|

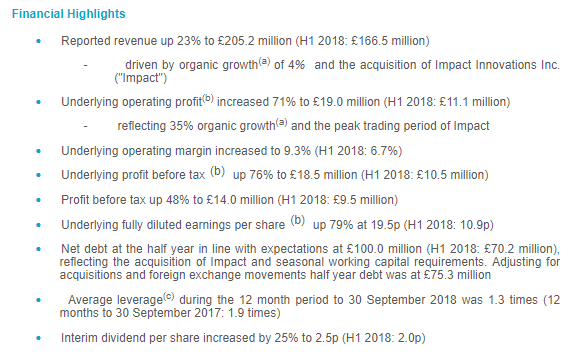

Voyager RNS Log at 14th December 2018, As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Firstly a quick refresh in terms of what was for the last couple of years, an almost weekly Voyager Log looking in some detail at RNSs relevant to Voyager holdings. Due to the sustained profit taking, I have implemented in my plan in 2018 the portfolio became greatly reduced both in terms of holdings and indeed the financial exposure for each retained investment in the portfolio: most have been cut back significantly. So, with that in mind, there has been little to write about: indeed, I have to say that I am enjoying my little break from the markets as we go through this current yet very predictable turmoil. A Few Thoughts On The Current State Of The Markets In The UK: Well, maybe it’s best to reiterate some of the words I used in the last Voyager Log: I just do not get fazed by such periods as I have simply been investing too long I guess; I have the scars and hopefully, the bolted on wisdom having invested through the bear markets of 2001 & 2008 which taught me the value of moving heavily into cash. Having been through some tough periods in the past, I feel that’s its imperative that an investor has a plan, a strategy and when they see the cliff face looming they at least consider executing that plan rather than waiting until their toes are dangling over the cliff and acting in panic mode. So, all in all, my move to take profits and stockpile cash started earlier in the year and whilst the current state of the market has diminished the value of my residual holdings, the overall effect on the performance of the portfolio has been greatly mitigated by the cash balance in the portfolio. So, where are the markets going? Well, I don’t know for sure but currently, I feel there is just too much risk for my comfort. Indeed, I think there is a real risk that we could continue to drift lower during the first quarter of 2019.  Looking back at some of the price action on the stocks that have exited the portfolio during 2018 and the reasons for those exits, we have: Stocks sold following my “Fag Packet” calculations on prospects after reading an RNS: OTB: sold for a >50% profit: Reason for sale my serious doubts about H1/H2 stretch being achievable. Since that sale, OTB has fallen by -35% & forecasts reduced which dodged them issuing a profits warning in my view. AMO: sold for >50% profit: Reason for sale my serious doubts about H1/H2 stretch being achievable. Since that sale, AMO has fallen -40% & issued a profits warning. BON: sold for >25% profit: Reason for sale based on my estimates the turn around was less likely to happen. Since that sale, BON has issued a couple of profits warnings and fallen by over -50%. TSTL: sold for an average profit of >100%. Reason for the sale was that according to my fag packet if you subtract share-based payments trousered by the directors, the profits were looking just marginally better than static. Since that sale, TSTL has fallen -15%. I would not consider reinvesting until the bonus system for top directors had been considerably revised and made manipulation a touch less likely. ITV: sold for a 12% loss: Reason for sale is that again based on RNS/fag packet, despite lots of lipstick being applied, at the end of the day, ITV was still resembling a pig that now has limited takeover potential. Since that sale, ITV has fallen by -20%. ADT: sold at a 5% loss: Reason for sale is that based on my fag packet estimate I reckon that ADT will have to use plenty of adjustments and talk the mystical language of EBITDA in order to meet the end of year market expectations. Since that sale, ADT has fallen by -7%. Note: the trusty Fag Packet does not always get it right as with the out of favour PMP where things still look good to me but we shall have to wait until January's trading update to see if I have dropped one here (I have actually topped up PMP at the low current price). I trust the above examples demonstrate the value I attach to simple numbers in the accounts and the associated value of checking through any RNS associated with one of your investments. Stocks sold on likely Brexit weakness: selling in the main from April/May 2018: The great majority of stocks sold have deteriorated significantly since the time of my sale: some have drifted down faster than the market average. SCT fallen -30% since profits taken, CCC fallen -25% since sale (sold at a 5% loss), NRR fallen -25% since profits taken, NXR -13% since profits taken, LGEN fallen a further -10% since profits taken, HSL fallen a further -12% since profits taken, BOO down a further -16% since profits taken. Then we have the stocks associated with housebuilding which were surely the most predictable ones to be hit by Brexit worries: GFRD fallen -50% since profits taken, TW fallen -30% since profits taken, PSN fallen by -30% since profits taken, TEF fallen -25% since profits, BDEV fallen a further -20% since profits taken. Note: I have to say that many of those stocks I sold when the storm clouds of Brexit were gathering are starting to look rather interesting again. Others: There have been other actions taken in the portfolio such as profit taking on KWS at £19, originally bought at £4, and running the residual for free. Buying TCG as the stock fell to 24p following a profits warning and grind down for the following few days: a nice 40% profit banked here plus associated spread bets in 24 hours. In the main by continually following my reasoned plan which is based on well over 20 years experience in the markets including two major market recessions plus some nice bull markets, I have protected profits & minimised any potential losses to the portfolio and this has particularly been evident this year, 2018. I do of course like anybody else purchase some stocks that don’t act in the desired way and a couple of recent examples are FDEV & SMDS which were both jettisoned with less than a 10% loss yet had I stubbornly stayed in them the loss would have been rather significant; they may well both make an upturn in share price in the near future and of course I have the option to go back in but for now, it’s crucial that capital is protected. Please Note: that the above notes are not offered to suggest I may have been a smart investor. I offer them merely to show that working to a preferred investment method aided with a plan can save you considerable pain in the markets. Top Ups & New Purchases: Repurchases: Firstly a couple of recent smallish repurchases of previously sold stocks: GFRD previously sold at about £12 and TEF previously sold at 385p. Both of these stocks were repurchased at what to me at any rate, look to be bargain prices. New additions: GDWN which was mentioned in a previous Voyager Log and also new positions in ARC (very appealing lease adjusted ROCE & CROCI plus EBIT Margin) & PEG ( a bit of a tiddler for me @ £15m Mkt Cap & not without risk). Top Ups: maybe at bargain prices there again maybe not, we will have to wait and see: IGR: lease adjusted ROCE = 17%, 3yr Av. lease adjusted CROCI = 14%, EBIT margin 6% & increasing. XPP: lease adjusted ROCE = 23%, 3yr Av. lease adjusted CROCI = 16%, EBIT margin 20%. PMP: lease adjusted ROCE = 18%, 3yr Av. lease adjusted CROCI = 18%, EBIT margin 11% & increasing. BOY: lease adjusted ROCE = 14%, 3yr Av. lease adjusted CROCI = 8%, EBIT margin 17% & increasing. SOM: lease adjusted ROCE = 53%, 3yr Av. lease adjusted CROCI = 31%, EBIT margin 30% & increasing. ABDP: lease adjusted ROCE = 20%, 3yr Av. lease adjusted CROCI = 6%, EBIT margin 20% & increasing: CROCI will improve here following completion of capital works. All of these are quality companies, in my opinion, having appealing ROCE/CROCI/EBIT Margin and outlooks. Additionally, they would have in my opinion less exposure to a hard Brexit than many companies. Three of them, XPP, PMP & BOY are mysteriously out of favour with Mr Market at the moment: either a bargain or me missing something! That’s what investing is really, making a judgement and then managing your position. All of these dealings still leave me sitting on around the 60% cash mark which gives me a comfy cushion in these times of uncertainty. What I won’t be looking to do is pick the bottom of the market, we may be there now, we may have further to fall but what I have learnt from previous challenging times, particularly in 2001 & 2008, is that a lot of money can be made with acceptable risk by hitching a lift once stocks have begun their glide back from the eventual bottom. Remember that this log is most definitely not offering advice but simply sharing my thought process on my style of investing. I guess that in summary, my careful approach in 2018 will result in the year being fairly uneventful for the Voyager’s bottom line compared to the past few very rewarding years. That in itself is fine as I continually bang on about the performance of one's portfolio being assessed over a minimum of a three year period and preferably five years to have a real feel of performance. Just a quick catch up on a couple of Voyager holdings that have reported recently and it will be brief as it’s a touch historic now: 27/11/2108: IG Design: IGR: Mkt Cap £430m RNS Interim Results:  My View: these were an excellent set of results with a massive increase in PBT accompanied by a very encouraging increase in operating margin. It’s well worth the time for any investor to have a viewing of the excellent interims video featuring CEO Paul Fineman. I have topped up my considerable holding of IGR recently when the share prices depressed an amount in line with the market worries. I have been invested in IGR for quite some time now and in my opinion, they have much further to travel but time will tell. 07/12/2018: Games Workshop: GAW: Mkt Cap £1025m: RNS Trading Update  My View: well a nice in line with expectations trading update despite some lack of understanding by some journalists types and simply that’s why I never listen to them. Salaried tipsters would in my opinion if they were any good, stop writing and bet the house on the stocks they speak so wisely about: end of mini rant.

I guess that’s it this side of Christmas for a Voyager Log which gives me time to spend on another project or two. I wish all readers a happy festive season and good fortune with their investment efforts in 2019. If 2018 has not met your expectations then just remember that this investment lark is not a sprint it’s more of a marathon. Happy investing

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed