|

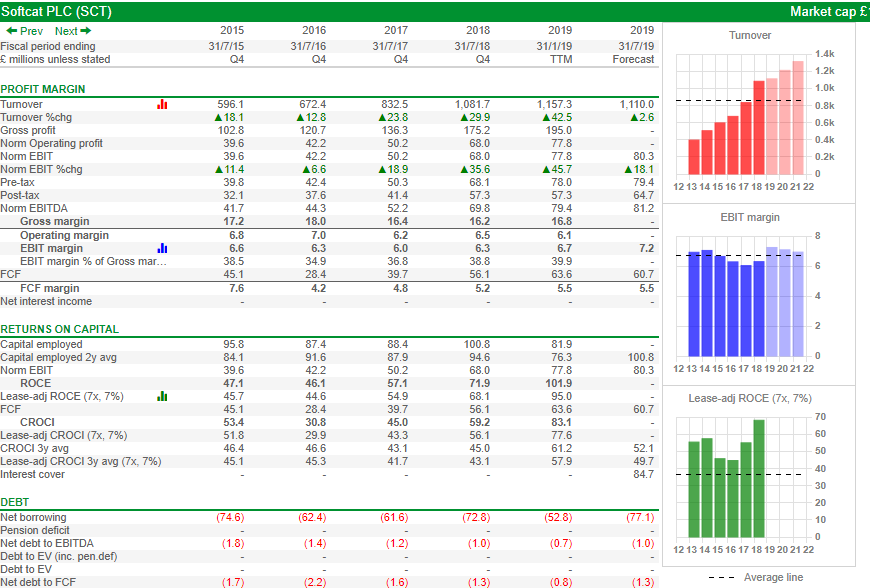

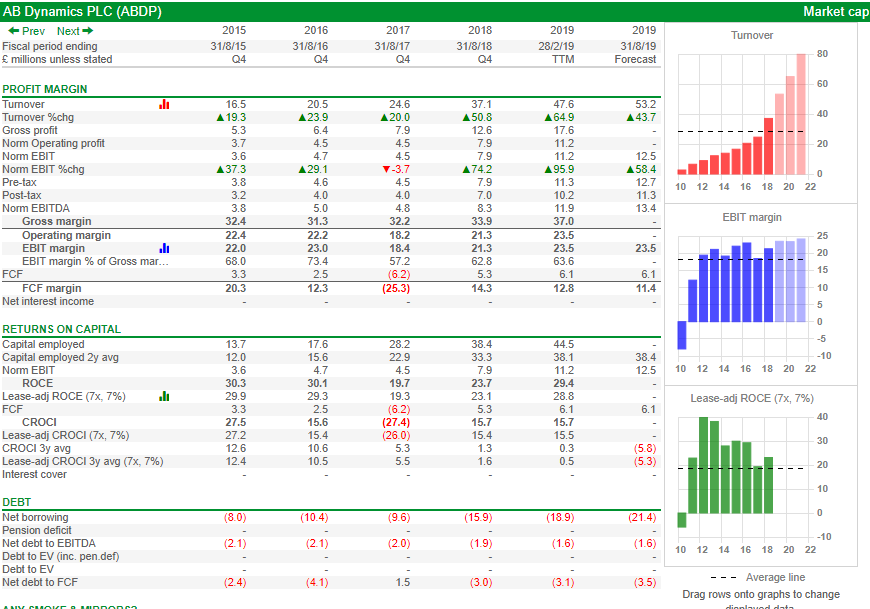

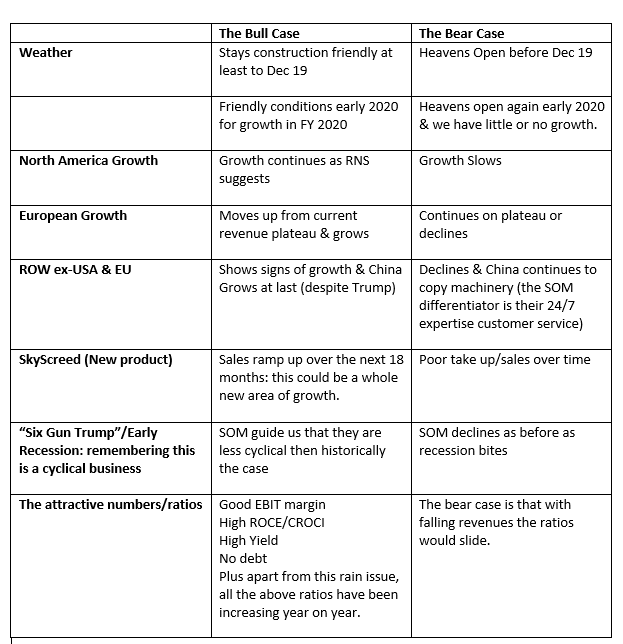

Voyager RNS Log 07/05/2019 to 07/06/2019 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. A sobering thought to start with in that I suspect that the great majority of us are enjoying apparent good returns so far in 2019, the actual fact is that the majority of stocks in the Smaller Cap/AIM sectors are still some way of their valuations as seen at the end of September 2018. Yes, I can hear you say, here he goes “emotionless bar**a*d” yet, as I always say, investing remains a long game. In the last quarter of 2018, the FTSE Small Cap Index fell by -11% & that of the FTSE AIM100 by -26%. The two following SharePad charts show that whilst 2019 is feeling easy by comparison, it’s a long haul back to where those indices sat at the end of September 2018; yes, investing is a long game.   As ever, apart from “silly times” when investing in almost anything makes you money, we live in a stockpicker's market. The last FY was rather kind to me and that was partly to my minimizing my exposure in Q3 of the financial year (October to December 2018). Simply put, in easy times even the turds float but in normal market conditions, it’s a touch more challenging to pick the winners. So, there is a fair bit of catching up to do since the last Voyager RNS Log, for the sake of boredom, I will keep the log brief with the exception of Somero: 07/05/2019:4imprint:FOUR: Mkt Cap £730m: gave an encouraging AGM statement “Although it is still early in the year, the Board is confident that the Group will deliver full year financial results in line with current market forecasts." My View: So, I am happy with that from what I consider to be a reasonably valued growth business with growing revenues/profits and excellent returns on capital; I would like the EBIT margin to be higher but otherwise, ok.  14/05/2019: Greggs: GRG: Mkt Cap £2240m: GRG gave a pleasing trading update “The exceptional level of like-for-like sales growth that began in January has been sustained in the months that have followed, driven by increased visits to our stores. Looking forward, the sales comparatives from 2018 become progressively stronger but we now anticipate materially higher sales for the 2019 year as a whole than we had previously been expecting: the Board believes that underlying profits (before exceptional costs) for the year will be materially higher than its previous expectation”. My View: originally bought in January and some profits taken but very happy to hold remainder as this company is on a roll. Just like my old boring holding SMWH travel, you usually are in a queue in this popular food/coffee outlet and the quality is value for money. Wherever you get the chance, it’s always valuable to check the popularity of such outlets; I never had to queue at CAKE!. Happy to continue to hold GRG.  14/05/2019: Portmeirion: PMP: Mkt Cap: £110m: Trading Update & profits Warning I have written some very encouraging things in the past 15 months about PMP and by all news-flow, the business was growing well and had overcome the glitch they had in South Korea back in 2016. However, totally unexpected it seems, the management were again showing a remarkable disconnect between themselves and their over stocking agent in South Korea. So, sorry, I have completely lost confidence in the “finger on the pulse” skills of the very well rewarded CEO and his team. Now sold and rather unlikely to return. 15/05/2019: Scientific Digital Imaging: SDI: Mkt Cap £52m: Trading Update giving revenue for the full year as moderately ahead of expectations and profits to meet expectations. The share price has come off a little since its earlier rise but happy to hold and take the occasional top up.  My View: I do like the business which to me resembles a Judges Scientific style. At the same time, you have to keep in mind the potential potholes that may confront highly acquisitive companies. 20/05/2019: Softcat SCT: Mkt Cap £1483m: Q3 Trading Update The Company continued to perform well during the Period and has delivered strong year-on-year growth across all income and profit measures. Performance drivers remained broad-based, with different technology areas and customer segments all showing growth. The Board is therefore confident that full year results will now be slightly ahead of previous expectations.  My View: I am happy to continue to hold SCT which has delivered a 40% return since my purchase in January. 23/05/2019; Hollywood Bowl: BOWL: Mkt Cap £352m: Interim Results Really nothing much for me to say about this tidy well run business that simply ticks along nicely. I don’t expect it to set the Voyager racing but nevertheless happy to hold this steady number. 24/05/2019: Bodycote: BOY: Mkt Cap £1510m: Trading Update: The Board's expectations for the full year remain unchanged. These days BOY is a very small part of Voyager as it has really struggled to please the market whilst making steady if unspectacular progress; probably hold and maybe add if the market takes a liking to BOY again. 28/05/2019: Litigation Capital: LIT: Mkt Cap £116m: Court Approval on Settlement Not much to say really other than I have traded these a couple of times since they came to market and currently hold maybe for a longer term, a position in Voyager, Its not my favourite beast of a business area but does kick off some rather decent financial ratios so let’s see what happens. 29/05/2019: Spectra Systems: SPSY: Mkt Cap: £58m: Trading Update Expects its profits for the year ending 31 December 2019 to exceed market expectations. The increased profits are related to a combination of central bank sensor related research funding and strong first half of the year optical materials sales. My Thoughts: well I did hold SPSY previously but sold as part of my move to cash in mid-2018. I bought back in April so it’s a case of work in progress. 06/06/2019: AB Dynamics: ABDP: Mkt Cap £505m: Result of Oversubscribed Open Offer This follows a very successful placing in May and ABDP now tell us that the open offer was very heavily oversubscribed: no surprise really as this is a quality outfit in a very good place at the moment. I first bought at £4 and will continue to hold/top-up. Rather than words, the following SharePad custom chart shows my attraction to the company:  07/06/2019; Games Workshop: GAW: Mkt Cap £1500m: Trading Update for Year End Games Workshop is pleased to announce that the sales and profit growth, which was discussed in the trading update released on 12 April 2019, has continued in the period to the end of the financial year. Sales growth has been across all sales channels. We expect the Group's sales for the year to 2 June 2019 to be approximately £254 million and the Group's profit before tax to be not less than £80 million. Royalties receivable from licensing are approximately £11 million. My View: once again another cracking performance from GAW which goes from strength to strength. Note the last trading statement on the 12th April stated “The Board's current expectation is that profit before tax for the year ending 2 June 2019 will be c. £80 million”. This trading statement says not less than £80million: happy days. An absolutely quality core company that I am very happy to continue to hold. 07/06/2019: Somero: SOM: Mkt Cap £155m: RNS Trading Update Profits Warning Trading during the five month period to the end of May 2019 has fallen below management's expectations, primarily due to adverse weather conditions in the US, the Company's largest market. Broad sections of the US experienced the highest levels of rainfall on record.* The record rainfall seen in the US has delayed project starts which in turn has slowed the pace of equipment purchased by our customers, the impact of which was seen through historically strong trading months of March and April. Whilst there was an improvement in trading to end the month of May, and although the Company expects weather conditions and therefore trading in the US will improve throughout the rest of 2019, the Board now does not expect the Company to fully recapture the shortfall caused by this extended period of poor weather in the current financial year. As such, the Company now expects to deliver 2019 revenues of approximately US $87m, EBITDA of approximately US $28m, and expects to have net cash at 31 December 2019 of approximately US $18m, after one-off investments of $4.0 million related to building expansions for the Skyscreed ® 25 and the Fort Myers Training Facility as well as the $2.0 million acquisition of Line Dragon. In the Company's other main markets, Europe and China, as well as in the Rest of World territories, trading in 2019 is at comparable levels to 2018, and the Company continues to see opportunities for growth in H2. Growth in India has been steady, as the Company continues to gain traction in the region. The Middle East and Latin America are trading below 2018 levels, however the Company expects improvement in H2 2019, notwithstanding the political uncertainly and economic challenges seen in these regions. The Company is pleased with progress on the new SkyScreed ® 25, having sold the first unit and with continued strong interest in the product. Traction gained so far with the SkyScreed ® 25 is in line with what the Company would expect when bringing a disruptive product of this nature to market. * An average of 36.2 inches of precipitation has fallen over the Lower 48 from May 2018 to April 2019 representing the highest level recorded in over 120 years and six inches over average. *Source: National Oceanic and Atmospheric Administration data My rambling: well not the news I was anticipating and in truth, I did not expect an “ahead of expectations” simply an “in line”. Now, with a profits warning, I usually have a quick think and then commence selling in batches but this one from SOM needed a touch more thought. SOM has always been to my mind a boring but classy/trustworthy outfit. I first bought then at about 100p back in 2014 and they have been very kind to me. I did top slice my position a couple of times over the past two years but due to the positive newsflow was happy to continue to hold the remainder. The original attractions of the 2014 purchase were:

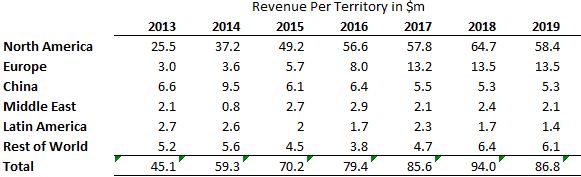

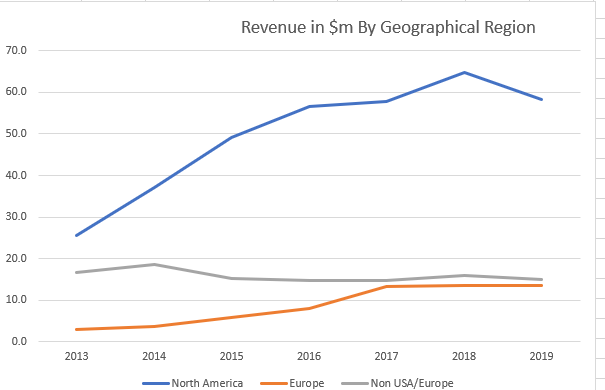

So, what actually did go wrong in 2019? Well, due to the nature of construction work, wet or in this case incredibly wet weather conditions slow down the construction projects and in turn slowed down the demand for Somero products. This is nothing new and happened as recently as 2017 but the weather conditions picked up in time to allow SOM to meet market expectations. However, 2019 rainfall has hit SOM to such an extent that the 2019 expectations have had to be revised downwards as seen in the RNS. It seems to me that the business demand will still be there when dry conditions prevail and that SOM will simply inadvertently bump sales into 2020. Ok, maybe no issue but I suspect that there will be an impact on the hoped-for further growth in 2020 that may have occurred without this rain delay; simply due to overall knock on effect of construction delays with projects being pushed back due to wet conditions. My fag packet calculation after bringing together the sales by geographic region over the last seven years, including the revised position for 2019 (Note regional assumptions based on the text of RNS), shows:   There are a few potholes that SOM has encountered in that whilst North America has been growing well enough, Europe has plateaued to a degree and areas of great promise such as China have proved near impossible to crack. Other potential potholes are of course the cyclical nature of construction which does not worry me too much as you can see this creeping up and weather conditions may possibly raise their head again. So, to my analysis, although Somero is a really good business, it is essentially over these last three years a company comfortably growing revenues within the USA yet at the same time, it is struggling to meaningfully grow its revenue streams outside of the USA and Europe. Note Europe was growing quite well but from 2017 has really levelled off (was that a pun). The graph below simplifies the revenue growth by my classification of revenue streams into the three areas of North America, Europe and non-USA/Europe and demonstrates my non-USA lack of growth concerns over these past three years.  As you can see the growth in revenue for SOM, this past couple or three years is really about North America and hence this hit on revenue and profit for 2019. In truth, this temporary weather issue is not the worrying part as that will pass, of slight concern is the lack of collective growth in recent years outside of the USA. I do believe that if weather conditions had been favourable, then 2019 expectations would have been fairly comfortably met. Yet, as I say, this growth would have been down to the USA as the commentary on other regions in the RNS is not particularly encouraging with regions either trading as in 2018 or the minor areas such as the Middle East & Latin America slipping a touch.  My position is a touch reduced from that bulky one of 2017/18 by top-slicing on a few occasions but it’s still a significant one. So, overall thankfully this profits warning has delivered just a bruise within a reasonably wide portfolio; profits warnings and bruises are simply irritants within this investment game we play.

Whilst I don’t think that SOM is still quite the hidden or undiscovered gem it was back in 2014 or those few following years, it's still a fine business producing some very attractive financial ratios and an excellent dividend. I really expect that with drier USA weather conditions SOM will meet their revised forecasts for 2019. Thereafter moving into 2020 growth hopefully be back on track; yet will it be able to really significantly grow its revenue stream away from the USA? That outside of the USA lack of significant revenue growth is I admit, a touch frustrating. Yet to be fair to SOM, once the USA usage picks up with more normal climate conditions, it should return to being an attractive growing business based on USA sales alone: we also have the temptingly very high dividend. Hopefully, SOM can get Europe & ROW improving in terms of revenues and then, of course, we also have the potential SkyScreed sales which if all goes well, could be a game changer; we shall have to wait and see with that one. Will I be selling, adding or simply holding the position that I have post PW? Well, for now, I will simply hold and just maybe squirrel away a few more as we see how Mr Market reacts over the coming weeks after offering prayer and forgiveness to Zeus the weather God. Somero Summary: Within investing, there are of course no certainties but my feeling is that on the balance of probabilities, that we still have here a high-quality well-managed albeit somewhat cyclical business that based on USA growth alone is worth a place in the Voyager portfolio. If SOM can achieve revenue growth outside the USA and exploit the likely potential of SkyScreed, then the presently reasonably attractive SOM would become an extremely attractive SOM. It’s maybe not the sexy concrete kitten it was in 2014 but still well worth holding this quality company in my view. Note: as ever, this is not advice for a reader to buy or sell but just me sharing my possibly incorrect reading of the current situation with SOM. Any lessons from this profits warning? Well, an oh so obvious one that we SOM followers may have picked up on; simply the news of the awful wet conditions with the heavy rainfall in the USA in the first few months of the year. Fairly obvious when you think about at that construction projects would be delayed; wish I was a touch smarter! Was the sale of £2.7m of shares by the CEO Mr JT Cooney on 28/03/2019 inspired by the sight of a modern-day Noah’s Ark floating past his second-floor window? We can speculate but never really know! If I were attending the AGM which up to 2017 was historically held in London, now back in Florida, I would probe about concrete plans for non-USA revenue growth, will Europe return to growth, can China be cracked etc. I would also ask about progress with sales and enquiries for the new product, SkyScreed. As ever, my appreciation and credit to Sharescope/SharePad; some of their tables are reproduced within this article. At this point, I should say that I have a rather demanding yet pleasurable summer planned with a mix of leisure/holidays and a couple of time demanding projects that I am involved with. The result of this is that it’s quite possible that there may be a gap in Voyager RNS publication until early September. I will just have to see how time goes. I hope all readers have a wonderful summer and wish you all the best in the markets. Happy investing

1 Comment

Pete Howat

6/11/2019 04:22:30 am

SOM - did you really say, 'concrete' plans for non-USA revenue growth? ;-) Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed