|

International Greetings issued a trading update in relation to the 12 months ended 31 March 2016. The Trading Update Reads: Financial performance is ahead of expectations, resulting in a further year of double digit earnings per share growth Operational cashflow and debt reduction continues to reduce leverage significantly ahead of expectations. Property held available for sale at Aberbargoed in Wales was sold with proceeds of £1.45m received on 31 March 2016 The strength of our performance and resultant cash generation underpins the payment of a final dividend for FY16 ahead of market expectations. The Company intends to pay a final dividend of 1.75p, resulting in an overall full year dividend of 2.5p (FY15: 1.0p) The Group is delighted to confirm that all regions have delivered year on year growth and an overall outcome ahead of market expectations. In the UK and China, record sales combined with an excellent manufacturing performance has delivered profitability ahead of forecast. In Continental Europe, sales growth and effective management of mix have successfully mitigated anticipated foreign exchange transaction headwinds. Trading in the second half of the year in Australia has resulted in significantly enhanced overall total profitability. In the USA, the commercial, operational and financial performance of our business has been extremely encouraging. This has included the successful implementation of phase 2 of our programme of fast payback investment in manufacturing. This investment will accelerate and enhance our capability to profitably grow our share in the world's single largest market. Commenting on the year's performance, Paul Fineman, Group CEO, said: "It is especially pleasing that we can report profits growth throughout all regions of the Group. This is a particularly exciting stage of our development in which we remain well positioned for organic growth and continue to seek compelling acquisition opportunities. Our culture of continuous improvement and our focus on creating commercially successful designs and products delivers a winning combination for our customers and trading partners. We are delighted to be meeting our core objectives of growth in underlying EPS and dividends whilst reducing average leverage all ahead of schedule." My View It’s always nice to see such a very positive trading update especially one which shows all areas of the business progressing well. I also like the large proposed increase in the dividend moving to 2.5p from 1.0p last year: whilst not a massive dividend, the increase does show confidence. I would expect some revision upwards of broker’s estimates and hopefully a further life to the share price. Although I don’t tend to select shares solely by either the Stock Rank of Stockopedia or Market rank equivalent of Sharelockholmes, I do tend to look to see what they score for my holdings. IGR reassuringly has a Stockopedia Rank of 93 and a Market Rank of 4 (equivalent to 96 when compared to the Stockopedia rating). Happy to hold!

0 Comments

Purchase of International Greetings (IGR)

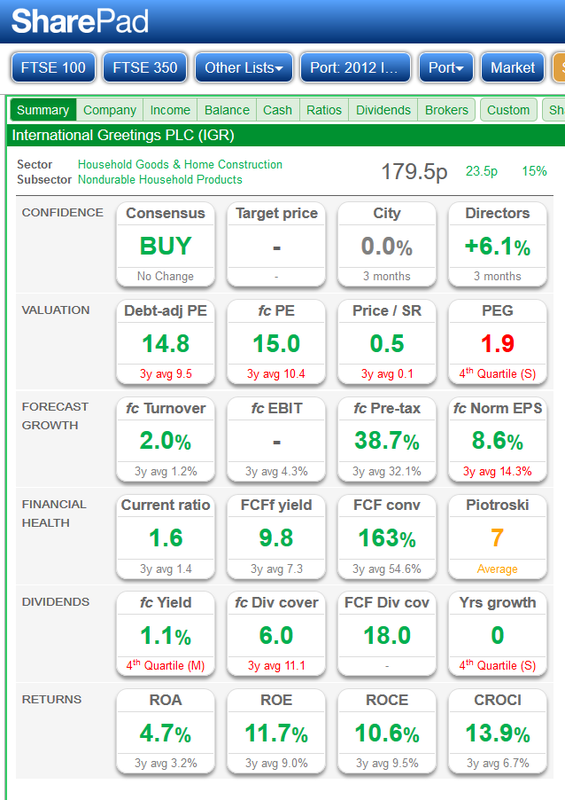

What do they do? International Greetings plc is a United Kingdom-based company, engaged in the design, manufacture and distribution of gift packaging and greetings, stationery and creative play products. The Company operates through four segments: the United Kingdom and Asia, Europe, the United States of America and Australia. Its gift wrap products can be supplied with accompanying coordinated accessories, which include bags, tags, ribbons and bows, and crackers. Its range of stationery products includes pens, paper and filing, among others under its brand A star Stationery. Its b. original & b.inspired product range include notebooks, project books, study books, jotters and journals. Its Kids Create brand products include coloring, drawing and children's activity products. The Company's other brands include Tom Smith, Hoomark, Paper Craft, pepper pot, Giftmaker, The Gift Wrap Company and gifted, among others. The Company sells its products in over 100,000 stores in approximately 80 countries. I have been watching IGR for a few of months now and gradually getting to like what I see. Going back to the period January 2014 to April 2015 the shares traded at 77p roughly plus or minus 10p nothing terribly exciting as the company strove to find its way after a disastrous period coinciding with the banking crisis that saw the shares tumble by 95% over an eight month period. International greeting was historically a name familiar to me as I had bought and sold the shares over the period 2004/2005. Over recent tears the company had lost its way to some extent but during 2015 things have taken a turn for the better. In fact pre-the interim results announced on 2nd December 2015, the shares had had a phenomenal rise of about 140% in this financial year to date. Looking at the numbers I rather like what I see but of course after such a brilliant run you tend to ask yourself have I missed the boat or is there more to come? It was not that long ago when I asked myself the same question with Dart Group which had enjoyed a spectacular 12 months October 2012 to October 2013 in rising 200%; would I be foolish to invest? We I did invest in Dart at 225p and they have since given me a very enjoyable 160% rise. So for me, the message is a clear one, if I believe in the current overall quality and value of the business then I will certainly research it further as a potential purchase. I will not be put off because of recent exhilarating performance. I will of course weigh in with a little witchcraft in the form of a little technical analysis; maybe asking if there has been an advantageous pull back that may offer an attractive entry point. I am whittling on, apologies, so on getting back to IGR what do I like about the current business we see in December 2015? Well let’s start with cash flow; I have virtually no interest in any business that does not make profits and taking things a stage further, limited cautious interest in a business that cannot convert profits into decent cash-flow. What gives me comfort is really decent Free Cash Flow and with IGR they score well in that department since their recovery has been under way. Looking at some quality measures, the profit margin whilst nor being outstanding at the current 5%, has been gradually increasing over the three year period which included YTD. Over the same period the ROCE has been 9.1, 11.0, 13.0. The rise in the CROCI has been impressive for the full years 2013@ 4.5, 2014@ 9.9 & 2015 @ 14.7; that looks good to me and is appreciating each year. Oh, yes, best not forget the PE(f) @ 13.8. Over the years Prof Piotroski has been a good aid to me. Possibly the good Professor may have blinded me to some profitable investments but on the other hand I feel certain that the good professor has reduced my exposure to foolhardy risk. The Piotroski score for IGR is a very healthy 8 and again that gives me some comfort. The dividend is rather small currently at 1.5% but it is easily covered by conventional dividend cover and turning to the measure I prefer, massively covered by the FCF. It looks to me as if there will be opportunity for IGR to up its dividend fairly easily in the future. Additionally the current ratio is fine and the interest cover good and there is no pension deficit. Having a look at recent director speak, we have the outlook statement from the most recent interims released on 2/12/15: Overall trading activities are in line with expectations with a strong order book in place for the balance of FY2015/16 and already beginning to build for FY2016/17. Our focus on excellent and highly commercial design, customer service and innovation, continues to deliver margin and profit growth. We are on course to achieve targeted growth in underlying earnings per share and remain firmly focused on reducing leverage through converting profit into cash, whilst continuing to identify and implement fast pay-back investments and delivering ever improving shareholder returns. Paul Fineman Chief Executive Officer There is also a very interesting article in the Telegraph form Monday 21/12/15 which gives both historic and current pictures of the business; an extract below: So where next? “The US is the biggest opportunity for International Greetings,” says Fineman. Admittedly, it already has a big business there, enjoying a 12pc share of the gift packaging market and supplying retailers such as Walmart, Target and the Dollar stores. It also makes gift wrap from a factory in the southern US state of Georgia. But because it’s so large and fragmented - America’s regional players are as big as Britain’s national retail chains - there is still “an awful lot to go for”, says Fineman, both through organic growth and acquisition-led expansion. “We have a small share of a massive market,” Fineman explained. “We have a new US chief executive and are excited because we can see momentum there. For the first time in a number of years we are working in the business, rather than on the business.” What’s more, Christmas crackers are growing popular in the US, but not just for the Yuletide season. Through canny marketing, IGR has been selling crackers as festive ways to celebrate other occasions, such as baby showers and birthdays. Already this year, Costco in the US has sold out of IGR's crackers. Fireman says gift bags also offer huge growth potential. This year, the company will make just over 19 million bags - more than double last year's sales - and will offload 40 million globally. Fineman is also eyeing opportunities to make acquisitions that will launch IGR into a new segment of the bag world, such as shopping bags for stores. He also says there is scope to snap up companies that haven't been able to afford to upgrade their equipment, “We are far from perfect now and we can still improve. But when you have the right team in place you feel confident to make acquisitions," he said. “With the amount of cash we are generating we can invest in people, equipment and look at fast payback acquisitions and to grow the dividend, all while cutting debt." On the financial side, Fineman's target is to achieve double digit growth every year for the next three years across the company and to boost the net profit margin from 5pc to 8pc by 2018/19. He added: “We are in the best shape we’ve been in for a number of years, but I am in no way complacent." The link to the full telegraph article: https://uk.finance.yahoo.com/news/international-greetings-christmas-wrapped-050006760.html Now just to add a little more confidence I usually have a look at the Stock Rank numbers on Stockopedia and also the Sharelockholmes market ranks. We have Stockopedia Stock Rank of 98 and a Sharelockholmes market Rank of 3. Note: Sharelockholmes has 1 as its most attractive value so to compare with the Stockopedia Stock Rank we take the Sharelockholmes market Rank of 3 from 100 giving a value of 97. So in conclusion both ranking systems rate the stock very highly and again that’s very comforting. So finally applying a little of the TA witchcraft and noticing that the shares had stabilised following a few days of pull-back after the interims, I bought an initial holding in IGR on 22/12/15 at 174p and with the information available to me at present, intend to hold for a couple of years that is unless something horrible and unforeseen arises. As ever please note that the above is most definitely not investment advice but just my thought and reasoning process that I followed through before making this purchase. Also not all of my purchases turn out to be a successful investment. |

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed