|

Voyager RNS Log Weeks Commencing 04/11 & 11/11 of 2018, As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. A few thoughts on October/November 18: I just do not get fazed by such periods as I have simply been investing too long I guess; I have the scars and hopefully the bolted on wisdom having invested through the bear markets of 2001 & 2008 which taught me the value of moving heavily into cash. Having been through some tough periods in the past, I feel that’s its imperative that an investor has a plan, a strategy and when they see the cliff face looming they at least consider executing that plan rather than waiting until their toes are dangling over the cliff and acting in panic mode. All through 2018 we have had the Brexit virus looming and threatening to deliver massive uncertainty which as we all know is what the market hates. As I have been continually writing in this log during this year, I chose to execute that plan and place a high reliance on a very substantial cash position. In fact, the overall cash position in the Voyager is the highest it has been since the financial crisis of 2008. In both 2001 & 2008 global factors were at work, sadly this time around the threats are far less global and largely self-inflicted by the UK upon the UK. Am I right with this strategy? Well maybe, maybe not but it’s a thought-out strategy that sits there to be used in case it’s needed and it’s rather like a Fire Assessment for a hotel i.e. you don’t wait until the smoke alarms go off to develop a plan for evacuation and safety. One thing is for sure is that our politicians right from the start of the referendum campaigning to this very day, have presided over a total shambles acting with the dignity and honesty of a Chinese AIM-listed company. One final comment on being in or out of the market: fund managers have little choice other than to be in the market and use the slogan “it's about time in the market not timing the market”. On the other hand, hugely successful investors like Minervini may withdraw from the markets for a period of time when things just don’t look favourable. Anyway, a few thoughts on the man at the top of a company, the CEO and certain traits they may have that I dislike, traits that ring alarm bells. This Magical Person The CEO: One bias that has developed with me over the years is that if I have doubts about the CEO of a business then it’s best on balance to listen to those doubts and maybe just leave it alone. You have probably come across such individuals yourself; the ones that may display some of the following traits:

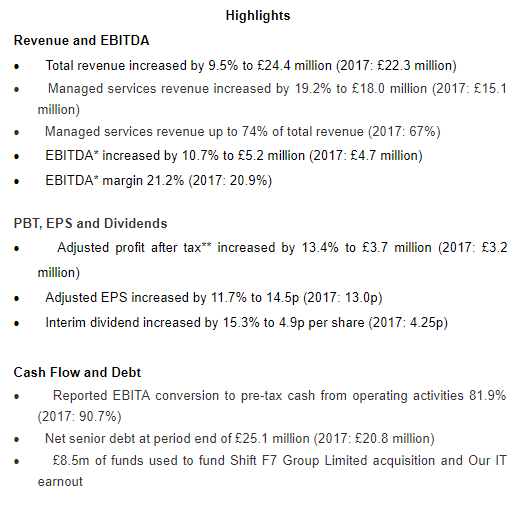

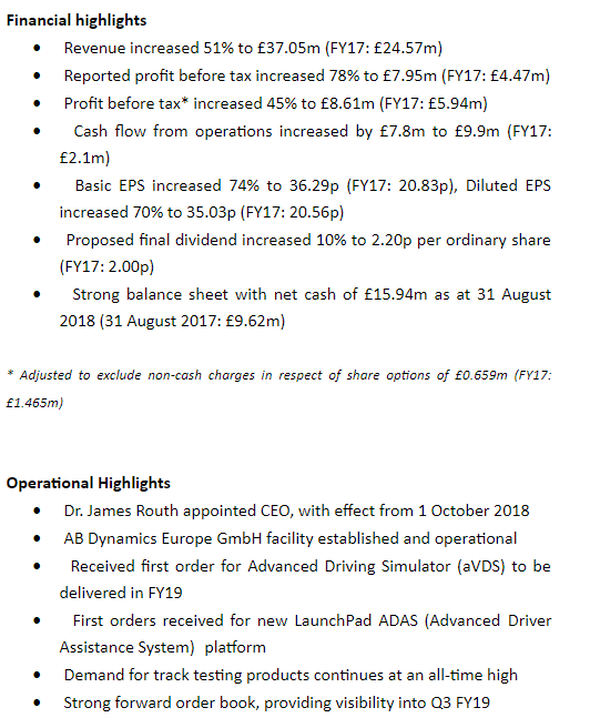

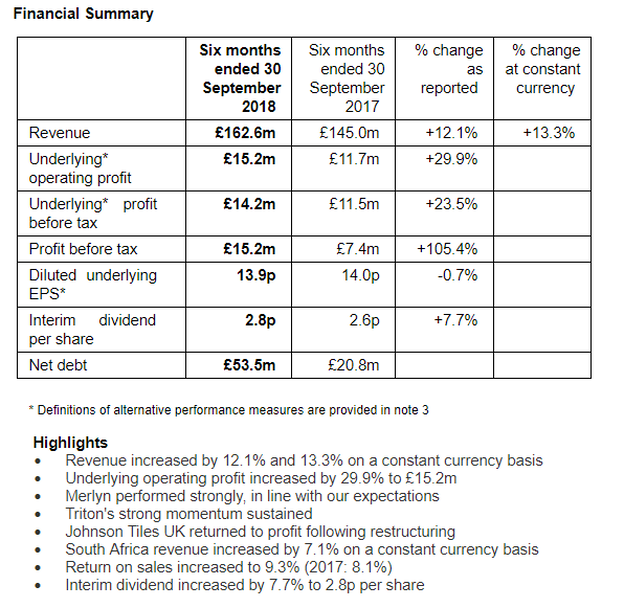

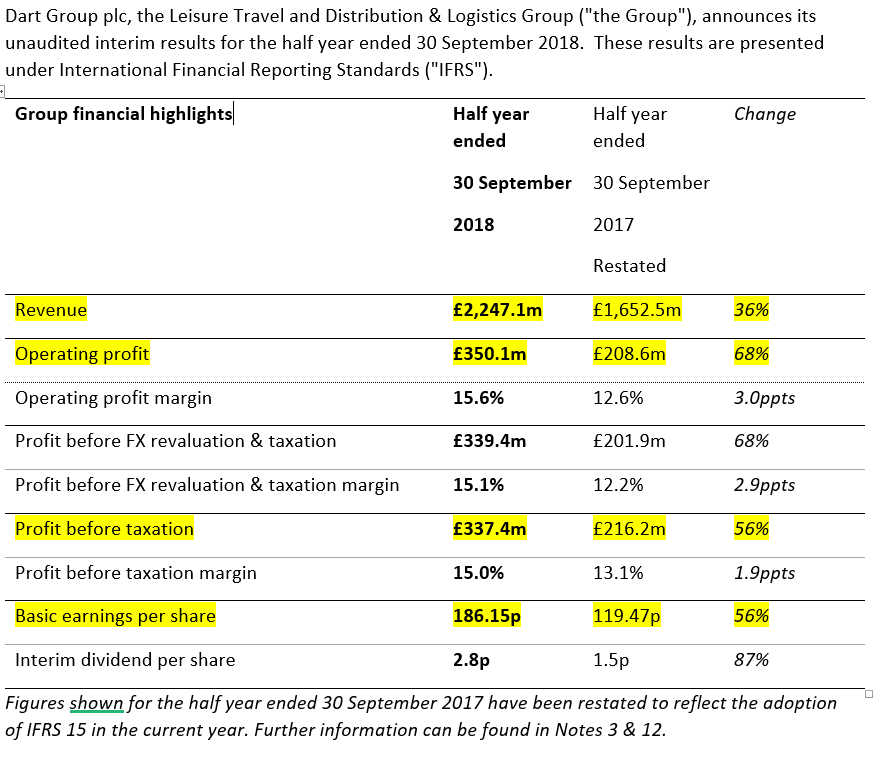

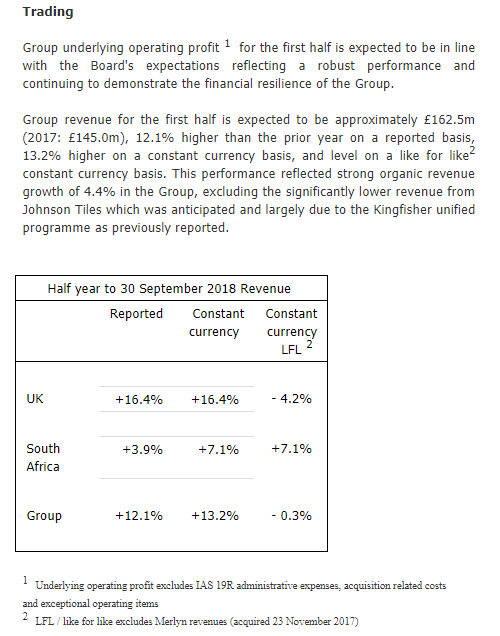

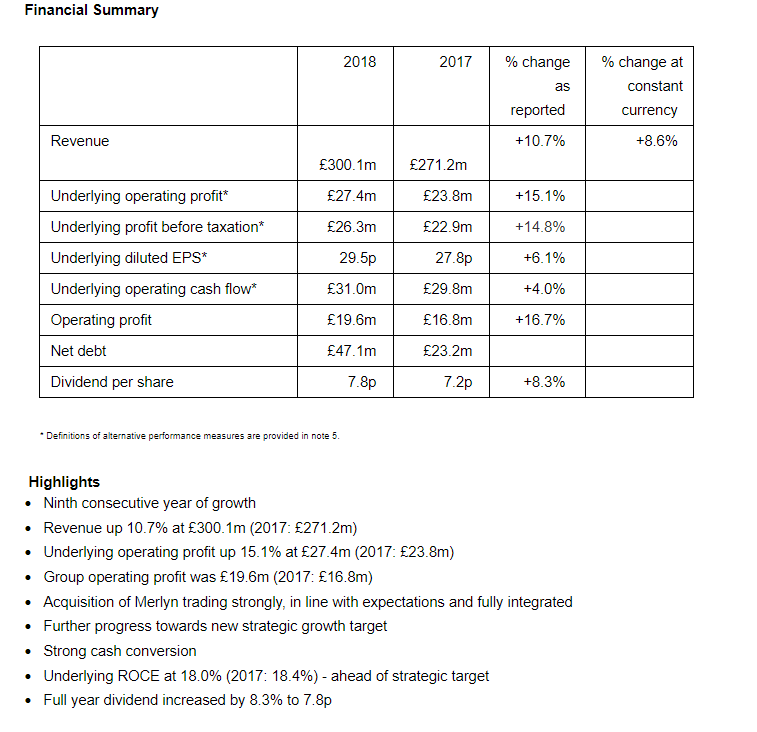

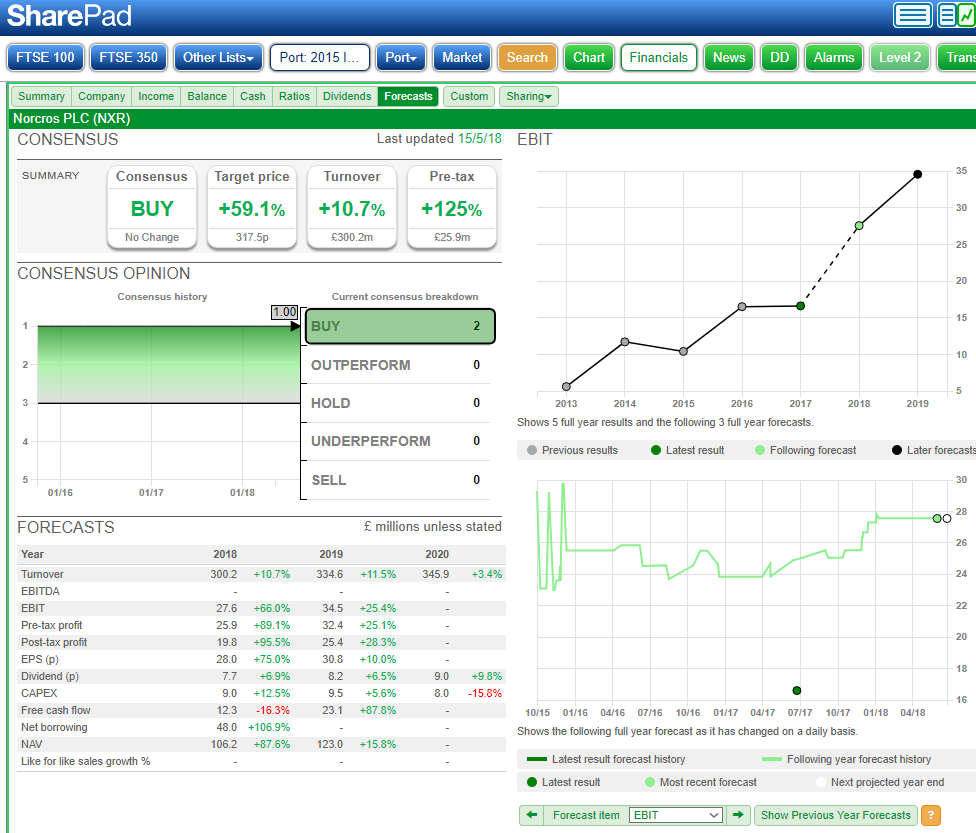

Although I don’t remotely claim to be a forensic accountant, I am after all a chemist by profession, I firmly believe that any investor who takes the time can dig around in the dirt to get a picture of what is really going on. In a good number of cases, if you take the time, you may well have a better picture of what’s going on with a stock than many of the brokers/analysts. Oh heck, why not, a few examples of companies that have exhibited some of the above traits in my opinion: ADT, CLLN, UTW, TRAK, TSCO, TCM, TSTL, CALL, VCP, VRS I should say that these are only a very brief example and I could actually produce a very long list to bore you with. Indeed, I have held a couple of those companies above. In fact, I made a very good profit on TSTL but sold when my fag packet told me that once the boys had been rewarding themselves and adjusting profits (sorry lads, share-based payments are remuneration in my book), profits look a touch flat. I did not own VCP but it was on the watch list. VCP alarmed me with the following in the Outlook statement from the CEO “I often hear non-shareholders worrying that they have "missed the boat" with Victoria - although I am at a total loss to understand why they would think that”. Indeed since that July statement, VCP has been down from its recent highs by as much as 50% in mid-October. The above are just some of the things I look out for in RNS or other communications by companies. Anyway, after a fairly quiet period, no RNS Log for three weeks as there has been very little to talk about, let’s have a look at what has been going on with Voyager stocks in recent days: Wednesday 07/11/2018: ITV: Mkt Cap £6bn: RNS Trading Update My View: finally lost patience with ITV after holding for quite some time and following this “dressed up” trading update, a little bit of digging and removing the cosmetics suggests that the ugly sister remains the ugly sister and maybe nobody will come along to buy her and take her out of her misery. Sold for a loss of 10%. Note: I never feel bad about taking a loss, especially one of 10% or less as part of the key to successful investing in my view is the protection of capital by jettisoning underperformers from the good spacecraft Voyager. Tuesday 13/11/2018: AdEPT Technology: ADT: Mkt Cap £88m: RNS Interim Results  My View: well the Poppycock EBITDA all looks impressive enough but that no surprise as Poppycock earnings are designed to impress, paint a potential ugly duckling as beautiful and just maybe mask what’s really going on underwater with our duck. So with my dislike of EBITDA claims and armed with the trusty fag packet I did dig a touch into the interim figures. Without boring you with the full conclusions of said fag packet, I am not overly impressed as I am left with the feeling that the true profits i.e after removing adjustments are only just sneaking up via the recent acquisitions which in themselves don’t appear that exciting and the pre-acquisition business is not doing what I reckon it should in order to comfortably make their full-year figures. Overall, for me, I get a whiff of more adjustments being needed to get anywhere near the full year expectations with Poppycock EBITDA in full flow. I may well be wrong but I sold at a 5% loss on my fairly recent purchase: again, if I don’t feel comfy with a stock, it’s cast out into outer space to drift. If I am wrong, I can always go back in again but rather suspect that I will listen to my reservations about cocky CEOs; indeed for that reason, it was a hesitant purchase in the first place. Wednesday 14/11/2018: AB Dynamics: ABDP: Mkt Cap £270m: RNS Final Results  Outlook Since its formation in 1982, Anthony Best Dynamics has gone through many changes to establish itself as a market leader in its targeted segments within the automotive R&D market. Our customers remain very active in introducing ever more complex ADAS equipment into their vehicles and in the development of semi- and fully-autonomous vehicles. Vehicle safety standards continue to evolve under Euro NCAP and NHTSA and their safety ratings are expected to continue to include more and more ADAS and crash avoidance systems, such as future Autonomous Emergency Braking and Autonomous Emergency Steering developments. Despite our very strong growth, order intake has continued to run ahead of sales and this has provided the Group with a healthy order book into our new financial year and, as usual, visibility into our third quarter. Against this pleasing backdrop, our progress continues to require ever greater investment in systems and our operational capability to ensure that we are fully capable of supporting current and future growth. In the coming year we expect to make further investment in new product development, marketing, service and support, our growing overseas footprint and, of course, our people, whose skills and energy remain so important to our future success. Inevitably this investment will provide some constraint to our operating margin, but the Board remains confident that, under the leadership of our new CEO, we are positioned to deliver a year of solid progress. My View: well nice to see relatively clean numbers and what appears a very good set of finals from one of my medium-term portfolio holdings, bought in mid-2016 and topped up since. The headline numbers are reported in almost real money as PBT, I say almost real as we have adjustments for those naughty little remuneration tricks; whoops, I mean share-based payments. Strangely this time around if you deduct share-based payments from this year and last years PBT calculations, which of course we really should do, rather than an increased PBT of 45% as published, you get a more meaningful figure of 79% which is simply outstanding. My fag-packet calculations also suggest that the lease adjusted ROCE has risen from 19.7% to about 22.5% & the EBIT margin at 23%; nice! Note: as the drag of capital expenditure reduces in the next couple of reporting years, I expect the ROCE to return to around the 30% level. The new facility at Bradford is now fully functional and demand for the product is high (implies that demand may well outstrip supply, what a lovely position); an outstanding business in a niche area; happy days! Incidentally, I have seen so much ill-informed crap written about ABDP via various sources including social media that it totally reinforces my fundamental belief that to have success in this private investing game you must cut out the noise. Simply study the figures and the RNS news flow and if you are minded to, talk to management. I have to admit that I took the opportunity to top up my holding of ABDP during the October market falls. Thursday 15/11/18: Norcros: NXR: Mkt Cap £176m: RNS Interim Results  Summary and outlook The Group has delivered a substantial increase in underlying operating profit in the six months to 30 September 2018 against the backdrop of a challenging trading environment in our key markets. This growth reflects the successful integration and performance of the recently acquired Merlyn business, the return to profitability of the Johnson Tiles UK business, the strong performance of our market leading Triton business and share gains in a number of our other brands. The robust performance in the first half continues to demonstrate the strength of our market positions, our leading brands and the financial resilience of our diversified business model. The Board remains confident that these attributes will continue to drive market outperformance and will enable the Group to make further progress in line with its expectations for the year to 31 March 2019. My View: A very good set of interims and yes, of course, the dreaded Brexit virus gets a cautionary mention. Anyway, as I say the results look good and NXR delivers a confident in line with expectation outlook for the remainder of the year. I should also make a mention of the pension deficit. In my mind, the worries about this deficit have been greatly overplayed by the market in recent years and that opinion I have offered in this log for the past few years. The scheme is a mature one with the average age of around 80 and as seen in these interims, the pension deficit aided by a 0.3% increase in the discount rate has fallen from £48.0m at 31 March 2018 to £28.8m at 30 September 2018. I will continue to hold NXR. Thursday 15/11/2018: Bodycote: BOY: Mkt Cap £1.5b; RNS Trading Update Summary and outlook in the Trading Update As anticipated, the pace of revenue growth will moderate in the last two months given the strong prior year comparator. Bodycote's outlook for 2018 remains unchanged. My View: a decent enough trading update for months 7 to 10 of the trading year. In the first 6 months of their financial year BOY had a turnover of £368.0m & months 7 to 10 was £243.5m giving a banked turnover of £611.5m leaving a gap of £115.5 to meet revenue expectation for the full year; fairly easily satisfied in my view. I am happy enough and will continue to hold. Thursday 15/11/2018: Dart Group: DTG: Mkt Cap£1.4b: RNS Interim Results   Outlook

With winter 2018/19 Leisure Travel bookings in line with expectations and notwithstanding the important post-Christmas booking period that is still to come, the Board expects current market expectations for the year ending 31 March 2019 to be met. Looking ahead, significant cost pressures such as fuel and other operating charges, plus the necessary continued investment in our products and operations including that required to retain and attract colleagues, are emerging headwinds. This, coupled with the overall uncertain UK economic outlook particularly related to Brexit and how it may impact on consumer spending, means we remain unclear how demand will develop in the medium term. However, our strategy for the long term remains consistent - to grow both our flight-only and package holiday products. On the assumption that the UK Government secures a pragmatic and balanced Brexit agreement with the EU, the outlook remains bright and we continue to have confidence in the resilience of both our Leisure Travel and Distribution & Logistics businesses. My View: well a fairly stunning set of half-year results as DTG become a really substantial player in air travel and package holidays. However, as good as these results are and with the company saying that they expect to meet full-year expectations, Mr Market predictably acted in slight panic mode latching onto talk of emerging headwinds & the routine mention of Brexit. So, lets cast back to the interims of 2017 when the company made similar comments “However, we are seeing the emergence of certain cost pressures as we continue to invest in our airport operations, colleagues and other related areas. Nevertheless, and despite the current uncertainty around the "Brexit " negotiations, we remain confident in the resilience of our Leisure Travel business, supported by our recent elevation to the UK's second largest Package Holiday Operator”. Essentially repeating most of what had been said a year ago i.e it’s usual cautious guidance and following the 2017 interims the share price appreciated by some 50% over the next 12 months. The company also mentions in these 2018 interims that they are investing in new aircraft and staff in order to continue their expansion; all suggests to me that the long-term future is rather bright for DTG. I will continue to hold DTG a stock that I first bought at just over 200p back in 2013. I still view the stock as a bargain at just over 800p but won't really know if my view is right or wrong until about a years time. Top-ups and new holdings: The following portfolio stocks have been topped up a touch in October/ early November: using just a little of the cash pile at what I considered to be bargain prices in the last three weeks: BVXP, KWS, PMP, DTG, ABDP, XPP & IGR (at below £5): I consider these small top-ups prices to be at rather attractive prices but the question is will there be more Brexit damage still to come? Only time will tell but it seemed reasonable to use a little of the cash pile whilst keeping a large chunk in reserve. New position: after such a good write up by Rhomboid on Twitter, Goodwin GDWN. I should say that I do see a difference between listening to the thoughts of a seasoned & respected investor and don’t consider this as noise. Leavers from the Voyager: LGEN, BKS, D4t4, SPSY & HSL: in all cases very decent profits were taken. Two stocks sold at very small losses: ITV & ADT: overall a very profitable effect on the bottom line delivered by the leavers. I did say early in the year that I thought the storm clouds were gathering and hence my move from the spring heavily into cash. Sadly, I rather feel that the degree of uncertainty thrust upon the UK by this “Brexit dogs-dinner” has the potential to turn into a fairly serious storm; we will see. I have to say that I just feel more comfortable holding a small number of stocks, currently standing at 12 stocks until we either move away from the Brexit cliff or start to bounce into recovery after falling over the edge of that cliff. Boringly as ever, I will say that it's been a brilliant run over recent years and at times like this it’s prudent to preserve profits and protect capital. Of course, having a relatively small number of stocks will reduce the frequency of the Voyager RNS log appearance and I would guess that until the walk along the cliff edge is negotiated, it will be more like monthly. Well, that’s it for this week, I will be back when there is something to report on and in the meantime will use my Voyager absence to add other parts to the StockWhittler site. Have a good weekend and as ever, Happy and risk-averse investing!

0 Comments

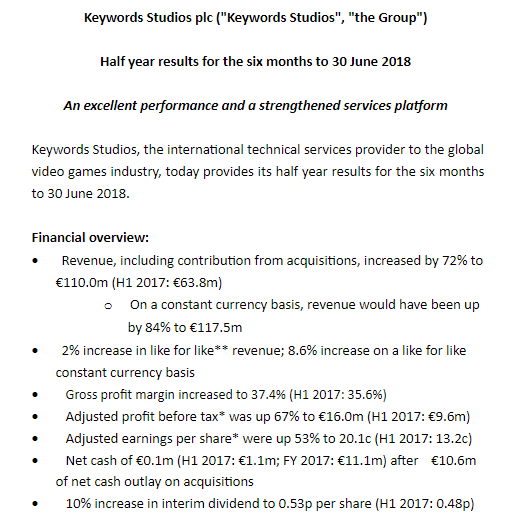

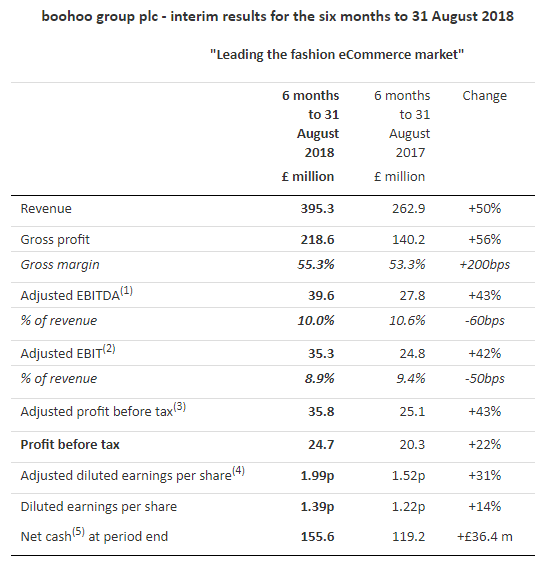

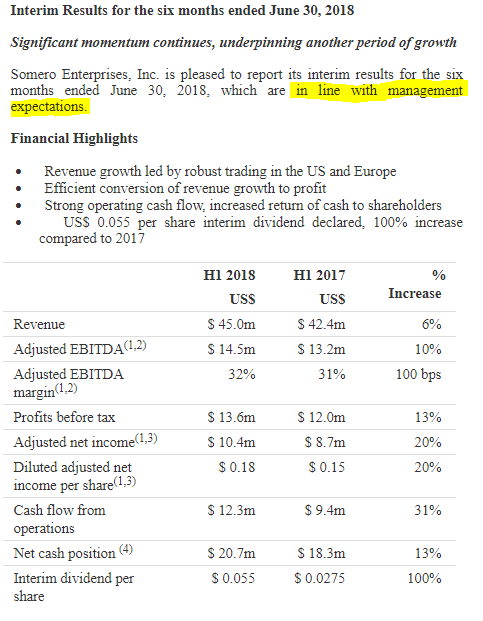

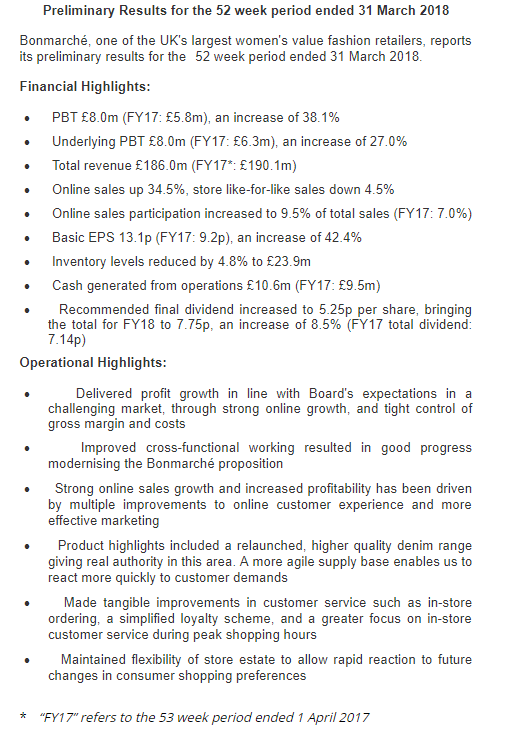

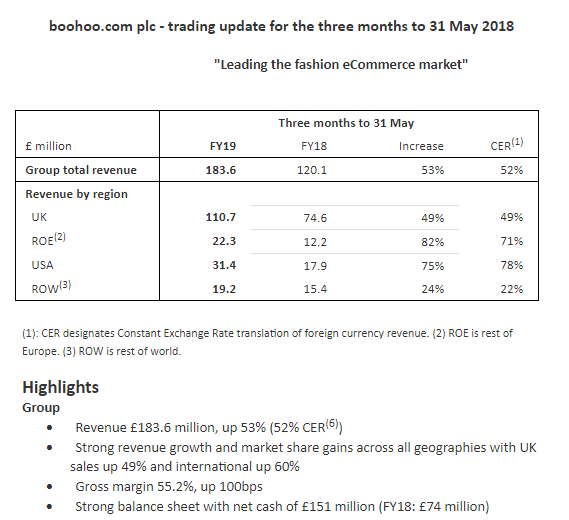

Voyager RNS Log Weeks Commencing 14/10 & 20/10 of 2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. In my last Voyager Log written two weeks ago, I commented that Mr Market had the jitters as displayed by the fall in all of the major LSE indices. Since that time, Mr Market has continued to fret and all the indices have declined further; more so here than on Wall Street. It just seemed so predictable to me back in the early summer that our EU/UK politicians were going to make a dog's dinner of the whole negotiation process. Oh, my apologies to any dogs that may read this log as I am sure you have far more sense than our glorious political leaders on both sides of the channel. Currently, I am feeling fairly vindicated in moving heavily into cash over the last five months. I still retain some attractive stocks and just like fellow investors holdings, these have declined a touch as the overall jitters continue. However, any bottom line decline is not that painful as it is heavily cushioned by the cash under the mattress. That cash will be used and gradually reinvested once the imbeciles settle down and agree on a way forward for the UK. However, with the world of the private investor, there is always something on the radar that may cause turbulence and with that in mind, I wonder how much longer the ridiculous single currency of the EU will last for. Something to look forward to I suspect. I repeat myself time and again; yes, ok, no need to agree! Firstly investing is a long game, it’s not a race. It does not matter unless you are selling of course, what your portfolio’s performance was yesterday, last week, last month, this year etc: what matters is you return over three or five years. Secondly, yes boring again, the application of risk management to one’s portfolio and by this, I mean having a risk management plan to protect your capital. Again on social media, I see that many folks are licking their wounds as their profits decline. If you invested at the top of the market then my sympathies, it happens: stocks go up as well as down. On the other hand, if you have less profits now than you had a few weeks ago, take comfort from the profits you have accumulated in the last 3,4,5 years of this friendly bull market: I suspect that overall most investors have done very well over the medium term. During turbulent times like we have been experiencing since the start of October, newsflow from companies is almost irrelevant in that even good news is insufficient to halt the gradual slump in stock prices. In fact, in terms of newsflow, it’s been rather light for the Voyager and this is down to having a reduced number of positions plus simply very few RNSs appearing. Oh, I should say that all my spread bets have now been closed for a couple of months: in my view, open spread bets at the moment are really too much of a gamble. Sometimes I tend to think that the words of the song Private Investigations, written by the excellent Mark Knopfler, sums up the logic of our friend Mr Market: well any excuse will do for me to play a few tunes by Dire Straits, the lyrics: It's a mystery to me, the game commences for the usual fee plus expenses, confidential information…….. I go checking out the reports, digging up the dirt, you get to meet all sorts in this line of work. Treachery and treason there's always an excuse for it and when I find the reason I still can't get used to it….. Now for a quick look at the few RNSs relevant to the voyager over the last two weeks: I won’t go into the usual detail as anything apart from a premium takeover bid causes a stocks price to decline at the moment. So, more of a summary note plus a few observations on some stocks that have been jettisoned from the Voyager in recent months as profits or an occasional slight loss taken: RNS newsflow from stocks currently within the Voyager: Tuesday 16/10/2018: IG Design Group: IGR: Mkt Cap £430m: RNS Trading Update: My View: a very sound update from what I consider to be quite an exceptional, high-quality business run by competent managers capable of communicating openly with investors. The trading update reads very positively with progress in all geographical areas and branches of the business. The big acquisition of Impact Innovations is performing well and I suspect will perform even better now it’s in the IGR stable. Overall, currently IGR is performing in line with management expectations but I have a sense that they will have an outturn at the top end of those expectations. I am happy to continue and touch away just a smidgen more of share price weakness. Thursday 18/10/2018: Games Workshop: GAW: Mkt Cap £1010m: RNS Trading Update: Following on from the Group's update in September, trading to 7 October 2018 has continued well. Compared to the same period in the prior year, sales are ahead and profits are at a similar level to the prior year. However, the Board remains aware that there are some uncertainties in the trading periods ahead for the rest of the 2018/19 financial year. A further update will be given as appropriate. My View: well according to my fag packet calculations when comparing actual to broker expectations, GAW is performing a touch ahead of expectations: the broker consensus was for a slight decline. Ok, so far so good, but then Mr Market frets about the “uncertainties” comment yet two things here: firstly that style of comment is now almost commonplace in company RNSs as the country struggles with the Brexit plague and secondly it’s the very same comment that GAW included in a trading update back in July 2017 yet Mr market worries!! Even worse still, I got a web copy of an article published by a journal that people actually pay for saying that the trading update was an unscheduled one; what utter nonsense as anybody who reads RNSs will appreciate. Do you own research and by all means test your thoughts with other respected investors but don’t blindly follow the shoddy work of journalists. Well after that little rant, I am more than happy to continue to hold. Monday22/10/2018: D4t4 Solutions: D4t4: Mkt cap £77m: RNS Trading Update Briefly: Adjusted profit is expected to be comfortably in line with management expectations & also confirmation of a strong cash position. My View: yes indeed a sound update and even Mr Market is his mean mood grudgingly let the shares rise a few %. My current batch of D4t4 was bought at 118p and despite a decent appreciation, I am happy to continue to hold as the valuation does not look overstretched and the returns on capital attractive. A few brief thoughts on stocks I have sold in recent months and NO LONGER HOLD who have issued RNSs recently: Softcat: SCT: which I sold at 846p as part of my derisking exercise, issued a reasonable trading update but with a note of caution: the shares are now at 670p. Good company and one to maybe return to later. Tristel: TSTL: a stock that had been very kind to me and my final batch was sold at 275p again during my Brexit risk management plan. TSTL issued final results which looked reasonably decent but lacked the USA market penetration evidence and the shares duly fell back to 210p: they were at 340p at the end of June. Again a very nice business but maybe a touch overly generous in terms of management rewards; silly me, I thought the directors were happy to simply work hard for a decent salary! Sadly and so many companies are doing this, we have adjustments for share-based payments. Once you consider share-based payments as simple remuneration, the PBT for Tristel is actually flat year-on-year and not the +15% adjusted claimed. Where did the 15% go, yes, to the directors/staff as remuneration which is simply a true cost to the business! RWS issued a confident trading update with revenues driven by that exciting acquisition of Moravia back in November 2017. I think I was right to sell at the time of their indigestion RNS at the end of April but maybe I should have bought back in when things improved. A quality business worth keeping on my watch list. Zytronic: ZYT: issued a run of the mill profits warning. Unfortunate but not totally unexpected from this rather nice well-managed business. I had held ZYT for a long period but the final significant batch left the Voyager last October when the share price became a touch overheated for my liking at 580p. Again a lovely little niche business but with an over-reliance on a small number of customers and difficult to forecast (potentially lumpy) sales. Patisserie Holdings: CAKE: well the snippets of news keep emerging and the extent of the fiddling may even go deeper as we now hear of nondisclosed share awards to directors. I won't comment further other than to say I am so glad I followed my gut instinct back in September 2017 when after visiting Patisserie Valerie I asked myself “so, where are all of these supposed customers; why aren’t they crowding out this near empty shop”? As ever, I sincerely hope current holders have something when the shares come back from suspension. Air Partner: AIR: issued interim results which looked fairly ok but after making some decent profits on AIR in the past, I just can’t get excited about a firm that loses some hefty invoices and seems to have systematically covered it up in their accounts for a few years: not for me, why take the risk? Finally, on an ex-holding XPD sold at 78p taking profits in August again as part of my Brexit risk management, the share price has during October fallen by some 40% yet no worrying RNS; strange times! A bargain now or further to fall? As Mark Knopfler of Dire Straits would sing: It's a mystery to me, the game commences……… I hope these notes encourage a few investors without an investment management plan/risk management strategy that just maybe having one is worthwhile. Things will every so often jump up and threaten your wealth on the markets; you can’t change that, it will always happen. Something you can do is be prepared by having a carefully thought out plan that you can execute in a cool collected fashion if required and believe me, every few years it will be required. Well, that’s it for this week except to say I have made one very significant purchase and a few little top-ups to current holdings. The significant purchase was some lazy money for the IPO of Smithson which gives me some global exposure within an IT to what in Terry’s terms are smaller and mid-cap global companies; in my world, they are fairly significant market cap companies. This weekend, despite industrial action on some trains, I am heading down to London for the Hatters game against AFC Wimbledon; hopefully, I will arrive in London early enough to make an interesting day of it. Whatever you are doing, have a good weekend as we turn the clocks back; never a good feeling is it! As ever, happy investing! Voyager RNS Log Weeks Commencing 06/10/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Well, Mr Market has certainly got the jitters these last couple of weeks and can any investor genuinely be surprised as we head towards Brexit with so many uncertainties and remember Mr Market does not care too much for uncertainty. Since it’s high point in mid-May 2018, the FTSE100, FTSE250 and FTSE All Share are all off by around -11% with a similar story on the AIM100 down by -14% in just a few days with the FTSE AIM All-Share down by -12% since the start of October. Now I note that a fair number of investors on social media are posting how dreadful the market has been this October with losses of x%. What I always say is that your performance over 1 day, 1 week, 1 month is of little relevance and will almost be forgotten in a year or so from now. Performance needs to be measured over to my mind, a minimum of 3 years and I suspect that many private investors feeling a little pain at the moment will have done very well indeed over the last 3 or 5 years: it’s a long game, not a sprint. I would suggest that investors don’t thrash themselves over performance so far this October; it’s investing and these things happen! Any regular readers of the Voyager will know that from early summer I have been derisking my portfolio and moving more and more into cash at least until this Brexit debacle reaches a conclusion with some visibility on the way ahead; currently I am about two thirds in cash, that’s the highest cash position since the dark days of the 2008 financial crisis. Now, I am not saying that we are about to hit another massive drop as in 2000 or 2008 but rather saying that having invested through those tough periods, that I appreciate the security of cash until the storm has passed. Incidentally, I have been writing about the gathering storm clouds since early summer and I have been banking some very decent profits rather than take unnecessary risk. The storm that has arrived whilst it‘s having an adverse impact on the smaller number of stocks that I hold but this is greatly buffered by the cash pile. For what it’s worth, I see this current drop as more of a combined wobble coupled in the UK with Brexit worries some of which will pass when we have an agreement with Brussels regarding the terms of our departure. Uncertainty is never a good thing for the markets and we are currently being hit by Brexit worries. I am not about to do a Tim Martin style rant or defend the views of either camp but rather comment on my sadness in that our politicians have strived to cock things up right from the fake-news of the Brexit campaigning to the plans for departure. To ask the public to vote on such a complex issue back in 2016 was to my mind simply political abdication for short-term party gain. If the voting public makes a regrettable mistake in a normal election, then we only live with the consequences for a few years. With this vote, we live with the uncertain consequences for generations to come. Just my view but any referendum much more complex than “red sauce or brown sauce on your sausage sandwich” is a just too complex for folk to anywhere near handle. Yet here we are and as investors are confronted with such uncertainty, I would suggest it wise to have a plan other than bury your head in the sand: a plan that may review the situation and maybe take no action is a plan but to simply not have a plan is not that wise. My approach, when faced with this type of uncertainty, is to derisk, head for cash and then try to take advantage of a future market upturn. Profits have been very good in the last few years and indeed 2018 whilst not been stunning, has been fair. So, my approach is as ever to take some profits, reduce exposure in uncertain times and protect your capital. Currently, the Voyager carries only a relatively small valuation of stocks and certainly the lowest percentage for quite a number of years. Myself, I just don’t buy into this outdated argument of avoiding dealing costs by simply holding. That argument may have been true 25 years ago when dealing charges were so high but these days that are almost insignificant. A simple truth of investing is to ride the wave when it's in your favour but simply don’t stick around and be greedy when the wave changes direction. So at the moment I will sit on the cash pile as it were, and wait for the shakeout to play out before I go bargain buying. I do suspect that many relatively new private investors, let's say those from 2010 onwards are feeling a touch wobbled at the moment having experienced a run of fairly fruitful years until 2018 but this is the normal world on investing. We can't expect outperformance every year; this is simply business as usual. Well, that’s enough joy, let's take a look at what's been going on with the Voyager and its such a shrunken Voyager in terms of positions held that I may well also look at some previous holdings that were jettisoned over the past year. Monday 08/10/2018: Bioventix: BVXP: Market Cap £155m: Final Results  My View: the results in terms of how the company has performed looked absolutely fine; so all good or indeed very good for the year ended. However, I did in early September have this nagging doubt in my mind due to the company not issuing a trading update with possibly a teasing paragraph or two on the troponin project with Siemens. The comment in the results on this project was a little reserved and as I always bang on about risk, I halved my position in BVXP @ £31 which means that my residual holding, rather like that in KWS, is now riding for free. I really do like BVXP but just feel that that degree of uncertainty will be a handbrake on the share price in the coming weeks and as I have written before, we have enough uncertainty around anyway. If promising news follows regarding troponin then I can always buy further shares and enjoy a less risky ride. Monday 08/10/2018: XP Power: XPP: Mkt Cap £550m: Trading Update: A couple of lines from the TU Order intake for the nine months ended 30 September 2018 was robust at £153.3 million (2017: £137.5 million) which was 11% higher than the prior year on a reported basis. In constant currency this was an increase of 18%. On a “like for like” basis, removing currency effects and the impact of the Comdel and Glassman acquisitions, order intake increased by 8%. Order intake remains healthy, although the rate of growth has moderated slightly during the period. Production volumes in China and Vietnam remain robust and we are encouraged by our design win pipeline and overall momentum across the business. The Board anticipates the Group’s performance for the full year will be in line with its current expectations as outlined at the time of the Group’s interim results on 30 July 2018. My View: XPP simply continues as a quality business with a decent enough in-line trading statement. Yet the market has the jitters and the price has continued to drift. It all seems solid enough to me and is simply out of favour in this nervous market. I will continue to hold. Wednesday 10/10/2018: Telford Homes: TEF: Mkt Cap £290m: Trading Update: It was a cautious update painting both some positives and some uncertainties and if anyone was shocked by what was said then goodness knows where they have been for the last few months. The positives were that Telfords houses in London are of the more affordable end of the market and should continue to sell. The more difficult end of the market, the higher priced houses are proving more difficult to sell. My View: Well, over recent months I have taken very good profits on housebuilders and TEF was my one remaining housebuilder stock but the TU although written very honestly, just leaves too much doubt for the immediate future. Regrettably, as Lord Sugar would say, Telford has been fired, I really like the business as I have written or bored readers within the past but that sentiment will not stop me from making the unemotional decision to sell and escaping with a small profit. Maybe I will return another day! On the day of this RNS I felt it a little odd that other housebuilders had held up fairly well on the day and was tempted to short a few. The other builders duly fell the following day. Thursday 11/10/2018: Norcros: NXR: Mkt Cap £162m: Trading Update  My View: to me this looks a sound enough update from NXR and as their strategy projects, the real growth comes from acquisitions with group LFL sales excluding the Merlyn acquisition down by a small amount -0.3%. If we do a quick “fag packet” estimation of this H1/H2 stretch we see the ratio as 2.05 which compares well to the same 2.05 ratio averaged over the last three years for H1/H2. The stock is on a very undemanding PE of 6.2 with a yield of 4.3%. Although I sold half of my NXR holding in the application of my derisking strategy in recent months, I am happy enough to hold the residual 50% in the Voyager; it’s been a boringly yet steadily profitable stock over the years. A few thoughts on stocks I once held that have issued RNS this week: Note I no longer have positions in these stocks but have covered them in some detail in the Voyager Log together with my reasoning for selling them at the time. Firstly Amino, AMO, who issued a profits warning on Monday 08/10/18. The reason I sold and reported my concern in the Voyager was the rather large H1/H2 stretch required to make their numbers for the year. To do this, simply take a look at historic H1/H2 ratios, then take into account any mitigating circumstances and ask yourself if the H2 gap can with reasonable confidence be closed. With AMO, which is a decent business, in my opinion, I decided that it was a stretch too far and sold. Secondly Patisserie Valerie, CAKE, where I had an almost surreal experience that day in Lincoln with queues at some other coffee shops yet hardly anybody in Patisserie Valerie: odd I thought, maybe just an anomaly as their reports suggest good customer numbers? After my acceptable but slightly expensive breakfast at Patisserie Valerie, I then moved on and had a couple of pre-match beers with a group of friends and their partners where we got onto the subject of Patisserie Valerie and surprise surprise, their experiences at outlets in other locations were similar to my own. I decided that all may not be as well as I would have hoped, I just did not feel comfortable and if I don’t feel comfortable I get out: a few days later sold all of my entire holding in CAKE for a 20% profit. Now I appreciate that this was not in-depth analysis and to be fair their accounts looked fine but often such observations can give you an indication of how well a business is doing. For example, the almost always empty Carpetright stores or Halfords a couple of years ago contrasting with the crowded “always have to queue” WH Smith travel shops: simple stuff but often of real value. For shareholders expecting a trading update at 7am on 10/10/2018, the black clouds began to form with a 7:30 am RNS which gave nothing at all in terms of current trading but simply said that he shares were to be suspended from AIM until some serious financial irregularities could be sorted. On a newscast the previous night there was a suggestion od a £20m black hole in the accounts. Further bad news was to follow during the day with a second RNS concerning a serious tax issue for one of the group companies. Then in the early afternoon of 11/10/18 another RNS saying “Without an immediate injection of capital, the Directors are of the view that there is no scope for the business to continue trading in its current form”. What happened to one of the attractions of Cake, the self-funding of the rollout of new shops? Also what a real slice of luck for some of the directors in selling over £20m worth of shares earlier in the year! I really do hope this “difficulty” is resolved soon; maybe Luke Johnson can sort something out and rescue the business and leave holders with something? A very sad position that I doubt anybody could have detected from the accounts. My commiserations to all involved, shareholders and staff alike; just glad I popped in for that pre-match breakfast, I simply felt uneasy after my on-site visit and talk with friends who had used PV: I got lucky; no skill involved at all. A quick look at another stock I sold due to an unusually high H1/H2 stretch being required to meet the market expectations; OTB. This stock and my reasoning was also covered in an earlier Voyager article back in May this year. When I looked at the H1 figures it told me that there was simply too much risk involved to remain as a holder as the H2 stretch was just too much. I sold at some distance above 560p. The market was slow to react but eventually did; hot UK summer etc and the shares fell to below 420p, a slow but steady decline of over 30%. Yet OTB were rather skilfull in managing market expectations slowly down from a turnover of £102.7m to £95.4 and sweetening the associated profits decline with a cut back in costs. Hence to my mind, derisking their likelihood of issuing a profits warning; that’s clever in my book! Then we have an RNS on 16/08/18 telling us that the profits will be broadly in line, a phrase which means slightly below, expectations. This was sweetened again with another snippet of news in the form of a tasty acquisition and the shares rose. Now I am not saying that OTB is a bad business, far from it, all I am saying is look closely at the newsflow from the business and do a fag packet calculation for yourself. If you do, you may find yourself way ahead of some of the analysts. Incidentally, I still reckon there may be a slight sting in the tail to come with OTB but I could be wrong. Well, that’s all for now. Have a good weekend and as ever, happy investing whilst remembering that it’s a long game and not a sprint. Voyager RNS Log Weeks Commencing 16/09/2018 & 23/09/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. After the game at Blackpool last Saturday, I had a few days away walking in The Lake District; I never need much of an excuse to visit some of the lovely locations in the UK and try wherever possible to blend it in with an away game. Sorry, I am in relaxed mode and drifting along but a point that I was mulling over when walking was how long does one really want to stay active in the market? After you have reached a point of sustainable comfort why do investors continue to strive for more and more? Why do Buffett and the like keep investing when the financial need has long been satisfied? What keeps such investors going? Why do folk such as Bezos of Amazon keep accumulating massive fortunes yet have such unhappy staff? Lots of questions yet no real answers that I can come up with but nevertheless interesting. Oh well, time for another lazy chunk of loot to be looked after by Terry Smith within his new Investment Trust, Smithson. I already have a sizeable holding, which I have held for a good number of years, in Fundsmith and indeed I use it’s excellent performance as one of my benchmarks. This IT will concentrate on “small to mid-cap companies” that Terry defines as between £500m & £15b but typically around the £7.5b market cap” which still to my reckoning are pretty substantial businesses but not the giants ROCE players of Fundsmith. Terry’s approach is difficult to fault giving an outstanding performance for lazy money since inception. For that reason, I rather expect the IT may trade at a premium to NAV; I do so much prefer Its over Unit Trusts/OEICs. General view on the markets: Still in my view, a degree of uncertainty lingering over the market and I rather doubt that will disperse until the UK’s future in its ongoing relationship with the EU is resolved. The FTSE All-Share index is down about 2% since the turn of the year and has experienced a fair amount of volatility and at one time was down by around 10%. So, most definitely a stock pickers market but as in my case with plenty of powder kept dry. Just a thought on software: whatever type of financial software you use, it’s so important in my opinion to become really familiar with all the facilities it offers. My favourite by some distance is SharePad but like anything, you really need to invest time learning how to get the very best out of the system; works so well for me right from the early morning RNS filtration to historic and current financial ratios. In a couple of previous Voyager logs, I have mentioned before the investment book I am bringing together that will cover 25+ years of my investing journey, approach, protection of capital, market timing and many other points learnt from both making mistakes and learning from the best investors. I am currently tinkering with a title, rather irrelevant I know, maybe the hitchhiking investor, maybe the hitchhikers guide to the investment universe; who knows! I hope to update in a couple of weeks time progress and then start to introduce the book by modular chapter/subject on the StockWhittler site. It’s not designed to be an “oh what a clever dick I am book” but rather a book that will aid some in their own investment journey. Onto the RNS log which does really remain a little sparse as there is just not much in the way of announcements recently. I am pleased to say that I dodged the bullet with respect to Bonmarch BON which issued a profits warning on Thursday 27/09/2018. I sold BON for a 25% profit at the end of July as a started to seriously reduce risk & exposure in the Voyager. I feel there are times to be fully invested and times to be cautious and at the present time, I place a lot of faith in the protection of profits. Tuesday 18/09/2018: Keyword Studios: KWS: Mkt Cap £2.2b: RNS Interim Results & a 2nd RNS regarding the acquisition of the Sound Lab and also The Trailer Farm: The key numbers  Outlook: Trading in the second half has been good and we expect to meet market expectations for the full year before the positive impact of any additional acquisitions. My View: every time I write about KWS it seems that the market capitalisation has gone up appreciably since the last time I hit the keys. When I first wrote about KWS it’s market cap was a touch over £100m we now have it bloated to over £1.2b is it grows at a speedy rate both via its highly acquisitive nature and organically. Is it pricy? Well, you could argue that it is but then how many companies are there on the LSE with such a proven track record at this high level of market capitalisation with such a great growth story. As for the acquisitions, in the early days of holding KWS I visualised the risk of the boardroom with all of those spinning plates on sticks representing each of the many acquisitions; these days, I take comfort from the excellent track record that KWS have of integrating these many bolt-on businesses. Unlike many companies, the CEO of KWS Andrew Day does a very good job of communicating with investors and the excellent PI video gang have again given Andrew a platform to discuss the results with investors. I am happy to continue my free ride and will keep holding. A link to the excellent PI World video where CEO Andrew Day talks us through the interims and discuss progress may be found on the following link: www.piworld.co.uk/2018/09/18/keywords-studios-kws-h1-results-september-2018/ Wednesday 19/09/2018: Games Workshop: GAW: Mkt Cap £1.25b: Trading Update: Games Workshop Group PLC announces today that trading is in line with the Board's expectations. Cash generation also remains strong. My View: although I normally dislike the approach of releasing an RNS on trading other than at 7 am, this looks absolutely fine. Its very simple, very concise yet the initial market reaction was subdued. I just reckon that many punters expect to see “Ahead….” Time after time. However, no matter, the shares duly pushed ahead over the next few days and even topped the £40 mark. I am happy to hold and just possibly for a rather long time. Then on Thursday after markets closed we had another RNS informing the markets that the ex-chairman Tom Kirby was selling via a placing in the order of £20m of shares. The shares were within an hour of that announcement at £36-50. That sale will probably have a little knock on the share price and maybe offer an opportunity for a little top up. Monday 24/09/2018: Spectra Systems: SPSY: Market Cap £49m: RNS Interim Results:  Commenting on the results, Nabil Lawandy, Chief Executive Officer, said: "The Company's revenues for the first half of 2018 are 11 % higher than 2017 and were driven by delivery of a large G7 customer order and royalty and license revenue from our agreement with a major banknote supplier. As a result of our operating gearing adjusted EBITDA for the first half of the year is markedly higher, 30%, than last year resulting in strong midyear profitability. The continued in line performance of the Secure Transactions Group as well as Brand Authentication puts the company in a strong position to meet market expectations for the full year. The delivery of two quality control devices to a tobacco manufacturer has increased our chances of introducing our TruBrand smartphone authentication technology in China. This is in addition to the recent allowance by the United States Patent Office of our patents on this technology. The Board therefore believes that the Company, by achieving key business milestones, will continue to perform well for the remainder of 2018 with excellent prospects for ongoing earnings growth thereafter." My View: well I have held SPSY for over 12 months buying at just over 80p and making further top ups a little later. Note: I usually limit my exposure to the more illiquid stocks and tend to never hold more than one sub £50m Market Cap in the Voyager. If something goes wrong it can be so difficult to sell small-cap stocks and even ones of around the £200m Mkt Cap for that matter. Anyway, the results and outlook look absolutely fine and indeed rather encouraging in my view yet Mr Market was a touch relaxed on the news. Finally, I see that the market has decided by Thursday 27/9 that “hey these are rather good” and the shares put on a spurt to 118p. Note although I don’t select stocks via the Stock Rank (SR) system, I see that SPSY scores a SR of 82 which is reasonably comforting. It also enjoys a nice royalty stream of earnings and pays a 4% yield; fine for me I will continue to hold. Wednesday 26/09/2018: BooHoo: BOO: Mkt Cap £2.5b: RNS Interim Results  Guidance

Group revenue growth for the year to 28 February 2019 is expected to be 38% to 43%, up from our previous guidance of 35% to 40%, with adjusted EBITDA margin between 9% and 10%. We reiterate our medium term guidance to deliver sales growth of at least 25% per annum and EBITDA margin of 10%. My View: I have traded BOO a few times since the days of 25p post its early profits warning shortly after IPO. Without doubt the growth rate in revenues of the group is impressive as is the management team who certainly seem to know their business area inside out. Note: an RNS dated 17/09/2018 covered the appointment of John Lyttle currently CEO at Primark who will become as from 15/03/2019 the new CEO of BOO. The headlines accompanying the interims choose to focus in on gross margin which is indeed impressive but I prefer to look for the EBIT margin which is just down a tad by 50bps but the cash position is looking very healthy. Overall nothing to worry about and indeed a good set of results: the market certainly reacted positively to the results: note in mid-September BOO was trading at 170p, as I write this log the price has risen to 220p. I will continue to hold. For investors who wish to hear a discussion of the results then log onto: protect-eu.mimecast.com/s/yVdaCvgOQhEDREOuQnSTn?domain=webcasting.buchanan.uk.com One new purchase added to the portfolio: Adept Telecom (ADT) Mkt Cap: £90m. ADT, which has been on my radar for a fairly long time having what I believe is a good business model with recurring contract revenues, increasing EBIT margin, increasing and good CROCI, modest dividend of 2.5% covered by more than 3x FCF & the good Prof Piotroski sees it as pretty sound with a Piotroski value of 7 and also loved by the SRs well into the 90’s. An RNS of 27/09/2018 gave a rather upbeat trading statement and announced that the company was changing its name: “Included in the AGM resolutions there is a proposal to change the name of the Company to AdEPT Technology Group plc. With more than 75% of revenues being generated from managed services and IT, the board believes that this new name better reflects the products and services being provided by the Company. Should the resolution be passed, the Company is expecting the change of name to take effect from Monday, 1 October 2018”. Note: generally I am not impressed when a company changes its name e.g. Matchtech to Gattaca, Post Office to Consignia but in this case, I fully understand and support the rationale for the change in company name. Well, that’s it for now. The next Voyager log will depend upon RNS news flow which should pick up a touch as we move into October. In the next couple of weeks I expect to see trading updates from XPP, TEF, NXR and finals from BVXP. As ever Happy Investing, have a good weekend and catch you again soon. Voyager RNS Log Week Commencing 03/09/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. I enjoyed a lovely drive last Saturday taking the slow way through the glorious Buckinghamshire countryside to High Wycombe for our football match. In fact, the drive was so leisurely I even had time to drop into the Bell Inn Winslow for a coffee and spot of lunch; what a lovely way to enjoy a Saturday at the tail end of summer. I note a lot of investors are commenting on social media that the markets at the present time are somewhere between annoying and tough going. That feeling are I feel sure is being voiced by folk who have yet to experience a real bear market. Believe me when the bear growls you most certainly know about it as you watch the various indices drop in a non-uniform stepwise direction usually spearheaded by the previous overstretched darlings of the market. In those surreal days when the technology bubble burst in 2001 and then seven years later this mystery concept of toxic debt emerged, many investors stumbled around on a slippery slope totally dazed seemingly either unwilling or unable to reduce their positions to the sanctuary of cash. Today, we are suffering no more than a very minor skin rash but as we head to the conclusion of the Brexit negotiations and of course the bad boys Trump & Putin playing a game of chicken in some location of the globe when domestic boredom sets in. It’s largely to risk manage these relative uncertainties that I have slimmed down the Voyager and become cash biased. My approach to investing is not one of greed and for that reason, I am simply protecting some of the very generous gains harvested from the last few very fruitful years. If all turns out well and the markets don’t wobble, then fine, as I say, greed does not drive me. On the other hand, if we do suffer some turbulence then I have a cash pile to go bargain hunting with. What I have learnt over the years is that with investing you simply have to have a plan and that plan should consider your reaction to various events both market-wide and stock specific. To run without a plan is simply close to gambling and hoping that things turn out all right. One other thing I would say is that I think investors should not get overly envious in comparing their returns with those of others, especially short term. Your goals are yours and that includes your time horizon. You may well have an entirely different risk/reward balance, maybe you don’t need to sleep at night, maybe you manage a few £k or maybe a million or two. The approach you choose is yours and hopefully, it is well thought through and based on a style that suits your personality. I always say that your prefered style should be backed by a plan. As regards measuring returns, a year is a short period and I only taker serious interest over a minimum three year period whilst at the same time continually jettisoning the lesser performers; it seems just a simple fact that the bulk of your progress is down to a very small number of exceptionally performing portfolio stocks that should be treasured. Looking back over the years, if I have twenty stocks over a period of time it's invariably maybe three or four that do the stellar stuff, the rewarding stuff; ok, the others can contribute a touch as well BUT you can’t let that stop you from exiting the losers. Remember the great words of wisdom from Lynch/Buffett "Selling your winners and holding your losers is like cutting the flowers and watering the weeds." If more private investors could live by those wise words rather than justifying losers by keeping them as “long-term holds”, then I truly believe their returns would greatly improve. Anyway, I reckon there is just about enough RNS news flow this week to warrant a bashing of the keys so, here we go: Monday 03/09/2018: Spectra Systems: SPSY: Mkt Cap £42m: RNS Two New Lottery Wins and Results Date. Firstly what an unfortunately worded headline. The more trusting may well have thought that SPSY had won the Euro Millions not once but twice, wow that’s a nice stroke of good fortune. However, when you read the words within the announcement you become aware that they have actually been awarded two fairly handy but not especially financially significant contracts that run over 7 & 8 years. I guess the interesting aspect is that these contracts are with two customers who have switched from other suppliers presumably that says something very positive about Spectra Systems. SPSY is one of my smaller holdings within the Voyager and just about earning it’s keep so it can stay but with a watchful eye. Monday 03/09/2018: IG Design Group: IGR: Mkt Cap £450m: RNS Informing the market of the completion of the acquisition of Impact Innovations Not that much to say really apart from reiterating the quality of IGR and I expect that quality and production efficiency to become part of the culture within the newly acquired business. Monday 03/09/2018: Bioventix: BVXP: Mkt Cap £168m: RNS Re: Date of Finals Well, the finals for the year ending 30/06/2018 will be revealed in early October which is fine enough in itself but I rather felt there may have been included a trading update as there has been in the last two years with the announcement of the finals. Still, I suppose no news is good news and we wait for the finals on 08/10/2018. Tuesday 04/09/2018: No RNS relevant to the stocks within the Voyager. Wednesday 05/09/2018: Somero: SOM: Mkt Cap £225m: RNS Interim Results  Current Trading and Outlook The positive trading momentum experienced in North America has carried over into H2 2018 reflecting robust non-residential construction markets and a high-level of confidence by our customer base. We are pleased with these strong market conditions as well as in the broad customer interest across our product lines highlighting a wide-range of project activity in the market. Positive market conditions and healthy customer project backlogs give us confidence in delivering a solid performance in North America for the remainder of 2018. The momentum of trading activity in Europe is expected to carry over in H2 2018 and we expect sales in the territory will be broad-based, with a variety of countries contributing meaningfully to sales. We expect the market will continue to be driven by demand for replacement equipment and technology upgrades, as well as interest in new products. In China, we are aiming to gain increased traction in H2 2018 with the sales and marketing initiatives launched at the beginning of the year starting to deliver returns, in addition to positive contributions to market performance over the medium-term from the recently added local leadership. We continue to view China as a significant long-term opportunity for the business and one which we are committed to pursuing. In the Middle East, we expect to see a continuation of the H1 2018 performance for the rest of the year while in Latin America, we anticipate H2 2018 will improve due to the meaningful opportunities and solid level of activity across a variety of countries in this territory. In our Rest of World territories, we also anticipate that the solid H1 2018 performance will continue through the remainder of the year and are particularly pleased with the traction we are gaining in the India market. Overall, we see strong activity across our entire geographic footprint and strong interest across our product categories in H2 2018. With the broad-based opportunity for growth and the performance of the Company in the first half of 2018, the Board remains confident in delivering another year of profitable growth for our shareholders in line with current market expectations. My View: a very impressive and solid set of figures from SOM and also excellently presented in such a straightforward upfront way i.e. you don’t have to search to find out how performance sits against expectations, it’s included in the first three lines of the report. Look at this lovely line which appears close to the front of the report “Four of six territories grew compared to three in H1 2017 led by strong contribution from Europe and North America, which together represent 83% of total revenues”. So, let's go and chuck in a very nice SR of 97 (my first purchase was in the days before the SR system was available), a very undemanding valuation and a dividend of about 5%; all in all a great company that I am happy to have as one of my top half dozen holdings. Incidentally three of those top six by value holdings, SOM, BVXP & KWS are now riding for free as although they are significant positions, in “Dragons Den Style” I have taken the capital value of my original investment back. Thursday 06/09/2018: Dart Group: DTG: Mkt Cap £1.5b: RNS AGM Statement "The positive start to the financial year as reported in our Preliminary Results Statement of 12 July 2018 has continued, with Leisure Travel bookings growing slightly ahead of our 25% summer 2018 seat capacity increase and winter bookings satisfactory at this stage. Demand for both our flight-only offering and our higher margin package holiday product remains strong and package holiday customer numbers as a proportion of total departing customers have increased slightly for summer 2018. Progress continues to be made at Fowler Welch, our Distribution & Logistics business, which is currently trading in line with management's expectations." Overall the Board expects the Group to meet the recently upgraded market expectations of profit before foreign exchange revaluations and taxation for the year ending 31 March 2019 and will provide a further trading update on publication of its interim results on 15 November 2018." My View: nice and simple confirmation of the positive outlook reported in the final results issued on 12/07/2018. I have commented on Dart for years now and that simply because it’s been such a key element within the Voyager. When I originally bought DTG back in 2013 at about £2, I was very watchful as feared I may have missed the boat, or plane in this case, as in the previous 12 months prior to my purchase, the stock had appreciated by over 100%. The point I am making is that as with SOM, buying into quality at a reasonable price backed by positive momentum, good EBIT margin and attractive return on capital (ROCE & CROCI) is a very successful formula that was discovered probably way before I ever landed on planet earth. Friday 07/09/2018: No RNS relevant to the stocks within the Voyager. That’s it for this week’s log so it’s time to head off into the weekend for a trip to rather welcoming Doncaster to see the Hatters play. I will be meeting up with a few Hatters mates from around the UK and am already being bombarded with the “why are you not drinking” line, followed by “are you unwell”. I seem to get strange questioning looks when I simply say I am dry at the moment with those looks turning to disbelief when I tell them the money saved is being donated to charity: folk are strange. Oh, almost forgot & indeed should have included in the August log, I added a starter position in Beeks last Wednesday at 82p. On reading through the results last week I was impressed with the potential for good EBIT margin and growth, so, we will keep a look see. Have a great weekend and should the RNS news flow be sufficient, I will post another Voyager log next Friday. In the meantime, I am drafting the outline for a dynamic/evolving investment book that should appear on this site in the next few months. The book will have sections covering my investment journey from the early 90’s, mistakes along the way, learning points, making an investment plan, searching for gems, buying & selling, risk mitigation and a section covering what I consider to be the sensible or useful side of “reading the tea leaves/technical analysis”. As ever not advice but simply the development of a private investor who has enjoyed the good times as well as two of the most savage bear markets in living memory. Hope to catch you next week. Voyager RNS Log August 2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. What a summer, in fact, it’s been so hot that I just don’t feel the need to have my usual September break in North Cyprus as I have simply had enough heat to last me a little while yet. I rather fancy I will settle for a few days walking in Cumbria away from the crowds. In fact, maybe I can juggle a trip to the lakes and take in the Hatters away game at Blackpool in late September; I can feel a plan forming. The summer months have been rather kind to the Voyager portfolio with the value steadily advancing even after slimming down the amount of capital invested. Strangely & simply due to a different percentage mix of the same stocks, the portfolio I manage for a friend is a few % points ahead of the Voyagers decent summer showing. As have I written in this log in the recent past, I tend to think there could be something of a storm brewing with uncertainties such as Brexit on the horizon and after such a profitable bull market it strikes me as simply prudent to take some profits and boost the cash coffer for future attractive buying opportunities. During August there has been some trading in the Voyager with a touch of profit been taken on a few ABDP after a wonderful run from my initial buy at £4. I also sold XPD for a 30% profit over a few months, IQE for a small overall profit; lost 2% on TW which despite decent results was not in a sector currently in fashion. One other sale was my earlier re-entry to previously profitable FDEV which could not get any traction in the current market. I did some quite substantial top-ups on share price weakness: GAW when it retreated to £28.50 on the release of good results, DTG, KWS when it drifted back below £17 and some further XPP on share price weakness. So, after all this trimming and topping, the Voyager holds only 18 directly owned stocks and of that 18, 6 account for 55% of the invested portfolio. With the degree of uncertainty we have at the moment I rather think that investors need to be aware of the difficulty that they can be exposed to when trying to sell small market capitalisation shares. That difficulty, of course, gets magnified the further we drop in market cap and generally I work on a guideline of having no more than one stock of below £50m market cap within the portfolio. I rather suspect that many of today's investors have not been through anything like the torrid bear markets of 2001 and 2008. In such bear markets or even major corrections, it can be almost impossible to shift any meaningful quantity of sub £50m cap stocks. Anyway, I have done my risk mitigation, migrated within a stockade of high conviction quality stocks (can I really call BOO high conviction?) and have plenty of dry powder if glorious opportunities materialise. The spread betting side of my investments has been going very well over the summer. I never use any exposure that could not be covered by capital held in the live account and I operate a strict risk management system in terms of potential losses. Ahh, I should also say that in my experience betting on an index is just not worthwhile; never worked well for me and so I leave it alone. So, let's have a quick look at RNSs that have been released in August covering stocks held within the Voyager. Firstly a couple of stragglers from the end of July: XP Power: XPP: Mkt Cap. £590m: Interims 30/07/2018: posted some sound half-year results although they did say they would need to manage component costs which had increased recently. The turnover & order intake were both up around 9% compared to H1 last year with gross margin at 46.7% and operating margin around 20%. The company at the H1 stage says it is confident of meeting the full year expectations. Initially, the shares reacted well almost hitting £38 on the following day but then a persistent seller emerged disposing of stock chunk by chunk which then worried a few smaller holders into discharging their position. I took the opportunity to top up with a couple of purchases below £31; I may have missed something but to me, this is a quality well-managed business with good growth forecast; let’s wait and see if I have missed a trick! Games Workshop: GAW: Mkt Cap. £1.2b: Finals on 31/07/2018: To my view, these were a terrific set of results with turnover up 39% & PBT up an astonishing 94%; yes everything about the results apart from one small section read very well, was well written and in straightforward text. So, why did the shares take a significant slide backwards to £28.50? Well, this buying opportunity was kindly created by the following comment in the report from CEO Kevin Rountree “It would be unrealistic, if not daft, of me to promise that we can continue to grow at the rates we have reported over the last two years. I am not, however, planning to scale down our ambitions, I am just informing you of the backdrop”. To my view, that was, of course, a perfectly sound and realistic comment but it did slightly wobble the market, cause a lovely price dip and of course the chance for me to make a significant top-up of my current holding. A lovely company which in my opinion has much further to travel. Portmeirion Group: PMP: Mkt Cap £127m: Interims 02/08/2018: As expected a decent set of interims with PBT up by 29% and my fag packet calculations still strongly suggest that PMP will beat earnings expectations for the full year although PMP is being politely conservative as the H2 is a big one for them and merely saying “we remain confident in our ability to meet full-year market expectations”. A really sound company that I am happy to hold. Keywords Studios: KWS: Mkt Cap £ 1.2b: two announcements this month firstly a half year trading update on 03/08/2018 and secondly an RNS on 20/08/2018 announcing two more acquisitions. So, firstly a look at the trading update which as you would expect indicated some very good numbers with a 66% increase in adjusted PBT. Then a statement saying “we anticipate a strong second half performance in line with current market expectations for the full year”. Now the ahead of market expectations traders may have been a bit disappointed with that statement and the shares drifted back as low as £16 and yes, for a quality company it offered another topping up opportunity which worked out rather well as I had recently top sliced at £18-50. We then had the two acquisitions announced on 20/08/2018 which as per usual with KWS seem a good addition at reasonable prices to the range of services on offer from KWS, The market warmed to these acquisitions and the shares rose over the next few days to go over the £20 mark which is nice as I bought my first batches at just over £3. D4t4: Mkt Cap £65m: Contract wins announced on 14/08/2018 which although not quantified in terms of delivery of revenue or profit, appear to be very encouraging. Also, the H2 weighting issue has been removed as a worry which is good news and indeed news that the market reacted to very positively. We then had an AGM statement of 23/08/2018 which was very positive in tone and also went on to say “the Board remains confident of delivering on its expectations for the year ahead”. All good news and the shares kept up their momentum reaching 180p; also good news to the Voyager as I topped up at 124p after the April positive RNSs. Computacenter: CCC: Mkt Cap £1.6b: Interim Results: a decent enough set of interims and as expected really and an “in line with expectations” comment for the full year. Maybe some were looking for another “ahead of expectations”. After a good run we are now seeing some profit taking and maybe a breather before possibly heading higher. I will keep a close watch on CCC and if the drift continues I will sell. IG Design Group: IGR: Mkt Cap £360m: Acquisition of Impact Innovations. A beautifully managed minimal discount placing to fund the acquisition of Impact Innovations plus leave a little in the war chest for further expansion of the group. As a consequence of this acquisition, IGR will become the largest consumer gift packaging business in the world and also very sweetly this acquisition vastly increases it’s exposure to the USA. Additionally, as the CEO Paul Fineman points out there will also be significant synergy savings and additionally unleash the group's expertise in automated production management on Impact. The large household names in the massive consumer goods market are customers of IGR and this will increase further and to a greater depth with having Impact as part of the enlarged group. The placing at the ridiculously meanest of discounts of 0.06% was heavily oversubscribed such is the regard for IGR and the enlarged group's prospects. As I write the shares have advanced to 600p almost 15% up from the pre-announcement price. Regular readers of the Voyager will know just how highly I regard IGR and its management team. The share price has increased fourfold since I bought and I have also topped up an appreciable number of occasions. Yet again I am tempted to top up further but they already occupy my No1 spot in terms of stock value within the Voyager; I bet I go and buy some more on a pullback! All in all, its been a very good summer for the Voyager and that slice of good fortune has been aided by my approach to stocks that I purchase. The approach would never fit all investors and almost certainly not value investors, the best of which do phenomenally well by exerting great patience with deep value situations. With me, I buy into a company and should the story that supported by buy decision change or the market indicate my timing was way out, I simply sell, protect capital and move on. With the stars of the Voyager I both top up when the price looks attractive or the newsflow is compelling and I also top slice occasionally when the price looks a little overheated. I then often buy further stock with those proceeds when overheating is followed by a touch of consolidation. As I say, this approach has worked well for me over a considerable time. In summary that approach is:  Turning to future Voyager logs, If readers find my ramblings useful then I will resume the weekly publication of the log as the newsflow picks up pace after the summer lull.