|

Voyager RNS Log at WC 03/03/2019 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Just back from a lovely winter break in India visiting the various major sites; can’t decide quite what was the most outstanding so, a close run thing between the Ganges religious ceremony after sunset, Taj Mahal and the fantastic Golden Temple especially at night. Anyway, as is my usual practice these days, I simply put on a few stop-losses and don’t even look at SharePad during my trips away; sort of fits in well with my laidback lifestyle I guess. Unless I am hit with a profits warning, then a month is merely a blip in time compared to my normal time horizon for measuring returns which is 3 to 5 years. Interestingly I get into conversation with lots of people on my travels and the subject of investment returns occasionally comes up. On this trip I had lunch with an investor who figured that a 7% return per year was outstanding; as casually as I could, I explained to her that I would be mightily disappointed with that over my timeframe: the look of shock was worth a photo! Over the years I have learnt that the more selective, critical and disciplined in terms of risk management I become, the luckier I get to be in my investment returns. I can’t think of the last time I read any journalists recommendations on stocks to buy although about a year ago I did backtrack the investment success of one very widely followed financial journalist; safe to say it was not that impressive and that’s maybe the reason why the journalist earns his living from writing rather than full time investing. As for me, I am most definitely not a pack animal when it comes to investing, in fact, when I see the enthusiasm or the pack especially for the “next big thing”, I tend to switch off right away. Honestly, I am not meaning to be arrogant; simply been there, done that and have the shallow yet healed scars to remind me of such folly. These days a private investor can really prosper provided they have real discipline once they find and develop an investment style that suits their personality and allows them to sleep at night. My simple nuggets on my investment approach:- Refine the 2000+ of LSE shares down to a number of quality shares. How do you define quality? Well for me its:

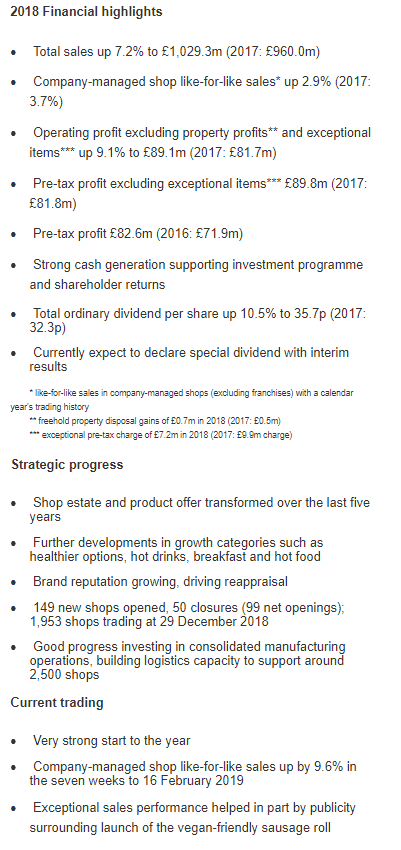

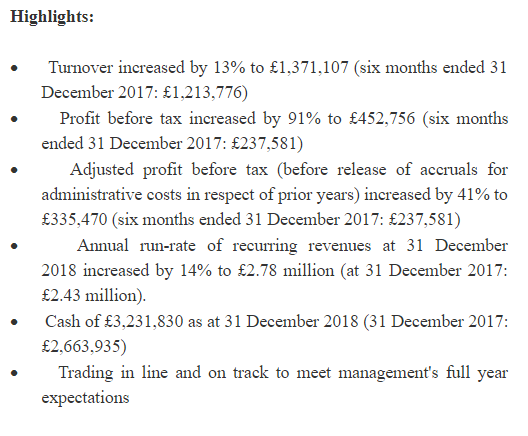

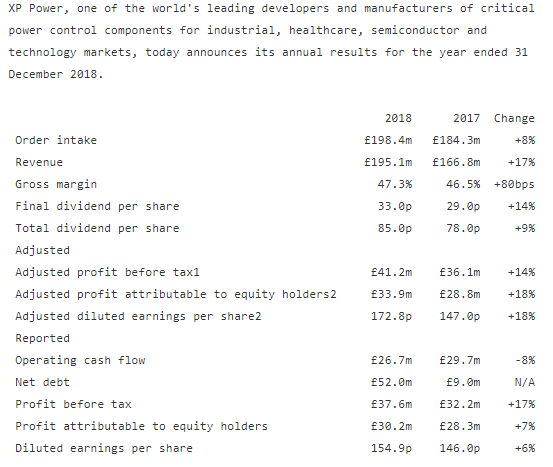

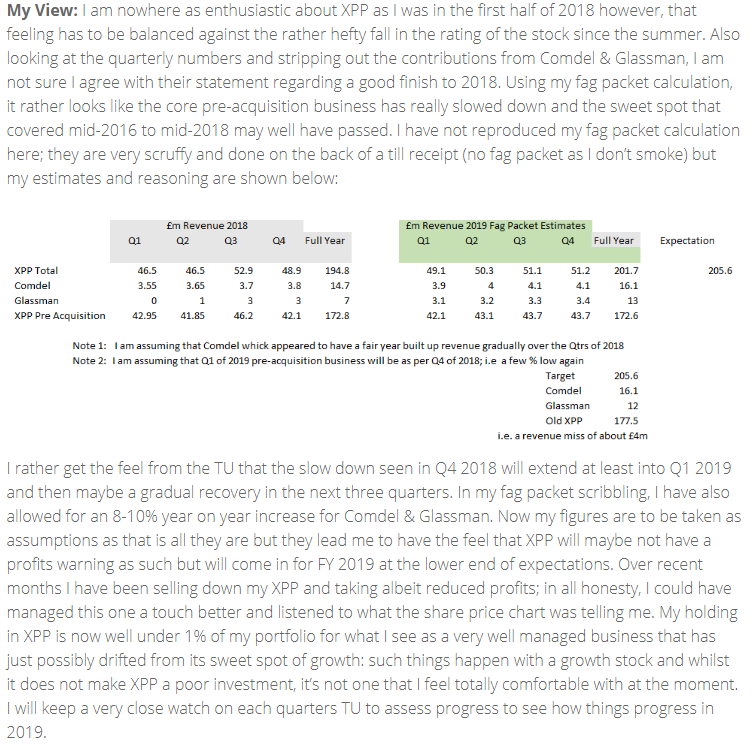

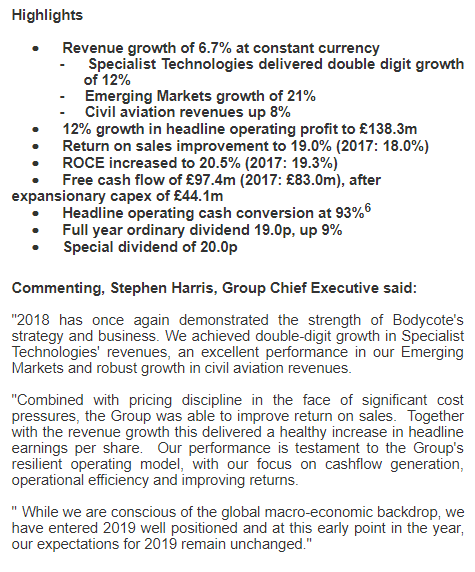

So, after applying the above, I may have whittled (come on admit it, you knew why I chose the name Stockwhittler) down the potentials to say maybe 100-150 stocks. Then it’s simply a case of following RNS newsflow, trading updates etc and then when all the fundamentals seem in your favour, asking yourself if current momentum will give you the edge. After all, there is little point in buying an apparent quality business that is simply unloved by the market and its share price is in decline as seen by the moving averages. Ok, you may get lucky and the price turn after you bought but do you need that gamble? Better in my book to wait until the momentum is in your favour and simply hitch a ride on the incline. Even after you have bought a stock, prepare to be wrong as much as 50% or even 60% of the time and when it heads south, simply sell, protect your capital and move on. In my view the greatest mistake made by private investors is listening to their ego when a stock they are holding falls by 20%, 50% etc and convincing themselves they were right in the first place to buy as they “still see value” in that stock; crazy, just plain crazy and a sure way to severely damage your returns. On the other hand, the ones that move in the desired direction and continue to offer positive RNS updates may be added to. See, simple stuff! Oh yes, keep a detailed log of your trades: reasoning to buy, hold, sell, log of RNS etc. Then very critically evaluate what went well and also what did not go so well and learn as much as you can about yourself as an investor. I may do a blog article of my approach to note keeping at some time in the future. Well, it’s been a while since the last Voyager RNS log and therefore there are a few things that I may update on or review so let's get started. Firstly a few thoughts on some the top dozen holdings in the Voyager that just keep powering away come rain or shine: AB Dynamics: ABDP: Mkt Cap £336m. Over the last three years, ABDP has delivered a very welcome 300% gain and the reason that I mention it specifically here is that in the last year alone it has put on a further 90% fueled by what appears to be some substantial institutional volume: The power of a quality business backed by strong momentum! H1 results are expected in the third week of April; I may not have finished topping up yet but will probably wait for the H1/interims. Bioventix: BVXP: Mkt Cap £198m. Another major holding in the Voyager that has been putting on a bit of a sprint in 2019. As with ABDP, BVXP is a high-quality business with impressive returns on capital and impressive EBIT margin. Interestingly BVXP only tends to issue a Trading Update RNS when there is a significant deviation from market expectations. The H1 results are expected later this month for this stock that has earned its keep in the Voyager since 2014. IG Design Group: IGR: Mkt Cap £431m: To my amazement, the market and particularly those custodians of all wisdom, brokers, have yet to stumble on the likely impact of the effect of the Impact acquisition on IGR’s financial performance. You have to dig a bit in the various RNSs/numbers but what is a little leg work? On the other hand, maybe my fag packet has got it wrong; we will have to wait and see what the next trading update says which I expect to be in the third week of April. Note: I gave my fag packet estimates for IGR in the last issue of the Voyager in January 2019. Actual RNSs announced for holdings since last Voyager Log: 31/01/2019: Keyword Studios: KWS: Mkt Cap £758m: RNS End of Yeat Trading Update The Board expects full year revenues to be at least €250m (FY17: €151.4m) and adjusted profit before tax* of approximately €37.8m (FY17: €23.0m). The Group's effective tax rate, based on Keywords Studios' measure of profit before tax* has continued to reduce and is expected to be 19.0% (FY17: 20.5%). As a result, adjusted earnings per share are expected to be c.47.0c, which would be an increase of 51% compared to the prior year (FY17: 31.18c). My View: Wow, possibly one of the most heavily shorted stocks on the market and indeed, it still appears to be shorted as I write. At one time KWS held a rather dominant position in the Voyager but I placed large sales of the stock in the summer of 2018 with an average sale price of £18-£19; it was simply a case of managing the risk associated with the spinning plates of a highly acquisitive business. I still retain an interest in KWS, about 4% of the Voyager, the bulk of which I bought at just over £3 back in the summer of 2016. The end of year trading update reads well enough yet is it likely to elevate the stock price back towards the £20 mark of mid-2018? Personally, I think the stock became a touch overheated at that time and whilst I still see KWS growing significantly it may take a year or two to reach those dizzy heights once again. Due to my perception of risk when first purchased, the shares were held in both an ISA tax-free environment and a dealing account. My retained holding, the ISA shares left in the summer at £18/£19, reside in my dealing account and foolishly are subject to CGT so, will be gradually shifted over time. I don’t mind paying taxes but enough is enough! 07/01/2019: EasyJet: EZJ: Mkt Cap £4890m: RNS Chairman's 2019 AGM Statement Our headline profit before tax increased by 41% - meaning our underlying profit, excluding acquisitions, was a record for the business. Revenue increased by 17% with both passenger and ancillary revenue performance being very strong while we at the same time delivered GBP107 million in savings this year. Plus lots of “Brexit words”. My View: well the statement reads encouragingly enough but this January purchase has yet to show any real degree of momentum either up or down. I will hold a little longer yet if the stock does not show signs of moving upwards, I will sell as I don’t wish to hold over a possible “no deal” Brexit: God, I hate that Brexit word! 12/02/2019: Scientific Digital Imaging Plc: SDI: Mkt Cap: Actually two RNSs relating to acquisitions. SDI remains on the acquisition trail with Thermal Exchange & Graticules in February following the January acquisition from Deep Matter of their Scanning Ion Conductance Microscope unit. My View: This stock was an early January purchase and in truth a bit on the low market cap size for me with all the joys of the difficulty in building a worthwhile investment position. Can’t really complain as the stock has appreciated about 20% over a relatively short space of a few weeks. If they can do half as well as JDG who remained on the acquisition trail in science and appreciated around 3000% over 10 years then I will be more than happy. I may look to add further on a pullback which is highly likely to occur with a small cap such as this. The next trading update will probably be in April or May. 19/02/2019: Greggs: GRG: Mkt Cap £1810m: RNS Trading Update Exceptionally strong start to 2019 Total sales up 14.1% for the seven weeks to 16 February 2019 Company-managed shop like-for-like sales up 9.6% for the seven weeks to 16 February 2019 Exceptional sales performance boosted by publicity surrounding launch of Greggs' vegan-friendly sausage roll. Greggs has made an exceptionally strong start to 2019. In the seven weeks to 16 February 2019, total sales grew by 14.1 per cent (2018 comparator period: 6.2 per cent) and like-for-like sales in company-managed shops increased by 9.6 per cent (2018 comparator period: 2.9 per cent). The performance builds on the strong finish to 2018, and has been supported by extensive publicity surrounding the launch of the vegan-friendly sausage roll at the start of January. As a result, customer transaction numbers have increased, with additional sales mainly comprising savoury products such as the vegan-friendly sausage roll and our other iconic sausage rolls and bakes. The rate of growth has eased slightly in February but the strength of trading is likely to have a material impact on the first half result for 2019, particularly as comparative sales growth for 2018 was weak due to the extreme weather. Sales comparatives then strengthen in the second half of the year. Overall the Board now anticipates that 2019 full year underlying profit before tax (excluding exceptional charges) is likely to be ahead of its previous expectations. Greggs again on 07/03/2019: RNS Final Results  My View: well what's not to like about Greggs? Pleasing ROCE, decent EBIT margin for this type of business and expanding with their “food on the go”. The sort of totally boring business that I like to have within my portfolio. In my view, Gregs have an excellent strategy as they open further stores in what they describe as travel and other convenience locations; not dissimilar to the strategy that proved to be so successful for WH Smiths. I also see that they are likely to pay a special dividend based upon these finals. Pleasingly momentum is on their side and somehow I have a sneaking feeling that at some time Whitbread may cast an acquisitive eye upon Gregs as there seems to be a gap in the Whitbread estate following the sale of Costa to Coca-Cola. With these easy to visit and assess companies, I have visited a few Greggs outlets and been suitably impressed by the customer demand, quality/value balance and the whole feel of a store that is cared for in a capital way. I have tended to do this type of visit for quite a few companies over the years; the likes of SMWH were always impressive yet CAKE, CPR & HFD continually ringing my unease alarm. Currently, GRG has returned me about 25% since early January and my action is to simply raise my stop loss and continue to hold whilst the company is enjoying such a positive phase. 27/02/2019: Arcontech Group: ARC: Mkt Cap £17m: RNS Interim Results:  Outlook Arcontech has a sound business base supported by a high level of recurring revenues and a strong balance sheet. Our business is international with customers operating in the UK, Europe, the USA, Hong Kong and Singapore. As such it is the Board's view that we are unlikely to be adversely affected by Brexit. We propose to maintain ongoing investment in product development and enhancement, and as a result of working with existing customers we are delivering world class solutions which provide cost savings and competitive advantage. As we repeatedly note in our statements to shareholders we remain mindful of the long and unpredictable sales cycles we often face and the challenges this brings in predicting the timing of contract wins. Nevertheless, the Board views the long term future for the business with optimism and in the short term expects results for the full year to be in line with expectations. My View: a decent enough set of interim results and ones that encourage me to continue to hold rather than add further. To qualify my sentiment I will list the things I like & the things that concern me with ARC: I like: the decent returns on capital, the very respectable EBIT margin, the strong cash position/lack of debt and recurring revenues. The things that concern me: are the low market cap (difficult to trade especially if bad news breaks), the unpredictable sales cycles which just scream out “potential profits warning”. My overall view is that this stock will remain as a small percentage of the Voyager whilst it retains certain attractions: I will hold rather than purchasing further stock for now. 28/02/2019: Telford Homes: TEF: Mkt Cap £240m: RNS Strategic and Trading Update A bit of a profits warning via displacement of some profits by a year and strategic move on more concentration on build to rent. My View: well I sold my fairly sizable holding in TEF for a small profit in the Autumn of 2018 (see Voyager 12/10/2018 ) when they issued a rather cautious trading update on 10/10/2018 which looked like a “softening up” for a future profits warning. However, as the stock gradually came back I did repurchase a small position which has now been jettisoned for a small loss: you can’t get things right all the time but as ever, you carry more risk when purchasing against declining moving averages which I did with that most recent TEF purchase. For most of my purchases, I like to see the momentum offering a tailwind rather than a headwind; a simple way of increasing the odds on your side. 05/03/19: XP Power: XPP: Mkt Cap £430m: RNS Final Results 2018  Outlook The new financial year has begun against a background of ongoing macroeconomic uncertainty. While we are not immune from the impact of external events, we are encouraged by our start to 2019 in terms of order intake and our healthy order book. On this basis, and with the benefit of the Glassman acquisition, we expect further revenue growth in 2019 but this will be weighted to the second half of the year. My View: well the results and weighting towards the second half of 2019 are pretty much spot on with my fag packet estimates published three months ago and I see no reason to move markedly from my cautious view as given on January at the time of the last trading update: reproduced below:  Today post results, I still see XPP as a very decent business yet with the growth as such, especially if H1 of 2019, having to come from Comdel and Glassman. I therefore still retain my view that XPP may just struggle a tad to meet the market expectations for 2019. Note after earlier profit taking, XPP is currently at less than 2% of the Voyager portfolio and I am reasonably happy to hold but will certainly be drilling down into each of the very informative XPP RNSs announced during 2019. I will possibly refrain from topping up until future trading updates ease my slight concerns. Greggs again on 07/03/2019: RNS Final Results; Notes appear above with trading statement. 08/03/2019: Bodycote: BOY: Mkt Cap £1.5b: RNS Finals for 2018  Summary and Outlook

2018 has once again demonstrated the strength of Bodycote's strategy and business. We achieved double-digit growth in Specialist Technologies' revenues, an excellent performance in our Emerging Markets and robust growth in civil aviation revenues. Combined with pricing discipline in the face of significant cost pressures, the Group was able to improve return on sales. Together with the revenue growth this delivered a healthy increase in headline earnings per share. Our performance is testament to the Group's resilient operating model, with our focus on cashflow generation, operational efficiency and improving returns. While we are conscious of the global macro-economic backdrop, we have entered 2019 well positioned and at this early point in the year, our expectations for 2019 remain unchanged. My View: Bodycote is a quality business that has earned its keep in the Voyager since early 2016. These results are in line with expectations, the outlook is decent, ROCE improves a tad, EBIT Margin 18% & the line in the report “The movement in revenue mix in favour of our higher margin Specialist Technologies also added to the improvement in return on sales and is part of our long term goal of improving Group margins to world class levels”. Also a handy special dividend has been declared. I see BOY as a high quality yet rather boring business; in fact the type of business that comfortably holds a quiet spot within the Voyager. Whilst BOY like so many businesses may be cyclical to a degree, I feel that risk has been somewhat reduced with the way the business has positioned itself in recent years. I am happy to continue to hold. Voyager: Stocks Welcomed Aboard & Those Jettisoned since 01/01/2019 Just to ensure that I have updated on purchases hence far in 2019, they are; Greggs purchased in early January; currently up 25% Softcat repurchased in early January; currently up by 15% Kainos & EasyJet both neither gaining or losing money but for both, it’s early days since purchase. In addition to those four stocks mentioned above, there have been a few minor top-ups of existing holdings. Some stocks left the Voyager entirely: Petards for a small gain and the residual Telford for a small loss on the most repurchased recent batch. This weekend it’s the long haul down to Plymouth for the Hatters match; that’s about a 640 mile round trip from home. The logical side of my brain simply does not work with football! Whatever you are doing this weekend, I hope you have an enjoyable time. As ever, Happy Investing.

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed