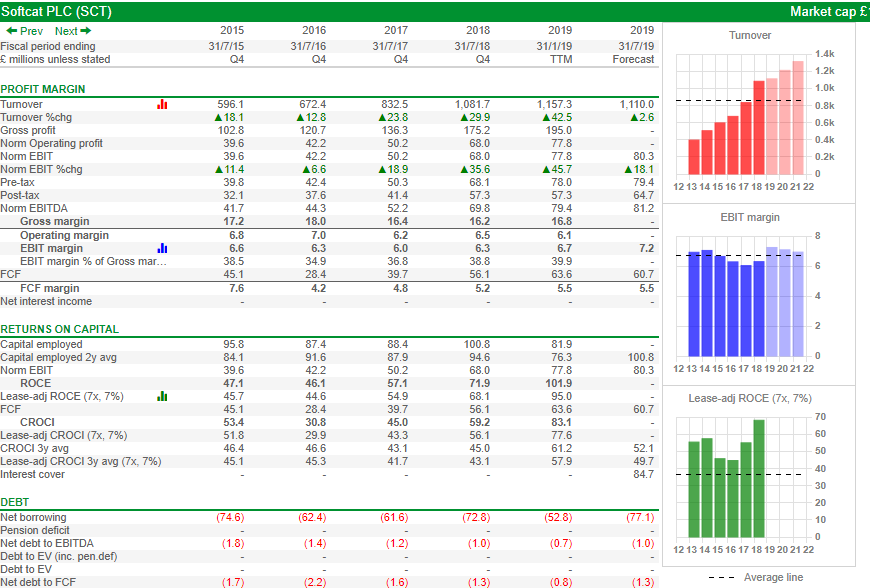

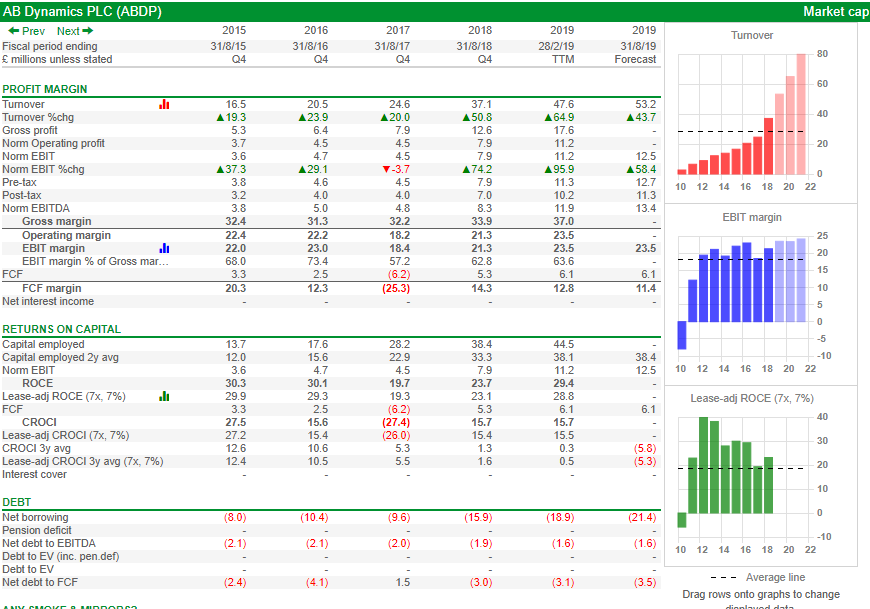

As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. I try to offer balanced; both bull & bear views on stocks that appear in the Voyager Log. I will never ramp a stock & simply try to offer my honest opinion on a company. Like everybody who offers an opinion, sometimes that opinion is proved to be wrong. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Note: the purpose of the Voyager is simply to share my reasoning in relation to selecting what I deem to be quality stocks, buying, selling and generally managing capital within a portfolio whilst responding to relevant news about a stock and overall market conditions. This month, it’s just a quick Voyager update for two main reasons. Firstly, nothing has changed regarding the current stock holdings within Voyager since the last log was published in early September and secondly, a rather painful hand injury makes any keyboard work less of a joy. In fact, whilst awaiting hand improvements, I purchased a rather comfy mouse; the Logitech Ergo, much comfier than any other mouse I have used. As I say nothing has changed much and the holdings are as listed in the September log. I still remain rather bearish on the immediate market prospects for stocks and for that reason, as stated before in earlier issues of the log, I moved heavily into cash once again at the end of June/July 2019. In reality, it’s a touch of Groundhog Day as I took similar action in the summer of 2018 and missed most of the October to December pains. Sadly it’s a market fact that no matter how convincing the fundamentals for a stock may be if Mr Market is grumpy your chances of making money are somewhat limited. I, of course, exclude those successful bargain hunters and value investors who have the skill to sniff out opportunities in these testing markets. However, analysis of my investments over 25 years shows that without a scrap of doubt my investment returns have been very significantly better when I buy into positive momentum rather than when one tries to bag a bargain on thinking “blimey that’s good value, surely it can't go down any further”. So often bargains become even bigger bargains as time goes by and then turn into the dreaded “long term hold” as an investor waits to maybe break even at some time in the future. To add to my bearish outlook, we seem to be seeing more and more profits warnings, sometimes a little tucked away in the detail and also a higher proportion of H2 weightings/contract delays/macro-economic uncertainty etc that to my opinion, we would normally see. I should say that I am certainly not immune to profits warnings and took three in the first six months of 2019: PMP which I had been quite bullish about yet sadly once again the CEO did not have a clue how sales/stock were moving in South Korea: resulted in a small loss. TEF a small gain as it had been in for an age and SOM which overall made excellent returns as a long term hold but was sold over two periods; firstly, some at the time of the June profits warning and the remainder following the fairly poor results in September. Interestingly both PMP & SOM have declined significantly further since those sales but an agreed take-over was announced for TEF. I will keep an eye on SOM but sadly I reckon the management remuneration at PMP is inversely proportional to their overall competence. My general rule on a profits warning is simply to exit fairly early and protect capital. As ever, I seek stocks that have amongst other things, the following attractive attributes: Increasing turnover, attractive returns on capital (ROCE + CROCI), good profit margins, low debt & so very importantly they show positive momentum. If we then throw into the mix some positive RNSs, we have a formula for success. Yet take away that positive momentum and the immediate reason to buy “right here, right now” tends to fizzle out & for my style of investing the stock remains on a watch list. The table below shows the medium to long term residents of the Voyager and gives a flavour of the easy first six months of 2019 we enjoyed on the markets, particularly for quality stocks, and the tougher conditions encountered as from July. Note: from the table below I no longer hold SCT, DTG, BOY, FOUR, ARC, D4t4 & GRG as these were sold in early July and gratefully, profits banked. I also sold my repurchases of an old star performer, KWS in July having rebought earlier in 2019. In addition to these sales, during the summer I also took some profits and reduced exposure (sliced by at least 60%) on ABDP, GAW, IGR & SDI as the cash position swelled. Table 1  Note the table is included to demonstrate what I look for in terms of fundamentals. These stocks have been medium/long-term residents of Voyager that were held for all or most of the first 6 months of 2019: the ones still resident are listed in the second table. A handful of others not listed have been resident for a very short period & cumulatively had a zero-sum effect on the bottom line. Also for clarity, I took profits in the ISA held XPP a stock I have often written about, in FY 2018/19 yet had a small long-serving residual holding outside of the ISA wrapper that I sold early in FY 19/20. The same style table but just including Voyager stocks continually held to date through 2019 is given below: Table 2  In addition to the above, relatively recent (mid-summer) cautious small starter positions sit in the portfolio: SPSY showing a modest profit, LTG currently treading water, LIT about 20% underwater as it got caught in the Burford tailspin and not to forget SND which has just left following a take-over.

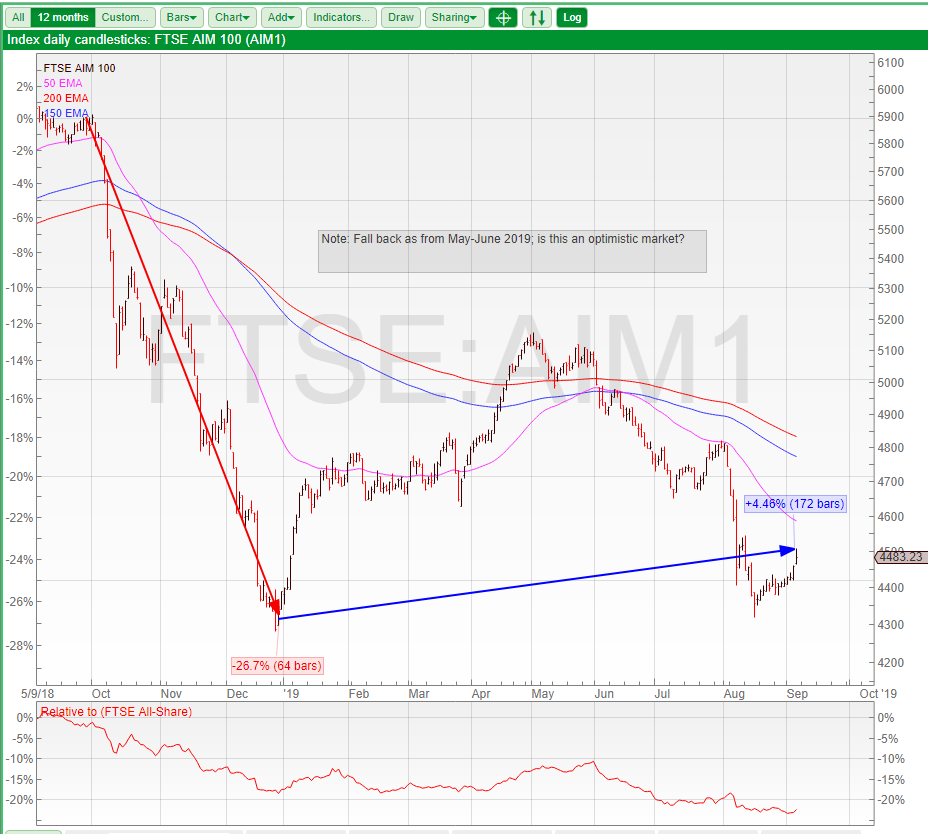

The striking thing from the above tables is just how much the mood has changed within the markets since July. We, of course, have the various political worries & trade wars to wobble the market and indeed many investors feel that a hard Brexit is baked into the current stock prices. However, I am not so sure and feel that wealth may possibly be seriously damaged over the coming months should an acrimonious divorce happen. Conversely, should Trump make friends with China and an acceptable deal be concluded regarding Brexit, then Mr Market may well smile again. As ever, should that happen then I will be happy to maybe not be the first one to arrive at the party but will arrive a touch later when risk and signs of that crucial momentum returns to those quality stocks. Oh yes, a few RNSs I should mention but is it really worth it at the moment with so few holdings and even as ABDP release an exceed market expectations RNS, there is a negligible effect on the share price; maybe that partly due to the fact that it’s had a cracking good year in terms of share price appreciation. At the moment I am pondering the future for the Voyager log as I think that currently, the blog-space is maybe a little crowded albeit with some very good commentators. In many ways, I feel that the communication of the methodology I originally set out to describe has been delivered and it boils down to selecting high-quality stocks, buying with momentum/positive RNS & protecting one's capital. Well, that’s it for now, stay safe in this unsettled market; catch you again soon, probably in November when hopefully typing is a touch more comfortable.

5 Comments

As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. I try to offer balanced; both bull & bear views on stocks that appear in the Voyager Log. I will never ramp a stock & simply try to offer my honest opinion on a company. Like everybody who offers an opinion, sometimes that opinion is proved to be wrong. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. I hope that everybody has had a good summer enjoying our mixed but wonderful climate. In terms of market activity, the Voyager portfolio is rather concentrated with a rather reduced number of stocks and as I have written before, contains a very significant percentage of cash after taking profits following a very good first half of 2019. Since the last Voyager RNS Log was published, profits have been taken on ARC, BOY, D4t4, DTG, FOUR, GRG, KWS, SCT & SOM. A small profit on IDEA was balanced by a small loss on IDEA. Also, I took a 7% loss on TM17 as I just did not feel comfy with it; not a good call as it’s moved up nicely since I sold. So, after all that activity the Voyager now consists of the following stocks: AAZ original buys at average 93p December 2018: a stock championed by my footy friend Simon on Twitter & showing the features I seek in a stock; let’s not go on about my dislike of the ex-Soviet block stocks! Simon writes a very good blog which can be found at http://share-knowledge.org.uk ABDP original buy at 410p in 2016 GAW original buy at 2400p in Feb 2018, I was late to the party here just could not identify with the product/hobby: yes, don’t tell me, daft reasoning from me. IGR original buy at 180p in 2016 LIT average buy at 93p and currently about 7% underwater caught in the Burford tailwind. LTG initial starter purchase at 115p fairly recently SDI original purchase at 35p late 2018 SND added at an average of 123p now subject of a low premium take over. SPSY traded a few times & current batch down by about 3% Just a note on why I moved to a higher cash position in late June/early July, really repeating my actions of 2018 which served me well in protecting me to a large extent from that rather torrid last quarter of 2018: well in addition to the current political uncertainty, it was my perception that we were seeing the following:

My thanks to SharePad for these charts

So, with that backdrop, again as I have communicated before, I moved to my highest cash position since the financial crisis of 2008; banking good profits and simply being cautious and managing risk. In addition, earlier in 2019 I increased my holdings in the “lazy stuff” that I just continually add to and let it sit in the bottom drawer: Fundsmith, Smithson, Blue Whale & a touch in Finsbury G&I: most of this gives me good non-UK exposure. Incidentally, I don’t consider this “lazy stuff” folio as part of the Voyager; I suppose that’s because it’s not really success via my own work but rather its excellent work done by some talented folk I trust. I should also say that now it looks likely that no-deal is an unlikely divorce scenario that I am feeling a touch less cautious and will be happier to take attractive positions as they show themselves; I may well have to wait but I am happy with that. Disturbingly once again we see some “lucky” dealing in terms of significant sales by some of the senior directors of AIM-listed companies; for example, take a look at ALT, AIEA, BUR and even one I did hold SOM. In the case of BUR, two directors sold a combined £118m of stock four months before the Muddy Water story broke. The directors then used essentially loose change to show their confidence post-Muddy Waters by buying back a miserly under £10m of “bargain price” shares. Sort of tells a story to take serious care particularly on AIM with very significant director sales. Note: not all director sales are bad news for shareholders, in fact far from it: it’s well worth reading the excellent article The Ducks Are Quacking by Tim Rogers. The article can be found on Conkers3.com site. A quick look at a couple of RNSs this week for a couple of ex-holdings: 04/09/2019: Somero: SOM: Mkt Cap: £125m: RNS Interim Results. Interim Results for the six months ended June 30, 2019 Flexibility of operating model demonstrated, enabling increased dividend Somero Enterprises, Inc. is pleased to report its interim results for the six months ended June 30, 2019. Financial Highlights -- Financials are tracking broadly in line with the guidance provided by management in its 7 June 2019 trading update, with full year revenue expectations of between US$ 83.0m - 87.0m -- H1 2019 results highlight the flexibility of the Company's operating model that allows for rapid adjustment of costs to align with product demand -- The Company is proceeding with long-term growth investments made possible by a strong balance sheet and positive cash flows -- In line with the Board's outlook for the remainder of the financial year, the Board has declared a US$ 0.0575 per share interim dividend representing a 4.5% increase compared to H1 2018 My View: Just as a piece of information regarding the way I interpret trading updates and the wording used & accepting my broad brush & not an exact science: My take on RNS cautious wording/profits warnings is:

Anyway, I did write a fair amount about the previous SOM profits warning in an earlier Voyager offering a bull & bear case and being in awe of the CEO’s luck in selling his shares at the end of March as I wrote at the time “Was the sale of £2.7m of shares by the CEO Mr JT Cooney on 28/03/2019 inspired by the sight of a modern-day Noah’s Ark floating past his second-floor window? We can speculate but never really know!”. I won't go into any great depth here as I covered this one quite fully in June. Suffice to say that sales are not going in the right direction and in addition to the rain-related USA market we have Europe & the Middle East falling back badly. China on first look you could say it’s the same as H1 2018 but if you dig a little deeper China sales have actually receded since 2016. Additionally at the time of the June profits warning an estimated turnover for the year was given $87m this has now been cautiously revised to $83m-$87m. Sorry SOM but it looks rather as if things are deteriorating further since the June profits warning-TU. Adding the painted outlook statement did not really encourage me to continue to hold as I sold the residual holding. Overall my investment in SOM has been a very profitable one as I entered at 100p back in 2014 but good things don’t last forever especially with cyclical stocks. Incidentally, although a very profitable experience, I really should have done better. I sold >60% of my SOM shares at something over 300p as they a) hit the 50d MA and b) touched the 8% trailing stop-loss. Of the remainder, which then went on to rise quite well and maybe should really have been sold when the share price fell below the ongoing trailing stop-loss/50d MA/150d MA last October: yet still a positive feel for SOM at that time in the investment community. I then sold a further chunk at the June profits warning and the residual after the 4/9/2019 poor TU. Overall, a very profitable investment but it would have been appreciably better if I had followed my own rules regarding:

Dart Group: DTG: Mkt Cap: £1100m: RNS AGM Trading Update At the Company's Annual General Meeting today, Philip Meeson, Executive Chairman, will make the following statement: "In our Leisure Travel business, the later booking trend as reported in our Preliminary Results Statement on 11 July 2019 has continued, with overall demand for both our Flight-Only offering and Package Holiday product continuing to strengthen. Encouragingly, package holiday customer numbers as a proportion of total departing customers have increased for summer 2019 to date. Ok, I reckon this part sounds fine. Winter season forward bookings have yet to match our seat capacity growth, therefore pricing for both our leisure travel products will need to remain continually enticing. Not so fine; what they are saying is that they are struggling to sell seats for the winter season & are lowering prices. Encouraging progress continues to be made at Fowler Welch, our Distribution & Logistics business, with new commercial wins improving the quality of revenue and operational excellence ensuring customer satisfaction. Maybe it’s just me, but they should have flogged off the Fowler & Welch legacy business years ago; it just doesn’t fit with the new look DTG. With still some way to go in the Leisure Travel winter booking cycle, the Board remains optimistic that current market expectations for Group profit before foreign exchange revaluations and taxation for the year ending 31 March 2020 will be met. What they are saying is “if everything really goes well for us we might just reach market expectations”. Looking further ahead, given the cost pressures the Travel industry is facing in general, which will intensify given the weakness in sterling, plus the deepening Brexit uncertainty and the impact this may have on consumer confidence, we remain very cautious in our outlook. The Board will provide a further trading update on publication of its interim results on 21 November 2019." My View: after being a Voyager resident since buying at 200p back in 2013, I sold 60% of my DTG holding leaving in mid-May at an average of 932p and the residual batch leaving at 800p in July. The reason for the sales was a combination of travel industry worries, Brexit worries and simply what the chart was telling me. It had been a great ride but time to disembark off the aeroplane for a little while at least until things become a touch less risky. As you can see from my comments against the RNS paragraphs, I reckon on balance it’s best not to be onboard DTG just at the moment; remains on the ex-holding watch list for now. Other bits: Does Success Rate Matter? I read a good conversation on twitter discussing the percentage success rate that private investors have in terms of profitable selections. Within Voyager over the years, I have held many shares that go up a few % and add just a touch to the bottom line and of course, jettison as early as possible those that fall over say 8%; simply protecting capital as it’s not at all painful to take an early small loss. The real work is done by a smaller population of stocks that go on to become long term resident in the portfolio and really significantly contribute to the portfolio success: the +10% and -8% leavers are really just incidental. In fact, you could be wrong 50% of the time with your stock selections and as long as you manage your portfolio well, be very successful. A touch of entertainment: If you are anything like me than a good investment video/story is really enjoyable. A few that I certainly found both enlightening and entertaining are: The Big Short: the story of the sub-prime lending that catalysed the financial crisis: Netflix Betting on Zero: the Herbal Life pyramid system: Netflix The China Hustle: really makes you think about the credibility and worth of some well known financial “stamps of approval”: Netflix The Inventor out for your Blood In Silicone Valley: the incredible story of Elizabeth Holmes and the Theranos scandal: should be available in the UK later this year probably on Netflix. Well, that’s it for now; maybe catch up again in October. Happy investing! Notes:

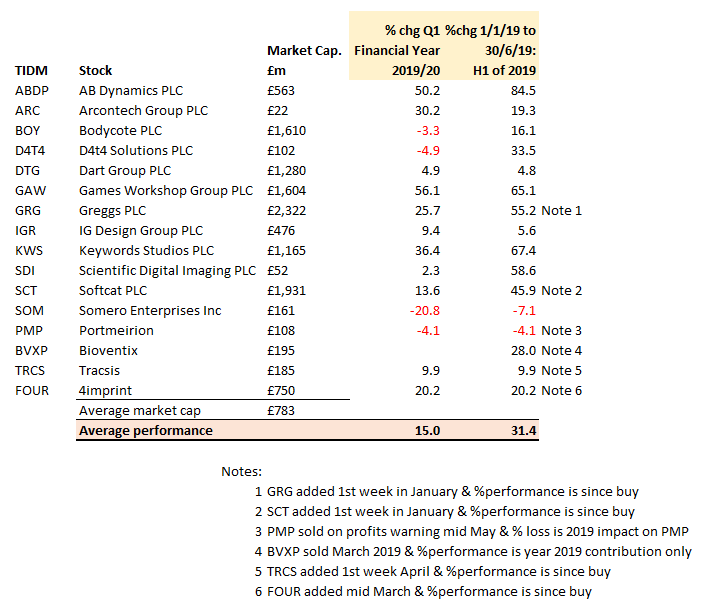

Whilst the Voyager RNS Log is taking a long summer break, I thought it would be worthwhile giving the briefest of updates on arrivals and departures since May and an overall feel on the performance the stocks held within Voyager both over H1 of 2019 and also in terms of Q1 of the 2019/20 financial year (FY being my preferred measure of a year). Like all private investors, I will suffer from occasional profits warnings and in H1 of 2019, I suffered two such warnings; PMP & SOM. To my mind, PMP was really unforgivable in terms of excessively paid management once again demonstrating that they had no “finger on the pulse of South Korea”. PMP was sold for an -11% loss in H1 although the individual impact for 2019 was -4% as the stock started the year in profit. On the other hand, SOM which has returned handsomely over the last five years was treated in a more forgiving fashion with its weather-related profits warning and remains in the Voyager. Also leaving was BVXP; previously recorded in the Log at just under £40 having first entered at £7 about five years ago. The new arrivals in May and like all new arrivals they will have to prove their worth or be jettisoned are SND, AAZ, IDEA, & LIT. Pleasingly all four are proving their worth with an average gain over the basket of four stocks of 16% since mid-May. Hopefully, one of them will develop into a gem that may be worthy of a portfolio place for several years, we shall have to see. The summary table for the other stocks currently held within Voyager for H1 of 2019 and also Q1 of financial year 2019/20 is given in the table below. Note: I heavily sold down KWS at >£18 during my risk mitigation in June 2018, they originally joined the Voyager at well under £4 in 2016 but retained a fairly sizable holding which was further added to at around the £12-£13 mark in late March/early April. As a reality check, it should be remembered, probably with most private investors portfolios, that January 2019 started from a very soft and easy base following the overall market decline of the last quarter, October-December, of 2018. So, all a touch unreal and overly flattering possibly. I rather suspect that H2 of 2019 may be a touch more challenging partly due to our inept politicians who amazingly in comparison make Trump appear a real statesman.  Oh well, back to my long summer break now; I will do the odd Tweet until the Voyager returns in September(ish).

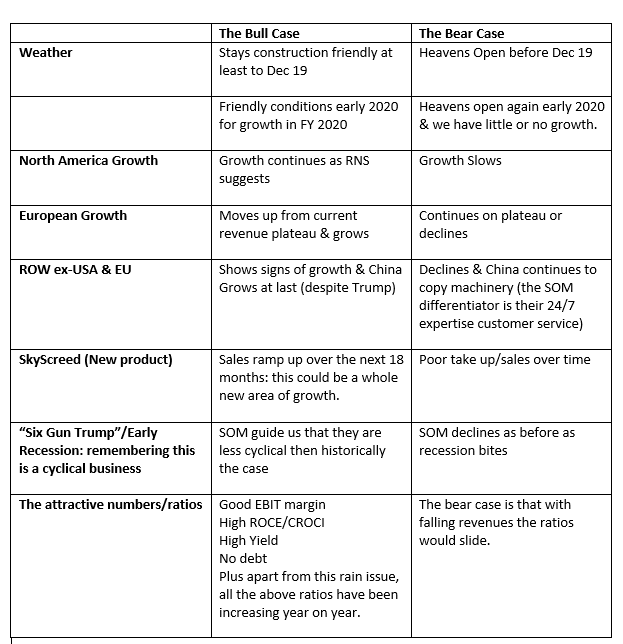

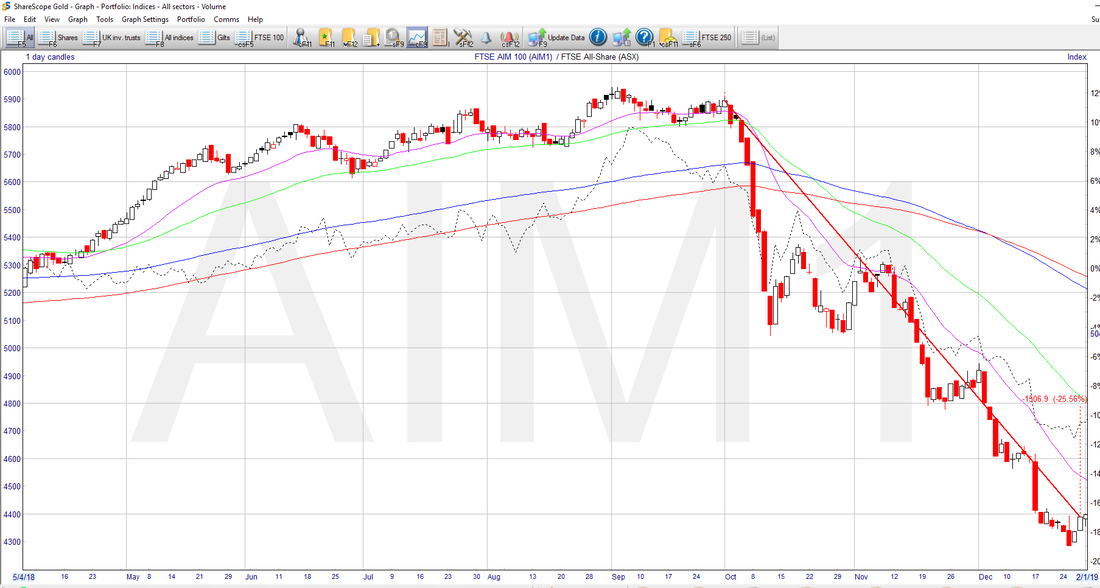

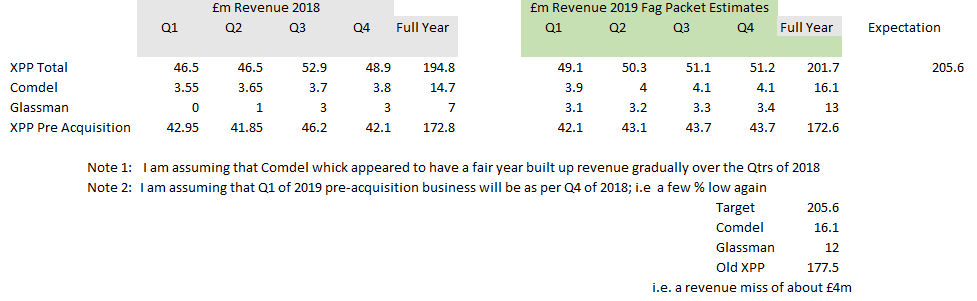

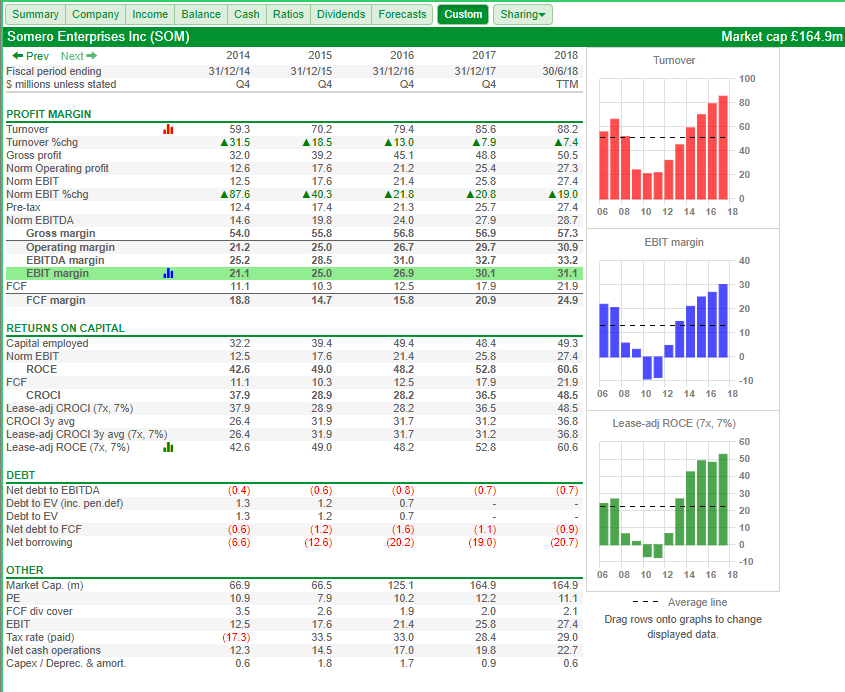

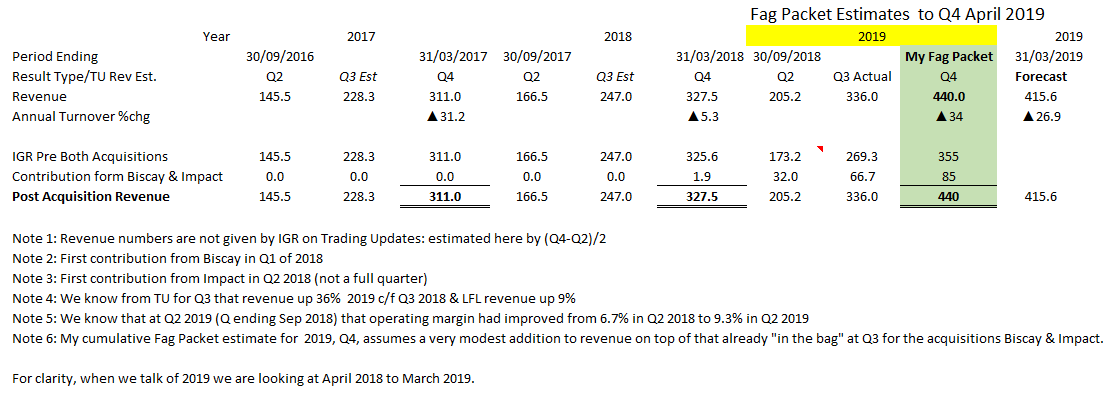

Enjoy the summer & cheer the Lionesses on tonight against the USA; I am really impressed with the standard of ladies football. Voyager RNS Log 07/05/2019 to 07/06/2019 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. A sobering thought to start with in that I suspect that the great majority of us are enjoying apparent good returns so far in 2019, the actual fact is that the majority of stocks in the Smaller Cap/AIM sectors are still some way of their valuations as seen at the end of September 2018. Yes, I can hear you say, here he goes “emotionless bar**a*d” yet, as I always say, investing remains a long game. In the last quarter of 2018, the FTSE Small Cap Index fell by -11% & that of the FTSE AIM100 by -26%. The two following SharePad charts show that whilst 2019 is feeling easy by comparison, it’s a long haul back to where those indices sat at the end of September 2018; yes, investing is a long game.   As ever, apart from “silly times” when investing in almost anything makes you money, we live in a stockpicker's market. The last FY was rather kind to me and that was partly to my minimizing my exposure in Q3 of the financial year (October to December 2018). Simply put, in easy times even the turds float but in normal market conditions, it’s a touch more challenging to pick the winners. So, there is a fair bit of catching up to do since the last Voyager RNS Log, for the sake of boredom, I will keep the log brief with the exception of Somero: 07/05/2019:4imprint:FOUR: Mkt Cap £730m: gave an encouraging AGM statement “Although it is still early in the year, the Board is confident that the Group will deliver full year financial results in line with current market forecasts." My View: So, I am happy with that from what I consider to be a reasonably valued growth business with growing revenues/profits and excellent returns on capital; I would like the EBIT margin to be higher but otherwise, ok.  14/05/2019: Greggs: GRG: Mkt Cap £2240m: GRG gave a pleasing trading update “The exceptional level of like-for-like sales growth that began in January has been sustained in the months that have followed, driven by increased visits to our stores. Looking forward, the sales comparatives from 2018 become progressively stronger but we now anticipate materially higher sales for the 2019 year as a whole than we had previously been expecting: the Board believes that underlying profits (before exceptional costs) for the year will be materially higher than its previous expectation”. My View: originally bought in January and some profits taken but very happy to hold remainder as this company is on a roll. Just like my old boring holding SMWH travel, you usually are in a queue in this popular food/coffee outlet and the quality is value for money. Wherever you get the chance, it’s always valuable to check the popularity of such outlets; I never had to queue at CAKE!. Happy to continue to hold GRG.  14/05/2019: Portmeirion: PMP: Mkt Cap: £110m: Trading Update & profits Warning I have written some very encouraging things in the past 15 months about PMP and by all news-flow, the business was growing well and had overcome the glitch they had in South Korea back in 2016. However, totally unexpected it seems, the management were again showing a remarkable disconnect between themselves and their over stocking agent in South Korea. So, sorry, I have completely lost confidence in the “finger on the pulse” skills of the very well rewarded CEO and his team. Now sold and rather unlikely to return. 15/05/2019: Scientific Digital Imaging: SDI: Mkt Cap £52m: Trading Update giving revenue for the full year as moderately ahead of expectations and profits to meet expectations. The share price has come off a little since its earlier rise but happy to hold and take the occasional top up.  My View: I do like the business which to me resembles a Judges Scientific style. At the same time, you have to keep in mind the potential potholes that may confront highly acquisitive companies. 20/05/2019: Softcat SCT: Mkt Cap £1483m: Q3 Trading Update The Company continued to perform well during the Period and has delivered strong year-on-year growth across all income and profit measures. Performance drivers remained broad-based, with different technology areas and customer segments all showing growth. The Board is therefore confident that full year results will now be slightly ahead of previous expectations.  My View: I am happy to continue to hold SCT which has delivered a 40% return since my purchase in January. 23/05/2019; Hollywood Bowl: BOWL: Mkt Cap £352m: Interim Results Really nothing much for me to say about this tidy well run business that simply ticks along nicely. I don’t expect it to set the Voyager racing but nevertheless happy to hold this steady number. 24/05/2019: Bodycote: BOY: Mkt Cap £1510m: Trading Update: The Board's expectations for the full year remain unchanged. These days BOY is a very small part of Voyager as it has really struggled to please the market whilst making steady if unspectacular progress; probably hold and maybe add if the market takes a liking to BOY again. 28/05/2019: Litigation Capital: LIT: Mkt Cap £116m: Court Approval on Settlement Not much to say really other than I have traded these a couple of times since they came to market and currently hold maybe for a longer term, a position in Voyager, Its not my favourite beast of a business area but does kick off some rather decent financial ratios so let’s see what happens. 29/05/2019: Spectra Systems: SPSY: Mkt Cap: £58m: Trading Update Expects its profits for the year ending 31 December 2019 to exceed market expectations. The increased profits are related to a combination of central bank sensor related research funding and strong first half of the year optical materials sales. My Thoughts: well I did hold SPSY previously but sold as part of my move to cash in mid-2018. I bought back in April so it’s a case of work in progress. 06/06/2019: AB Dynamics: ABDP: Mkt Cap £505m: Result of Oversubscribed Open Offer This follows a very successful placing in May and ABDP now tell us that the open offer was very heavily oversubscribed: no surprise really as this is a quality outfit in a very good place at the moment. I first bought at £4 and will continue to hold/top-up. Rather than words, the following SharePad custom chart shows my attraction to the company:  07/06/2019; Games Workshop: GAW: Mkt Cap £1500m: Trading Update for Year End Games Workshop is pleased to announce that the sales and profit growth, which was discussed in the trading update released on 12 April 2019, has continued in the period to the end of the financial year. Sales growth has been across all sales channels. We expect the Group's sales for the year to 2 June 2019 to be approximately £254 million and the Group's profit before tax to be not less than £80 million. Royalties receivable from licensing are approximately £11 million. My View: once again another cracking performance from GAW which goes from strength to strength. Note the last trading statement on the 12th April stated “The Board's current expectation is that profit before tax for the year ending 2 June 2019 will be c. £80 million”. This trading statement says not less than £80million: happy days. An absolutely quality core company that I am very happy to continue to hold. 07/06/2019: Somero: SOM: Mkt Cap £155m: RNS Trading Update Profits Warning Trading during the five month period to the end of May 2019 has fallen below management's expectations, primarily due to adverse weather conditions in the US, the Company's largest market. Broad sections of the US experienced the highest levels of rainfall on record.* The record rainfall seen in the US has delayed project starts which in turn has slowed the pace of equipment purchased by our customers, the impact of which was seen through historically strong trading months of March and April. Whilst there was an improvement in trading to end the month of May, and although the Company expects weather conditions and therefore trading in the US will improve throughout the rest of 2019, the Board now does not expect the Company to fully recapture the shortfall caused by this extended period of poor weather in the current financial year. As such, the Company now expects to deliver 2019 revenues of approximately US $87m, EBITDA of approximately US $28m, and expects to have net cash at 31 December 2019 of approximately US $18m, after one-off investments of $4.0 million related to building expansions for the Skyscreed ® 25 and the Fort Myers Training Facility as well as the $2.0 million acquisition of Line Dragon. In the Company's other main markets, Europe and China, as well as in the Rest of World territories, trading in 2019 is at comparable levels to 2018, and the Company continues to see opportunities for growth in H2. Growth in India has been steady, as the Company continues to gain traction in the region. The Middle East and Latin America are trading below 2018 levels, however the Company expects improvement in H2 2019, notwithstanding the political uncertainly and economic challenges seen in these regions. The Company is pleased with progress on the new SkyScreed ® 25, having sold the first unit and with continued strong interest in the product. Traction gained so far with the SkyScreed ® 25 is in line with what the Company would expect when bringing a disruptive product of this nature to market. * An average of 36.2 inches of precipitation has fallen over the Lower 48 from May 2018 to April 2019 representing the highest level recorded in over 120 years and six inches over average. *Source: National Oceanic and Atmospheric Administration data My rambling: well not the news I was anticipating and in truth, I did not expect an “ahead of expectations” simply an “in line”. Now, with a profits warning, I usually have a quick think and then commence selling in batches but this one from SOM needed a touch more thought. SOM has always been to my mind a boring but classy/trustworthy outfit. I first bought then at about 100p back in 2014 and they have been very kind to me. I did top slice my position a couple of times over the past two years but due to the positive newsflow was happy to continue to hold the remainder. The original attractions of the 2014 purchase were:

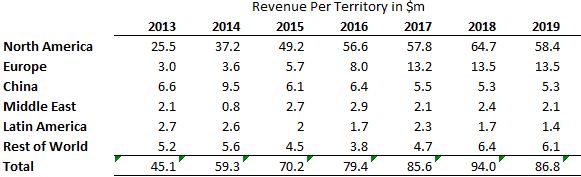

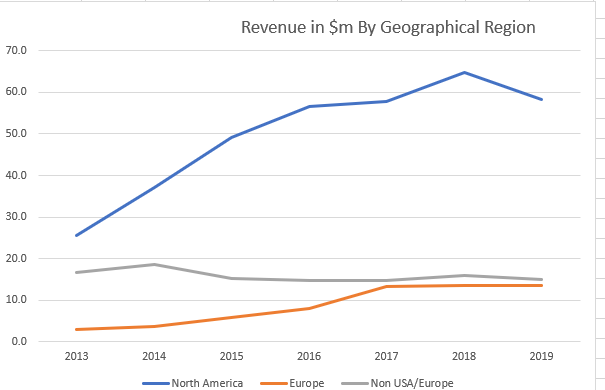

So, what actually did go wrong in 2019? Well, due to the nature of construction work, wet or in this case incredibly wet weather conditions slow down the construction projects and in turn slowed down the demand for Somero products. This is nothing new and happened as recently as 2017 but the weather conditions picked up in time to allow SOM to meet market expectations. However, 2019 rainfall has hit SOM to such an extent that the 2019 expectations have had to be revised downwards as seen in the RNS. It seems to me that the business demand will still be there when dry conditions prevail and that SOM will simply inadvertently bump sales into 2020. Ok, maybe no issue but I suspect that there will be an impact on the hoped-for further growth in 2020 that may have occurred without this rain delay; simply due to overall knock on effect of construction delays with projects being pushed back due to wet conditions. My fag packet calculation after bringing together the sales by geographic region over the last seven years, including the revised position for 2019 (Note regional assumptions based on the text of RNS), shows:   There are a few potholes that SOM has encountered in that whilst North America has been growing well enough, Europe has plateaued to a degree and areas of great promise such as China have proved near impossible to crack. Other potential potholes are of course the cyclical nature of construction which does not worry me too much as you can see this creeping up and weather conditions may possibly raise their head again. So, to my analysis, although Somero is a really good business, it is essentially over these last three years a company comfortably growing revenues within the USA yet at the same time, it is struggling to meaningfully grow its revenue streams outside of the USA and Europe. Note Europe was growing quite well but from 2017 has really levelled off (was that a pun). The graph below simplifies the revenue growth by my classification of revenue streams into the three areas of North America, Europe and non-USA/Europe and demonstrates my non-USA lack of growth concerns over these past three years.  As you can see the growth in revenue for SOM, this past couple or three years is really about North America and hence this hit on revenue and profit for 2019. In truth, this temporary weather issue is not the worrying part as that will pass, of slight concern is the lack of collective growth in recent years outside of the USA. I do believe that if weather conditions had been favourable, then 2019 expectations would have been fairly comfortably met. Yet, as I say, this growth would have been down to the USA as the commentary on other regions in the RNS is not particularly encouraging with regions either trading as in 2018 or the minor areas such as the Middle East & Latin America slipping a touch.  My position is a touch reduced from that bulky one of 2017/18 by top-slicing on a few occasions but it’s still a significant one. So, overall thankfully this profits warning has delivered just a bruise within a reasonably wide portfolio; profits warnings and bruises are simply irritants within this investment game we play.

Whilst I don’t think that SOM is still quite the hidden or undiscovered gem it was back in 2014 or those few following years, it's still a fine business producing some very attractive financial ratios and an excellent dividend. I really expect that with drier USA weather conditions SOM will meet their revised forecasts for 2019. Thereafter moving into 2020 growth hopefully be back on track; yet will it be able to really significantly grow its revenue stream away from the USA? That outside of the USA lack of significant revenue growth is I admit, a touch frustrating. Yet to be fair to SOM, once the USA usage picks up with more normal climate conditions, it should return to being an attractive growing business based on USA sales alone: we also have the temptingly very high dividend. Hopefully, SOM can get Europe & ROW improving in terms of revenues and then, of course, we also have the potential SkyScreed sales which if all goes well, could be a game changer; we shall have to wait and see with that one. Will I be selling, adding or simply holding the position that I have post PW? Well, for now, I will simply hold and just maybe squirrel away a few more as we see how Mr Market reacts over the coming weeks after offering prayer and forgiveness to Zeus the weather God. Somero Summary: Within investing, there are of course no certainties but my feeling is that on the balance of probabilities, that we still have here a high-quality well-managed albeit somewhat cyclical business that based on USA growth alone is worth a place in the Voyager portfolio. If SOM can achieve revenue growth outside the USA and exploit the likely potential of SkyScreed, then the presently reasonably attractive SOM would become an extremely attractive SOM. It’s maybe not the sexy concrete kitten it was in 2014 but still well worth holding this quality company in my view. Note: as ever, this is not advice for a reader to buy or sell but just me sharing my possibly incorrect reading of the current situation with SOM. Any lessons from this profits warning? Well, an oh so obvious one that we SOM followers may have picked up on; simply the news of the awful wet conditions with the heavy rainfall in the USA in the first few months of the year. Fairly obvious when you think about at that construction projects would be delayed; wish I was a touch smarter! Was the sale of £2.7m of shares by the CEO Mr JT Cooney on 28/03/2019 inspired by the sight of a modern-day Noah’s Ark floating past his second-floor window? We can speculate but never really know! If I were attending the AGM which up to 2017 was historically held in London, now back in Florida, I would probe about concrete plans for non-USA revenue growth, will Europe return to growth, can China be cracked etc. I would also ask about progress with sales and enquiries for the new product, SkyScreed. As ever, my appreciation and credit to Sharescope/SharePad; some of their tables are reproduced within this article. At this point, I should say that I have a rather demanding yet pleasurable summer planned with a mix of leisure/holidays and a couple of time demanding projects that I am involved with. The result of this is that it’s quite possible that there may be a gap in Voyager RNS publication until early September. I will just have to see how time goes. I hope all readers have a wonderful summer and wish you all the best in the markets. Happy investing Over recent months I have had a number of requests regarding Voyager holdings and their performance etc. Now I should say and I am sure most readers will know that I take a view of performance based on a minimum of three years; simply miles less stressful and more realistic in terms of investment objectives. In reality, the only true assessment of portfolio performance can be made by the person nominated as executor for your estate once the grim reaper has visited. Of course, by that time it’s too late to write or tweet! Generally, I don’t tend to look at bottom line portfolio progress over small time frames although I do continually review individual performance in order to either root out detractors or add to compelling situations. So, briefly, the following two tables offer a flavour of how performance of firstly long term holdings held over the 3x Financial Year period FY 2016/17 to FY 2018/19 as a cumulative change and then the performance stock by stock during this financial year. The second table considers residents added over the last six months that are still part of Voyager. Note: I always work to the financial year and never a calendar year; done it this way for the last 25 years and it, of course, fits in with the tax year. The selection criteria for Voyager stocks is based upon my favoured criteria to identify stocks with the following characteristics:

PE is never the driver but merely a safety or sanity check: sometimes a stock will have a high PE because of its business success alternatively, others may be chased crazily high just spelling RISK. For a more comprehensive outline of the approach, see my article: Staying Safe on The Planet Aim: The Planet Revisited, published at the end of April 2019. Over the past three financial years, eight of the nine stocks in Table 1 have been resident in the Voyager for all three years and the ninth, GAW, for two of those years. I have included BVXP which I held for around five years but sold at just under £40 in late March 2019. Table 1 Long Term Residents of Voyager  DTG has kept its place in Voyager despite not been stunning over the last three years. It has delivered a four-fold return since purchase in 2013 and with the gradual transformation of the business, there is more to come in my opinion. Note other stocks have had periods of residence in the folio for maybe as much as a year or two or even as little as a couple of months: sales being determined by taking profits on overheating or minimizing loss. I reckon every private investor has to bury their ego and appreciate that their stock selection may not produce significant winners maybe half of the time. The important thing being to weed out the detractors before they can damage the portfolio and keep stepwise adding to the winners when deemed appropriate: it’s invariably the handful of real top performers that greatly influence portfolio success. It does not necessarily mean that a detractor is a bad stock; might just be that momentum and buying volume are not smiling on that stock at the time. Note: a profits warning is a different case and the initial loss on the day is something rather outside of your control. Table 2 below lists stocks that have been added to the Voyager over last 6 months  Note: PMP position building started greater than 6 months ago but for simplicity fits better with Table 2 timeframe.

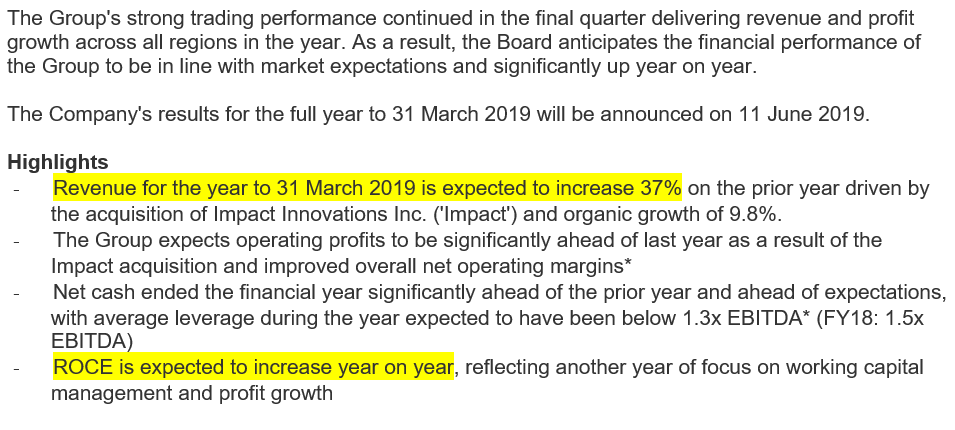

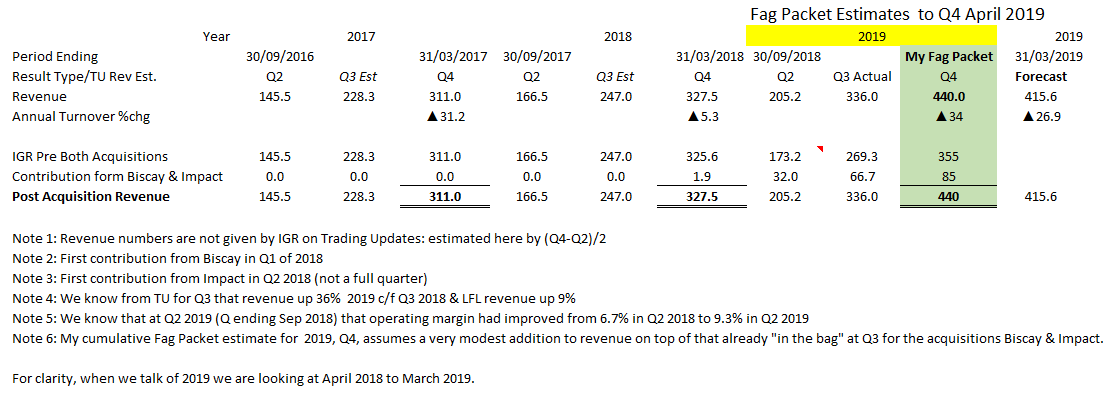

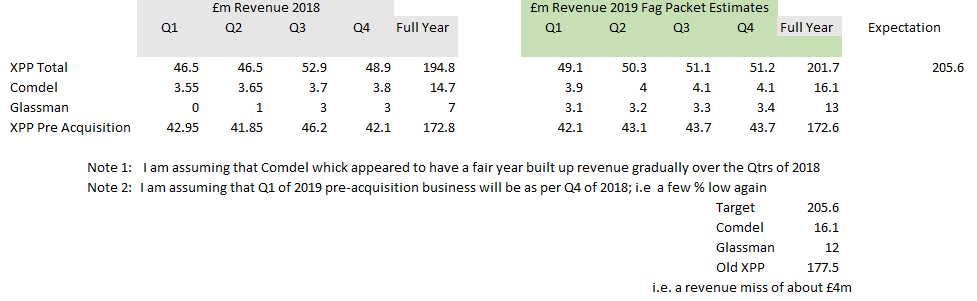

I also operate two other portfolios which are rather dwarfed by the Voyager. These two portfolios are: Firstly a special situations portfolio not based on my usual Voyager criteria but more based on where something is happening to that has in my opinion, a chance of improving the fortunes of the business. This could be something potentially transformational, a potential bid situation, a turnaround situation, neglected/under the radar etc. Simply opportunistic stuff really but it works rather well. Secondly, a high yield portfolio based mainly on what I consider to be quality small companies that offer dividends that are well covered by free cash flow with the added benefit of capital growth via the stocks being reasonably valued. All of the stocks mentioned here have been reviewed in the Voyager since the start of publication of the Voyager Log. As ever, happy investing and remember it’s only money and once you pass the threshold of relative comfort, it ain’t really that important as you are never likely to spend it all. Voyager RNS Log April 2019 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. I have probably bored people to death with my notes on moving rather significantly into cash from Q2/Q3 last year as I observed the storm clouds gathering and that storm eventually broke in the last quarter of 2018. The way the market declined in Q4 of 2018 can be seen from the following two charts of the FTSE-AS & the AIM-100:   Whilst I appreciate that many a fund manager tells us that it’s all about time in the market & not timing the market etc yet in my view, that’s when you are buying and selling really significant percentages of a holding within a company. Within the world of a private investor, we are not restricted so much by the volume of shares we are buying or selling that’s unless we are in a multi-million pound ISA; volume, apart from when dealing in really illiquid stocks, is really on the side of the private investor. Also as I have mentioned many times before, dealing charges are really just not a significant consideration these days as they are so low. So for me, provided that once significantly into cash you a not overly cautious about moving back into the market, then placing some of your capital into safety makes sense when we have such obvious storm clouds looming as we did last summer. In fact, my strategy luckily delivered another very decent financial return for the year 2018/19; I have mentioned before that I don’t operate on a calendar year, the April financial year simply fits in better with my financial/tax-year obligations. So, another financial year has passed and I am happy enough with what 2018/19 has added to the rolling five-year performance. Incidentally, as I discovered years ago with investing, the more I apply myself to my chosen investment pathway, the luckier I get; lesser performance occurs if that pathway is occasionally detoured. I honestly feel that regardless of proven style i.e. an investment style that delivers good results for you and indeed one you are comfortable with, then keep learning, keep improving and success follows. To my mind, this applies to all styles of investing whether it is value investing, momentum investing, growth investing or seeking high-quality companies. Personally, I would not bracket myself into any such investment style but will admit to having a base requirement of what I deem to be quality & momentum for any potential investment; I just reckon I know myself, my strengths and weaknesses and therefore what works well for my personality. Having said that about one’s preferred investment pathway, I honestly feel that many inexperienced private investors damage their wealth prospects by flitting from style to style in a desperate attempt to get the numbers moving in their favour; such horse changing rarely works. It’s best to work to discover what you are good at, comfortable with and stay within that cultural route; note, this is not really new thinking and really the basis behind Jim Slater’s “Zulu Principle”. Incidentally, there is a notable story behind the chosen title of Zulu Principle that Jim selected for his book. During the past two to three months I have been gradually using that cash pile built up last year by adding to current holdings showing positive momentum and also taking up a couple of new positions within the voyager. The Voyager is now somewhere around 70% invested and apart from one slightly speculative stock, the holdings are all ones I classify as really decent quality businesses. In my terms “fully invested” in reality rarely goes over 90-95% as I like to have an available cash buffer to deploy rapidly when I see an attractive situation. Well, let's move on and have a look at recent RNSs that are relevant to shares within the Voyager portfolio. Just for clarity, it’s probably worth describing my approach to what I call core holdings within the Voyager as not all Voyager stocks have earnt this “core holding badge”. A good number of stocks will have real promise to become a core holding but as yet may have some degree of uncertainty about them e.g. within this April Log a couple of potential cores that are still in the apprentice stage KWS & SDI. KWS has bee a Voyager resident since 2016 but suffers shorting attacks & also the risks associated with its highly acquisitive nature. Then we have SDI where I have been building a position for the past five months; small-cap, thinly traded & highly acquisitive. So, three core holdings that are reviewed in this April Voyager are IGR, GAW & ABDP. There are other core holdings and other potentials/apprentices in Voyager but for now, I will just stick to the ones I am writing about in April. I actually visualize the system as a solar system with highly trusted long term hold stocks sitting in the core and orbiting are the apprentices that one day subject to risk diminishing, may well become part of the core.  Voyager Companies with recent RNS: 05/04/2019: Scientific Digital Imaging: SDI: Mkt Cap £50m: RNS Re: Acquisition of MPB MPB designs and manufactures flowmeters and process control instrumentation, with applications in water treatment, oil and gas production, medical anaesthesia, scientific analysis and many other areas. SDI tell us that the acquisition will become earnings enhancing in the FY commencing 01/05/2019. My View: This looks a decent acquisition and at an attractive price of 5x PBIT. Also, it’s good to see that the acquisition at £1.5m has been funded from SDI’s existing cash resources. I do like SDI and have been slowly and painfully building a position from 35p upwards in December 2018. The average price of the position is very reasonable when compared to the current stock price so it’s easily earning it’s keep even though it is a relatively minor fraction of the Voyager. I may add further on a non-RNS pullback. 08/04/2019: Keywords Studios: KWS: Mkt Cap £940m: RNS Final Results:  My View: another very sound set of results for the highly acquisitive KWS. My fear since first buying KWS back in in 2016 for about £3, was really one of fearing how the board of KWS would assimilate the various acquisitions. Well, I guess it’s a case of “fear not” as KWS have done a very good job up to now. It’s worth watching the PI World video produced by the excellent Tamzin were the CEO of KWS, Andrew Day, explains the results and the potential market available to the business. As I have said before in the log, I sold the bulk of my fairly large holding in KWS at prices between £18 & £19 last summer. However, despite the short attacks on this stock, I have been actively rebuilding my position from around the £13 mark. On conventional PE terms, some would say the stock was expensive but I don’t have a lot of time for valuation based on a stand-alone PE test as a worthy measure of valuation. 12/04/2019: Games Workshop: GAW: Mkt Cap£1260m: RNS Trading Update & Dividend Following on from the Group's half year report in January, trading to 7 April 2019 has continued well. Compared to the same period in the prior year, sales and profits are ahead. Royalties receivable are also ahead of the prior year following the signing of new licence agreements. The Board's current expectation is that profit before tax for the year ending 2 June 2019 will be c. £80 million. The Group also announces that the Board has today declared a dividend of 35 pence per share, in line with the Company's policy of distributing truly surplus cash. This will be paid on 31 May 2019 for shareholders on the register at 26 April 2019, with an ex-dividend date of 25 April 2019. The last date for elections for the dividend re-investment plan is 10 May 2019. This dividend will take the total dividend declared and paid during the year ending 2 June 2019 to £1.55 per share. My View: well once again this splendid business delivers the goods and it’s my opinion they will continue to deliver for some considerable time to come. In truth and indeed as I have written in this log before, I was relatively late to buy into the GAW story with my first purchase being at just over £20. Why was I so late? Well, all the financials and ratios looked really good but my inbuilt bias of non-identifying with the draw of the GAW offerings “men playing with strange toys” stopped me from buying in at a much lower price. Still, GAW has been in the Voyager for a while now and following a fair number of top-ups are really earning their profitable place in the Voyager. 15/04/2019: IG Design Group: IGR: Mkt Cap £472m: RNS Trading Update  My View: Once again super progress being made by the well-managed business with the trusty Paul Fineman CEO at the helm. The 2018 revenue was £327.5m and this TU tells us that it will be 37% up in 2019. So to my calculation that gives a figure of £448m which exceeds my January fag packet, see below, where I estimate a conservative £440m: NOTE; as ever, the brokers were slacking as they estimated £416m back in January and even today (day of RNS) only estimate £425m; I’ll take my fag packet any day over the brokers!  The January Fag Packet previously published in this log after the January trading update:  I expect broker upgrades to eventually follow for 2020 as they realise the potential of both IGR organic growth and the exciting contribution from Impact. I will continue to hold and may well top-up further on a pull-back. 15/04/2019: XPP: Mkt Cap £490m: RNS Trading Update Once again I struggle to reconcile the narrative of “The Company has made a good start to the new financial year” & Group revenue for the three months to 31 March 2019 was £46.9 million (2018: £46.6 million), up 1% on Q1 2018 on a reported basis, or 5% below in constant currency. On a “like for like” basis revenue decreased by 12%”. My view is that whilst XPP is a quality company, business is not going anywhere near as well as it was 18 months ago and indeed this trading update for Q1 shows a considerable lower revenue than the pessimistic fag packet I produced back in January 2019; reproduced below:  The Q1 revenue comes in for the group at £46.9 which is a fair bit lower than my bearish estimate above. It suggests to me that XPP who already use the dreaded “H2 weighting” wording will really struggle to meet the £204m revenue expectation (which has been scaled back from the £205.6m revenue originally expected for 2019). I reckon there is a very good chance that there will either be a profits warning as we go through the year or the blushes of a warning will be saved by the gradual erosion of expectations by the brokers. Alternatively, revenue could pick up and XPP may make their numbers for 2019! So, for me, it’s a question of balancing the consideration of continuing to hold this decent business and wait for recovery, after all its reasonably valued at the moment, or selling and moving on. I chose the latter, taking my profits and moving XPP as it gained momentum and placing it back onto the watch list. I may well be back but will keep a close analytical eye on the RNS flow. 17/04/2019: Dart: DTG: Mkt Cap £1.3b: RNS Trading Update Year ended 31 March 2019 (FY19) Due to the continued success of our growing Leisure Travel business, the Board expects Group profit before foreign exchange revaluation & taxation for the year ended 31 March 2019 to be slightly ahead of current market expectations. My View: another long term resident of the Voyager with the original batch purchased for just over £2 back in 2013. DTG has been a very profitable stock as it has developed considerably from the business it was six years ago. I try to get as much feedback as I can from friends and acquaintances who have used jet2.com & jet2holidays and all reports back have been very positive: they are certainly doing a lot right. One thing I would like DTG to do is to consider offloading the Fowler Welch division which just does no longer seem an ideal fit to the current overall business. It’s nice to see the comment “profit slightly ahead of expectations”: it’s not on a demanding rating and has both an ROCE and EBIT margin in excess of 20%. 18/04/2019: D4t4: Mkt Cap £97m Trading Update  My View: nice to hear that progress in terms of profits (adjusted) are to be slightly ahead of expectations: nice and steady and one I may well add further to as D4t4 is doing very well with its Celebrus offering. 24/04/2019: AB Dynamics: ABDP: Mkt Cap £375m: RNS Interim Results  My View: what a splendid set of interims from the excellent ABDP which has been a long term resident of the Voyager since the days of £4. At one time I did sell a few of my ABDP taking some profits but could not resist rebuying the stock and adding more as this quality business continues its success story within their distinctive position in the market. The H1s are really quite outstanding and clearly demonstrate the companies organic growth within the specialist services it supplies to the vehicle industry.

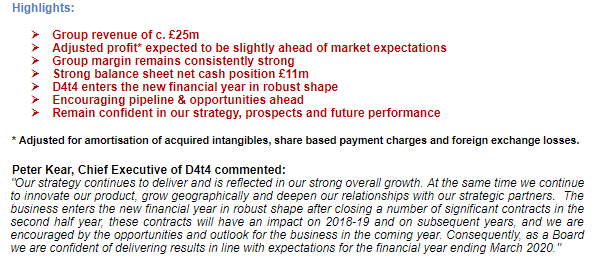

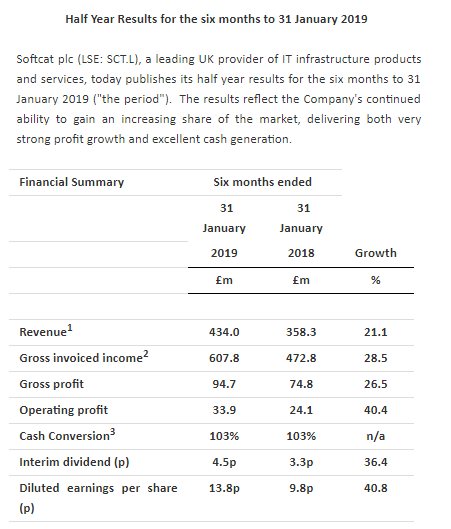

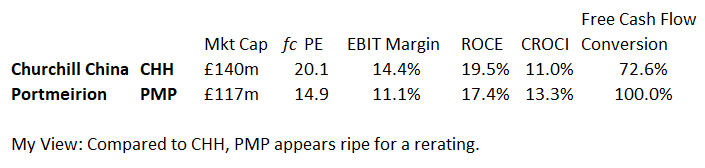

I see that within the narrative of the interims we have the following note on the CFO “As previously reported, Rob Hart has decided to step down from his role as Chief Financial Officer and the Board and will leave ABD in July 2019”. In my view, that’s perfectly fine in terms of the benign & planned departure of a CFO as the business develops under the new CEO Dr James Routh. James Routh incidentally replaced Tim Rogers the previous CEO again in a long term planned way. Tim Rogers was in my mind a fine guy but recognised that a fresh CEO was required to move the group to its next stage of commercial development. I am comfortable with both of these changes as ABDP looks to the next level of successful ordered expansion: you could liken the changes to a football club getting promoted to the next higher league where new possibly stronger skill sets are necessary to ensure progression of the unit. As ever, I used by fag packet calculation; maybe it's rough and crude but it’s my trusty fag packet and seems to be a fair bit more reliable and accurate than the eBay sourced abacus that the lazy brokers play with. Oh, why not, let’s have a rant: I really reckon some of the brokers have simply coined in the cash for the most modest effort; if they were just to analyse the data companies offer the market, then they would be in a far more informed place. So, rant over, let's have a look at the fag packet based on these interims: Over the last two years, the H1/H2 stretch has been about H2 = H1 x 2.3. Taking the 2019 H1 x 2.3 gives revenue for the full year of £59.3m but let's be conservative and say the sale of the next aVDS yield revenue into H1 of 2020, so reduce this £59.3m to say £57m. Can I be confident in this “fag packet”? Well yes, I feel I can as the narrative tells us in the outlook statement “The second half of the financial year has started positively, and our order book visibility gives the Board confidence in the outlook for ABD for the remainder of 2019 and beyond”. So in my view, I expect ABDP to be more than 10% ahead of current market estimates for the full year. Abacus at the ready for Mr Broker to deliver upgrades I reckon. Personally, I will be adding to my holding on any slight pullback as I see ABDP as a high-quality growth business that's in a special place and certainly a business I want to hold for a long time. A few general small, cap (sub £50m) thoughts: I have been taking some positions in stocks of small market cap, less than £50m, over the last six months. Initially, a starter position and then gradual build as the stocks show momentum. This is a slight departure from my normal approach of having no more that one or at most two stocks in the portfolio of less than £50m capitalisation: simply a question of bumps in the road and liquidity. I have often pondered with letting an Investment Trust offer me a basket of decent quality sub £50m cap stocks and to that length have kept tabs on the two Downing Micro Cap Its but their performance has been rather poor of late. So, the conclusion that I will be very selective and manage my own handful of sub £50m cap stocks. Two were added to the Voyager & two others also added to the high yield portfolio within the FY18/19; Note, I don’t usually write about the HY folio in this log. I may well pen something shortly to cover the high yield folio although its all fairly boring stuff based on FCF dividend cover etc. The two sub £50m stocks in the Voyager are of course SDI and ARC. Well, that’s all for now; I hope you all have a very pleasant weekend and as ever, happy investing! Voyager RNS Log 10/03/19 to 29/03/2019 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Although I have been putting some money back into the markets from that hefty cash pile I partially retreated to in the summer of 2018, by the end of September it had reached about 70% cash, presently I am a touch more of a trading animal rather than a longer-term investor due to our political climate with the dreaded B word. That approach will no doubt change as time progresses and we come through this silly European episode. Until the dust settles I intend to take what risk-weighted opportunities I can as long as those opportunities suggest a good chance of adding to the bottom line. Investing is about making money and not simply showing steadfast loyalty to one of your chosen holdings. On reflection, I am very happy that I took that cautious approach as the storm clouds gathered and I, fortunately, was not greatly affected by the turmoil of October to December 2018. As described in the Voyager before, my approach is to seek stocks from the 2200+ that reside in the LSE that meet my prescribed quality criteria; this yields about 150 or so stocks that merit further investigation. In addition over the coming months I will pay particular attention to attractive momentum stocks that may or may not be derived from my universe of 150 or thereabouts stocks a recent example was the trades in GRG, KNOS and EZJ; two went very well for a very handy short term profit and the other sold for a small loss but overall the bottom line of the portfolio benefited nicely. I don’t let the worry of dealing fees lock me into a stock as after all, such charges are incredibly low these days. Therefore, I am happy to move in and out of a stock and once sold, if the stock then looks attractive, I simply reenter: as ever, it’s the bottom line that counts. Turning to price movements in previously held stocks, I am really glad that I decided back in July 2018 that Bonmarch was not delivering the turn-around I was looking for and sold for a handy profit. Since that sale at 110p, BON has issued two profits warnings and now sits at 20p: be cold, be ruthless, don’t have blind loyalty to a stock as it’s incapable of returning that affection. Let’s turn to RNSs for Voyager stocks issued in the last couple of weeks: Wednesday 13/03/2019: Somero: SOM: Mkt Cap: £218m: RNS Final Results Financial Highlight  Outlook: The Board believes the Company has numerous meaningful growth opportunities in 2019 across its broad portfolio of markets and products that is supported by positive non-residential construction market conditions and reinforced by customers reporting project backlogs that extend beyond 2019. Based on this positive environment and the momentum of the business, the Board is confident that Somero is poised to deliver another year of profitable growth to shareholders in 2019. My View: well another set of excellent results from Somero with a steady increase in turnover by 10%, PBT up by 13% and adjusted EPS increased by some 23%. In addition, the cash position at SOM looks very healthy and supports a special dividend to be paid to shareholders. Looking forward we have the new SkyScreed product designed for use with high rise building, so, hopefully, another income stream to be brought online as the year's progress. It seems that I am repeating myself yet again with SOM but this is a high-quality company that I have happily held in the Voyager since October 2014 and I am again happy to hold plus add when price action invites a top up. Note: I do read some commentary about SOM being a cyclical business and indeed many businesses are cyclical to an extent. My argument is simply “well so what, you don’t fall in love with a stock and once it goes into decline you have the sell button”. How do you know when it’s going into decline? Well fairly easy really, you read the RNS flow and take note of the share price graph. Tuesday 19/03/2019: Softcat: SCT: Mkt Cap £1.7b: RNS Half Year Results  Outlook The Board expects a full year outcome marginally ahead of previous expectations. My View: well as signalled earlier in the Trading Update of 09/01/2019, the interims were likely to be very decent and that exactly what we were treated to with revenue up by 21% and operating profit up by 40%. I do have a touch of history with SCT having purchased in May of last year and then selling, almost at its all-time high, at the end of August, The stock price of SCT then declined by about 35% before again swinging north aided by the excellent trading update in early January this year. I will hold for the moment but with the current political climate, I am mindful that unless I have a really high conviction for a stock, when it’s momentum turns profits will be taken and targets reassessed. Thursday 21/03/2019: Portmeirion: PMP: Mkt Cap £116m: RNS Final Results  Outlook Firstly the usual Brexit notes; becoming boring but all companies do it! Although we face political and economic uncertainties around the world, including Brexit, we look forward into 2019 with confidence and at this very early stage of the year expect trading to be in line with expectations for the full year. My View: readers will know that I really like the financials of PMP, the very underpromising way that they communicate progress and the overall quality of the business. What do I like? Well, lets first look at the years of continuous growth: that’s 10 years of very decent revenue growth & EBIT growth. Then we have the significant and well-performing acquisition Wax Lyrical that continues to boost sales. Then we can chuck in the rapidly growing but still infant online sales offering which grew by 25% adding contributing £4.3m to the £89m revenue for the year. So, now a quick look at the financial numbers and ratios: 18% ROCE, 13% CROCI (both lease adjusted), 89% FCF conversion, no debt, year on year gradual increase of EBIT margin to 11.2%, dividend well covered by FCF. All in all, a very tidy business. In fact, back in January, I did in this log do a comparison of PMP with the higher rated Churchill China suggesting that PMP was somewhat undervalued compared to it’s Stoke neighbour; I still feel that and rather expect it to make up that 30%-40% in the coming year or two. I am happy to continue to hold. 26/03/2109: D4t4: Mkt Cap £108m: RNS Contract Wins  My View: I have been with D4t4 at times taking profits and at other times topping up, since 2016 buying at prices ranging from 125p to 220p. In fact with the market wobble in late 2018, I completely exited D4t4 in November yet returned again in early February 2019. These contract wins certainly appear to have excited the market and the share price has appreciated nicely. My thought is that with this Celebrus offering D4t4 will continue to prosper. As ever, it’s a relatively small business and there could be bumps in the road but I am very happy to hold and will consider adding further.

27/03/2019: AB Dynamics: ABDP: Mkt Cap: RNS Trading Update My View: An in-line trading statement and nothing to get overly excited about given the fact that ABDP share price has actually doubled in this financial year. Once again, I felt that the price had got a little ahead of itself and did peak lop some at close to £18; first entry bought at £4 back in the summer of 2016. A nice company that once again has some cracking good financial numbers that attract me: 24% ROCE, 16% CROCI, 21% EBIT Margin & no debt. It’s got a touch expensive hence my peak lopping but I feel I may top up again on further positive newsflow/more attractive price. Stocks Welcomed Aboard Voyager & Those Jettisoned in the last three weeks: New positions: 4imprint Group: FOUR: following a decent set of finals early in March: decent increase in turnover, EBIT and a lease adjusted ROCE in the ’60s, good FCF conversion, no debt. I normally like a higher EBIT margin but this company has a good solid track record. Note to myself; Come on Whittler, wake up you sleepy idiot, you have been watching these for how many years? One most unlikely one for me as I am utterly useless with holes in the ground and certainly even more useless with holes in the sea, but the momentum of Hurricane Energy: HUR encouraged me to take an initial position; will it all end in tears? One on the nearly watch list: where I did open and close spread bet position ahead of a potential significant ISA purchase: D S Smith: SMDS: we are in my view, reaching a transformational state for SMDS having announced the agreed sale of its plastics division, therefore, shedding the “toxic plastic taint”. The funds from the sale of the plastics division to Olympus for £450m will be used to reduce the debt at the SMDS which removes a slight obstacle; I don’t like masses of debt. Anyway, the initial little touch failed so it's back on the serious watch list. Stocks sold: Greggs: GRG for an 18% return in 10 weeks: I may well go back in shortly. Kanios: KNOS sold for a handy 8% profit; yes, I know it’s a tough market at the moment but at least it keeps the bottom line ticking over. Easyjet: EZJ: for a 4% loss in 6 weeks Finally, one stock that left the Voyager in mid-March 2019 having been a resident for these past five years: Bioventix: BVXP: the stock has had a fairly exhausting climb over the last seven weeks with the stock price appreciating by some 25% to hit the £40 mark. Now whilst BVXP has been a fabulously rewarding stock for me since my entry point at £7 back in 2014 and has many of the characteristics I look for in an investment, at £40, to my mind it had become a touch overheated fanned by the flames of expectation over its troponin antibodies. With all of this in mind and despite the fact that I have really enjoyed a fabulous rise from £7 to £40, I sold my entire holding in BVXP at prices between £39.50 & £40: simply time to take a profit and sit on the fence for a little while. I believe BVXP is a really top-notch outfit with the stunning financial numbers I crave for in a stock but the valuation had become a touch overstretched in my view. My philosophy is to always manage risk and after that recent 25% rise, it simply seemed sound to bank some profits. As ever when I exit a share, that exit may possibly only be temporary: I will keep an eye on RNS newsflow and share price action with a real possibility of taking another position in BVXP at hopefully a more attractive price. The interim results released on 29/03/2019 look rather as expected, so, for now it goes back on that active watch list. On the non-markets front, I am rekindling my passion for making sourdough bread and the first batch with the new sourdough starter I have produced should be ready today: happy days! At the weekend it’s off to Bristol for the Hatters game against Bristol Rovers: will we be able to get back to back promotions and return to the Championship I wonder? Whatever you are doing, have a great weekend and happy investing! Voyager RNS Log at WC 03/03/2019 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Just back from a lovely winter break in India visiting the various major sites; can’t decide quite what was the most outstanding so, a close run thing between the Ganges religious ceremony after sunset, Taj Mahal and the fantastic Golden Temple especially at night. Anyway, as is my usual practice these days, I simply put on a few stop-losses and don’t even look at SharePad during my trips away; sort of fits in well with my laidback lifestyle I guess. Unless I am hit with a profits warning, then a month is merely a blip in time compared to my normal time horizon for measuring returns which is 3 to 5 years. Interestingly I get into conversation with lots of people on my travels and the subject of investment returns occasionally comes up. On this trip I had lunch with an investor who figured that a 7% return per year was outstanding; as casually as I could, I explained to her that I would be mightily disappointed with that over my timeframe: the look of shock was worth a photo! Over the years I have learnt that the more selective, critical and disciplined in terms of risk management I become, the luckier I get to be in my investment returns. I can’t think of the last time I read any journalists recommendations on stocks to buy although about a year ago I did backtrack the investment success of one very widely followed financial journalist; safe to say it was not that impressive and that’s maybe the reason why the journalist earns his living from writing rather than full time investing. As for me, I am most definitely not a pack animal when it comes to investing, in fact, when I see the enthusiasm or the pack especially for the “next big thing”, I tend to switch off right away. Honestly, I am not meaning to be arrogant; simply been there, done that and have the shallow yet healed scars to remind me of such folly. These days a private investor can really prosper provided they have real discipline once they find and develop an investment style that suits their personality and allows them to sleep at night. My simple nuggets on my investment approach:- Refine the 2000+ of LSE shares down to a number of quality shares. How do you define quality? Well for me its: