|

Don’t you just hate it on the daily routine of looking at RNS’s for companies in which you have a holding issue the dreaded words that appear in colour on your chosen highlighter. Well this morning a company I have held stock in for a fair while and added to just a few months back, issued the following: Total revenue for 2016 is expected to be ahead of 2015, notably because of the recent acquisition of the Wax Lyrical business. However, pre-tax profits are expected to be materially below the record level of £8.6 million reported for 2015. At the Annual General Meeting, we reported an unexpected decrease in demand from Asian markets. In particular, sales to South Korea still show no signs of recovery and the performance of our distributor in India has continued to be extremely disappointing. In addition, we have seen negative effects on demand in the UK before and following the leave vote at the EU referendum. The potential benefits of a weaker pound have yet to translate into firm overseas orders. However, the United States continues to perform well. That phrase materially below, never sits well with me but such is life particularly with smaller companies; simply a part of the inherent risk/reward we have to live with when investing in the small market capitalisation stocks. Now my normal practice on a profits warning is to ask myself the question every 10 seconds for 30 seconds and just about always come up with the same rapid answer of SELL. It has served me well in the past and certainly limited losses indeed since commencing writing about my buys and sells in this blog, swift action got me out of Sprue Regis at 185p; they subsequently fell to 120p and have as of today, partly recovered to 145p. I appreciate this approach is not for everybody but experience over the years has taught me to bail out as soon as I can on a profits warning thus hopefully limiting my losses. If I get it wrong and the company subsequently start to recover and the fundamentals still appeal, then I can always buy back in again. Returning to today’s announcement from Portmeirion, I went back through recent trading updates and their final results issued on 19th March 2016. What I wanted to do was to take a good look at the geographic spread of their sales:

So we have the USA which is doing ok, the UK was doing ok but already seeing signs of a pre & post-Brexit slowdown, South Korea not recovering as previously planned and India, last year’s star, now listed as “distributor continued to be extremely disappointing”. Wax Lyrical, the recent acquisition, is also mentioned and credited for the reason for 2016 revenue being ahead that of 2015. Now Wax Lyrical was to my mind a decent bolt on acquisition but the thought that it really struggled through the last downturn did not quite light that candle for me.

All in all, I took the decision to sell. My initial purchase was at £6.50 but the top up at £11.40 so overall a minor kick on the portfolio but even though I am heavily in cash at the moment, I expect that these minor kicks to become fairly frequent over the next two or three years of political turmoil as the “baby boomers lead us to salvation in a chorus of land of hope and glory”. Yes, I am very bearish at the moment. I actually think in three years time we will be absolutely fine, maybe even stronger than had we remained within the EU, but for the moment I am a bear looking at a potentially painful and unsure path to the future.

0 Comments

I rather like the acquisition of Lighthouse Holdings by Portmeirion announced today, Lighthouse own Wax Lyrical Ltd the UK's largest manufacturer of home fragrances. They produce such items as reed diffusers and scented candles and there seems to be good demand from the public for such items with every supermarket stocking various varieties of each. Amusingly I first came across reed diffusers a few years back whilst staying in a rather nice Hong Kong hotel. I was washing my hands in the plush bathroom and thought I would try this “rather nice oriental handwash in a bottle containing sticks for application to ones hands”; enough said!

The £18m acquisition won’t in my view have any real impact in terms of carrying debt as the £18m consideration has been funded from cash reserves and debt draw down on new banking facilities comprising a £10 million loan facility, a £10 million revolving credit facility and a £2 million overdraft facility from Lloyds. Previous to this acquisition Portmeirion had no debt; a market cap of £127.6m and an enterprise value of £116.5m so no worries at all there. Lighthouse looks a solid business these days and the accounts for the year ended 31 December 2015 recorded revenue of £13.8 million, a pre-tax profit of £2.1 million and net assets as at 31 December 2015 of £7.6 million. That’s a very decent operating margin of 15% which bolts nicely onto the latest declared operating margin for Portmeirion on 12.5%. Incidentally Portmeirion have grown this margin year on year over the last six years. I particularly like the comments in the RNS: Strategic Highlights The Acquisition brings the following strategic benefits for Portmeirion:

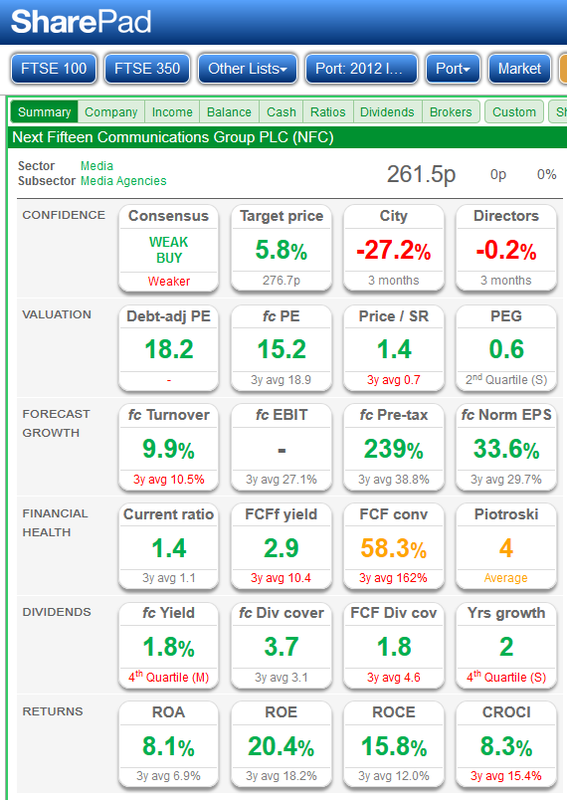

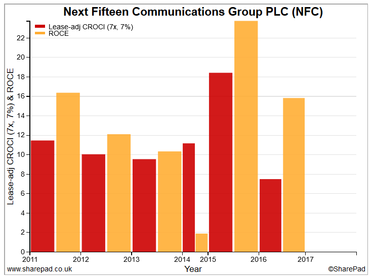

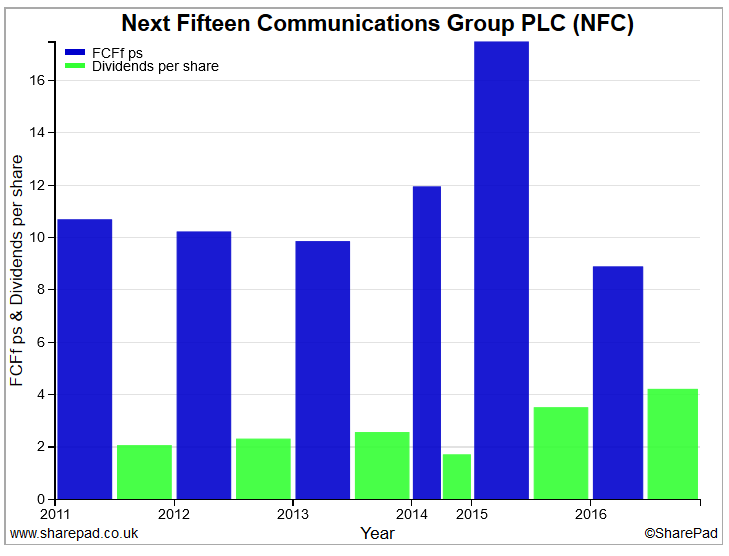

It’s also good to read that Joanne Barber, the current Managing Director of Wax Lyrical, will continue to run the business: always good to see continuity. I did blog a note on the 17th April regarding my top up of my Portmeirion holding and all in all I am a happy holder. It appears that Mr Market is fairly happy today with the news as the share price has nudged up a modest but pleasing 3%. It’s time I gave an update on portfolio activity in the last few days. There have been three new additions to the portfolio and one top up of a current winner. The new additions include two purchases identified my cash is king screen/free cash flow screen (CashKi.FC, not a third division Polish football club but a screen I regularly use to identify companies with good free cash flow and good returns on capital). The new additions are Next Fifteen Communications (NFC) and XP Power (XPP). One purchase of a fairly boring buy steady consultancy, Waterman Group (WTM) and finally a top-up of a current holding in Portmeirion Group (PMP). NOTE: I am moving to use a financial dash board as per SharePad on my blog notes when discussing share purchases and sales. For those who do not use SharePad, I can only suggest that you give it a try: a totally superb tool in my opinion. Next Fifteen Communications: Market Cap. £189m NFC previously held and allowed myself to get bumped out by the “noise of experts”; quite silly really, you listen to the noise, ignore the numbers and the genuine news and before you know it you have hit the sell button. When I sold NFC I had made a 90% total return in 12 months but the fear of losing some profits combined with that dreaded noise resulted in the sell button being pressed. Had I done the sensible thing and just let the trailing stop loss do its work, I would have made a gain of around 220% for just holding for another 18 months. A strange part of investor psychology is that it can be very difficult for an investor to convince themselves to go back and buy a share that they have previously sold at a lower price having taken a profit; just the way we are wired I guess! Anyway, my CashKi.FC screen kept showing NFC and in addition, I was impressed with the finals for NFC delivered on the 12th April; summary below. Final Results of 12th April 2016 Highlights:

Current trading and Outlook Looking ahead, the Group has made a good start to the new financial year with trading patterns continuing as in the second half of our last fiscal year. The Group has made two further acquisitions in the UK of Publitek, a specialist content agency, and Twogether, a technology-focused digital agency. My View So there we are, a purchase that as with most of my purchases will not be looking to generate a fast buck. I will use an initial 20% stop loss on ShareScope but manually execute if applicable. Price target? Well, I will set a target of 20% TR and review if we get to that level. Oh, for good measure a fairly decent Stock Rank of 78 on Stockopedia and a value of 18, equivalent to 82, on Sharelockholmes: with Stockopedia 100 is best and it’s reversed on Sharelockholmes with the lower figure being the best. The financial summary looks attractive, the returns on capital CROCI/ROCE are attractive and the dividend is well covered by FCFfps.

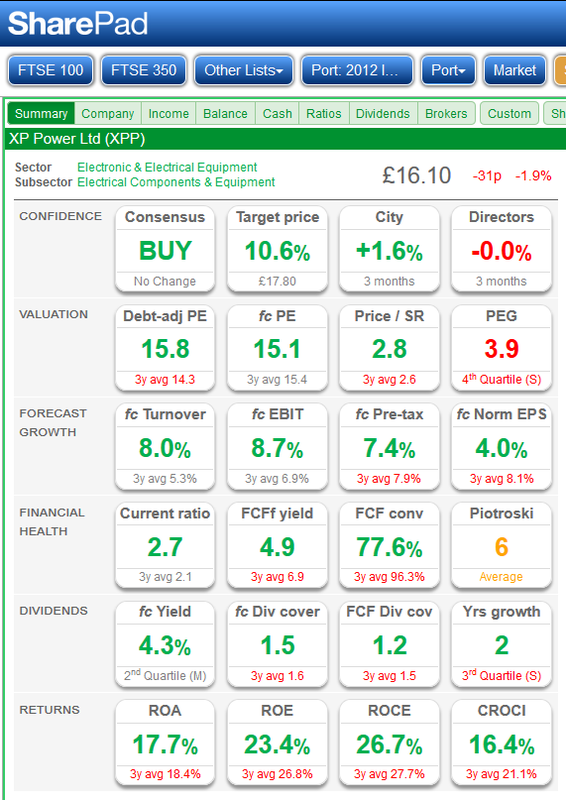

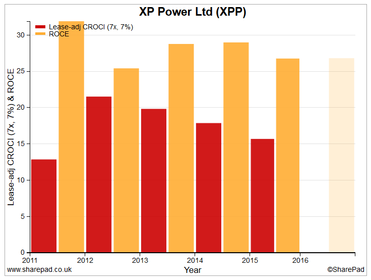

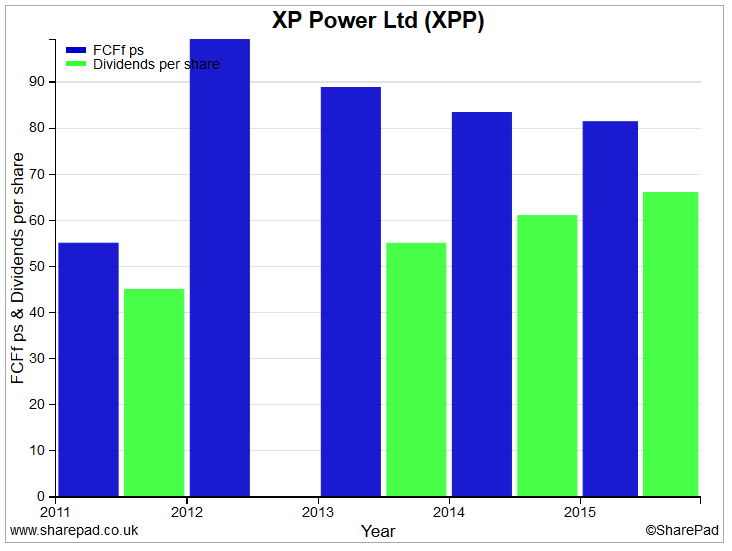

XP Power: Market Cap. £310m Another share that came through my CashKi.FC screen is XP Power. It’s not a share I have owned before but it’s attractive enough for me to make a purchase. They produced their most recent finals on 22nd February and whilst not stunning, they were solid.

Outlook We are encouraged by the stronger order intake experienced in the fourth quarter of 2015 following the weakness we saw in the North American order intake in the third quarter and by the progress of the integration of EMCO. Despite the mixed global economic picture, we have positive momentum and therefore expect further growth in revenues in 2016. We now have a high voltage product offering, which we believe we can grow using our direct sales channel and approved supplier status with our existing customer base. We also have a strong balance sheet and a business model that provides excellent cash generation to fund our existing needs and targeted acquisitions to further broaden our product offering and engineering capabilities. Trading Update 11th April 2016 Trading in the first quarter has been strong. Group revenues in the three months to 31 March 2016 were 28.2 million (2015: 25.6 million) up 10% from those achieved in the same period a year ago. In constant currency, revenues were up 6%. My View I am attracted by the financials, excellent free cash flow and the prospects for steady growth in profits. For good measure, Stockopedia have a Stock Rank of 94 whilst on Sharelockholmes they have a value of 3 which is 97 in Stockopedia terms (with Stockopedia 100 is best and it’s reversed on Sharelockholmes with the lower figure being the best). The financial summary looks attractive, the returns on capital CROCI/ROCE are attractive and the dividend is well covered by FCFfps.

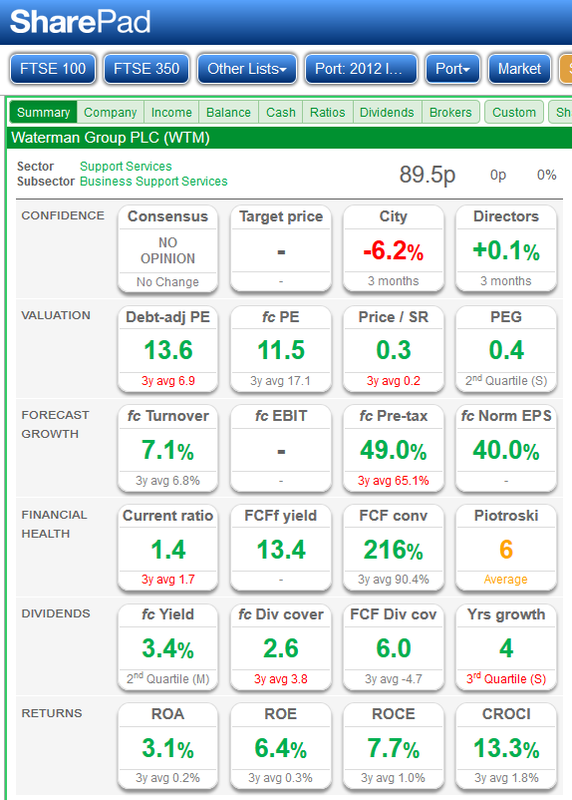

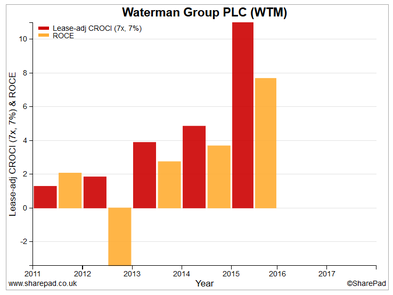

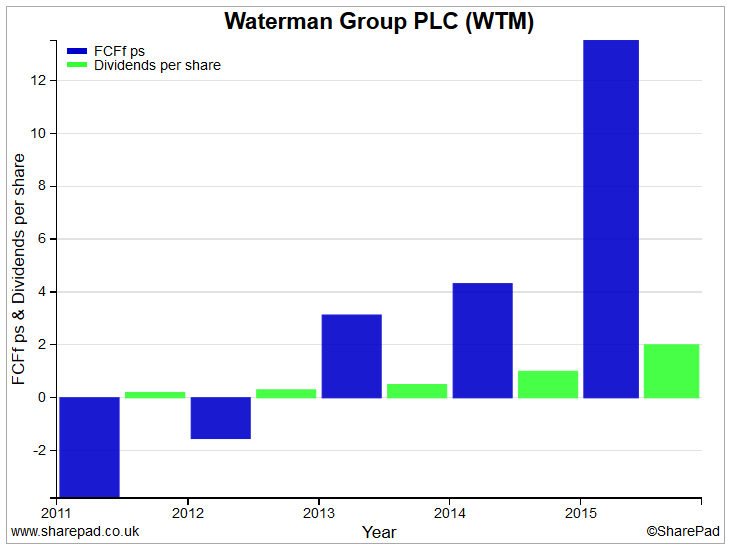

Waterman Group: Market Cap. £27m This one is a fairly boring consultancy group. The Company, through its subsidiaries, is engaged in the provision of design services and advice in the fields of civil, structural, mechanical and electrical engineering together with environmental and health and safety consultancy. All fairly unexciting stuff but somebody has to do it and also make money at the same time. In truth, they are a touch on the small side for me with a market cap of around £28m. They don’t have any debt and after a fairly lean 2010 to 2012, their operating profits have been climbing nicely resulting in net profit in 2015, decent projections in both the current FY and next FY. The business is cyclical by nature and not very high margin. Heavens, I am almost convincing myself to sell it as I read the text I am typing! No, seriously I do feel there is scope for some SP appreciation and they also carry a fairly decent yield at over 4%. However, the most interesting part sits in the outlook statement below with target increases in PBT, ROCE, and operating margin. Highlights Interim results of 29th February 2016 6 months to 31 December 2015

Outlook Waterman is on target to exceed its previously declared financial objectives to triple adjusted annual profits before tax to £3.3m over the three year period to 30 June 2016, with a return on capital employed (ROCE) of 20%. In October 2015, the Board announced a new aspiration to increase the Group adjusted operating profit margin to 6.0% by June 2019. As noted above, the Group's progress against this objective is positive with adjusted operating margins increasing from 3.3% to 4.1% over the last twelve months. The Board expects further progress to be made during the second half of the current financial year and beyond. The results have benefitted from the Board's strategy of focusing primarily on the UK, where 90% of Waterman's revenue is now generated and this focus is anticipated to continue for the foreseeable future. Waterman's long-standing relationships with blue chip companies continue to generate repeat business year on year and the Board expects this to continue whilst the UK economy is strong. The Board looks to the future with confidence. My View I quite like the business and whilst not wanting too many of it’s type in my portfolio, I feel comfortable enough to have bought a reasonable but not large holding in terms of % of my portfolio. For good measure, Stockopedia have a Stock Rank of 99 whilst on Sharelockholmes, they have a value of 4 which is 96 in Stockopedia terms (with Stockopedia 100 is best and it’s reversed on Sharelockholmes with the lower figure being the best).

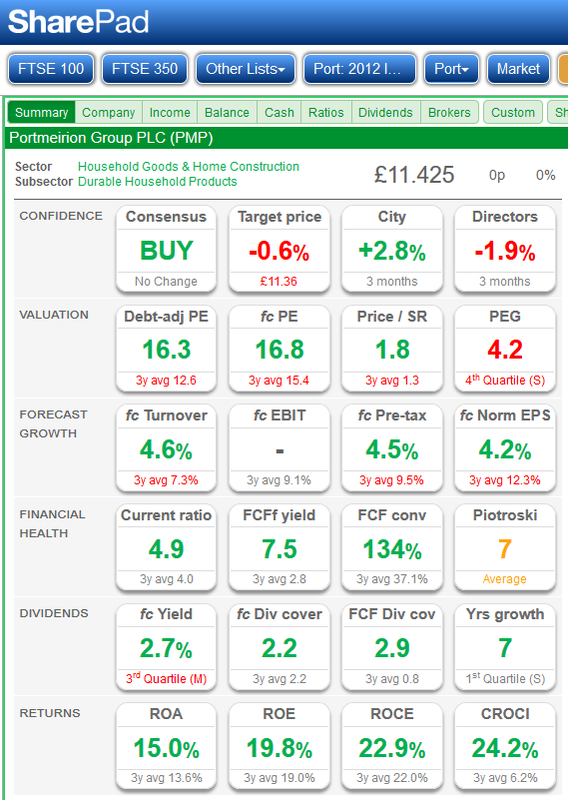

Portmeirion: A Top-Up: Market Cap. £130m Simply another top up of a current holding that has already given me an increase of 80% since my original purchase two years ago. A nice boring, unexciting company with steadily rising revenue and associated profits and offering a yield of just under 3%.  Happy investing!

|

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed