|

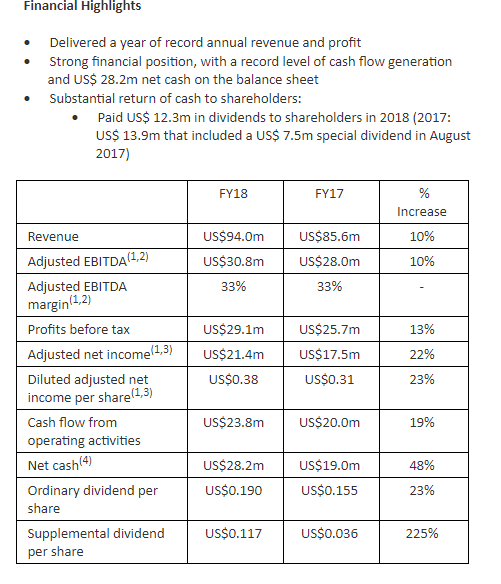

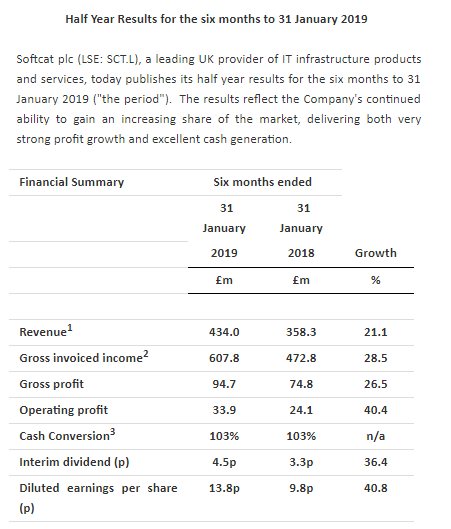

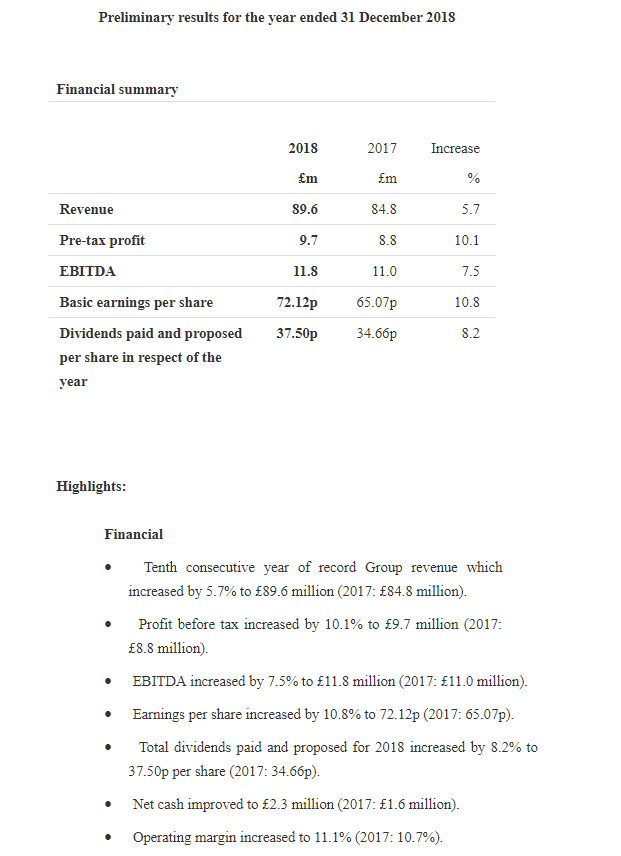

Voyager RNS Log 10/03/19 to 29/03/2019 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Although I have been putting some money back into the markets from that hefty cash pile I partially retreated to in the summer of 2018, by the end of September it had reached about 70% cash, presently I am a touch more of a trading animal rather than a longer-term investor due to our political climate with the dreaded B word. That approach will no doubt change as time progresses and we come through this silly European episode. Until the dust settles I intend to take what risk-weighted opportunities I can as long as those opportunities suggest a good chance of adding to the bottom line. Investing is about making money and not simply showing steadfast loyalty to one of your chosen holdings. On reflection, I am very happy that I took that cautious approach as the storm clouds gathered and I, fortunately, was not greatly affected by the turmoil of October to December 2018. As described in the Voyager before, my approach is to seek stocks from the 2200+ that reside in the LSE that meet my prescribed quality criteria; this yields about 150 or so stocks that merit further investigation. In addition over the coming months I will pay particular attention to attractive momentum stocks that may or may not be derived from my universe of 150 or thereabouts stocks a recent example was the trades in GRG, KNOS and EZJ; two went very well for a very handy short term profit and the other sold for a small loss but overall the bottom line of the portfolio benefited nicely. I don’t let the worry of dealing fees lock me into a stock as after all, such charges are incredibly low these days. Therefore, I am happy to move in and out of a stock and once sold, if the stock then looks attractive, I simply reenter: as ever, it’s the bottom line that counts. Turning to price movements in previously held stocks, I am really glad that I decided back in July 2018 that Bonmarch was not delivering the turn-around I was looking for and sold for a handy profit. Since that sale at 110p, BON has issued two profits warnings and now sits at 20p: be cold, be ruthless, don’t have blind loyalty to a stock as it’s incapable of returning that affection. Let’s turn to RNSs for Voyager stocks issued in the last couple of weeks: Wednesday 13/03/2019: Somero: SOM: Mkt Cap: £218m: RNS Final Results Financial Highlight  Outlook: The Board believes the Company has numerous meaningful growth opportunities in 2019 across its broad portfolio of markets and products that is supported by positive non-residential construction market conditions and reinforced by customers reporting project backlogs that extend beyond 2019. Based on this positive environment and the momentum of the business, the Board is confident that Somero is poised to deliver another year of profitable growth to shareholders in 2019. My View: well another set of excellent results from Somero with a steady increase in turnover by 10%, PBT up by 13% and adjusted EPS increased by some 23%. In addition, the cash position at SOM looks very healthy and supports a special dividend to be paid to shareholders. Looking forward we have the new SkyScreed product designed for use with high rise building, so, hopefully, another income stream to be brought online as the year's progress. It seems that I am repeating myself yet again with SOM but this is a high-quality company that I have happily held in the Voyager since October 2014 and I am again happy to hold plus add when price action invites a top up. Note: I do read some commentary about SOM being a cyclical business and indeed many businesses are cyclical to an extent. My argument is simply “well so what, you don’t fall in love with a stock and once it goes into decline you have the sell button”. How do you know when it’s going into decline? Well fairly easy really, you read the RNS flow and take note of the share price graph. Tuesday 19/03/2019: Softcat: SCT: Mkt Cap £1.7b: RNS Half Year Results  Outlook The Board expects a full year outcome marginally ahead of previous expectations. My View: well as signalled earlier in the Trading Update of 09/01/2019, the interims were likely to be very decent and that exactly what we were treated to with revenue up by 21% and operating profit up by 40%. I do have a touch of history with SCT having purchased in May of last year and then selling, almost at its all-time high, at the end of August, The stock price of SCT then declined by about 35% before again swinging north aided by the excellent trading update in early January this year. I will hold for the moment but with the current political climate, I am mindful that unless I have a really high conviction for a stock, when it’s momentum turns profits will be taken and targets reassessed. Thursday 21/03/2019: Portmeirion: PMP: Mkt Cap £116m: RNS Final Results  Outlook Firstly the usual Brexit notes; becoming boring but all companies do it! Although we face political and economic uncertainties around the world, including Brexit, we look forward into 2019 with confidence and at this very early stage of the year expect trading to be in line with expectations for the full year. My View: readers will know that I really like the financials of PMP, the very underpromising way that they communicate progress and the overall quality of the business. What do I like? Well, lets first look at the years of continuous growth: that’s 10 years of very decent revenue growth & EBIT growth. Then we have the significant and well-performing acquisition Wax Lyrical that continues to boost sales. Then we can chuck in the rapidly growing but still infant online sales offering which grew by 25% adding contributing £4.3m to the £89m revenue for the year. So, now a quick look at the financial numbers and ratios: 18% ROCE, 13% CROCI (both lease adjusted), 89% FCF conversion, no debt, year on year gradual increase of EBIT margin to 11.2%, dividend well covered by FCF. All in all, a very tidy business. In fact, back in January, I did in this log do a comparison of PMP with the higher rated Churchill China suggesting that PMP was somewhat undervalued compared to it’s Stoke neighbour; I still feel that and rather expect it to make up that 30%-40% in the coming year or two. I am happy to continue to hold. 26/03/2109: D4t4: Mkt Cap £108m: RNS Contract Wins  My View: I have been with D4t4 at times taking profits and at other times topping up, since 2016 buying at prices ranging from 125p to 220p. In fact with the market wobble in late 2018, I completely exited D4t4 in November yet returned again in early February 2019. These contract wins certainly appear to have excited the market and the share price has appreciated nicely. My thought is that with this Celebrus offering D4t4 will continue to prosper. As ever, it’s a relatively small business and there could be bumps in the road but I am very happy to hold and will consider adding further.

27/03/2019: AB Dynamics: ABDP: Mkt Cap: RNS Trading Update My View: An in-line trading statement and nothing to get overly excited about given the fact that ABDP share price has actually doubled in this financial year. Once again, I felt that the price had got a little ahead of itself and did peak lop some at close to £18; first entry bought at £4 back in the summer of 2016. A nice company that once again has some cracking good financial numbers that attract me: 24% ROCE, 16% CROCI, 21% EBIT Margin & no debt. It’s got a touch expensive hence my peak lopping but I feel I may top up again on further positive newsflow/more attractive price. Stocks Welcomed Aboard Voyager & Those Jettisoned in the last three weeks: New positions: 4imprint Group: FOUR: following a decent set of finals early in March: decent increase in turnover, EBIT and a lease adjusted ROCE in the ’60s, good FCF conversion, no debt. I normally like a higher EBIT margin but this company has a good solid track record. Note to myself; Come on Whittler, wake up you sleepy idiot, you have been watching these for how many years? One most unlikely one for me as I am utterly useless with holes in the ground and certainly even more useless with holes in the sea, but the momentum of Hurricane Energy: HUR encouraged me to take an initial position; will it all end in tears? One on the nearly watch list: where I did open and close spread bet position ahead of a potential significant ISA purchase: D S Smith: SMDS: we are in my view, reaching a transformational state for SMDS having announced the agreed sale of its plastics division, therefore, shedding the “toxic plastic taint”. The funds from the sale of the plastics division to Olympus for £450m will be used to reduce the debt at the SMDS which removes a slight obstacle; I don’t like masses of debt. Anyway, the initial little touch failed so it's back on the serious watch list. Stocks sold: Greggs: GRG for an 18% return in 10 weeks: I may well go back in shortly. Kanios: KNOS sold for a handy 8% profit; yes, I know it’s a tough market at the moment but at least it keeps the bottom line ticking over. Easyjet: EZJ: for a 4% loss in 6 weeks Finally, one stock that left the Voyager in mid-March 2019 having been a resident for these past five years: Bioventix: BVXP: the stock has had a fairly exhausting climb over the last seven weeks with the stock price appreciating by some 25% to hit the £40 mark. Now whilst BVXP has been a fabulously rewarding stock for me since my entry point at £7 back in 2014 and has many of the characteristics I look for in an investment, at £40, to my mind it had become a touch overheated fanned by the flames of expectation over its troponin antibodies. With all of this in mind and despite the fact that I have really enjoyed a fabulous rise from £7 to £40, I sold my entire holding in BVXP at prices between £39.50 & £40: simply time to take a profit and sit on the fence for a little while. I believe BVXP is a really top-notch outfit with the stunning financial numbers I crave for in a stock but the valuation had become a touch overstretched in my view. My philosophy is to always manage risk and after that recent 25% rise, it simply seemed sound to bank some profits. As ever when I exit a share, that exit may possibly only be temporary: I will keep an eye on RNS newsflow and share price action with a real possibility of taking another position in BVXP at hopefully a more attractive price. The interim results released on 29/03/2019 look rather as expected, so, for now it goes back on that active watch list. On the non-markets front, I am rekindling my passion for making sourdough bread and the first batch with the new sourdough starter I have produced should be ready today: happy days! At the weekend it’s off to Bristol for the Hatters game against Bristol Rovers: will we be able to get back to back promotions and return to the Championship I wonder? Whatever you are doing, have a great weekend and happy investing!

1 Comment

Andrea34l

5/1/2019 03:51:49 am

I'm happy to see you have bought FOUR!! :-) I bought two lots this year, and they have smashing momentum. Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed