|

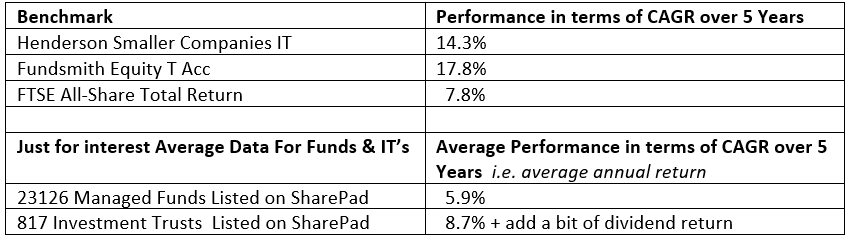

Anybody who reads the Whittler Blog as I ramble on about my investment universe will be aware that I don’t overly pay much attention to short-term portfolio performance as I think that a true assessment of performance can only be made over a period of say three years and preferably five or more years. In fact, the only time real portfolio performance can finally be assessed is when Mr Grim Reaper has called; blimey, that’s cheerful stuff. Let’s move on quickly and have a look at the small time window of 2017/18 and see how things went. Note: I always consider the tax year end as a time when one really does need to assess profit and loss: it simply fits in with the new tax year and therefore has to be done. When I previously used to write about portfolio performance, I used to quote actual percentage moves and compare this to my benchmarks. However, after much discussion considering the merits of such a definite declaration approach of percentage portfolio movement over time; this deliberation included input from respected investors, I wrote in a recent article that in future I will simply say if I have beaten or failed to beat the benchmarks I measure my performance against. I will quote the various the benchmark percentage performances and then simply say if my portfolio has fallen below, matched or beaten those benchmarks. The reasoning behind this is that after a great deal of thinking and discussion with others is that your performance needs to be measured against what targets are pertinent to you. For example, what are you trying to get? Is it simply high income or steady capital growth or maybe you like the blue sky stuff. Also, and it’s just an observation, it seems to be a fact of life that investors & horse racing punters are sometimes happy to report the wonderful stuff but less likely to report the poor stuff. Finally, and this is very important, somebody with let's say 10% of their savings/capital invested may well be more open to risk than say the individual with 80% of the precious dosh invested: what I am saying here is that the bigger your capital pot grows, the more likely you are to be increasingly selective with your stock selections minimising to almost zero punts and concentrating on stocks of proven quality. At this point, I should give a reminder of my philosophy on what one should benchmark against. A very popular benchmark for investors is the FTSE All-Share Total Return with the argument that you are measuring your performance against the full market and including dividend return. Now whilst I can see the rationale for that, it is not a terribly challenging benchmark as it includes the good the bad and the ugly stocks; simply put, it’s a low benchmark. My preference for more challenging benchmarking is to raise the bar a touch and find a benchmark that matches more closely your investment style. Now my investment style has a bias away from the FTSE 100 preferring smaller companies: hence one of my benchmarks is the Henderson Small Companies IT. Now don’t be confused by the small companies tag on this Henderson IT as many of the companies are at least mid cap but overall quality businesses. The second benchmark I use is one that matches very much my investment philosophy in terms of companies that make very good returns on capital and good free cash flow: that benchmark is the very excellent Fundsmith. My way of thinking is that over time if I cant beat Henderson Smaller Co’s IT or Funsdsmith then simply hand my money over to them and go fishing, down to the pub or whatever grabs your leisure interest. Incidentally, in a separate portfolio, I do hold a respectable investment in Fundsmith as it offers me that non-UK exposure and also an investment in Henderson Small Companies IT. So, after painting the background rationale, how has my approach done in the financial year 2017/18? Firstly, the main thrust of the portfolio that tends to concentrate on two mini-universes of stocks: companies that make good returns on capital & have attractive Free Cash Flow characteristics and secondly what I term as special situations, companies were something is changing for the better. This section of the Voyager performed well in the FY 2017/18 and was comfortably ahead of all it’s benchmarks in terms of total return. The benchmarks returns are shown below:  For the Voyager which currently holds a couple of dozen shares, the star performers were: KWS @ over 100% Stocks in the 40% to 80% range: OTB, DTG, XPP, ABDP, BVXP, & three that have been sold: RBG, ZYT, JE. & IQE. A fair number of others also earned their keep delivering in the range of 15% to 30% total return. There were of course stocks that did not earn their keep and in the Return on Capital /FCF segment my blind spot was ITV. Other stocks that may have caused harm were jettisoned usually after a less than encouraging RNS: DTY for a small profit that could have turned into an almighty loss, FUL, GFRD that if they had not been sold would have been harmful and finally ZYT where profits were taken in stages before a 35-50% decline in share price. The Boring Bit As ever, I firmly believe that the art of managing a portfolio and the protection of one's capital is of almost equal importance to stock selection. When I research a stock, I spend a very significant amount of time looking at the potential downside as well as the sexy upside part. You can carry out your risk assessment during your research but unfortunately, you just don’t know what the future holds. In truth, if an investor selects say 10 companies that meet their required criteria and invests in those 10, you may well find that 2 or 3 do very well indeed; another 3 or 4 do reasonably, a couple tread water and finally, a couple head slowly south. I suspect this outlook is typical for most private investors if they were to buy 10 stocks. Also, every one of us without exception will have held a stock that issues a profits warning RNS; ouch not nice but simply an occupational hazard we WILL encounter on our investment journey. What makes the crucial difference in the performance of that basket of stocks is how you actively manage those stocks. By this, I mean continually topping up the winners and jettisoning those not displaying the momentum that you desired. I am not talking about chopping & changing or being simply impatient as with quality stocks it can take time for them to grow. What I am really trying to get over is once the story/rationale behind your purchase moves from compelling to risky, you take swift action to protect your capital. With the uncomfortable situation of a profits warning RNS, I rapidly evaluate and in 95% of cases sell at the opening bell. When confronted with the evidence that a stock for whatever reason, is proving a serious threat to one’s capital, I without emotion or regret jettison that stock: self-denial & procrastination are in my view simply serious risks to portfolio performance. Returns are of course much more correctly assessed over a much longer timescale than one FY as that’s simply a snapshot in time. I really think you should consider a period of at least three and preferably five years to get a real feel for performance and with that thought in mind let’s have a look at the compound annual growth rate (CAGR) for my benchmarks. I believe that for all but the income/high yield investor, these should be the type of long-term returns a private investor should aim to surpass if he/she is doing reasonably well. Note: if you are relatively new to investing and did some staggering 40%+ stuff in 2017, then please don’t get comfortable and think that’s the norm as it simply is not the case. If you can achieve let’s say a total return of 16% per year over many years, taking fully into account the good and less good years, then you will be a very successful investor. Anyway, the CAGR for my benchmarks over five years is:  Comment: in truth, if you were a touch selective with the better Investment Trusts & relied on Uncle Terry Smith for your OEIC, you would have done fairly well and had a lot of leisure time and maybe a lower blood pressure! I am not suggesting that this is the way for us private investors to go, merely my whimsical observation. Incidentally, as mentioned elsewhere, I do hold Fundsmith & a few ITs; I really am quite a fan of investment trusts but these sit in my separate passive portfolio.

The High Yield Portfolio Turning to the High Yield portfolio, it’s been a decent enough 2017/18 but not quite as outstanding as the previous year. I reckon that over time on a high yield portfolio you should set a baseline target over say five years of something in the order of an annual 6% post-tax return; you don't really want to target any lower than this in my opinion as you need some compensation/reward for the risk you are taking on the stock market. For the FY 2017/18, the high yield comfortably beat this baseline even though it was somewhat bruised by BT & SSE. So a decent income year but not quite as good as the previous FY which was maybe a touch exceptional. Note: as ever when I seek candidates for my high yield portfolio, I seek companies whose dividends are well covered by free cash flow; the exception, of course, being the likes of utilities. Conventionally most investors look for dividend cover in terms of the ratio of EPS/DPS but as EPS is often so open to manipulation by overly eager CEOs who love their annual bonuses, I much prefer to use the ratio of the number of times that FCF covers the dividend payments. The odd miss is forgivable especially if there are obvious reasons such as capital investment to grow the business. Overall FCF is so much more difficult to apply the “smoke & mirrors” treatment to than the often manipulated EPS. Just a thought but I strongly suspect that not many companies assess the CEO/CFO bonus measured against criteria that include ROCE/CROCI trends FCF & share price combined in a set of annual bonus targets; silly me! So, that’s a quick review of FY 2017/18 with a bit of whittler philosophy plus being as ever aware that your next profits warning may be just around the corner; simply an occupational hazard. I hope all readers have a successful 2018/19. Happy Investing!

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed