|

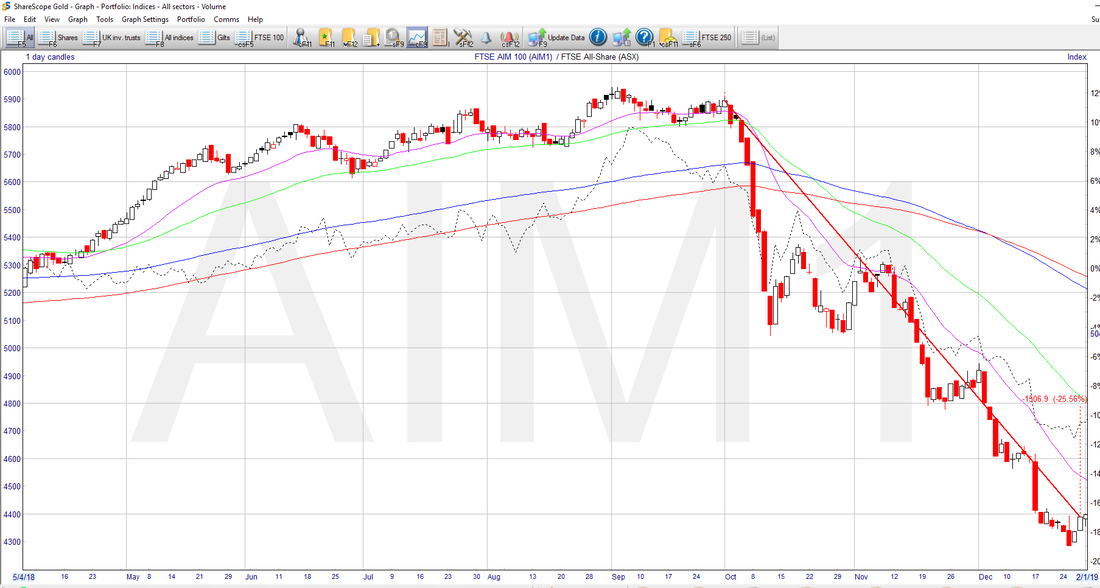

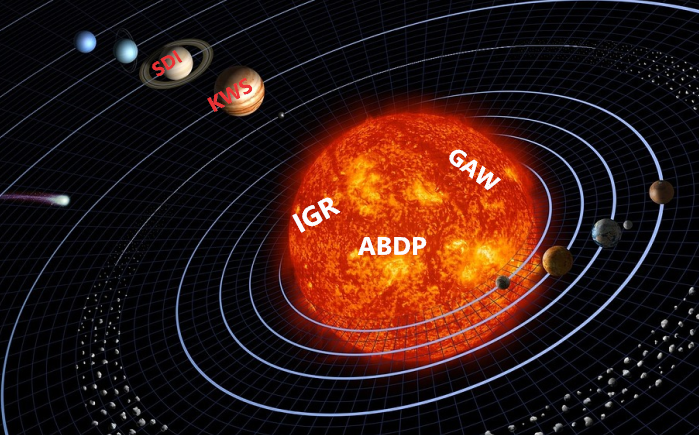

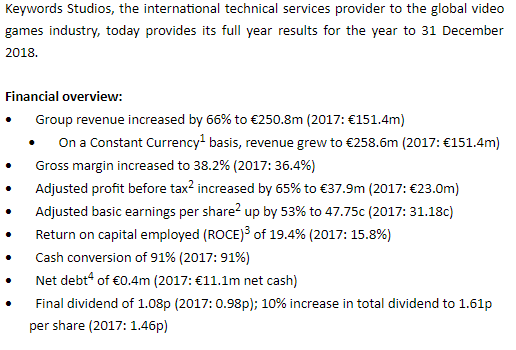

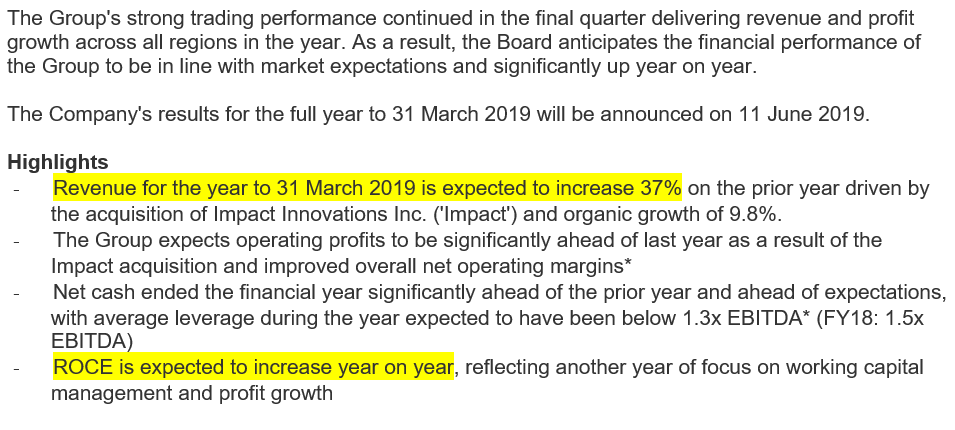

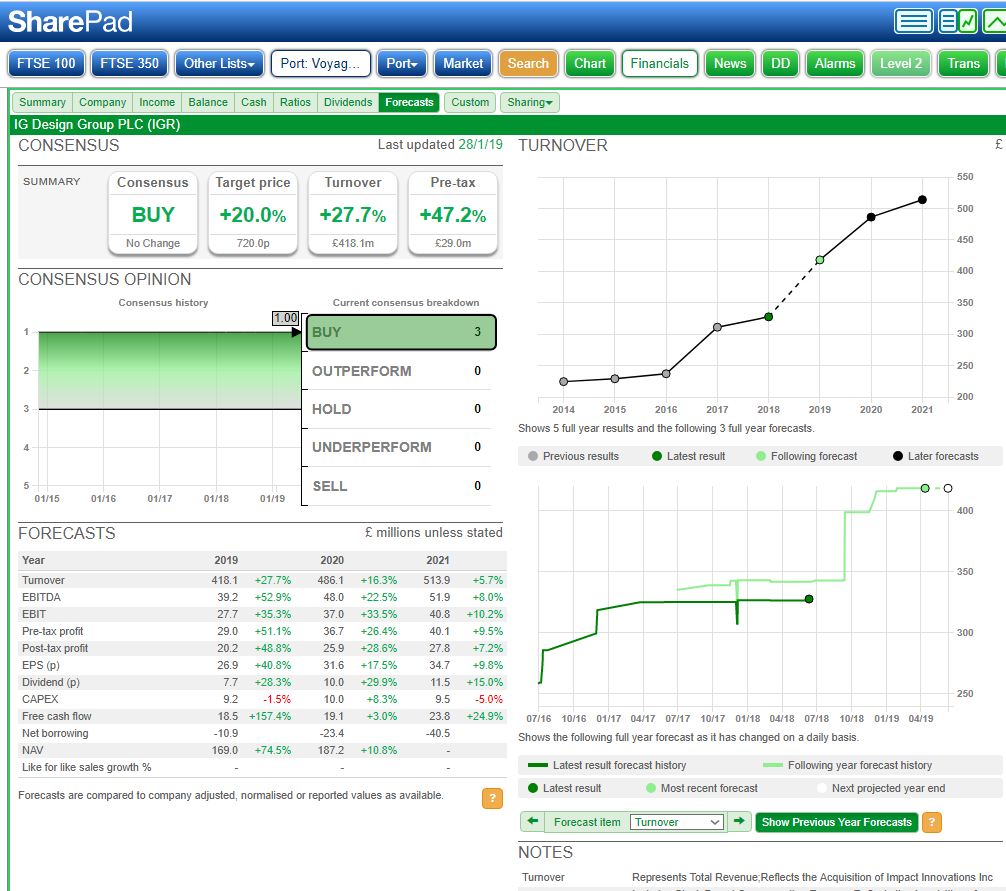

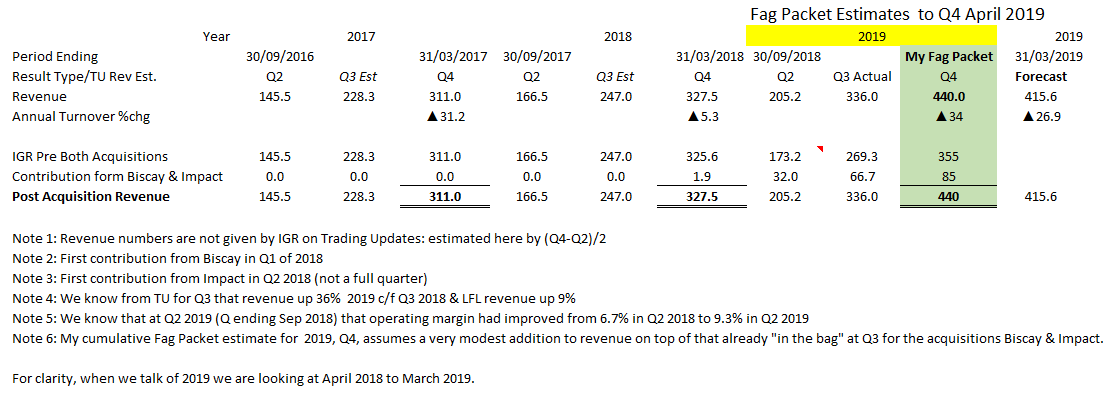

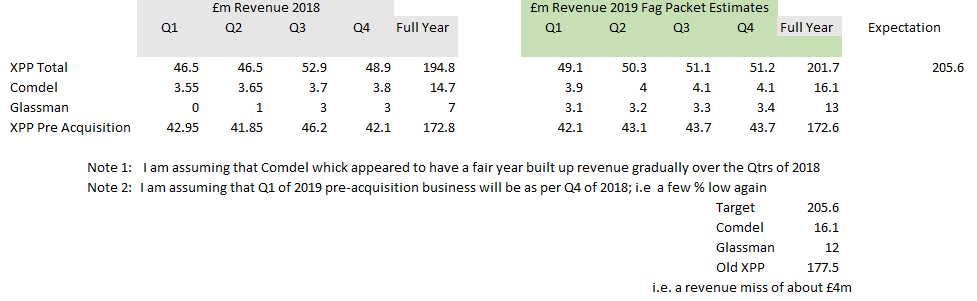

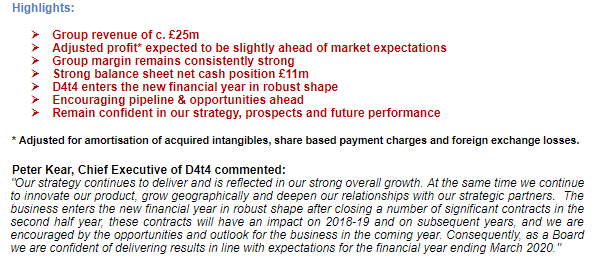

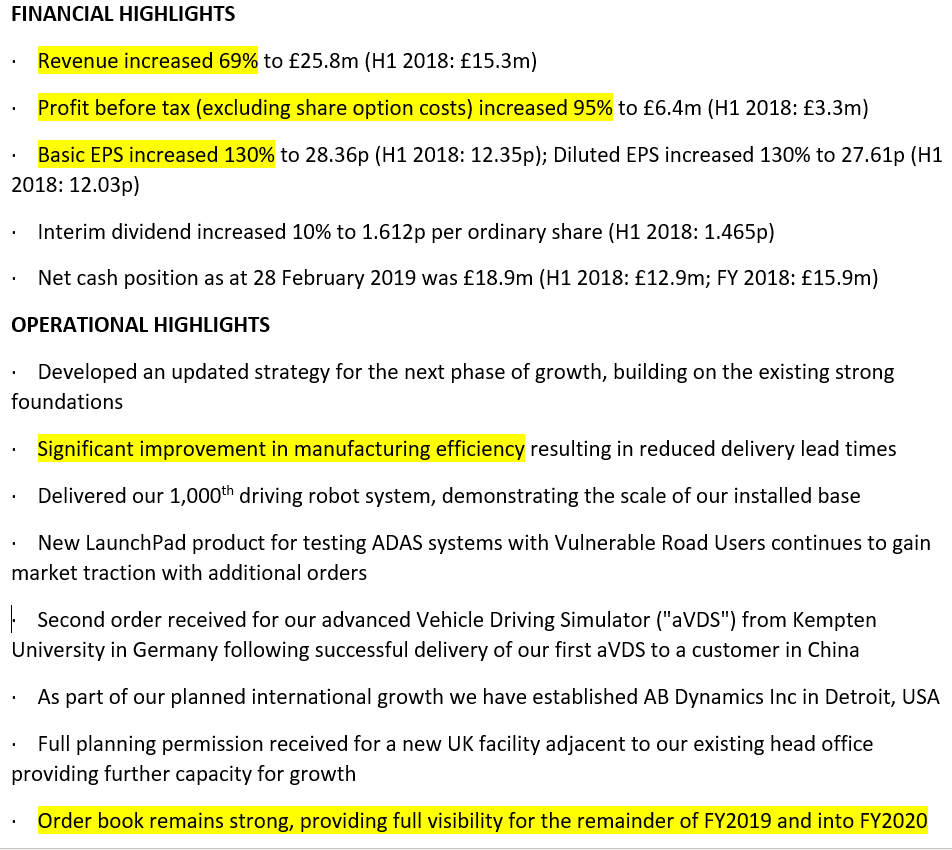

Voyager RNS Log April 2019 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. I have probably bored people to death with my notes on moving rather significantly into cash from Q2/Q3 last year as I observed the storm clouds gathering and that storm eventually broke in the last quarter of 2018. The way the market declined in Q4 of 2018 can be seen from the following two charts of the FTSE-AS & the AIM-100:   Whilst I appreciate that many a fund manager tells us that it’s all about time in the market & not timing the market etc yet in my view, that’s when you are buying and selling really significant percentages of a holding within a company. Within the world of a private investor, we are not restricted so much by the volume of shares we are buying or selling that’s unless we are in a multi-million pound ISA; volume, apart from when dealing in really illiquid stocks, is really on the side of the private investor. Also as I have mentioned many times before, dealing charges are really just not a significant consideration these days as they are so low. So for me, provided that once significantly into cash you a not overly cautious about moving back into the market, then placing some of your capital into safety makes sense when we have such obvious storm clouds looming as we did last summer. In fact, my strategy luckily delivered another very decent financial return for the year 2018/19; I have mentioned before that I don’t operate on a calendar year, the April financial year simply fits in better with my financial/tax-year obligations. So, another financial year has passed and I am happy enough with what 2018/19 has added to the rolling five-year performance. Incidentally, as I discovered years ago with investing, the more I apply myself to my chosen investment pathway, the luckier I get; lesser performance occurs if that pathway is occasionally detoured. I honestly feel that regardless of proven style i.e. an investment style that delivers good results for you and indeed one you are comfortable with, then keep learning, keep improving and success follows. To my mind, this applies to all styles of investing whether it is value investing, momentum investing, growth investing or seeking high-quality companies. Personally, I would not bracket myself into any such investment style but will admit to having a base requirement of what I deem to be quality & momentum for any potential investment; I just reckon I know myself, my strengths and weaknesses and therefore what works well for my personality. Having said that about one’s preferred investment pathway, I honestly feel that many inexperienced private investors damage their wealth prospects by flitting from style to style in a desperate attempt to get the numbers moving in their favour; such horse changing rarely works. It’s best to work to discover what you are good at, comfortable with and stay within that cultural route; note, this is not really new thinking and really the basis behind Jim Slater’s “Zulu Principle”. Incidentally, there is a notable story behind the chosen title of Zulu Principle that Jim selected for his book. During the past two to three months I have been gradually using that cash pile built up last year by adding to current holdings showing positive momentum and also taking up a couple of new positions within the voyager. The Voyager is now somewhere around 70% invested and apart from one slightly speculative stock, the holdings are all ones I classify as really decent quality businesses. In my terms “fully invested” in reality rarely goes over 90-95% as I like to have an available cash buffer to deploy rapidly when I see an attractive situation. Well, let's move on and have a look at recent RNSs that are relevant to shares within the Voyager portfolio. Just for clarity, it’s probably worth describing my approach to what I call core holdings within the Voyager as not all Voyager stocks have earnt this “core holding badge”. A good number of stocks will have real promise to become a core holding but as yet may have some degree of uncertainty about them e.g. within this April Log a couple of potential cores that are still in the apprentice stage KWS & SDI. KWS has bee a Voyager resident since 2016 but suffers shorting attacks & also the risks associated with its highly acquisitive nature. Then we have SDI where I have been building a position for the past five months; small-cap, thinly traded & highly acquisitive. So, three core holdings that are reviewed in this April Voyager are IGR, GAW & ABDP. There are other core holdings and other potentials/apprentices in Voyager but for now, I will just stick to the ones I am writing about in April. I actually visualize the system as a solar system with highly trusted long term hold stocks sitting in the core and orbiting are the apprentices that one day subject to risk diminishing, may well become part of the core.  Voyager Companies with recent RNS: 05/04/2019: Scientific Digital Imaging: SDI: Mkt Cap £50m: RNS Re: Acquisition of MPB MPB designs and manufactures flowmeters and process control instrumentation, with applications in water treatment, oil and gas production, medical anaesthesia, scientific analysis and many other areas. SDI tell us that the acquisition will become earnings enhancing in the FY commencing 01/05/2019. My View: This looks a decent acquisition and at an attractive price of 5x PBIT. Also, it’s good to see that the acquisition at £1.5m has been funded from SDI’s existing cash resources. I do like SDI and have been slowly and painfully building a position from 35p upwards in December 2018. The average price of the position is very reasonable when compared to the current stock price so it’s easily earning it’s keep even though it is a relatively minor fraction of the Voyager. I may add further on a non-RNS pullback. 08/04/2019: Keywords Studios: KWS: Mkt Cap £940m: RNS Final Results:  My View: another very sound set of results for the highly acquisitive KWS. My fear since first buying KWS back in in 2016 for about £3, was really one of fearing how the board of KWS would assimilate the various acquisitions. Well, I guess it’s a case of “fear not” as KWS have done a very good job up to now. It’s worth watching the PI World video produced by the excellent Tamzin were the CEO of KWS, Andrew Day, explains the results and the potential market available to the business. As I have said before in the log, I sold the bulk of my fairly large holding in KWS at prices between £18 & £19 last summer. However, despite the short attacks on this stock, I have been actively rebuilding my position from around the £13 mark. On conventional PE terms, some would say the stock was expensive but I don’t have a lot of time for valuation based on a stand-alone PE test as a worthy measure of valuation. 12/04/2019: Games Workshop: GAW: Mkt Cap£1260m: RNS Trading Update & Dividend Following on from the Group's half year report in January, trading to 7 April 2019 has continued well. Compared to the same period in the prior year, sales and profits are ahead. Royalties receivable are also ahead of the prior year following the signing of new licence agreements. The Board's current expectation is that profit before tax for the year ending 2 June 2019 will be c. £80 million. The Group also announces that the Board has today declared a dividend of 35 pence per share, in line with the Company's policy of distributing truly surplus cash. This will be paid on 31 May 2019 for shareholders on the register at 26 April 2019, with an ex-dividend date of 25 April 2019. The last date for elections for the dividend re-investment plan is 10 May 2019. This dividend will take the total dividend declared and paid during the year ending 2 June 2019 to £1.55 per share. My View: well once again this splendid business delivers the goods and it’s my opinion they will continue to deliver for some considerable time to come. In truth and indeed as I have written in this log before, I was relatively late to buy into the GAW story with my first purchase being at just over £20. Why was I so late? Well, all the financials and ratios looked really good but my inbuilt bias of non-identifying with the draw of the GAW offerings “men playing with strange toys” stopped me from buying in at a much lower price. Still, GAW has been in the Voyager for a while now and following a fair number of top-ups are really earning their profitable place in the Voyager. 15/04/2019: IG Design Group: IGR: Mkt Cap £472m: RNS Trading Update  My View: Once again super progress being made by the well-managed business with the trusty Paul Fineman CEO at the helm. The 2018 revenue was £327.5m and this TU tells us that it will be 37% up in 2019. So to my calculation that gives a figure of £448m which exceeds my January fag packet, see below, where I estimate a conservative £440m: NOTE; as ever, the brokers were slacking as they estimated £416m back in January and even today (day of RNS) only estimate £425m; I’ll take my fag packet any day over the brokers!  The January Fag Packet previously published in this log after the January trading update:  I expect broker upgrades to eventually follow for 2020 as they realise the potential of both IGR organic growth and the exciting contribution from Impact. I will continue to hold and may well top-up further on a pull-back. 15/04/2019: XPP: Mkt Cap £490m: RNS Trading Update Once again I struggle to reconcile the narrative of “The Company has made a good start to the new financial year” & Group revenue for the three months to 31 March 2019 was £46.9 million (2018: £46.6 million), up 1% on Q1 2018 on a reported basis, or 5% below in constant currency. On a “like for like” basis revenue decreased by 12%”. My view is that whilst XPP is a quality company, business is not going anywhere near as well as it was 18 months ago and indeed this trading update for Q1 shows a considerable lower revenue than the pessimistic fag packet I produced back in January 2019; reproduced below:  The Q1 revenue comes in for the group at £46.9 which is a fair bit lower than my bearish estimate above. It suggests to me that XPP who already use the dreaded “H2 weighting” wording will really struggle to meet the £204m revenue expectation (which has been scaled back from the £205.6m revenue originally expected for 2019). I reckon there is a very good chance that there will either be a profits warning as we go through the year or the blushes of a warning will be saved by the gradual erosion of expectations by the brokers. Alternatively, revenue could pick up and XPP may make their numbers for 2019! So, for me, it’s a question of balancing the consideration of continuing to hold this decent business and wait for recovery, after all its reasonably valued at the moment, or selling and moving on. I chose the latter, taking my profits and moving XPP as it gained momentum and placing it back onto the watch list. I may well be back but will keep a close analytical eye on the RNS flow. 17/04/2019: Dart: DTG: Mkt Cap £1.3b: RNS Trading Update Year ended 31 March 2019 (FY19) Due to the continued success of our growing Leisure Travel business, the Board expects Group profit before foreign exchange revaluation & taxation for the year ended 31 March 2019 to be slightly ahead of current market expectations. My View: another long term resident of the Voyager with the original batch purchased for just over £2 back in 2013. DTG has been a very profitable stock as it has developed considerably from the business it was six years ago. I try to get as much feedback as I can from friends and acquaintances who have used jet2.com & jet2holidays and all reports back have been very positive: they are certainly doing a lot right. One thing I would like DTG to do is to consider offloading the Fowler Welch division which just does no longer seem an ideal fit to the current overall business. It’s nice to see the comment “profit slightly ahead of expectations”: it’s not on a demanding rating and has both an ROCE and EBIT margin in excess of 20%. 18/04/2019: D4t4: Mkt Cap £97m Trading Update  My View: nice to hear that progress in terms of profits (adjusted) are to be slightly ahead of expectations: nice and steady and one I may well add further to as D4t4 is doing very well with its Celebrus offering. 24/04/2019: AB Dynamics: ABDP: Mkt Cap £375m: RNS Interim Results  My View: what a splendid set of interims from the excellent ABDP which has been a long term resident of the Voyager since the days of £4. At one time I did sell a few of my ABDP taking some profits but could not resist rebuying the stock and adding more as this quality business continues its success story within their distinctive position in the market. The H1s are really quite outstanding and clearly demonstrate the companies organic growth within the specialist services it supplies to the vehicle industry.

I see that within the narrative of the interims we have the following note on the CFO “As previously reported, Rob Hart has decided to step down from his role as Chief Financial Officer and the Board and will leave ABD in July 2019”. In my view, that’s perfectly fine in terms of the benign & planned departure of a CFO as the business develops under the new CEO Dr James Routh. James Routh incidentally replaced Tim Rogers the previous CEO again in a long term planned way. Tim Rogers was in my mind a fine guy but recognised that a fresh CEO was required to move the group to its next stage of commercial development. I am comfortable with both of these changes as ABDP looks to the next level of successful ordered expansion: you could liken the changes to a football club getting promoted to the next higher league where new possibly stronger skill sets are necessary to ensure progression of the unit. As ever, I used by fag packet calculation; maybe it's rough and crude but it’s my trusty fag packet and seems to be a fair bit more reliable and accurate than the eBay sourced abacus that the lazy brokers play with. Oh, why not, let’s have a rant: I really reckon some of the brokers have simply coined in the cash for the most modest effort; if they were just to analyse the data companies offer the market, then they would be in a far more informed place. So, rant over, let's have a look at the fag packet based on these interims: Over the last two years, the H1/H2 stretch has been about H2 = H1 x 2.3. Taking the 2019 H1 x 2.3 gives revenue for the full year of £59.3m but let's be conservative and say the sale of the next aVDS yield revenue into H1 of 2020, so reduce this £59.3m to say £57m. Can I be confident in this “fag packet”? Well yes, I feel I can as the narrative tells us in the outlook statement “The second half of the financial year has started positively, and our order book visibility gives the Board confidence in the outlook for ABD for the remainder of 2019 and beyond”. So in my view, I expect ABDP to be more than 10% ahead of current market estimates for the full year. Abacus at the ready for Mr Broker to deliver upgrades I reckon. Personally, I will be adding to my holding on any slight pullback as I see ABDP as a high-quality growth business that's in a special place and certainly a business I want to hold for a long time. A few general small, cap (sub £50m) thoughts: I have been taking some positions in stocks of small market cap, less than £50m, over the last six months. Initially, a starter position and then gradual build as the stocks show momentum. This is a slight departure from my normal approach of having no more that one or at most two stocks in the portfolio of less than £50m capitalisation: simply a question of bumps in the road and liquidity. I have often pondered with letting an Investment Trust offer me a basket of decent quality sub £50m cap stocks and to that length have kept tabs on the two Downing Micro Cap Its but their performance has been rather poor of late. So, the conclusion that I will be very selective and manage my own handful of sub £50m cap stocks. Two were added to the Voyager & two others also added to the high yield portfolio within the FY18/19; Note, I don’t usually write about the HY folio in this log. I may well pen something shortly to cover the high yield folio although its all fairly boring stuff based on FCF dividend cover etc. The two sub £50m stocks in the Voyager are of course SDI and ARC. Well, that’s all for now; I hope you all have a very pleasant weekend and as ever, happy investing!

1 Comment

Andrea34l

5/1/2019 02:32:48 am

A very interesting read. Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed