|

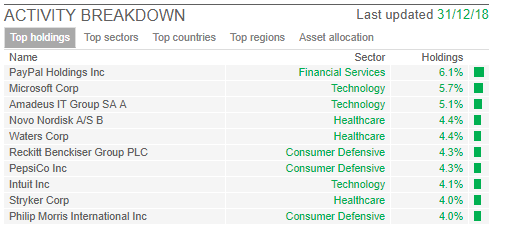

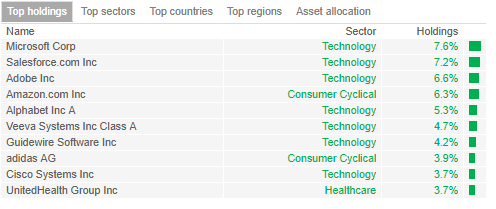

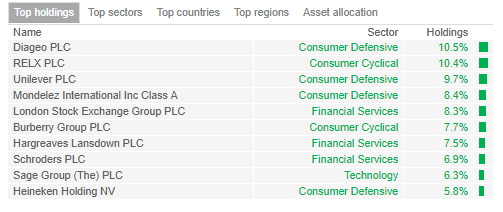

As private investors, and by private investors, I include anybody who directly puts money into stocks, funds and investment trusts, following the recent frightening publicity with the demise of a once high flying fund manager, should funds/OEICs or maybe even for that matter ITs be avoided? Well as Arthur Scargill would say “that’s an interesting question but the one you should be asking is….”. I feel the real question is “should you abdicate your sanity when investing in anything”. Let me explain: many investors are sadly poor investors with purchases based on little or flawed research and sadly if you try to walk across a busy road without cautiously looking each way, the outcome may not be the one you planned for. Just maybe a touch more consideration and research is needed rather than “I bought this share because it was tipped in Petite Company Stalker” or “some bloke on Twitter who has a great reputation said…etc”. To my mind, many an investor takes the same ill-researched approach with the selection of a fund or investment trust and sadly that culture may also apply to some advisors who make a living from their professional guidance where maybe their own wealth creation distorts advice. How did Kent County Council seek their advice regarding the investment for some of their pension funds? I don’t know but would be fascinated to find out. Now the point of this article is really to say that with a little research you can select some quality OEICs or Investment Trusts to invest in but, and it’s a real but, you have to take a peek under the bonnet. Of course, you want to keep an eye on exorbitant management fees but at the same time, if a fund manager can make me 15% to 20% a year whilst he resides on some Indian Ocean island, why the heck should I care? Should I really let my social ethics force me to invest in “Frugal Fred’s from Macclesfield” Fund that can on a good year maybe beat the FTSE? Sorry, I am easily bought, I am here to make money, stay in Macclesfield Frugal Fred, I am off to the Maldives. There is also another consideration and that revolves around the structural merits of an OEIC compared to an Investment Trust. Structurally, I have to say that I by far prefer Investment Trusts but I don’t allow that bias from precluding my investing in what I consider to be high-quality OEICs. In broad terms, if an OEIC needs to fund investors cash coming in or being withdrawn, then it has to either buy or sell some of its holdings: the value of the fund will broadly be the composite value of the components. With an IT you are simply investing in a company that holds a number of stocks and the share price of that IT will be like any other listed company i.e. it will be valued at whatever Mr Market values it at and not the composite value of the basket of shares that it holds; hence the premium/discount to NAV that you will see quoted for an IT. So, how does this impact my investment universe? Well, I write the Voyager RNS Log which covers the great bulk of my investing universe; that’s the majority of stocks that I purchase directly into my accounts. I rarely write anything about my “lazy portfolio” which whilst being very significant in value is rather dwarfed by my dealing and ISA investments; maybe not that surprising as I go back to the days of PEPs, remember them? Well, I currently only hold four holdings in this Funds/ITs portfolio and each has been selected with some degree of care and looking under the bonnet to see what stocks each have invested in. What I am personally looking for is at least some global diversification and above all, the selection of high-quality profit-making businesses; I am not really interested in something that “might one day make a profit”. So, how do I do that? Well, I simply gauge a feel for the quality of the management, past performance and take a look at the top ten investments in each. Dead easy to do and a number of ways of accessing this data; by preference, I use SharePad as they make that first look so easy. Does it work? Well, the performance of my Funds/IT portfolio is up by over 20% so far in 2019 (to mid-June 2019 compared to FTSE AS TR @ 12%) and for the difficult year of FY 2018/19 three of the investments averaged 19.9% with Smithson which was only launched in October 2018 returning 18% to the end of FY 2019 compared to the FTSE AS TR @ 7.5%. Not a bad performance and all achieved with just a little care in terms of selecting quality. The messages therefore are:

So let’s have a quick look under the bonnet at the top ten holdings for each of the four investments in my Funds & ITs portfolio (these details are from SharePad): Fundsmith: Manager: Terry Smith  Blue Whale Growth Fund: Manager: Stephen Yiu  Finsbury Growth & Income Trust: Manager: Nick Train  Smithson Investment Trust: Manager: Simon Barnard (Under the Terry Smith umbrella)  In my view, all four hold quality stocks, have a good manager and track record.

To conclude, there is quality out there in the world of OEICs and ITs but you will have to take care with your selection and look at the basket of stocks within an instrument and take a judgement on the overall quality. You may ask why do I have such a portfolio when I invest directly myself for the bulk of my portfolios? Well, two reasons. Firstly a loose benchmark for Voyager and secondly the realisation that one day hopefully in the distant future, any investor may become less qualitative in their thinking ( a polite way of saying aged incompetence) and need to move to a trusted and respected manager to look after their hard-earned dosh. So, why not develop that expertise along the investment journey whilst you still have all of your marbles! Happy Investing!

0 Comments

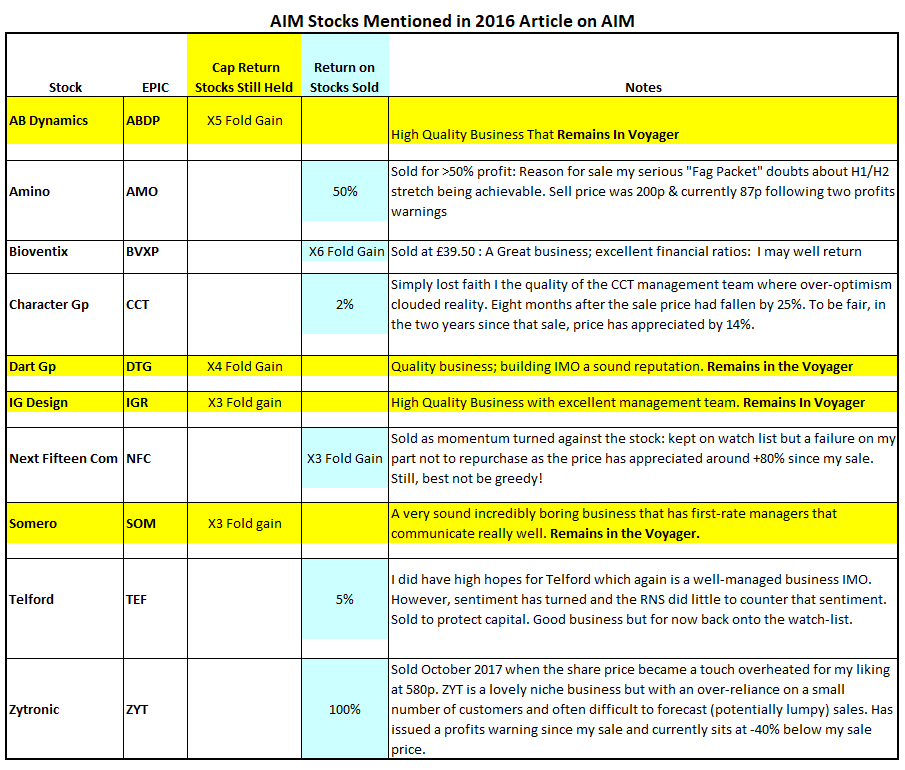

A few years back I wrote an article considering how an investor may mitigate risk when investing on the planet AIM. As a few years have passed and after various shenanigans by some AIM companies, I thought it would be timely to revisit the stocks originally mentioned and see how they have performed. Remember each of these stocks was invested in at the time based upon criteria that I consider to be attractive and also give a degree of confidence in that you are buying into a quality business. Selection criteria included improving revenue/profits, good returns on capital employed, hopefully, a high gross margin and attractive EBIT margin plus cash generation. Then being savvy and investing when momentum is with you. I am never fussed about being the first one to arrive at the party; simply happy to arrive after a few others have got things going and hitch a ride on the coat-tails of momentum. Our own planet Earth has some treacherously dangerous environments such as the wild oceans, jungles and deserts, snake-infested swamps and I certainly would not contemplate settling in such areas. AIM certainly has such hostile environments in abundance but the savvy explorer landing on AIM will head for the richer fertile plains to settle upon and hopefully thrive. Hence, the selection criteria I use that fits my personality. Now I really should say there are other very successful ways to thrive on AIM, for example, you may have the steady unflappable patient personality of a value investor who spots an undervalued maybe unresearched stock, buys and sits it out; a good approach yet one that does not readily fit my personality. So, how have the 10 AIM stocks I held when I wrote about AIM a few years back performed:  Note: the appreciation in value is based on the quantity of stock originally purchased. Do remember that as you make further purchases of a stock as it appreciates in value, the important thing, the bottom line, improves but the sometimes misleading percentage gain of the new pot will not look so impressive.

In summary, I have been very fortunate that the stocks I previously reviewed on AIM over the years have either performed well or have been jettisoned from Voyager without damage. The key for me is to keep looking at the numbers declared from the company as given in each relevant RNS release which include Interim results, Final results and for many companies trading updates. If in doubt, get out and protect one’s capital. There are of course the usual considerations that are often magnified with AIM stocks and these include:

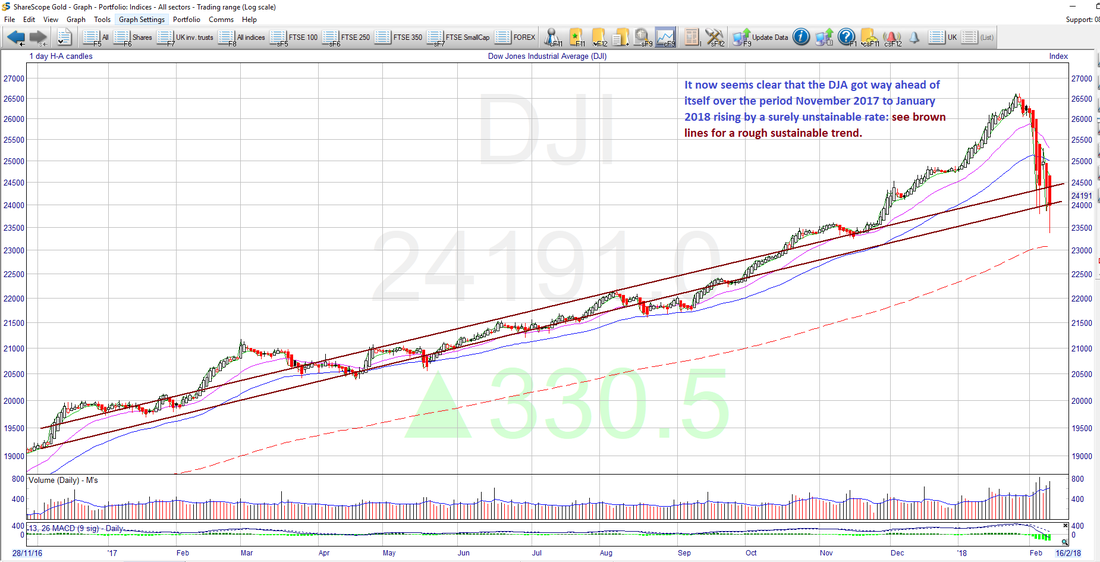

At this point, I should say that I have penned this article In response to some enquiries regarding what AIM stocks I currently hold and my approach to managing them. In truth, my approach to AIM is strikingly similar to that of the main market and it is quite simple: 1. Seek quality stocks to invest in: good returns on capital employed, increasing revenue/profits, attractive margins, acceptable debt position, acceptable valuation & remember sometimes you just have to pay for quality. 2. Look for any “smoke & mirrors accounting” or sloppy process such as at UTW, TCM, AIR: I have commented on all three of these companies in the Voyager Log at various times. Simply looking for things that don't stack up; those mislaid invoices, whoops we have not paid the full amount of tax, overly ambitious revenue recognition, manipulating of operational costs etc to boost foggy profits. 3. Avoid wafer-thin margins 4. Ensure you are comfortable with the newsflow/annual report; challenge some of the figures with your own calculations. 5. Maybe avoid the bulletin board highly followed shares: don’t be seduced by the next big thing. If the next big thing really does work, then hitch a ride on its coat-tails. 6. Don’t take a position when a stock is on a downtrend. Remember, "the trend is your friend"; yes, I know its an old saying but nevertheless very reliable. 7. When comfy, take an initial position with a tight indicative stop loss and add to the position as it hopefully appreciates. Say you are planning to invest maybe £xk in a stock, start with a position of £xk/3, then add as appropriate (by appropriate I DON’T mean averaging down). What I mean is building a position in a winner. 8. Protect your downside with an indicative stop loss (SL) that you raise in steps based on multiples of your actual stop. Maybe when the stock is really motoring I may change to an indicative trailing stop loss. Note, I say an indicative stop loss not an automated one. Simply a bell that may ring to say “hey you dozy so & so, do you need to take any action”. It does not mean that you have to trigger that SL but rather evaluate the situation. For example, the day after the referendum would not really be a sensible day to press the sell button as guided by the SL but merely a time to evaluate things. 9. Leave your ego in a small box outside of your office; ego has no place in investing. Sadly so many investors don't sell a losing position as their pride will not allow them to do so at least until break even is reached. I simply admit I am wrong when a stock goes against me, shrug my shoulders, learn what I can and move on. 10. When things work well with a stock, don’t be afraid to let it run: maybe adding more or taking a comfort reward, give yourself a treat, on top-slicing. Apologies if the list is not exhaustive as it was penned on a train ride back from a footy game. So, whilst the Voyager log has been running, there have been a further 16 AIM stocks purchased in addition to the 10 traded that are listed in the table above. Of these other 16, the following five remain in the Voyager: ARC, D4t4, KWS, PMP and SDI. The stocks D4t4, KWS, PMP and SDI are giving very good returns whilst a relatively recent position, ARC has yet to move appreciably. From the 26 AIM stocks covered either in this article or recorded in the Voyager Log, we have: Eight very appreciable winners and one apprentice (ARC) that remain in the Voyager: ABDP, ARC, D4t4, DTG, IGR, KWS, PMP, SDI & SOM. = 9 AIM stocks currently held within Voyager. Whoops, almost forgot I have a “wild card” or rule breaker on AIM with a small holding in HUR: as I have said before, I am useless with holes in the ground and even worse with holes in the sea so, let’s see if my treading from the path of safety ends in a loss. Also just after their recent interim results, I took a small initial starter position in TRCS. Note also regarding some sold AIM holdings: eight stocks that delivered very good returns up to the point that profits were taken following my feeling less comfortable with an RNS, went on to have fairly significant falls in price; indeed CAKE went bust but I made 20%; see notes about CAKE in the Voyager Log from earlier months. Ok, I was very fortunate regarding CAKE, however, had I simply stayed inactive invested in the other sold winning positions and not followed the RNS newsflow, then eight winning positions would have turned into losing positions. I can’t stress enough the importance of the RNS newsflow to my investment approach. Of the remaining stocks sold a few have remained in a trading range and a small number have appreciated a touch more. Of the three stocks making a slight loss, this was risk controlled to an average of -7%. In summary 16 of the 26 stocks have added significantly to the value of the Voyager and downside has been strictly managed with risk control. That’s roughly 6 or 7 winners from every 10 investments which I think is fairly routine for my work or maybe even a touch flattering. Of that win ratio, I usually find its just a small number of stocks that do the really heavy lifting within a portfolio. That’s fine and dandy but the crucial thing is to ensure that the ones that don’t turn into winners do not have an opportunity to damage your bottom line. So, a couple of key points to my approach to managing a position once I have bought into a stock: Key Point 1: The key point I am trying to get over here within my approach is the vastly important aspect of reading and interpreting the RNS newsflow issued by each business. This does two things. Firstly on encouraging news, it leads you to either add more shares or simply continue to hold. Secondly as a once encouraging story begins to show signs of change e.g. “H2 weighting” it gives me an early opportunity to sell, hopefully, take profits and move on. Hence the Voyager RNS Log that I keep and publish. Key Point 2: A second key point is that even with the most diligent research, I completely accept that I will not be right all of the time. When this appears to be the case and it can be quite often, I simply sell without emotion or regret and simply move on. This article is not designed to say “how clever I am” because I am not. It simply demonstrates my approach to investing and in particular AIM stock investing that attempts to manage risk. I honestly feel that selecting good quality stocks that turn into winners is only half the story of success: the other half is managing your downside; absolutely crucial in my opinion. Happy Investing! A few months back I wrote a piece on benchmarking your portfolio and why, at least to my mind, you should do this on a regular basis. The exercise can be both enlightening and in some cases, offer a hefty wake-up call to the more gambling style of investor who enjoys sporadic years of feast followed by famine. As I have written before, an investor will almost certainly have an objective for investment; is it for a major purchase, possibly to fund your lifestyle, preparation for when you disembark from paid employment or possibly to leave a legacy inheritance behind you when the grim reaper calls. Whatever reason you have, life provides a continuous stream of opportunities for making mistakes, learning from those mistakes and hopefully improving or in many cases doing the same thing that has failed time and again in the hope that it will eventually work out. A wise chap by the name of Albert Einstein once said: “insanity is doing the same failing thing again and again and expecting a different result”. Just why do so many investors in all walks of life keep making the same mistakes over and over again and sadly never learning from those mistakes or even worse kidding themselves that they are learning when all they are doing is repeating them albeit less frequently. So, with benchmarking, provided you select high-quality investments to measure against, you can at least get an idea of how your approach is doing. I would go so far as to say even to get a feel if you are wasting your valuable time i.e. if you can’t beat the quality benchmarks over time then simply let those guys do the work for you, hand your money over to them and free up some valuable time to maybe do something in life that more suits your character. Note, I did mention two key points here; quality benchmarks and time so let's be clear what I mean about both. Firstly quality benchmarks: now it is almost accepted convention to benchmark one's portfolio and indices and often as not that chosen index is the FTSE All Share Total Return. However, it is important to benchmark against something that suits your investment style e.g if your objective is a very low-risk growth return then why not measure against a normal interest rate return with your target being to do say 5% better than the bank to compensate for risk. On the other hand, if it’s simple good continuous growth, then you may choose like me, to benchmark against the likes of Henderson Small Co’s IT & Fundsmith.  Now to the concept of time; what do I really mean by time? Is it now you faired on a day, a week, a month, a year, five years of your investment lifetime? Well in my case I take almost zero interest in daily changes or weekly changes in portfolio value; it’s simple fairly meaningless background noise in my opinion that you will forget almost as quickly as you have assessed it. I take a passing interest in quarterly performance, a slightly higher interest in financial year performance and a real interest in five-year performance. I honestly reckon that apart from special situations and of course spread betting, that anything more frequent than quarterly almost qualifies as fluctuations within the baseline noise. Having said that, once out of the pool each morning, I check before the markets open the RNS announcements just to see if there is anything of note for a stock I hold such as a profits warning, a transformational positive business change, a trading statement etc. I find that real company RNS news coupled with fundamental and momentum as opposed to “Freddie the experts view” to be my chosen worthwhile investment style. In my view, unless a stock is in a game-changing place and that could either be a positive or negative change, then any more frequent measuring than quarterly just causes anxiety. You have the exhilarating rush “lovely jubbly” of a good day which is far surpassed by the ”blues” you may feel from a bad day, so in my book why do it? In the past, on the Whittler, I have stated that performance over a small time window; quarterly, six monthly or even yearly, means little. It’s been my belief for some time now that the minimum period to derive a meaningful “how am I doing” is a five year period. Now how does that fit with what I have blogged in the past? Your true performance will be measured though by the grim reaper and the executor of your estate: in the final reckoning, it’s as simple as that; touch sobering that one! I do see and read many investors quoting on a very regular basis their returns; it may be daily performance ranging up to YTD or a calendar year. Myself I have always tended to offer financial year performance against a benchmark. However, I now question if there is any real value in doing that? It’s not a competition; I don’t have an ego to feed and show how clever or stupid I am and I strongly suspect that in reality most investors simply care about their own performance rather than the claimed performance quoted by some investor in cyberspace. In fact, I don’t intend to quote any percentage in future for any of the portfolios I run as I can’t really see that as being helpful to any readers. I rather suspect, the most helpful way forward, apart from individual share returns within the Voyager RNS report, would be to simply indicate if my portfolio basket of shares is ahead of, matching or falling behind my rather challenging benchmarks. Personally, I feel that will serve what I am trying to achieve with my sharing of my ramblings about my investment thoughts far better than a “look at me” percentage performance. As I have said on a number of occasions, an average annual return of around 12%-16% sustainable over 10, 20 years or more makes in my book, for very valuable investment return. The wonderful returns we all enjoyed in 2017 where 30-40% returns were commonplace, is certainly not typical of the long haul and to my mind, can fool investors into thinking they are actually much smarter than they really are. For the sake of completeness and full disclosure, and aware that many investors measure their performance as YTD rather than the FY minimum that I use, I thought I should say that I am in the same boat as many investors since with the February 2018 correction. My portfolio is down in the order of 5% YTD which is in line with my benchmarks. In my view that’s the sort of thing that a switched on investor should really come to expect after that totally unsustainable run by the Dow Jones Industrial Average in the crazy three month period November 2017 to January 2018. As investors, we should not celebrate correction; albeit we may top up some bargains, but simply come to accept this is all part of the investment environment.  Finally, just to requote some words I included in the WC 04/02/2018 Voyager RNS:

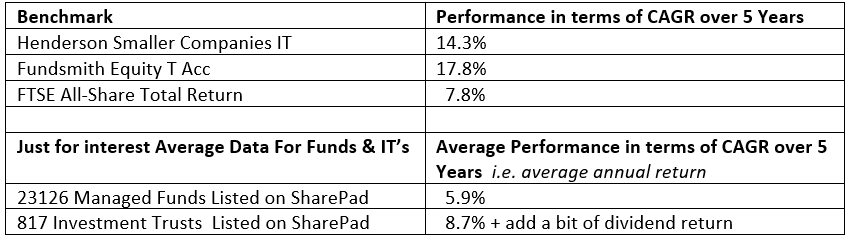

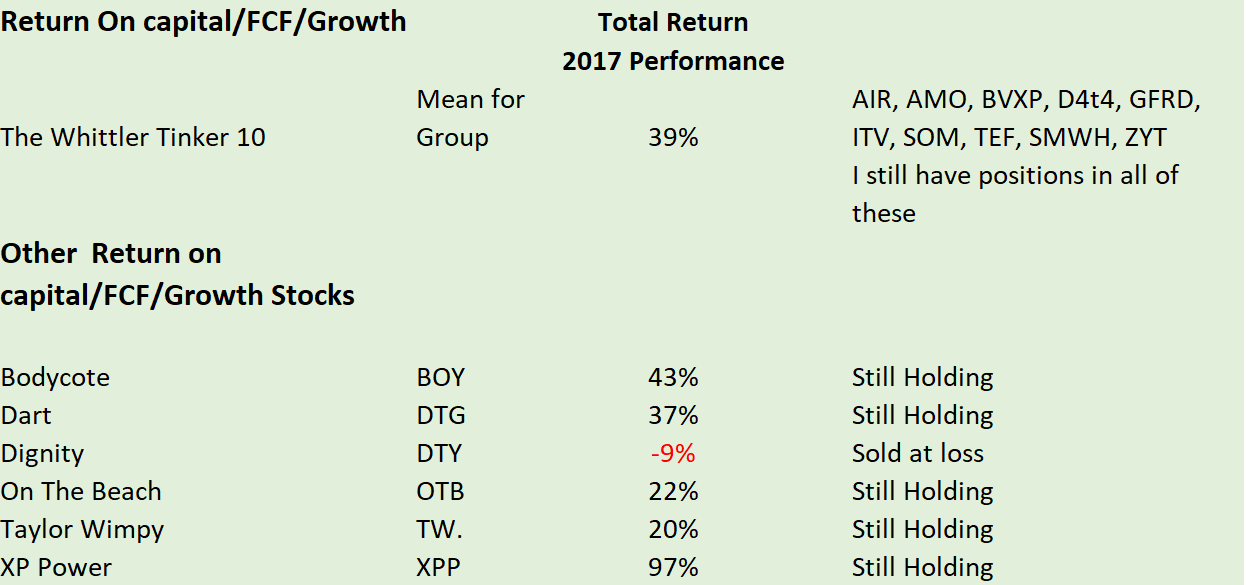

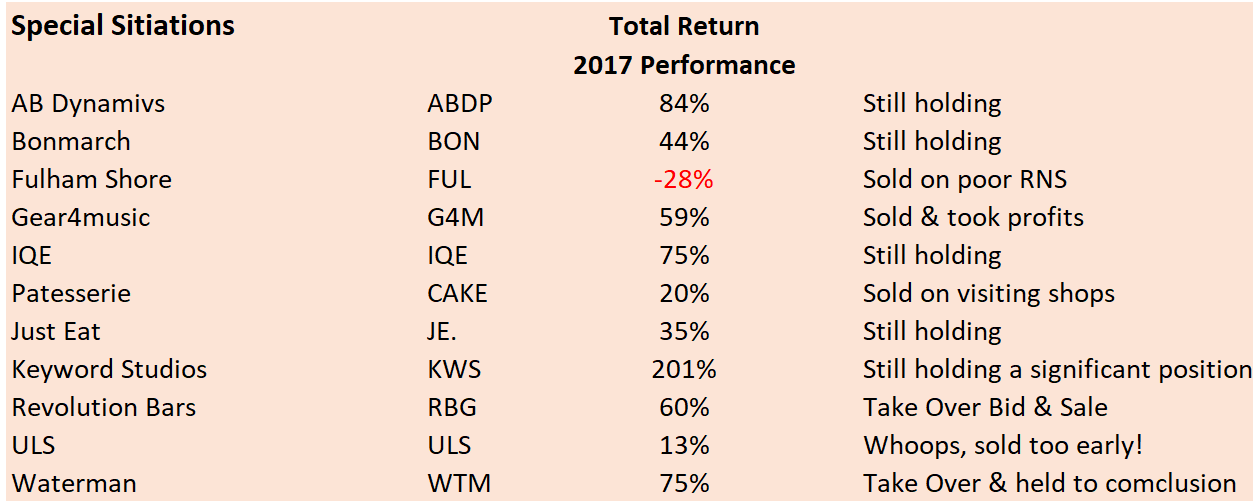

Overconfidence can be a killer and I suspect after the sweet spot of 2017 that many PIs will feel they are very good investors. However, a strength for an investor is to remain very self-critical and examine the downside at least as much as you enthuse about the possible upside. I hope you have followed my rambling reasoning covering benchmarking and investment returns as its taken at least a couple of decades to reach my held beliefs. Happy investing. Anybody who reads the Whittler Blog as I ramble on about my investment universe will be aware that I don’t overly pay much attention to short-term portfolio performance as I think that a true assessment of performance can only be made over a period of say three years and preferably five or more years. In fact, the only time real portfolio performance can finally be assessed is when Mr Grim Reaper has called; blimey, that’s cheerful stuff. Let’s move on quickly and have a look at the small time window of 2017/18 and see how things went. Note: I always consider the tax year end as a time when one really does need to assess profit and loss: it simply fits in with the new tax year and therefore has to be done. When I previously used to write about portfolio performance, I used to quote actual percentage moves and compare this to my benchmarks. However, after much discussion considering the merits of such a definite declaration approach of percentage portfolio movement over time; this deliberation included input from respected investors, I wrote in a recent article that in future I will simply say if I have beaten or failed to beat the benchmarks I measure my performance against. I will quote the various the benchmark percentage performances and then simply say if my portfolio has fallen below, matched or beaten those benchmarks. The reasoning behind this is that after a great deal of thinking and discussion with others is that your performance needs to be measured against what targets are pertinent to you. For example, what are you trying to get? Is it simply high income or steady capital growth or maybe you like the blue sky stuff. Also, and it’s just an observation, it seems to be a fact of life that investors & horse racing punters are sometimes happy to report the wonderful stuff but less likely to report the poor stuff. Finally, and this is very important, somebody with let's say 10% of their savings/capital invested may well be more open to risk than say the individual with 80% of the precious dosh invested: what I am saying here is that the bigger your capital pot grows, the more likely you are to be increasingly selective with your stock selections minimising to almost zero punts and concentrating on stocks of proven quality. At this point, I should give a reminder of my philosophy on what one should benchmark against. A very popular benchmark for investors is the FTSE All-Share Total Return with the argument that you are measuring your performance against the full market and including dividend return. Now whilst I can see the rationale for that, it is not a terribly challenging benchmark as it includes the good the bad and the ugly stocks; simply put, it’s a low benchmark. My preference for more challenging benchmarking is to raise the bar a touch and find a benchmark that matches more closely your investment style. Now my investment style has a bias away from the FTSE 100 preferring smaller companies: hence one of my benchmarks is the Henderson Small Companies IT. Now don’t be confused by the small companies tag on this Henderson IT as many of the companies are at least mid cap but overall quality businesses. The second benchmark I use is one that matches very much my investment philosophy in terms of companies that make very good returns on capital and good free cash flow: that benchmark is the very excellent Fundsmith. My way of thinking is that over time if I cant beat Henderson Smaller Co’s IT or Funsdsmith then simply hand my money over to them and go fishing, down to the pub or whatever grabs your leisure interest. Incidentally, in a separate portfolio, I do hold a respectable investment in Fundsmith as it offers me that non-UK exposure and also an investment in Henderson Small Companies IT. So, after painting the background rationale, how has my approach done in the financial year 2017/18? Firstly, the main thrust of the portfolio that tends to concentrate on two mini-universes of stocks: companies that make good returns on capital & have attractive Free Cash Flow characteristics and secondly what I term as special situations, companies were something is changing for the better. This section of the Voyager performed well in the FY 2017/18 and was comfortably ahead of all it’s benchmarks in terms of total return. The benchmarks returns are shown below:  For the Voyager which currently holds a couple of dozen shares, the star performers were: KWS @ over 100% Stocks in the 40% to 80% range: OTB, DTG, XPP, ABDP, BVXP, & three that have been sold: RBG, ZYT, JE. & IQE. A fair number of others also earned their keep delivering in the range of 15% to 30% total return. There were of course stocks that did not earn their keep and in the Return on Capital /FCF segment my blind spot was ITV. Other stocks that may have caused harm were jettisoned usually after a less than encouraging RNS: DTY for a small profit that could have turned into an almighty loss, FUL, GFRD that if they had not been sold would have been harmful and finally ZYT where profits were taken in stages before a 35-50% decline in share price. The Boring Bit As ever, I firmly believe that the art of managing a portfolio and the protection of one's capital is of almost equal importance to stock selection. When I research a stock, I spend a very significant amount of time looking at the potential downside as well as the sexy upside part. You can carry out your risk assessment during your research but unfortunately, you just don’t know what the future holds. In truth, if an investor selects say 10 companies that meet their required criteria and invests in those 10, you may well find that 2 or 3 do very well indeed; another 3 or 4 do reasonably, a couple tread water and finally, a couple head slowly south. I suspect this outlook is typical for most private investors if they were to buy 10 stocks. Also, every one of us without exception will have held a stock that issues a profits warning RNS; ouch not nice but simply an occupational hazard we WILL encounter on our investment journey. What makes the crucial difference in the performance of that basket of stocks is how you actively manage those stocks. By this, I mean continually topping up the winners and jettisoning those not displaying the momentum that you desired. I am not talking about chopping & changing or being simply impatient as with quality stocks it can take time for them to grow. What I am really trying to get over is once the story/rationale behind your purchase moves from compelling to risky, you take swift action to protect your capital. With the uncomfortable situation of a profits warning RNS, I rapidly evaluate and in 95% of cases sell at the opening bell. When confronted with the evidence that a stock for whatever reason, is proving a serious threat to one’s capital, I without emotion or regret jettison that stock: self-denial & procrastination are in my view simply serious risks to portfolio performance. Returns are of course much more correctly assessed over a much longer timescale than one FY as that’s simply a snapshot in time. I really think you should consider a period of at least three and preferably five years to get a real feel for performance and with that thought in mind let’s have a look at the compound annual growth rate (CAGR) for my benchmarks. I believe that for all but the income/high yield investor, these should be the type of long-term returns a private investor should aim to surpass if he/she is doing reasonably well. Note: if you are relatively new to investing and did some staggering 40%+ stuff in 2017, then please don’t get comfortable and think that’s the norm as it simply is not the case. If you can achieve let’s say a total return of 16% per year over many years, taking fully into account the good and less good years, then you will be a very successful investor. Anyway, the CAGR for my benchmarks over five years is:  Comment: in truth, if you were a touch selective with the better Investment Trusts & relied on Uncle Terry Smith for your OEIC, you would have done fairly well and had a lot of leisure time and maybe a lower blood pressure! I am not suggesting that this is the way for us private investors to go, merely my whimsical observation. Incidentally, as mentioned elsewhere, I do hold Fundsmith & a few ITs; I really am quite a fan of investment trusts but these sit in my separate passive portfolio.

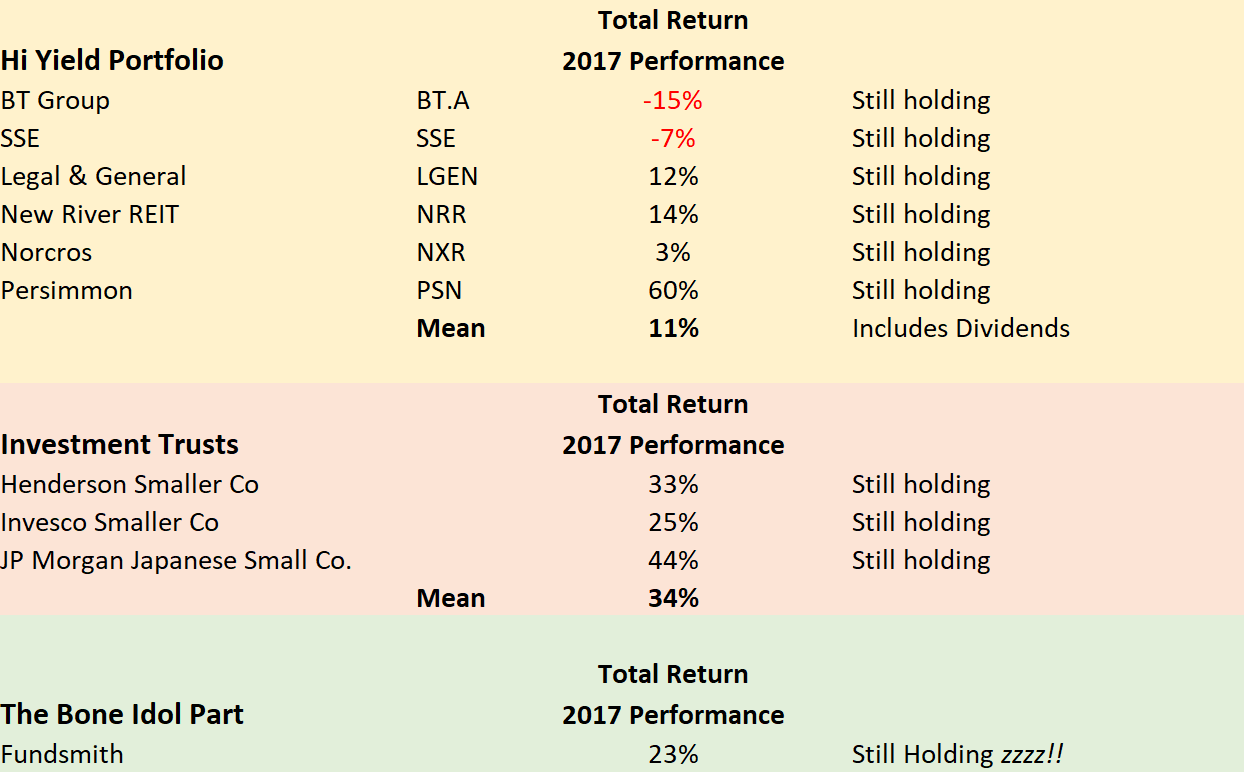

The High Yield Portfolio Turning to the High Yield portfolio, it’s been a decent enough 2017/18 but not quite as outstanding as the previous year. I reckon that over time on a high yield portfolio you should set a baseline target over say five years of something in the order of an annual 6% post-tax return; you don't really want to target any lower than this in my opinion as you need some compensation/reward for the risk you are taking on the stock market. For the FY 2017/18, the high yield comfortably beat this baseline even though it was somewhat bruised by BT & SSE. So a decent income year but not quite as good as the previous FY which was maybe a touch exceptional. Note: as ever when I seek candidates for my high yield portfolio, I seek companies whose dividends are well covered by free cash flow; the exception, of course, being the likes of utilities. Conventionally most investors look for dividend cover in terms of the ratio of EPS/DPS but as EPS is often so open to manipulation by overly eager CEOs who love their annual bonuses, I much prefer to use the ratio of the number of times that FCF covers the dividend payments. The odd miss is forgivable especially if there are obvious reasons such as capital investment to grow the business. Overall FCF is so much more difficult to apply the “smoke & mirrors” treatment to than the often manipulated EPS. Just a thought but I strongly suspect that not many companies assess the CEO/CFO bonus measured against criteria that include ROCE/CROCI trends FCF & share price combined in a set of annual bonus targets; silly me! So, that’s a quick review of FY 2017/18 with a bit of whittler philosophy plus being as ever aware that your next profits warning may be just around the corner; simply an occupational hazard. I hope all readers have a successful 2018/19. Happy Investing! Well, it’s been an interesting year and indeed one of the most prolific years in recent times for many private investors exercising a degree of discipline and wise selectivity on the stock market. Of course every year we have stories of huge percentage gains made by what I term as punters on the markets investing in a hole in the ground in the middle east or some other excrement or bust enterprise. The thing is with these types of punter who usually appear on those dreadful bulletin boards is that they emerge to tell the world of their wisdom but then rapidly submerge again as investment reality kicks in: not my style or approach to investing but each to their own. Thankfully we have a very healthy Twitter community and some really excellent blogs where respected honest investors share their thoughts and long may that continue. So, a few thoughts on 2017: Firstly, have I changed in my thoughts on noise? No, most definitely not, I steer well clear of investment periodicals; have a look at my watching the detectives blog. I also take no note tipsheets which to my mind are a blasted nuisance should a company you are researching be filled by one of them. Also, I have to say that whilst never being the most prolific tweeter, I have become rather selective both in terms of reading and time spent on Twitter. To my way of thinking, investment is about choosing an approach or combination of approaches, you feel comfortable with, continually refining that approach and keeping a timely eye on any RNS from one of your stocks. Oh yes, let’s not forget the vitally important ruthless weeding out on any stock showing a risk to the bottom line of the investment basket. Secondly, Have I changed my investment approach in 2017? Not really as my universe is still based on a number of building blocks. That’s two major blocks that probably cater for the bulk of my investments are firstly a combination of Return on capital/FCF & Growth and another fairly big section covering what I call special situations. Bringing up the tail I have three more minor sections covering high yield, investment trusts and finally a few years worth of ISA subs in Fundsmith; that’s the bone idle part that Terry Smith manages so very well. The two main blocks are in a little more detail: Firstly a combination of attractive returns of capital invested and good cash flow/free cash flow and some growth stocks with properties along the lines of the great Jim Slater, a chap that taught me so much back in the late 1990’s. SecondlyThe Special Situations Block: this block may to an extent to having some of the characteristics of the first block described above but will really be looking at companies that have something relatively exciting happening; possibly a potential takeover situation, a game-changing event or maybe just simply a stock that the market has in my estimation dreadfully mispriced. We then have other smaller blocks: The Income Stocks Block: just doing what it says on the tin but avoiding income traps where an apparently attractive yield is miserably covered and indeed nowhere near covered by free cash flow (utilities are of course an exception). Investment Trusts Block: I have for years been a fan of investment trusts and indeed some of my very first investments were in these vehicles The Totally Bone Idle Block: this consists of an appreciable block of the superb Terry Smith’s Fundsmith which I have held within an ISA wrapper since shortly after the fund was introduced to the market. Why do I like Terry’s approach; well for two reasons: firstly his approach to ROCE and cash flow with quality businesses mirrors my own approach to investing and secondly it gives me very valuable overseas exposure. So, what if anything has changed in terms of my writing in 2017? Well in July 2017 I added a new section into the Whittler blog to cover a roughly weekly review of any RNS stories that affect stocks from within my portfolio. As with everything I write, it is in no way a recommendation to either purchase or sell a stock but simply my sharing of my thought process. Oh yes, maybe I should mention that my ruthless jettisoning of any “did not get it right” purchase or resolve to sell immediately on a profits warning have become even firmer during 2017. I honestly just do not understand investors who cling on to a stock that is either underperforming or surrounded by bad news. To hold on to such a stock in the hope that you can be proved that you were “right in the first place” is to my mind totally flawed thinking. So, how have things gone for the markets in 2017? Well let's have a look at the various indices: FTSE100 gained 8.0% FTSE250 gained 14.7% FTSE Small Cap gained 15.2% FTSE All-share total return gained 13.2% FTE AIM 100 gained 33.3% Overall the markets were in a fairly good place during 2017 with worthwhile gains being had on the major indices but the real hard work being done on the AIM market. Now I appreciate that AIM may have had something of a bad press over the years and indeed that’s a well earned for many blue sky stocks pumped by mouthy CEOs and stocks from dubious locations outside of the UK. However, careful stock selection can be incredibly rewarding on AIM. As an example take the Whittler Tinker which I blogged about before bringing the series to a close. That portfolio of 10 stocks which closely mirrors my own overall approach and performance, appreciated by 39% in 2017 and 74% since January 2016 (I own or have recently owned all of the stocks within that series of blogs). Interestingly the lions share of the gain in 2017 being delivered by five quality AIM stocks; Bioventix (BVXP), Air Partner (AIR), Somero (SOM), Telford (TEF) & Zytronic (ZYT). The other major gainer within the Whittler Tinker in 2017 was my incredibly boring but lovely WH Smith (SMWH) which waded in with a total return of 53%; I love boring stocks. Now I should say that gains within a calendar year cut little ice with me as what significance does a calendar year have? I really don’t know. I find it far more sensible to consider the gains or losses one makes over a financial year as this at least ties in with the tax year and the ISA year. Indeed, I would go further as to say that gains only really become really meaningful over a period of let’s say five years. However, having said that, let’s for a bit of amusement at the end of 2017 see what the performances have roughly been over the last 12 months:-    The returns have been very decent in 2017 but as ever, I have been totally ruthless in removing any stocks where the original story or reasoning behind the purchase has changed. This vitally important approach has over the years done so much to preserve the capital within the overall portfolio. To give an example, in 2017 I sold Revolution Bars Group when an RNS informed the market that the third CFO in 12 months was leaving the business; simply a red flag in my opinion. Subsequently, RBG issued a profits warning and the skates were hammered by some 50%. The story then began to change when a new sector experienced CFO was appointed, accounting improved and a decent trading RNS issued. I then bought back in with two thoughts in mind. The stock had become what I term as a special situation firstly in terms of recovery and secondly takeover potential as the wounded RBG looked ripe for a predator to pounce. Fortunately, the competitive bid situation emerged and I subsequently sold at a very decent profit. It was a similar story with Waterman earlier in 2017.Was I lucky? Well undoubtedly I was but the more I persistently apply my approach based on sound research and quality companies, the luckier I seem to get. I should add that the number of underperformers that needed to be weeded out early in 2017 was the lowest number I have ever encountered; just a small few and thus having a negligible effect on the bottom line. What will 2018 offer? Well, I don’t have the slightest idea in fact truthfully nobody knows what the following 12 months may bring. All right, you get plenty of paid commentators offering their opinions but I just see this as totally irrelevant noise; put it another way, if they did not comment, they would not have a job. What I would say is that sooner or later we will be in for a couple of negative return years and then I suspect we as thoughtful investors will be more than happy with an annual return of 12-16% over a period of let’s say a 10-year timeframe. So for all of those investors who have enjoyed some really good gains in 2017, particularly fairly new investors, do take care of those precious gains as 2017 has been anything but a typical year. What do I plan to do in 2018? Well for certain there will be no new year’s resolutions; never really saw the point in resolving to do something that you give up on by February. What I will continue to do is research stocks for universe consideration, continue the Stochwhittler blog continuing to publish a weekly or thereabouts RNS log and continue with my football writing. I will also keep reading some of the splendid blogs written by some excellent twitterdrome investors. Whatever you plan to do in 2018, I wish you firstly good health and a successful 2018. I thought I would have a bit of a change to the usual format of the Tinker update and start with some, dare I call it wisdom that I have grafted into my way of investing over the years. The approach I describe below, listed in points 1 to 4, gives a decent thumbnail description of my approach to investment and managing my portfolio and as you will see, this approach has served me well in the application of the Tinker. Just for clarity, I should say that my overall investments have three groupings. The dominant grouping is based on companies offering very good return on capital invested, good cash flow and delivering real profits i.e. the type of business that this passive/reactive series has involved. The second category are what I term as special situations examples recently have been Lavendon, Waterman, KWS, ULS, OTB, JE. and IQE. Then we have the truly boring Hi-Yield portfolio that does what it says on the tin but yields far more than a bank or BS account but of course comes with a slight degree of risk. Anyway, onto the return of capital, free cash flow world of the Tinker: For want of a better description, let’s call it Tinker management guidelines No’s 1 to 4 (no reference to the highly respected football Tinkerman of Leicester City FC, Claudio Ranieri). Health Warning: non of my writings should be seen as me giving advice on individual investments or indeed which shares to buy or sell: I don’t do that! It is simply my sharing of my way of thinking in how I go about making investment decisions. Number 1: Buy Quality For me, it’s about buying quality companies that actually make real profits with decent returns on capital, have good cash flow and are fairly valued at the time; we all try not to overpay but sometimes you just have to stump up the money for real quality. Also and very importantly, satisfy yourself that the companies don’t manipulate the accounts to create illusionary profits. Number 2: Feed The Positive Momentum If and when your quality companies prosper then don’t be afraid to reinvest further capital or reallocate capital from those performing less well and buy more of the quality stock showing positive momentum. Examples from the Tinker during it’s lifetime to date are buying further Somero, Zytronic & Bioventix yet being sensible and top-slicing when the market had possibly overheated the prices of these stocks. Number 3: The Importance of Dividends Dividends are important and should not simply reside as cash in the foot of the portfolio, they should be reinvested and made to work. Number 4: Profits Warnings and Bad News

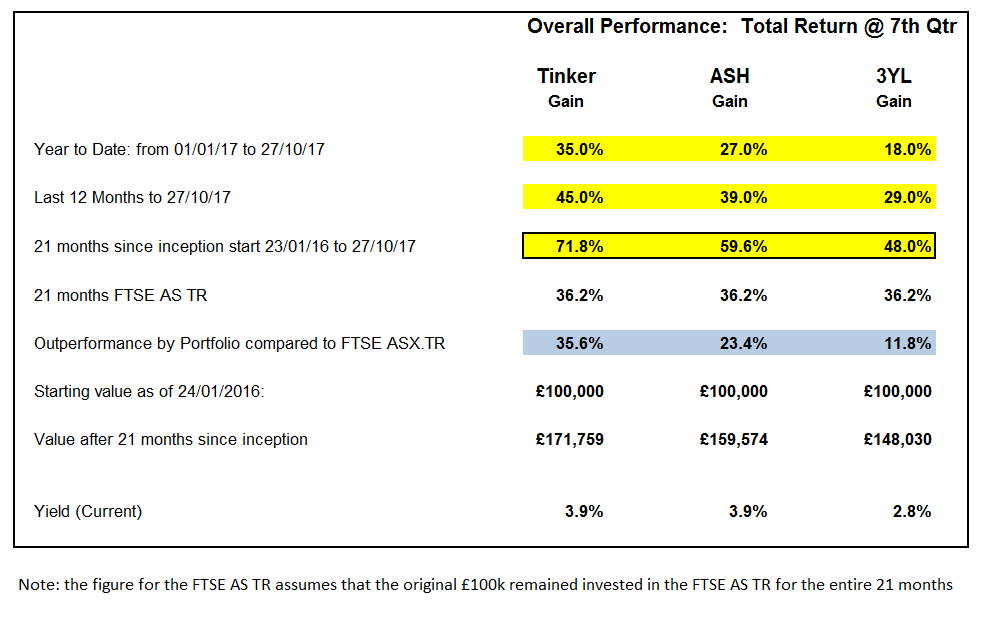

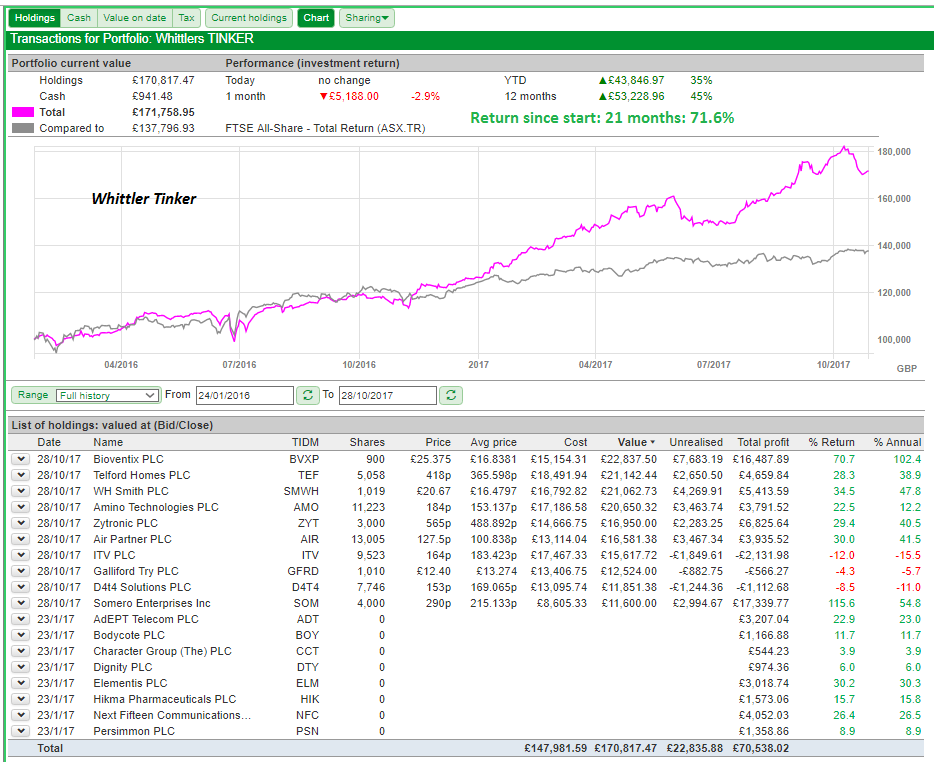

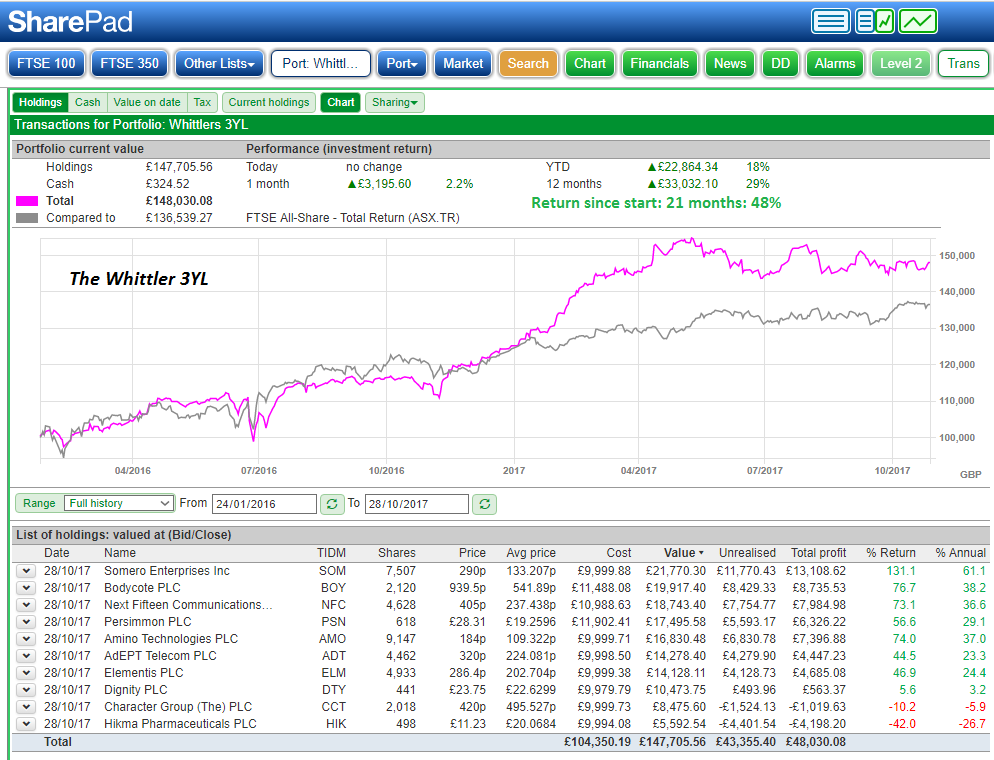

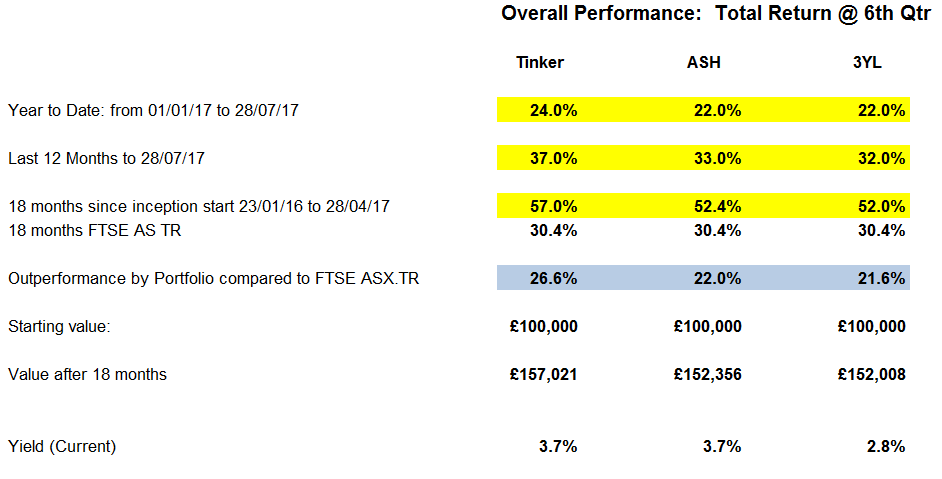

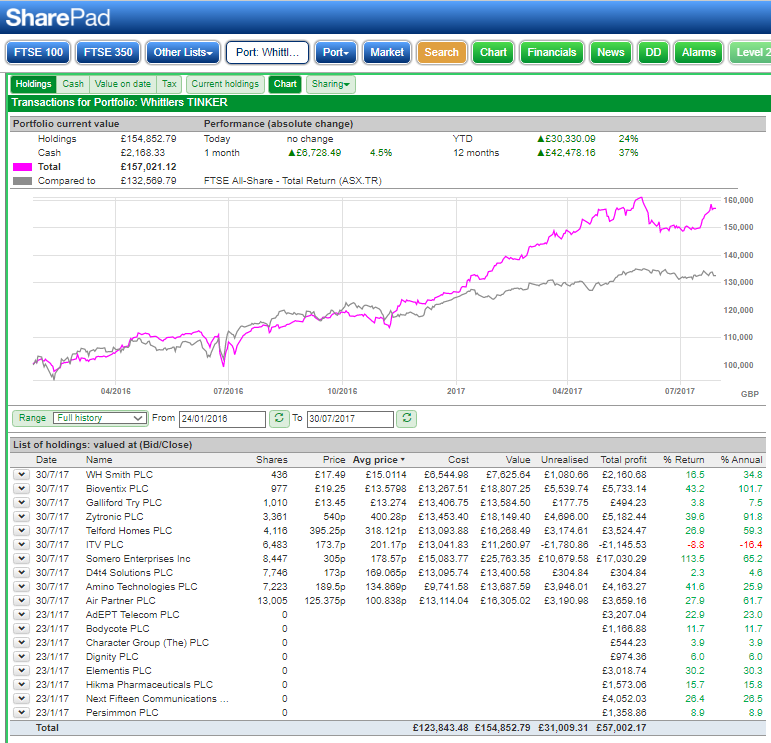

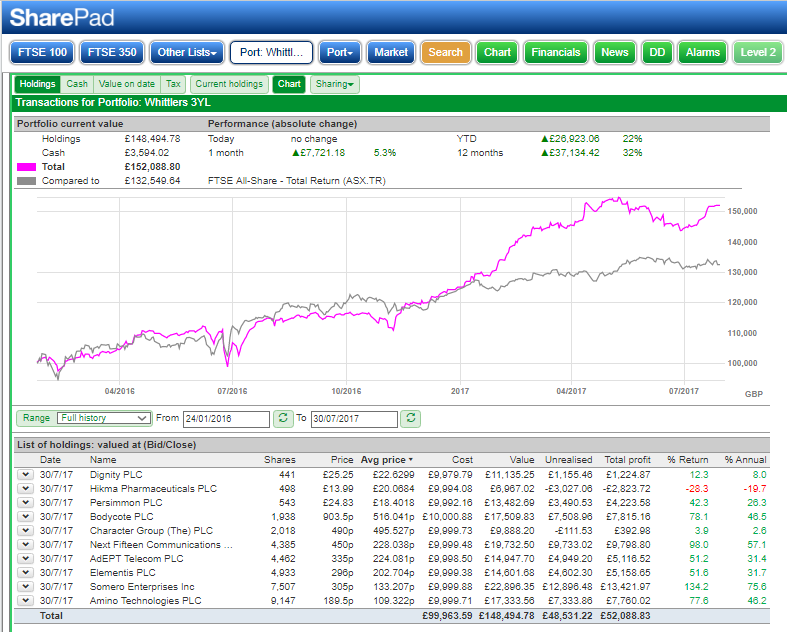

The number of stocks currently held between all three portfolios, 3YL, ASH & Tinker is 18 stocks. The stocks were the identical 10 for the first year and then following the rules, reallocation of funds made to a maximum of 10 stocks at the end of the first year for the ASH & Tinker with the 3YL retaining simply the original 10 stocks selected back in January 2016. I should declare that out of the 18 stocks involved I have held all 18 at least for some fairly lengthy period over the 21 months to date and currently have 15 still within my portfolio. Indeed 8 of my 10 largest holdings are from this retained list of 15 stocks. Why only 8 in the top 10 largest holdings? That’s simply down to the success of KWS and XPP pushing a couple down outside of the top 10 of my main portfolio (Note: I also run a High Yield portfolio and at sometime may include a note or two on that within the Blog). For the sake of ease and confidentiality, I have based the performance on an initial allocation of £10,000 in each of the original stocks when first purchased in January 2016. The management of the Tinker closely mirrors my approach to managing my investments with investments, sales, top-slicing and topping up matched in my long-term portfolio. Note: as a brief reminder of the Passive/Reactive rules can be found at the base of this article in the appendix. How have the three portfolios performed in the last three months and particularly since inception? The performance is given in the table below:  The Tinker Performance:  3YL (retain the same 10 stocks for the full 3 year period) Performance  The Tinker Dealing In 7th Quarter At the end of July I decided it was time to feed a little more to the stocks showing exceptional positive momentum when compared to other stocks in the portfolio. Some stocks became what I felt to be a little overheated or in ITV’s case lacked momentum in July and I sliced a few ITV, Somero & Telford reinvesting the proceeds in the highly positive momentum of Bioventix, WH Smith’s and Zytronic. These stocks performed very well over the next three months and in turn two of them, Bioventix and Zytronic were themselves top sliced in mid-October following results and a TU that were ok but the market had become overly thirsty for “greater than expectations” and in the realistically that sort of statement cannot appear in every RNS. The money released in mid-October was then reinvested in Amino Technologies and the previously sliced Telford and ITV. In the case of ITV, the arrival in January 2018 of the highly capable Carolyn McCall dropped in from EasyJet will, in my opinion, get some positive momentum under the share. Oh dear, I see that Woodford has been buying as well: why do I see images in my mind of Woodford and myself in BBC’s Apprentice shoot-out sitting in the grim greasy spoon Cafe prior to one us being fired by a ferret in a suit for making a potentially bad decision in buying ITV? Poor old Woodford, his previously great track record has been a touch tarnished recently but that happens, it’s would be wise for all private investors to remember that. In fact staying on that very theme, I have mentioned before that many PI’s are currently making very tasty percentage returns over the last 12-18 months; it’s not uncommon to see Tweets declaring 30%, 40% or even 50%. However, we have been in a very sweet period for stocks and as I have reminded readers before, these are simply not the type of returns one can expect forever. I would say that an investor who over a significant period, let’s say 10 years, can average something along the lines of 12-16% will be a relatively wealthy investor especially if they top up each year on their ISA allowance; to my mind, it’s all about being sensible, managing that portfolio, applying risk management and very importantly remembering that get rich quick is a dream not a reality when investing on the stock markets. The 3YL (simply invest in apparently good companies and leave them to it) has performed well giving a 48% return over the 21 months. Reappraising the ASH back in January 2017, boosted the return up to just under 60% and the more dynamic approach of the Tinker which has the same 10 stocks as the ASH, showing at the end of 21 months a gain of 71.6%. We also have some fairly hefty dividends that will land in the next three weeks; I do like dividends. I am of course very happy with this performance but as I said in the text above, the markets have been in a very sweet spot for a couple of years now and I would imagine that almost all investors with the exception of bulletin board sheep would have prospered in this time. The next update will be at the completion of the second year which will be in the third week of January 2018. At that time I will either decide to conclude the series as I believe the points about wise portfolio management have been, at least to my mind, well demonstrated with an open dynamic journal of activities or rebalance and take it into the third year. Whilst investment style may be a very different thing between individual private investors, I hope you have found a smidgen of enjoyment within this series and as ever, I wish you happy investing. Appendix: The boring stuff! Reminder Of The exercise Rules. The three portfolios will be firstly a buy and hold for three years, ploughing on regardless through economic conditions, profit warning and any other news either good or bad. I will call this the three-year life portfolio (3YL). The only time a change to the portfolio will be permitted is if a business is de-listed for any reason: the funds liberated would then be discretionally invested between the remaining stocks in the portfolio. The second portfolio will start out with exactly the same holdings as the 3YL but each January the same cash flow screens/returns on assets screen will be run and a revised set of ten stocks nominated. This revised set of stocks will have the proceeds of the sale of the previous years stocks equally divided between them i.e after one year we have £110k of funds then a purchase of £11k will be made for each of the ten stocks. I will call this the annual sit on your hands portfolio (ASH). The third portfolio will again start the same as the 3YL & ASH portfolios but I will alter the percentage invested in each position within the portfolio in reaction to RNS announcements from the companies, economic conditions or any other reason that seem valid for altering, reducing or increasing a position. I will call this portfolio the managed annual tinker portfolio or simply the TINKER. All 10 stocks will remain within the portfolio throughout the year although the investment in each stock may vary. For example, one stock, let’s say xyz Co. may issue a particularly bullish RNS “results will be appreciably ahead of market expectations”. The Tinker may sell down one or more of the other holdings to invest more in xyz company but still retain a position, although not equal positions, in the same 10 stocks that we started within January each year. In January 2017, 2018 & 2019 this portfolio would be treated in the exact same way as the ASH and funds equally balanced across the each of the ten stocks starting that year. The common rules for all three portfolios:

NOTE: A new section has been added to the Whittler: Voyager RNS Log where I take a weekly or thereabouts, review of any RNS stories that are relevant to shares that I either hold or are of close interest: see page in the header menu. It may seem a strange thought but it’s worth taking a little time to just ask yourself this simple question “why do you invest?” Yes, I know there could be a great many different responses to such a question; they could range from the most impractical to the very sound well-planned strategy. Whilst I suspect there are many individual reasons some of them may include the sensible such as “To make a better return than you could by simply leaving you money in the bank, building society or other deemed to be safe alternatives”. Then there are also the less sensible reasons such as “it gives me a thrill & I like the adrenaline rush” and the dreaded “I want to get rich quick”. So, whatever your reason for investing, another question, do you benchmark your portfolio on a regular basis or indeed, should you benchmark your portfolio? Well before we get into such a discussion, then let’s understand what I mean by benchmarking in the context of this article: always a reasonable place to start, so what are we talking about? Well, it’s about measuring the performance of your portfolio against an alternative investment vehicle or Index. For example, you could simply measure your performance against a soft “should be easy to beat” benchmark such as the FTSE All Share total return (FTSE AS TR). I say soft as that index includes such a large number of stocks including quality ones and ones not of such high quality. If you can’t beat the FTSE AS TR on a very regular basis, and incidentally most fund managers can’t, then maybe your benchmark finding is suggesting you should modify your stock picking approach. Of course, you could constantly put a smile on your face and benchmark against the Boris Becker Nigerian Oil Company system? No, sorry Borris but no thank you if only he had read the basket case blog! Alternatively, you could benchmark against a fund or guru style of investing that you respect or admire and that you would be happy to beat on a regular basis. Anyway, we will come back to my way of benchmarking after a few more paragraphs of background. Now let’s go back for a moment to consider why, at least in my opinion, you should benchmark. Well, Peter Drucker, the management consult and author of many books on management is credited with the quote "you can't manage what you can't measure." What Drucker is really saying is that you can't know whether or not you are successful in what you are trying to achieve unless success is defined, measures agreed and performance tracked. Ok, that’s fine enough but in the twilight world of our portfolio performance what does that actually mean? Well, firstly it means that we keep strictly accurate and honest records of our investment decisions both in terms of the reason behind each investment decision and the performance or that investment. Now to me having learnt the hard way many years ago from my experience in horse racing betting, if you don’t keep accurate honest records then your mind has a natural bias to place you in a fantasy place where you so fondly remember the winners and that feeling of exhilaration but anaesthetise the overall performance: in those long ago days was I making money or simply providing the good old honest bookmaker with a comfortable living. Needless to say, once I started keeping decent records on my betting activities my flirtation with the world of horse racing came to an abrupt end: I was just not making money simply letting the good times blot out the overall performance. Thankfully these days, dynamic record keeping of our transactions is made just so easy for us. We can use free tools such as basic brokers ledgers, the free portfolio services of the LSE to track transactions or the more sophisticated alternatives such as Sharescope/Sharepad. So, really, we don’t have an excuse for not keeping a track of progress. Record keeping is no longer an issue & we can keep Mr Drucker as we can measure our investment performance. That’s fine, we can measure our performance but does an average return of say 4% sustained over a number of years make it worth our while. Would we be better off simply handing over our funds to say Terry Smith of the excellent Fundsmith or Warren Buffett’s Berkshire Hathaway? So, we have the concept of measuring performance over a period of time and the thought of at least trying to beat the FTSE All Share Total Return; note, I say total return because dividends historically form a large percentage of one’s overall sustainable return. Our first measure then is to assess our total return over time against the total return of the FTSE TR and hopefully we can beat it in say four years from five. However, let’s make things a little tougher and start to measure against something more challenging than the FTSE AS TR. The choice of what we consider as tougher is entirely up to us but for my part, I like to measure against two highly respected large company funds; Fundsmith & Berkshire Hathaway whilst the smaller company funds I measure against are Henderson Smaller Companies IT and Marlborough Special Situations Fund. These benchmarks have performed excellently over the past three years with Fundsmith returning about 100%, Berkshire Hathaway 33%, Marlborough 50% and Henderson Small Co IT also 50%. In comparison the FTSE All Share total return has offered a still good but softer 26% return over the three year period. Graph below shows a simple benchmark comparison between my Tinker Portfolio & Berkshire Hathaway/Marlborough Special Situations/FTSE ASTR over the period since inception of the Tinker in January 2016. The software I use here is of course the superb Sharescope. Note: click or tap on graph to enlarge.  Now you might think that my approach to benchmarking is being a touch hard on myself but I prefer to think of it stretching as I take the view that to adopt realistic but stretching targets makes you improve at almost anything.

Finally, what do you do if you find you are falling short of the performance of your chosen benchmarks. Well firstly don’t panic if it’s just for the odd year or two and definitely don’t take foolish risks in order to bridge any gap. Secondly, remember that successful investing is about learning and then even more learning: take a slow detailed look at your stock selection, your risk management and also ask yourself are you ruthless enough to rapidly jettison losers whilst nurturing the winners or do you try to convince yourself that you will be right in the long haul and that loser will eventually turn. It’s my experience that by adopting a culture of benchmarking your performance can indeed make you a more successful investor. Happy Investing. NOTE: A new section has been added to the Whittler: Voyager RNS Log where I take a weekly or thereabouts, review of any RNS stories that are relevant to shares that I either hold or are of close interest: see page in the header menu. We are now halfway through the 3 year reactive/passive portfolio exercise: for the rules and structure then it’s worth referring back to the previous quarterly reports on performance: use the categories link on the right hand side of the page; passive/reactive folio. Just as a very brief refresher; the original 10 stocks of the Tinker and ASH (annual sit on hands) were reviewed and rebalanced in late January 2017 and had and had 8 of the original 10 stocks replaced. Following the rules, the 3YL (leave it alone and don’t do anything for 3 years apart from reinvesting dividends) was left intact with no rebalancing taking place. So the 10 stock portfolios have between them contained a total of 18 stocks selected from those stocks that formed my universe from which I normally consider purchases. That universe is considerably under 3% of the 2000+ combined fully listed & AIM stocks available for consideration. All all of the 18 stocks mentioned here are either still currently within my portfolio or have been at some time since the exercise began. The portfolio exercise described here started on the 22nd January 2016 with £100,000 invested in equal blocks of £10,000 between ADT, AMO, BOY, CCT, DTY, ELM, HIK, NFC, PSN & SOM. The January 2017 rebalancing/reappraisal of the Tinker & ASH introduced AIR, BVXP, D4t4, GFRD, ITV, TEF, SMWH & ZYT: all stocks that I had been holding for some time in my various accounts and all selected by my usual universe criteria on the basis of FCF, ROCE & CROCI. As mentioned previously in this series I am a great believer in the security of investing in a basket of stocks, in fact, I recently published an article on the subject of a basket of stocks “Guess I Am A Basket Case”. So, how are the various approaches performing at this stage as measured against each other and the fairly soft benchmark* of the FTSE All Share Total Return. The table below gives the performance data “warts and all” :-    * Note: I am shortly publishing an article on what I consider to be the very important subject of benchmarking your portfolio’s performance.

At the 18 month, 6th quarter stage, it’s quite amazing to see that there is nothing really significant in the performance of the three portfolios and they have all performed very well within fairly kind, although at some times choppy, overall market conditions. I suppose a couple of the reasons why the performances are so close are: 1. If you select quality companies that are already making decent profits, producing good cash flow and making a decent return on capital(ROCE, CROCI both over periods of time), then in my opinion you generally enhance your chances of success. 2. I am possibly not the best type of character to run the Tinker as I don’t listen to market noise or really make knee jerk decisions. In fact, I have only made a handful of reallocations (trades) within the Tinker in the 18 months it has been running; I simply tend to be a fairly laid back/patient investor. What I would say is that in my actual portfolio rather than the 3YL, HIK would no longer be in the portfolio as it would have been sold or at the very least a serious evaluation of whether to keep, sell or reduce taken when the trailing stop loss, at the time in profit, was breached. HIK would certainly have been jettisoned on the profits warning of 3rd August 2016. Selling on the day of that relatively average profits warning would have still retained a profit on the original purchase of 15% rather than the loss of -28% that detracts from the performance of the 3YL. Incidentally a couple of years back I did a blog article on my actions with profit warnings and since that time Stockopedia have also produced an excellent article on profit warnings; worth a read. In summary I am happy with the performance of the stocks discussed in this series and indeed many of them form the top 10 or 20 holdings from my current portfolio holding of about 30 stocks. Just by way of a slightly different tack to this quarter's update, at some time I will include within the Stockwhittler site either an article or more probably a section on my investment disciplines that I apply to myself. Until I get that from draft to finished, although I guess such a thing will never really be finished, a couple of tasters but remember this is not advice but rather me sharing my approach to investing: 1) Use a trailing stop loss at all times. Now, by that, I don't mean an automated stop loss set on the broker's software that automatically sells when you bridge say a 12% trailing stop loss. No, what I mean is a real "wake up moment" where you totally and UNEMOTIONALLY evaluate that holding: ask yourself based on the current information at hand, would you a) genuinely buy that stock today if you did not already hold a position i.e. make a totally new addition to the portfolio & b) just for a moment, forget about what apparent attractions the stock may have and seriously and I do mean seriously, evaluate the potential of any further downside within that investment. c) if after a & b you are not totally UNEMOTIONALLY convinced, then simply sell; you will probably feel better for it, after all, you can always reinvest but with an uncluttered mind and so remember so importantly, I have preserved capital. 2) Almost invariably sell as soon after the market opening as possible on a profits warning. A PW almost certainly means several months of gradual decline in the share price until the management actions kick in and Mr Market begrudgingly starts to forgive the business. Again, it’s about preserving your capital. 3) Whatever investment software you may possibly decide to use DO take the time to become so totally familiar with what the system has to offer. Just that simple learning process will in my experience be a very worthy investment of your time. 4) Do not listen to market noise and in there I include the stuff that is churned out daily by journalists, brokers or the media in general: simply stay unemotionally focused. Well, that’s it for this quarter’s update. The markets have been in our favour and sensible investing has paid a handsome financial return. However, who knows firstly what the general market conditions will be in the next 12 months? Indeed, in my usual sober way, remember that no matter what basket of great stocks you hold, the next profits warning could be just around the corner: all part of the varied tapestry of investing! As ever, Happy Investing I suppose that you could feel rather hurt if a friend or colleague described you as a basket case but in the world of investing, that’s what I am. So why am I a basket case? Well that's easy to explain really in that I seek the comfort of a collective of stocks within my portfolio rather than simply relying on one or two stocks; it’s all about that simple old concept of managing risk. For me, investing needs to be something I do that will hopefully make me a positive return on my capital whilst being able to sleep soundly at night. I painfully recall the days back in the late 90’s when at times I ran a very concentrated of just a handful of stocks, at times about four or five, and experienced what an underperforming stock may do to both your concentrated portfolio and indeed, your serenity.

You could well ask why don’t I become the ultimate withdrawn basket case and just invest in managed funds which after all usually have upwards of 40/50 stocks and frequently more. Well, the sad truth is that an alarmingly high percentage of fund managers dismally underperform the market. Ok, there are some star managers out there but I would say that over time you would be better off investing in a low-cost tracker than a managed fund. Why are the fund's performances generally so poor? Well, a fair part of this is down to the manager’s fear of falling below the index for that particular style of fund; not only could the fund manager’s bonus be at risk but after a couple of years of underperforming indeed his continued employment which is often determined by how he performs against his peers. All a bit of a sad situation that results in that large percentage of fund managers, despite having a fairly substantial basket of shares, failing to do even achieve the performance of a simple tracker fund. However, as private investors, we have within our grasp quite incredible control of our investment universe. Firstly we can use whatever screening, research or other technique that selects that universe from which we decide to buy a stock from. Secondly, we decide how much of our “hard earned” we want to expose to that purchase: yes, with every purchase there is an element of risk but there are ways of mitigating that risk but risk in general terms calls for a future article dedicated to the subject. The risk we expose ourselves to is in my view especially great if that stock is the only holding within our portfolio. Well, you may ask surely with that one share we can simply sell if things don't progress as desired and the price drifts slowly down. Well, yes we can in that scenario we can sell easily and move on but with every stock, I am always mindful that a profits warning could be just around the corner. Now a profits warning can hit the really big boys as well as the tiddlers; look at retailer Next & rail/road passenger operator Stagecoach both of whom dramatically dropped before the markets opened with a 7 am RNS profits warning, you simply don't have the opportunity to react before the initial mark down of the share price on bad news. Yes, you can sell rapidly on a profits warning as I invariably do and thus avoid the next few months of gradual decline but you just can't avoid that early pre 8 am hit; don't lose sleep over it but do ruthlessly manage it. That risk can certainly be greatly reduced by holding more than one stock i.e spreading the risk: by holding two stocks, if one suffers a profits warning and the unfortunate stock falls by 20% in value, the damage is balanced over the portfolio and the bottom line suffers by only 10%. However let's say we own five stocks, then that hit on the value of the portfolio falls to a still uncomfortable but manageable 4% assuming equal weighting of the stocks. Doing the maths, the loss following a -20% drop on a profits warning falls to 2% with ten stocks and only 1.3% with fifteen stocks. What has this taught me over the years is that I feel comfortable and certainly more secure in being a totally committed basket case with that basket of shares in my portfolio usually comprising around thirty stocks which I don't find anything of a challenge to manage given the wonderful IT available at the click of a switch; no idea how I managed back in the 90’s but to be fair I rarely exceeded eight or ten stocks in those days and at times as little as four or five; I remember the uneasy sleep pattern only too well. Now being a basket case has other advantages of course as well as impact of profits warning mitigation:

Is it more expensive being a basket case? Well possibly it is marginally more expensive in terms of dealing charges but you can minimise that cost by using a £5 or so per transaction broker. The tax charge in terms of stamp duty is the same; here I am leaving to one side the differences between duty on the main market and AIM. As you know, I don’t offer advice, I merely whitter on about my thoughts but if my relative Matt Tress, he was the subject of an earlier blog, were to ask me my opinion of the minimum number of shares he should accumulate, then I would say about 15 shares. Why do I say 15 stocks? Well, The simple fact is that even the very best investors we read about simply don't get it right every time in terms of every share purchase becoming a winner. In fact, I was listening to a podcast recently when one of the very most universally respected investors said that around 6 out of 10 of his picks are not successes: as ever, it's the way you manage your portfolio that is crucial; ruthlessly jettisoning the stocks that the market does not smile upon. So if we have a basket of stocks rather than just the odd one or two, we can continually improve the performance of that basket by managing those under performers whilst building possibly larger positions for the appreciating stocks. I use this culture constantly in my own portfolio ruthlessly without sentiment or regret, weeding out any underperformer before it can have a material effect on the portfolio. The strange thing is the way we are emotionally wired and the sense of relief one feels having had the courage to exit a losing position. So in summary, my reasoning for being a committed basket case is:

Happy Investing Well, watching the detectives, yes a great old number by Elvis Costello back in the late 70’s and in terms of investing maybe something that private investors get overly hung up on; watching the share detectives. But hang on, who are the share detectives? Well for the purpose of this article they are experts who give their advice either freely or not so freely via subscription. Now there is nothing wrong in reading about the views, impressions or recommendations of a respected guru and there is especially something really positive if you can learn and develop as an investor by building on the messages many of these articles/books contain.

Well, my first real share detective: Many years ago I used to almost hang on to every word Jim Slater said; his column in the Mail on Sunday simply used to move the markets the following Monday such was his following and for many people that was simple enough. Jim recommends Blacks Leisure, DCS & Parity; off they would go being probably marked up by 10% or so by the market makers when the market next opened. Now that in itself was fine: after all Jim’s style was to seek out attractive companies that were in a fairly good financial state, already making real profits and with the prospect according to brokers, of continuing to enlarge those profits. Jim would explain in his articles what he saw as attractive about a company that would prompt him to highlight the situation for potential investment. As I say that’s all well and good but as I see it the danger with an inexperienced private investor is that they may get too used to that comfort zone where a share detective identifies the opportunity and they progress no further. Now sadly that great man Jim Slater passed away a couple of years ago but for anybody even the slightest bit willing he left behind him a legacy of teaching as exemplified by his superb book the Zulu Principle. The title itself just like the entire book had easily understandable reasoning of his approach to identifying attractive opportunities. Our Jim was essentially a growth stock investor and of course, there are other share detectives/experts out there who have equally successful approaches to investing: value investing, momentum investing, special situations etc and their writings are available on the net either freely or via a paid subscription. The general approach is to argue the rationale for a particular stock they identify and what makes it a potentially worthy investment etc. For some private investors that’s the end of the research story, they simply pile in and buy the said recommendation; hmm, well maybe not so good if you want to develop as an investor but that’s just my opinion. What I would urge any aspirational private investor to do is learn from the experts and not to simply follow “Captain Marvel, Tom, Dick or Harry have bought this stock so it must be good; here I go”! One thing that I regularly see on a very good subscription investment site is the reaction of a private investor when the said expert does not include a review of a company that issues an RNS that day. The reaction that saddens me is “Paul, you did not review Alchemy’s results, could you take a look at them please and give us your thoughts”. Now if somebody is a novice and seeking simple guidance or an investor not feeling confident enough to back their own judgement until said share detective give a favourable assessment, then that’s all fairly understandable but the investor in my opinion really has to move on and start to use the many resources available these days particularly on the net today to develop themselves as a serious private investor. Now you may be reading this article and think “I am already at that stage of my investment journey, I already do my own research”, well that’s fine and with sensible risk management I suspect you will have significantly increased your chances of achieving acceptable investment returns. However, for those that have yet to start to dig into the world of doing your own research as they say, there is just an incredible wealth of stock information available. Sites that I find to be particularly excellent are Sharescope/SharePad and Stockopedia. Yes, you have to pay a subscription but the data is good, reliable and as time progresses, easily understood with the added benefit of a team of helpful experienced staff who whilst not telling you to buy this or that stock will provide a supportive environment for you to learn and gain the confidence to become hopefully a share detective in your own right. What are the risks and rewards of developing yourself as a more independently minded investor and I am not talking about the gamblers who invest in the roulette of AIM resource stocks, blue sky/jam tomorrow companies. One of the risks is that possibly half of the time your investment decisions won’t turn out to be winners; they will need early and ruthless management. Half, oh dear I hear you say but if you were to keep an eye on these highly followed share detectives you will soon become aware that:

Even with these mistakes and in the second case “rush of blood to the head”, the private investor can learn two incredibly important lessons:

What really matters is how these expert guys or indeed yourself handle those less than good investments and how they nurture their success: again lots of share detectives freely give their approach to these situations that as investors, we encounter all of the time. Unfortunately, even some share detectives remain foolishly optimistic about a favoured, I should really say loved, stock when the momentum clearly indicated that one should head for the exit door; the expert may well be fallible and the emotional illogical part of the brain overrules cold unemotional logical reason. If you have hung on to this article and got to this stage, then I would suggest that for any investor to really improve that they should certainly not simply blindly buy into whatever stock our detectives particularly like but to rather learn from their methodology & what wisdom they are so kindly and freely sharing. By all means, ask questions, be curious and above all try to develop yourself as a private investor capable of identifying attractive opportunities. The key messages from this article are:

Anyway, before I close, I will leave you with a small reading list that in my world is a dynamic list as it changes as all too rarely an excellent book or worthwhile article emerges. It’s not an exhaustive list but hopefully one that you may find useful: The writings of Jim Slater The books by Robbie Burns; The Naked Trader The reasoning and exposure over the years by the superb Terry Smith: do you know, I am certain that Terry would take it as a compliment if I described his approach as boring; I just love boredom in my portfolio. The articles and wealth of guidance on Stockopedia including the excellent teaching of Paul Scott. A couple of very recent yet excellent publications: The Art of Execution by Lee Freeman-Shor and Phil Oakleys just published book How to Pick Quality Shares. Also very much worth a listen once you tire of Elvis Costello are the podcasts from Conkers Corner where he interviews private investors who describe their investment journey. A number of very good blogs also exist written by private investors and they are well worth a read and in my view far more worthy than the often poor articles written by lazy journalists in the investment magazines or newspaper investment sections. If you managed to read right to the end of this article, then we'll done and I hope you find the thoughts contained useful. Happy investing! |

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed