|

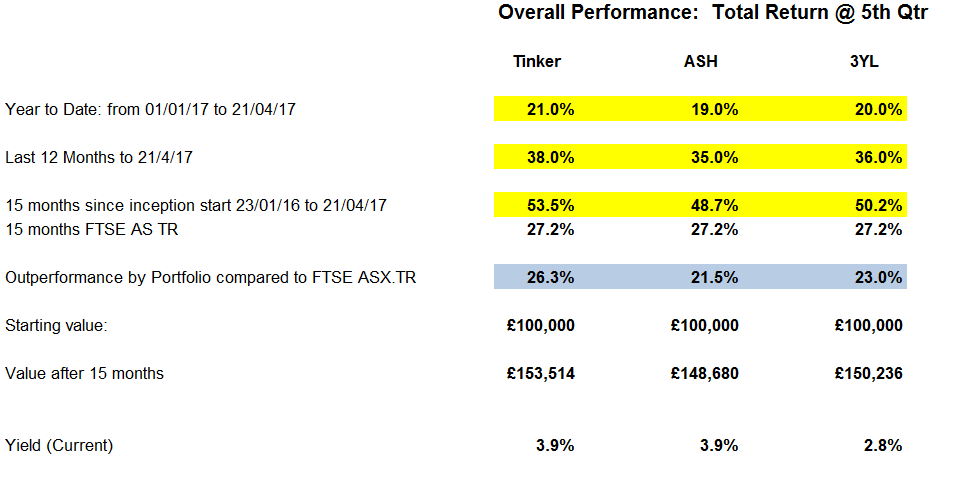

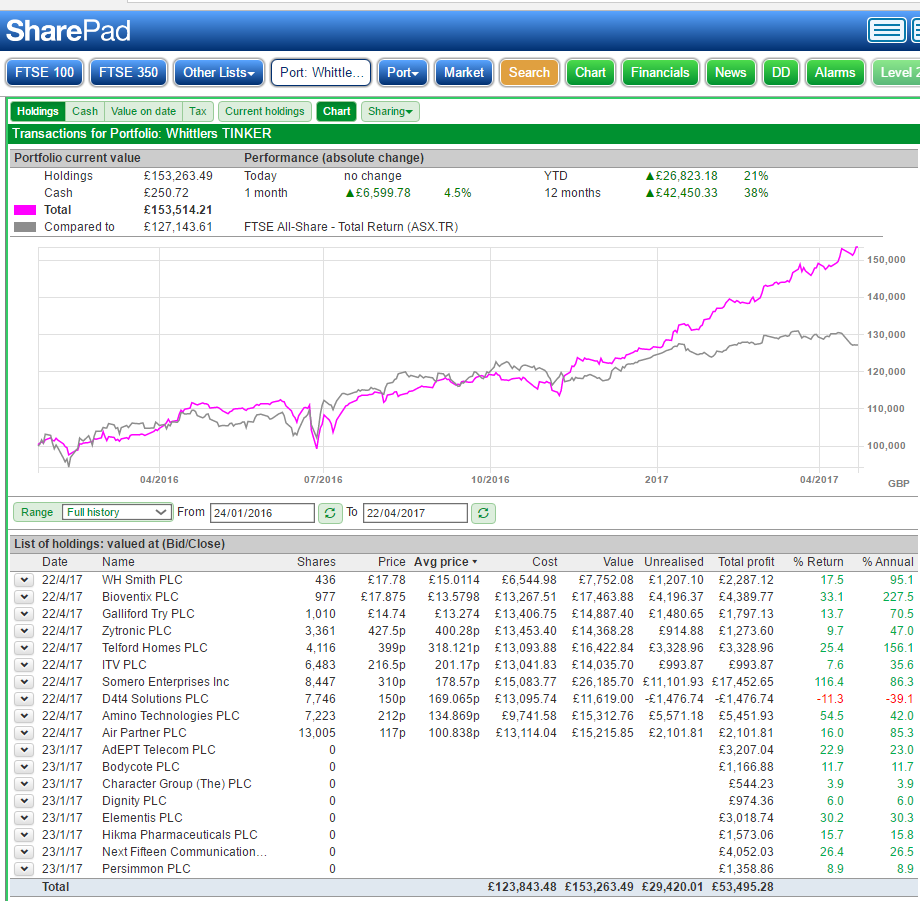

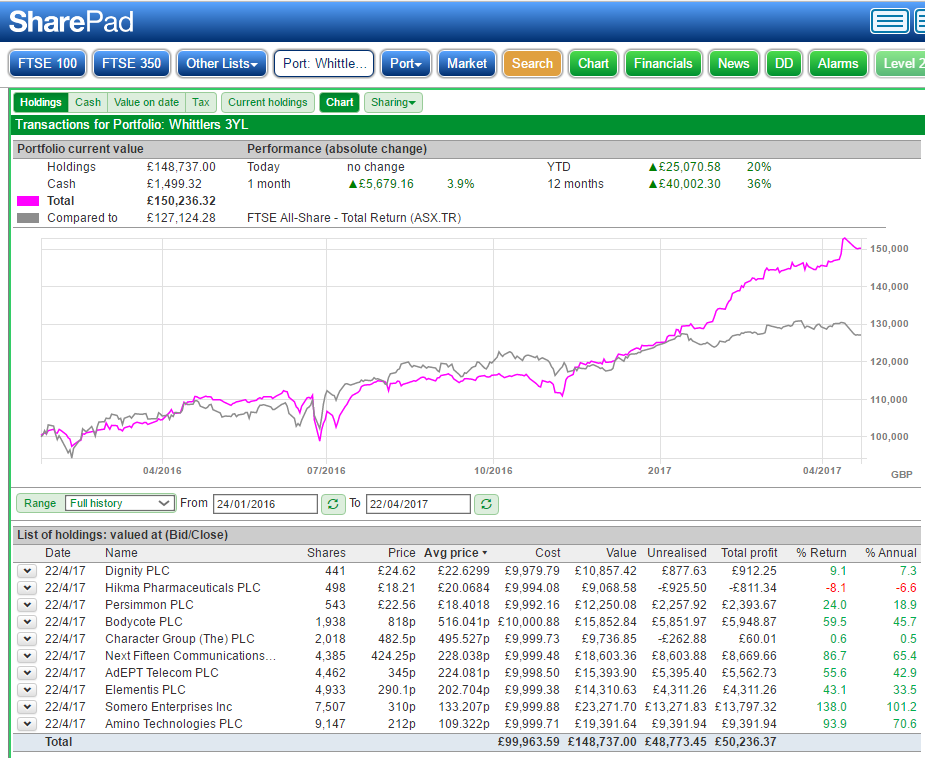

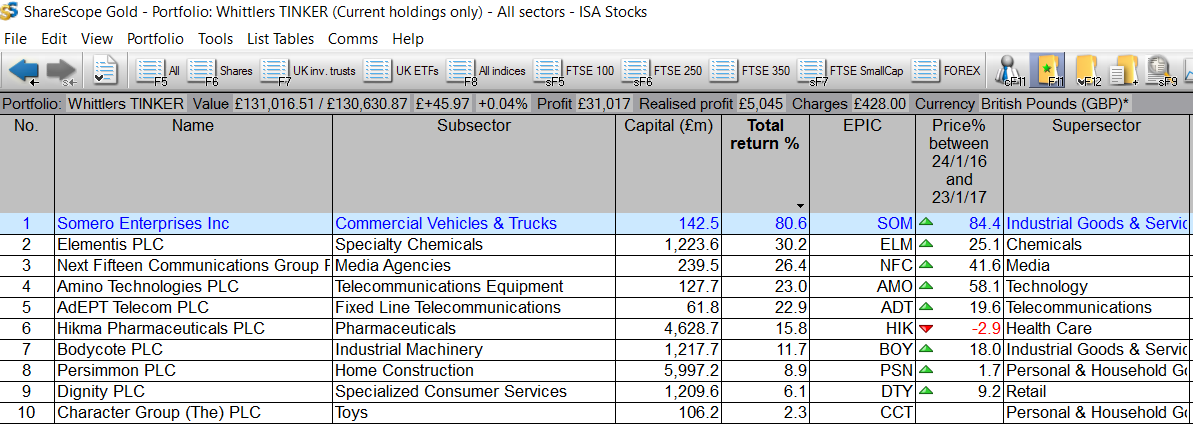

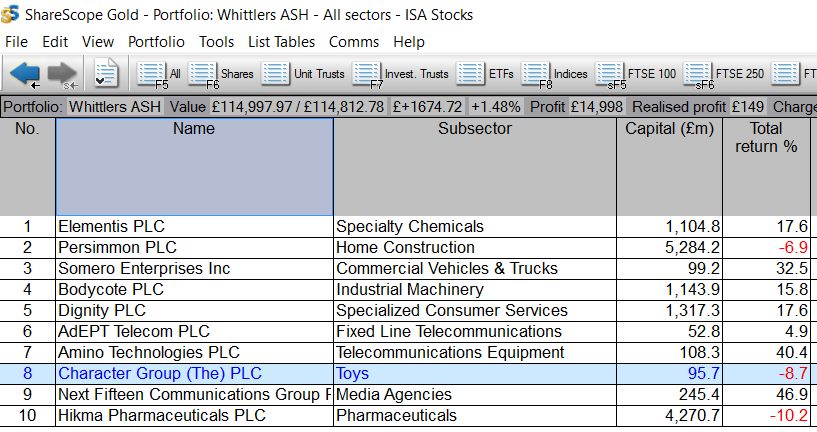

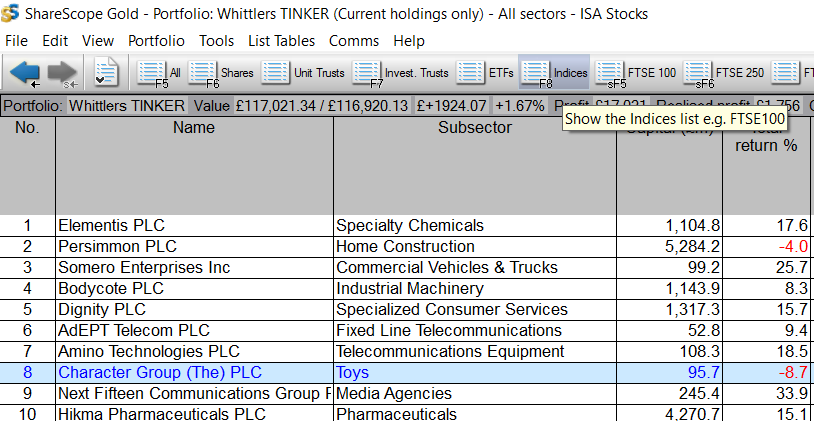

We have now reached the end of the fifth quarter of the Passive v Reactive Whittler portfolios so how are things going? The Tinker and ASH (annual sit on hands) had 8 stocks sold at the year-end review; see earlier blog of January 2017, to be replaced with 8 stocks identified from my investment universe. For clarity & to declare ownership: since the start of this Tinker series back in January 2016, a total of 18 stocks have been involved across the 3YL (leave it alone and don’t do anything for 3 years apart from reinvesting dividends), ASH & Tinker. All of these 18 stocks form or have formed part of my “best 10” portfolio and I still hold the majority of these 18 stocks and they form the backbone of my portfolio. The quarterly performance and dealing history, warts and all, is openly & honestly published within this Stockwhittler site. By way of a reminder, the ten original stocks common to the three portfolios and the eight replacement stocks identified in January 2017, come via my routine free cash flow+ returns on capital screen i.e. they all exist within my whittled down universe from which I make the majority of my share purchases. This universe shrinks the 2000 or so LSE shares down to about 40-50 for further really detailed appraisal: interim & final reports, all RNS news and particularly outlook statements. Within the rebalanced Tinker once the eight new stocks had been added following the sale of eight original stocks on 23/24-January 2017: In the Tinker and ASH out went Adept Telecom, Bodycote, Character Group, Dignity, Elementis, Hikma, Next Fifteen Communications & Persimmon. They were replaced with: Air Partner, Bioventix, D4t4, Galliford Try, ITV, Telford Homes, WH Smith & Zytronic. In Tinker portfolio terms I say out and replaced however, in terms of my actual investments, I continue to hold and indeed top up the majority of the 18 stocks discussed in this series to date. As mentioned previously in this series I am a great believer in the security of investing in a basket of stocks. Within that basket, you may well have a few outstanding stocks whose overall impact on the portfolio performance is somewhat diluted by other less well-performing stocks but conversely, a basket approach reduces risk when a couple of stocks are not heading in the desired direction. Now, of course, the rules I apply to this Whittler/Tinker exercise limit the ownership to my 10 best ideas as identified in January of a particular year and only in the Tinker can I manipulate the % on any of the 10 stocks in that portfolio in a 12 months period. Turning to the general concept of one’s entire portfolio i.e. stepping out of this 10 stock scenario for a moment is that many investors struggle with is the size of that basket and I usually run with a basket of around 30 stocks. You could argue that 30 stocks are a touch high and difficult to manage but personally using the systems that I operate, it’s a doddle. Yet I do feel that my overall performance which I must say I am generally happy with, could up a notch or two if I had the conviction to simply invest in my best 20 or even 10 ideas rather than the 30ish I usually manage. Having said that, I do ruthlessly and without emotion weed out stocks where it seems I did not get it right i.e. ones where the fundamentals for example or the story/original reason to buy no longer appears to be sound. Anyway, enough of this waffling on about the number of stocks within one’s portfolio, let’s see how the three ways of managing a portfolio discussed in this series, Tinker, ASH, 3YL, have performed by quarter 5 that’s 15 months since inception  I have also included tables from the excellent SharePad showing Tinker and 3YL: I reckon I must be one of Sharescope’s original customers many years ago and now am also hugely appreciative of the SharePad version   The performance of the 18 stocks across the Tinker, ASH & 3YL has been really very good since this series started with 10 stocks at £10,000 each back in January 2016. The Tinker is slightly ahead at 53.5% gain over this five quarter or 15 month period but really there is nothing significant to mark one portfolio out from another as the performance of all three strategies has been really very good. Thankfully the shares discussed here have been the backbone of the total portfolio I run and as such have contributed handsomely to my annual performance and I confess to being a happy investor.

Maybe we will see a more significant difference in performance within the three portfolios within the coming months but to my mind, all performance has been extremely good and too close to draw any significant conclusion as to portfolio management approach other than to again see that quality counts in investments. The comparisons with the returns that would have been made had we invested in the FTSE all share total return, FTSE ASX.TR are given in the tables SharePad below and as you can see the FTSE ASX.TR has been very significantly left behind by Tinker, ASH & 3YL but who knows what the future mat bring? After all the next profits “Oh no it’s a profits warning” or delightful “exceed market expectations” RNS may just be around the corner. Trading within the Tinker since 21/01/17 i.e. since rebalancing in January this year: well only one trade has taken place and that was on 3rd march 2017 when ½ of the WH Smith holding was sold and reinvested in that lovely high-quality stock Somero: I have to confess that I have held an appreciable quantity of SOM in my ISA since 2013. Not falling in love with a particular stock, but an appreciation of quality and backing a winner. As ever, anything produced here should not be taken as investment advice but rather a sharing of the whittling methods of a fellow investor trying to openly and honestly communicate the quest for reasonable returns from the stock market. Once again the rules of the exercise are reproduced below. Happy Investing! Appendix: The boring stuff! Reminder Of The exercise Rules. The three portfolios will be firstly a buy and hold for three years, ploughing on regardless through economic conditions, profit warning and any other news either good or bad. I will call this the three-year life portfolio (3YL). The only time a change to the portfolio will be permitted is if a business is de-listed for any reason: the funds liberated would then be discretionally invested between the remaining stocks in the portfolio. The second portfolio will start out with exactly the same holdings as the 3YL but each January the same cash flow screens/returns on assets screen will be run and a revised set of ten stocks nominated. This revised set of stocks will have the proceeds of the sale of the previous years stocks equally divided between them i.e after one year we have £110k of funds then a purchase of £11k will be made for each of the ten stocks. I will call this the annual sit on your hands portfolio (ASH). The third portfolio will again start the same as the 3YL & ASH portfolios but I will alter the percentage invested in each position within the portfolio in reaction to RNS announcements from the companies, economic conditions or any other reason that seem valid for altering, reducing or increasing a position. I will call this portfolio the managed annual tinker portfolio or simply the TINKER. All 10 stocks will remain within the portfolio throughout the year although the investment in each stock may vary. For example, one stock, let’s say Hattersville Dream Co. may issue a particularly bullish RNS “results will be appreciably ahead of market expectations”. The Tinker may sell down one or more of the other holdings to invest more in Hattersville but still retain a position, although not equal positions, in the same 10 stocks that we started within January each year. In January 2017, 2018 & 2019 this portfolio would be treated in the exact same way as the ASH and funds equally balanced across the each of the ten stocks starting that year. The common rules for all three portfolios: • Start January 2016 with the same 10 stocks each having £10k invested. • The basis of stock selection will be common to all purchases and in line with my usual investment principals based on strong cash flow, good returns on capital and sound financial health. • Dividends will be reinvested. • All three portfolios will be continuously fully invested in the relevant 10 shares. • The 3YL will not have any actions taken apart from dividend reinvestment and be left alone to prosper or otherwise over the three year period. • The ASH & Tinker will commence each January as fully invested in 10 stocks. However, the Tinker will have the discretion to rebalance the allocation of funds to one or more of the 10 stocks in the portfolio. • Transaction charges will be £5 per transaction with stamp duty deducted as relevant. • Dealing are now applied to the reinvestment of dividends as per iWEB costs.

0 Comments

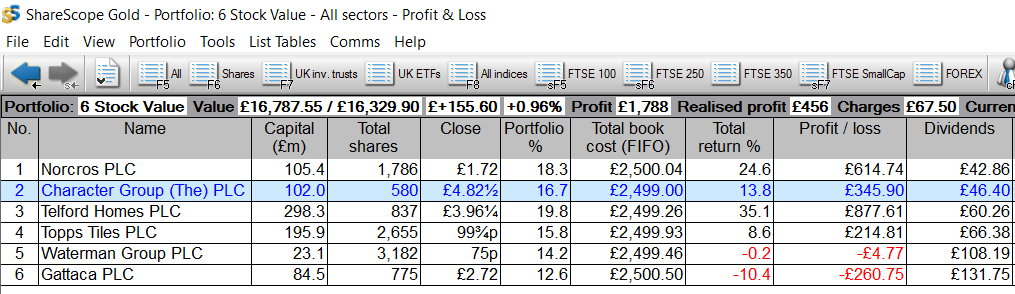

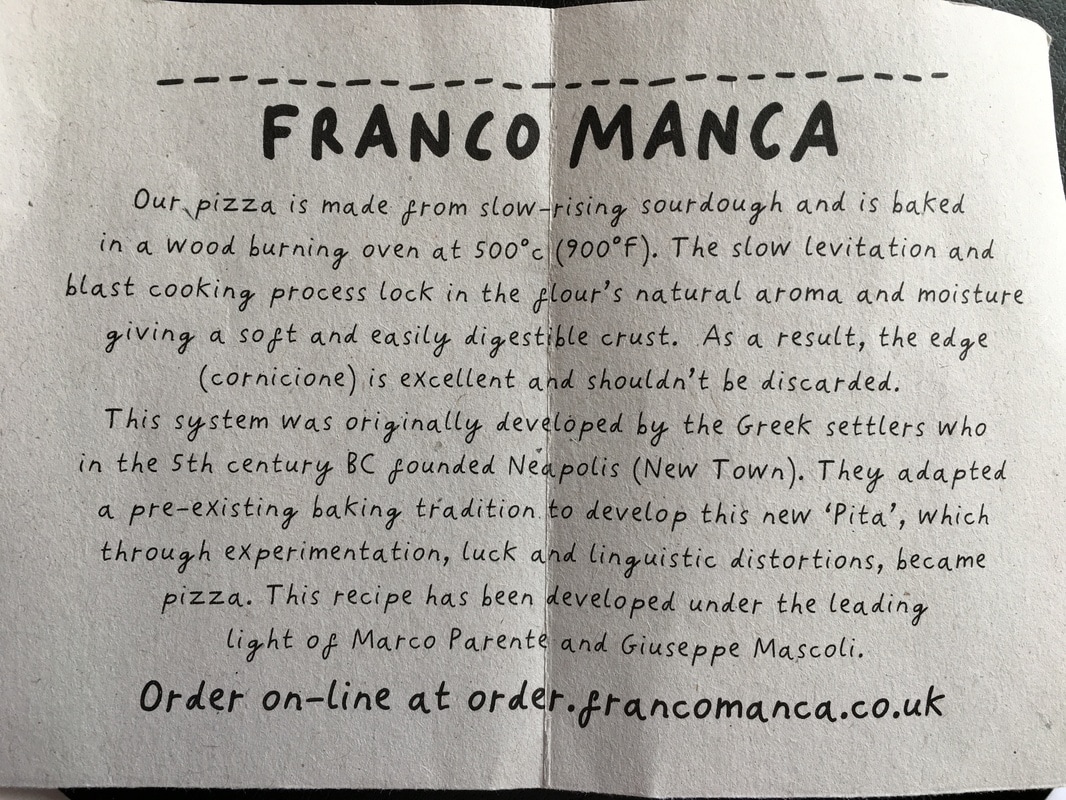

Just as a refresher; this article is the third and last in the brief series “Is The Stock Market For Matt”? Now my relative Matt, not his real name but as I said in part 1, I protect his anonymity buy calling him Matt simply because the silly so and so keeps a fair sized chunk of spare cash around the house under the mattress if you like; so he is Matt Tress. Anyway Matt has the usual bank accounts etc. but with interest rates as they are he feels why bother just leaving money in the bank as the current rate of return although risk free, is just so very poor. So six months back I sat down with Matt and devised a phantom portfolio where his spare £15000 would be invested in six value stocks paying tolerable to good dividends and in my judgement having an acceptable risk as the stocks are all lowly rated being a touch unloved but by and large sound businesses. Today six months after the start of this exercise, Matt still has his £15000 which has of course not gone anywhere apart from a little nibbling at the edges by that annoying little mouse called inflation. Let’s have a look at the performance of that £15000 had it been invested in equal £2500 amounts in the companies in the phantom portfolio whose dealings were sown in part 1 & part 2. Note I do need to say at this stage that at the time of construction of Matt’s phantom portfolio I held positions in all six companies; so walking the talk if you like such American expressions. The table below gives the progress Matt would have made over the six month period and it shows a total return of about 12% equal to an annual return of 24% and that includes £456 in dividends or as a %, 3% over the six month period. Had Matt invested that money in a bank he would have had a top end return of well under £100 over that six months. Had he invested in the FTSE All Share, which has performed quite well, he would have made around 4.5%; still fairly attractive. How does Matt feel about that tempting but definitely not guaranteed return? Well, to be honest he is impressed and slightly kicking himself for not taking the plunge but don’t kick yourself Matt, that’s life.  How does this compare to the FTSE AS Total return:  Now as I don’t give advice on share purchases, can you imagine the phone calls from Matt late at night if things go wrong, it’s really up to Matt to decide how to enter the world of stock market investing. He does not yet have what he feels is the expertise to select individual shares and certainly not the time to monitor RNS progress for companies yet he really wants to make a start. Matt than asks about these things called unit trusts and investment trusts and comments that I benchmark my portfolio performance against three of these, Fundsmith, Marlborough Special Situations and Henderson Smaller Companies Investment Trust. After a discussion about track record, the managers involved and fees, Matt decides that this is for him and will now invest £5000 in each of these three with a view to the long term and happily tells me that he will only look at progress monthly. Now with funds and investment trusts that is one bit of advice I was happy to give Matt as there is simply no point in looking more frequently and getting the negative or positive feeling as the funds move with each day. I can almost guarantee that the negative feeling of loss will outweigh the exhilaration of gain so why give yourself that pain? So in the end I feel quite comforted that Matt has decided to try and make his cash work for him and I am of the opinion that as long as he takes a long term view, say 5-10 years, he will do well. Strange you know, over the years I have made some of my best returns from attractive companies by simply sitting on my hand and doing little else but reinvesting the dividends. Happy investing Matt! As an investor it’s always nice to try the products from a company one invests in. The trouble is that I have little use in my daily life for the laser flat concrete from Somero, sheep monoclonal antibodies from Bioventix and certainly am not ready to personally sample the final drive services of Dignity. So in truth my chances to sample the quality of the service & products offered by the companies I invest in is down to the likes of Dart Group, WH Smith and a recent initial purchase in Fulham Shore who run the Franco Manca & Real Greek restaurants.  Now I should say that Fulham Shore is a fairly unlikely investment for me to even take a small initial holding in and that’s simply for the following reasons: The less good bits:

The bits that interest me:

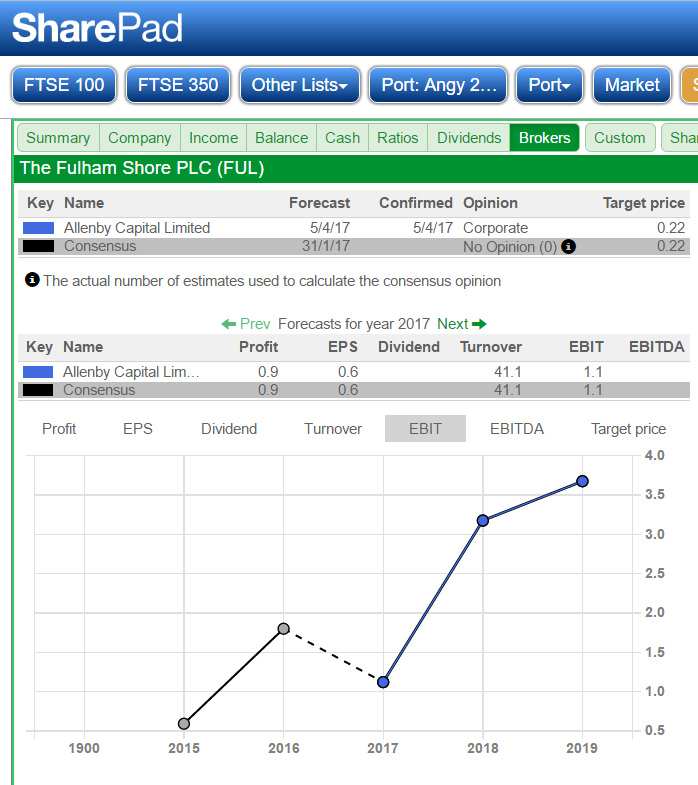

Now pizza itself is not my number one choice of food as I find the majority of high street offerings simply far too heavy with stodgy bases and well overdosed with tomato base. I do in fact make my own Australian pizza at home using a pizza stone. Why Australian? Well although I am a pretty decent in the kitchen, the round pizza shape escapes my skills and every pizza that sits on the stone resembles the map of Australia, sometimes even Tasmania can be seen. So after some late 2016 research, I took a small position in Fulham Shore in January this year fully appreciating the downside risk. As it happens, on Saturday my Hatters travels took me to London, we were playing Barnet, giving me a perfect opportunity to have lunch at the Tottenham Court Road Franco Manca. Yes, I know it’s nowhere near Barnet but who cares when you have a multi-zone travel card for the day: terrific value. I was impressed with my visit I have to say. The service was very good, a free jug of tap water in a recycled wine bottle delivered to your table on arrival. The drinks reasonably priced and the sourdough pizza one of the most impressive I have had; you could appreciate the taste of the fresh ingredients so rapidly cooked via their blast cooking process. Also, the staff were hugely impressive and appeared genuinely attentive. All in all a thoroughly enjoyable eating experience at very reasonable cost in the centre of London: two plate-sized pizzas, a glass of red and a glass of white with a bill of £25; can’t be bad. The broker view: data from SharePad:   Well, where do we go from here? In truth, it’s only a tiny % of my portfolio at well under 0.5% but it’s something I will keep an eye on and maybe add to as time progresses remembering that it’s a crowded marketplace and roll outs can by their nature become self-limiting in terms of growth.

Happy eating & happy investing. Investing in shares is not a love affair and to my mind, an investor has to evaluate not only when to make the purchase having completed your thorough research but also without emotion decide when it is time to leave. With some shares, this holding time can be very lengthy e.g. Somero, Bioventix, Dart Group which met my buy criteria in 2013,14 and continue to look attractive investments.

As I have mentioned in previous blogs my approach is to create a mini-universe of shares that qualify for consideration by virtue of attractive metrics such as free cash flow, returns on capital (CROIC and ROCE), increasing turnover, increasing profits etc. I should say that I also spend a fair amount of time pondering over what could go wrong with a business before I feel comfortable to make an investment. I don’t invest in anything that could be described as a blue sky stock: each company I invest in has to be a proven profitable business with real and not imaginary profits. As ever, I find myself building into winning positions as confidence in them gains: not the easiest of things for an investor to do “why should I pay £2.31 for something I paid £1.97 for a couple of months ago? My investments are for the bulk part held within a tax-free environment and I have been utilising PEPs and subsequently ISAs going back into the mid-1990’s. One thing I am certain about with investing, well at least with my outlook on life, is that in the early days of one’s investment journey you make many mistakes and you also have the odd wonderful year. In my experience the rates of return on small value portfolios, say under £100k, where you may have a greater appetite for risk as the potential loss is possibly not life changing in monetary terms, decreases markedly as your pot of dosh increases. The bigger the pot, the more risk averse one becomes. In terms of overall returns, your volatility tends to even out as you become comfortable with your investment approach, nurture the winners and ruthlessly jettison the stocks that don’t move in the desired direction. In general terms, once I “found myself” as an investor, I estimate that over a period of many years averaging out the good and bad years should with discipline yield in the range of 12-16% PA. Investment returns are not governed by magic tricks, they are dictated by a combination of individual company performance and the overall health of the market: fortunately the markets in 2016/17 were in pretty good health. In terms of performance measurement, I tend to go against the flow whereas most investors assess on a calendar year, I measure performance on a tax year. It seems sensible to me as that coincides with topping up the ISA pot and balancing CGT. The year 2016/17 was an unusual year with the FTSE all share total return taking a significant tumble at the end of June after the unexpected Brexit referendum result. We also had the unexpected result of the USA presidential election where a man who would need an annual review due to his age to retain employment in the UK took the most powerful job on the planet. Both results were unexpected and certainly not predicted by the well-paid commentators; who needs experts! So, onto the overall performance of the Whittler portfolio for the financial year 2016/17; the performance against my usual comparators are given below: Stock Whittler portfolio: +28.4% FTSE All Share TR: +23.8% Fundsmith Equity T Ac +24.4% Marlborough Spc Sit: +22.0% Henderson Sm Co’s IT +19.1% Overall the year 2016/17 was a good year to be investing even if on the end of June, post-referendum, it did not look that way. However, one can be easily misled into thinking that 2016/17 was a vintage year overall as it was Oil & Gas, Commodities, Miners & Banks that did all of the really hard work; these sectors between then averaged a gain of 77%. If you strip those sectors out then the gain for the FTSE all share fell to a more modest 13.6%. Now I rarely invest in any holes in the ground and after the financial crisis, I won’t touch banks with a bargepole so overall I am very happy indeed with a return of just over 28% from what I call proper companies that don’t live in the more speculative sectors. Now although I am delighted with that performance, I am ever mindful that the markets will at some time take a dip and at some time we will enter a bear market. I am also very mindful that the next profits warning for a stock within my portfolio may be just around the corner. The fact is that these events happen and the important thing is how you react to them. Note as I write the example portfolio I blog about the Tinker which is roughly my best 10 ideas taken as a modest initial investment of £100k is up 39.0% for the financial year 2016/17. Incidentally I will write up the 5th quarter’s performance at the end of April. I actually wonder if one day I will be brave enough to eventually just run with by best ideas in a concentrated portfolio of 10 stocks rather than the roughly 30 that I perpetually run with; I am sure that would be an even more productive way forward. Happy investing Well following on from the 12-month review of performance the three portfolios, 3YL, ASH & Tinker the revisions to the ASH and Tinker have been made. Remember that the 3YL remains totally unaltered in composition over the three years of the comparison and will continue to hold it’s original investments in:-

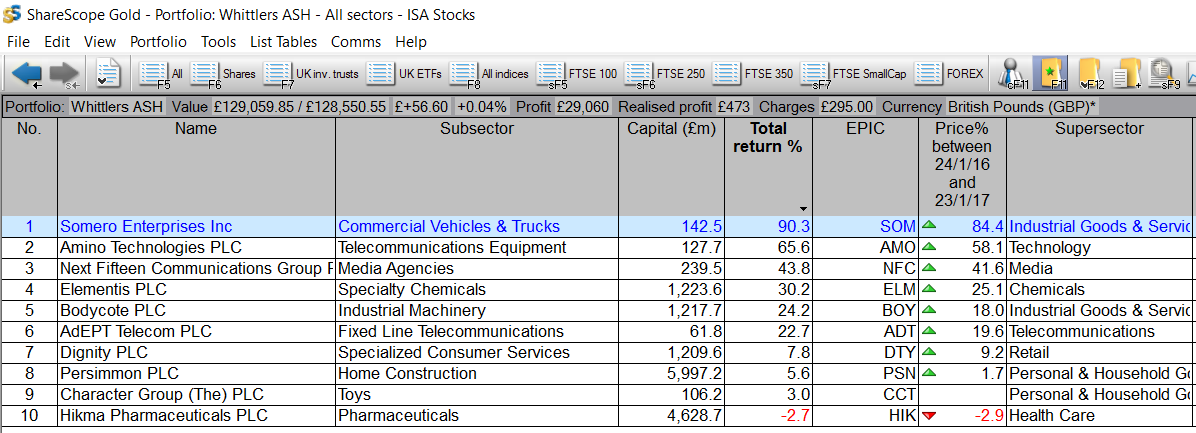

AdEPT Telecom, Amino Technologies, Bodycote, Character, Dignity, Elementis, Hikma Pharmaceuticals, Next Fifteen Communications, Persimmon and Somero Enterprises. This portfolio followed the investment rules of selection of what I assess as quality companies having good returns on capital employed and good free cash flow: as ever, I am not really looking for fudged or manipulated earnings per share. I like companies that are mature enough to pay dividends and in terms of sustainability of that dividend I am fare more interested in FCF dividend cover rather than conventional dividend cover. As discussed in the first year review, the 3YL & Tinker converted £100k to £129k in 12 months; a 29% return and the Tinker converted the £100k into £131k; a 31% return. The proceeds from the first year of the ASH (annual sit on hands) £129k will be reinvested equally in the following 10 companies as will the proceeds of the Tinker £131k. The 3YL will continue with the original shares simply left alone to do their stuff and the ASH will chug along with its new allocation of shares and remain untouched for the next 12 months. The Tinker of course will of course contain the same collection of shares as the ASH but l freely shift the capital allocation between the 10 companies as I react to company news and prospects. In reality I don’t make vast number of changes in a year and avoid market noise such as brokers views or tips preferring to make my decisions on what is actually happening within a business. For example if one of my companies puts out a statement such as “trading ahead of expectations”, I may well be tempted to sell a part position in another stock and reallocate to the one showing improved prospects/momentum. So, to the meat of this article, the revisions to the ASH & Tinker for the next 12 months: From the stocks in year 1, I have retained two of the very successful AIM stocks: Amino Technologies: AIM Listed: Market Cap: £136m: Yield 3.5%: FCF Div Cover 1.9: ROCE: 15.2%: CROCI: 16.1% & 3 year Average CROCI: 13.4%. Somero Enterprises: AIM Listed: Market Cap: £141m: Yield 3.6%: FCF Div Cover 2.6: ROCE: 50.2%: CROCI: 29.6% & 3 year Average CROCI: 26.6%. The new stocks to enter both the ASH and Tinker portfolios are: Air Partner: AIM listed: Market Cap £56m: Yield 4.8%: FCF Div Cover 2.2: ROCE: 26.1%: CROCI: 35.9% & 3 year Average CROCI: 50.4% (81.8, 47.0, 22.4) Bioventix: AIM listed: Market Cap £78m: Yield 3.3%: FCF Div Cover 1.5: ROCE: 56.7%: CROCI: 43.2% & 3 year Average CROCI: 34.4%. D4t4: AIM listed: Market Cap £64m: Yield 1.4%: FCF Div Cover 7.7: ROCE: 21.4%: CROCI: 39.0% & 3 year Average CROCI: 3.3%.(3.2, 10.5, -2.7) Galliford Try: FTSE250: Market Cap £1190m: Yield 6.4%: FCF Div Cover 1.1: ROCE: 15.3%: CROCI: 8.7% & 3 year Average CROCI: 4.2%. ITV: FTSE100: Market Cap £8296m: Yield 3.5%: FCF Div Cover 1.8: ROCE: 40.2%: CROCI: 23.4% & 3 year Average CROCI: 22.1%. Telford Homes: AIM listed: Market Cap £260m: Yield 4.4%: FCF Div Cover 1.4: ROCE: 15.6%: CROCI: 7.9% & 3 year Average CROCI: -0.5% (19, 6.7, -27.2). WH Smith: FTSE250: Market Cap £1840m: Yield 2.9%: FCF Div Cover 1.8: ROCE: 63.7%: CROCI: 45.3% & 3 year Average CROCI: 50.8% (45.9, 48.0, 58.4) Zytronic: AIM Listed; Market Cap £58.5m: Yield 4.3%: FCF Div Cover 2.1: ROCE: 18.0%: CROCI: 20.3% & 3 year Average CROCI: 16.2%. Points to note: Four of the stocks have market capitalisations in the range of £50m to £100m, three stocks in the range £130m-£270m & three fairly big boys including two FTSE250 & one FTSE100 company. The average yield for the portfolio is around 3.5% and is well covered by FCF which for me adds a little comfort: all dividends will be of course reinvested. Although I don’t use the Stock Ranks system in my share selection process, I do once selected go and have a look at what SR values have been allocated to my chosen stocks; just adds a little to ones confidence I suppose. For the ten stocks in the revised portfolio, the average SR is 85. Also a quick check of the Piotroski scores for each company gives an average Piotroski score of 6. The first year of the Tinker was highly successful in giving a total return of 31% and I hope this selection and rebalancing to given equal weights of the respective portfolio totals to each of the 10 stocks in the ASH and Tinker will be somewhere near as successful. I will publish as a minimum, quarterly updates of portfolio progress. Ownership: I own investments in all of the ten companies listed within the revised ASH & Tinker as well as positions in most of the portfolio before it’s 2017 rebalancing/refreshing. The stocks have all been identified via my screening methods mentioned previously within this blog where I am looking for companies that make very good returns on capital invested, have good FCF and are increasing profitable turnover. As ever, nothing written here is investment advice but merely a blog of my investment process to hopefully make a reasonable return from the UK stock market. I hope you find such articles possibly informative and entertaining and should you have any comments or questions than contact me and I will be happy to respond. Happy investing. Well, we have now reached the end of the fourth quarter and hence the end of year 1 of the Passive v Reactive Whittler portfolios so it’s now time for a detailed review to see how my meddling has done compared to Mr Cool who simply sits on his hands and lets time do the work. Just by way of a reminder, the ten stocks common to the three portfolios were identified via my routine free cash flow+ returns on capital screen i.e. they all exist within my whittled down universe from which I make the majority of my share purchases. At the time of entering the fourth quarter, I hold positions in seven of the ten companies: SOM, CCT, DTY, AMO, HIK, NFC & PSN. So that’s a financial interest in 70% of the stocks within this exercise and I am very grateful for the positive impact that the likes of SOM, AMO & NFC have brought to my ISA over the last 12 months. I have long held the belief that investing via a basket of stocks approach is far preferable than “all your investment in one or two companies” approach; simply balances and reduces associated risks. To my view if you invest in a stock, there is always a risk that the stock may depreciate in value for one reason or another, maybe the dreaded profits warning or just simply falling out of favour. It certainly would be nice to pick winners with every share purchased but in reality that is just not going to happen; maybe as investors, we are right 5 or 6 times out of 10, hence the importance to my mind, of investing via a basket of stocks.  The basket of stocks performed admirably during the 12 months period and with dividends, the static version yielded a profit of 29% with dividends reinvested. In the Tinker version, eleven trades were made within the same population of stocks where I reacted to positive company trading updates, outlook statements and in one case, PSN, a Brexit opportunity. The only trade I regret was actually reacting to a touch of market noise in the form of a broker downgrade and decreasing my holding in Bodycote: strange one that as I always preach about avoiding market noise.  Overall this medalling within the Tinker boosted the annual performance to 31% compared to the 29% of the passive investment again with dividends reinvested. I would not say that extra 2% was massively significant and in reality was achieved by reallocating some investment from the average performers to the strong performers. My risk aversion probably cost the Tinker a couple of more percentage points of potential outperformance had I not dithered and taken a third extra allocation in the best performing stock, Somero which rose by 84% over the 12 month period. Other notable performers were Amino 58%, Next Fifteen Com 41%, Elementis 25%, AdEPT 20% & Bodycote 18%. Only one stock ended the year lower than it started, Hikma Pharma (2.5%). Interestingly HIK shows a positive total return in the Tinker as I sold the stock immediately following a mild profits warning and retained some profit from its previous good run. As can often happen even with a mild profits warning, the price can drift south for quite a few weeks.

How does this compare to my usual benchmark indices the FTSE All Share Total Return (ASX), well reasonably well as although this particular index had an excellent year at +24.2% over the identical 12 month period the passive outperformed by a few percent at 29% and the Tinker even more satisfying at 31% total return. So after a very pleasing initial 12 months of the Tinker, it’s now time for the annual review of both the Tinker and the ASH. Remember the rules, of the three-year exercise are that the 3YL is simply the original 10 hopefully quality stocks selected and just left to their own devices for three years. The ASH (annual sit on hands) which had the same first year % composition throughout the initial 12 months as the 3YL and the Tinker will now have the current 10 stocks reappraised; some will be held and some will undoubtedly be replaced by current more attractive propositions to yield a set of 10 stocks for investment over the next 12 month period. With both the ASH and the Tinker the total value of the portfolio will be equally rebalanced between the 10 selected stocks. The ASH will then, of course, remain unchanged in composition for the 12 months period whilst the funds in the Tinker may be reallocated between the 10 stocks as I react to positive or negative news and hopefully take opportunities whilst at the same time actively managing risk. This means that with the Tinker, £13.1k less dealing charges and stamp duty, will be invested in the 10 stocks I run with for the next 12 months and with the ASH, £12.9k per stock again less dealing charges and stamp duty. The 3YL will of course just be left alone to hopefully carry on it’s good “sleeping” work. The 10 stocks that compose the revised ASH & Tinker will be discussed in a blog introducing year two in a few days time. As before the stocks involved have come through my own rigorous but not always right, screening processes based on good returns of capital employed, attractive free cash flow, what I perceive to be reasonable growth prospects/prosperity (this may not always agree with the widely held opinion of Mr Market) and hopefully not too much exposure to unnecessary risk. As ever, anything produced here should not be taken as investment advice but rather a sharing of the whittling methods of a fellow investor trying to openly and honestly communicate the quest for reasonable returns from the stock market. Once again the rules of the exercise are reproduced below. . Reminder Of The exercise Rules. The three portfolios will be firstly a buy and hold for three years, ploughing on regardless through economic conditions, profit warning and any other news either good or bad. I will call this the three-year life portfolio (3YL). The only time a change to the portfolio will be permitted is if a business is de-listed for any reason: the funds liberated would then be discretionally invested between the remaining stocks in the portfolio. The second portfolio will start out with exactly the same holdings as the 3YL but each January the same cash flow screens/returns on assets screen will be run and a revised set of ten stocks nominated. This revised set of stocks will have the proceeds of the sale of the previous years stocks equally divided between them i.e after one year we have £110k of funds then a purchase of £11k will be made for each of the ten stocks. I will call this the annual sit on your hands portfolio (ASH). The third portfolio will again start the same as the 3YL & ASH portfolios but I will alter the percentage invested in each position within the portfolio in reaction to RNS announcements from the companies, economic conditions or any other reason that seem valid for altering, reducing or increasing a position. I will call this portfolio the managed annual tinker portfolio or simply the TINKER. All 10 stocks will remain within the portfolio throughout the year although the investment in each stock may vary. For example, one stock, let’s say Hattersville Dream Co. may issue a particularly bullish RNS “results will be appreciably ahead of market expectations”. The Tinker may sell down one or more of the other holdings to invest more in Hattersville but still retain a position, although not equal positions, in the same 10 stocks that we started within January each year. In January 2017, 2018 & 2019 this portfolio would be treated in the exact same way as the ASH and funds equally balanced across the each of the ten stocks starting that year. The common rules for all three portfolios:

A brief update on my dealings within the Tinker portfolio; the last quarterly update was given on 1st November 2016. Firstly a few points regarding the portfolio exercise:

I hold or have held during the period of this folio 80% of the stocks discussed. When I first but a stock I usually allocate at least a 15% stop loss, could be as much as 20% for a small market cap: I like to give the stock time to breathe as it were. As the stock appreciated in value, I move to a trailing stop loss which is somewhat tighter at 10-12%. Four Trades On 15th December 2016: A rather successful stock, Next Fifteen Communications, had risen nicely but over the last couple of weeks had started to drift back and breached the 12% trailing stop loss. This prompted me to sell just over 75% of the holding for a 36% profit and releasing £12000 to be reinvested in other constituents of the Tinker portfolio. The reinvestments of £4000 per stock, less fees, were made into each of the following stocks currently held within the portfolio:

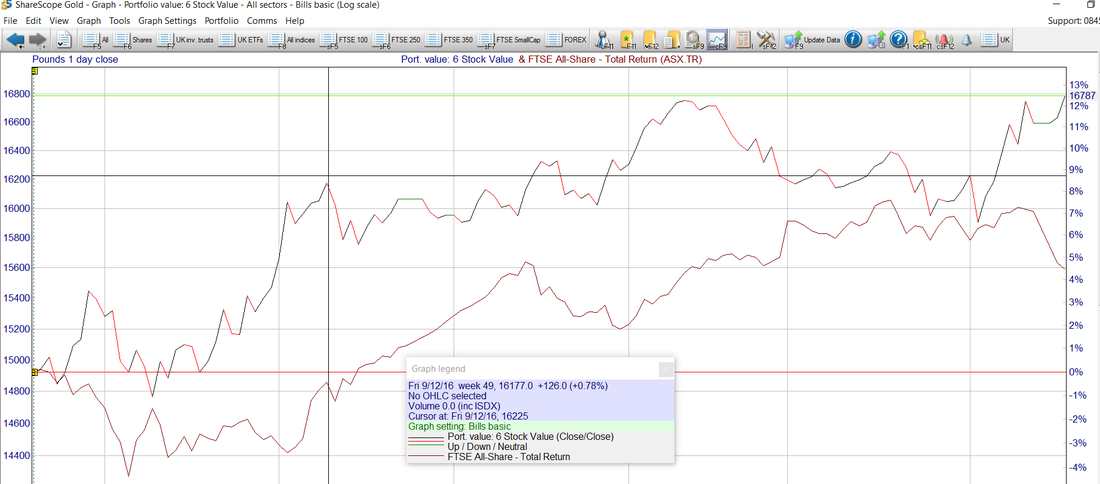

Current Tinker Portfolio Performance: Since the start of the Tinker portfolio on 25th January 2016, it has increased in value from £100,000 to £123,500 i.e an increase of 23.5% compared to the FTSE All Share Total Return (ASX.TR) of 19.0%: who back in January or indeed I after Brexit would have thought that the FTSE ASX.TR would have performed so well? Decreasing or Increasing Positions: I really only sell when I see a pre-planned reason to do so as I totally ignore market noise. At least that’s what I tell myself! Remembering that the portfolio exercise rules are that no new stocks may be introduced during a 12 month period starting 27/1/16, the pre-planned strategy for selling is:

The strategy for adding to positions within the portfolio is simply based on really encouraging news released by the company. That could be “profits materially ahead of market expectations” or something happening with the business that is claimed to be transformational. The next planned update of the portfolio in at the end of January 2017 and for the revisions, I am currently working through my usual cash flow/returns on capital screens. Happy investing. Just a quick update on trades in November and December within my portfolio:

The following have been sold or position reduced: BOO: 50% sale of position bought at 27p: maybe just getting a touch lofty and occupying too higher a percentage of the dealing account and subject to CGT. TRAKM8: their results on 28th November were in my view a bit of a disaster and to add zero joy, a profits warning. In 95% of the cases where I hold a stock that suffers a profits warning, I sell as soon as I can on that morning. Thankfully I only had a tiny initial position of 1000 shares as I felt slightly uncomfortable opex costs being partly capitalised. I sold my holding at 141p for a niggly little loss of £700; apart from “I told myself so”. I also feel that TRAKM8 management could have been shall we say, been a touch more dynamic in keeping the market informed. Once I lose trust in management, that’s it, I am out and unlikely to return. Interestingly I got out early at 141p on the day of the RNS, 28/11/16, the price has kept dropping and at the time of writing sits at 90p to sell. GVC: I bought these back in January this year as I liked the transformational story that was unfolding. On an initial purchase, I place a 20% stop loss which I then convert to a non-automated 12-15% trailing stop loss as the share appreciated. This one has done quite well but has been falling back recently and breached by 15% trailing stop loss so time to lock in a 33% profit on a medium sized holding. The following have been purchased or added to in the last couple of weeks: IG Design: a top up of current position following very good interims on 29th November and a very positive outlook statement. I also get a very good impression of the management of IGR and with the exception of really bad news, intend to hold for some time. Topps Tiles: I rather liked the final results and the ditching of low margin products and the move to higher margin item including the large sized tiles; my thought was that the market had just not latched onto the change. However, an unfortunate accounting oversight in like for like sales has caused a jitter but not so much a jitter as that to be felt within their finance directorate I would suspect. These things happen, unfortunately, yet no lasting damage done as such in my opinion. Patisserie Holdings: CAKE: I was impressed with their interims and the organically funded roll-out programme and therefore added to a current position in CAKE. I really like the business and did not take much persuasion to adding stock on 29th November. D4t4: this one has been shouting at me through my cash flow screens over recent weeks and has really impressive returns on capital: ROCE 21% & CROCI 39%. I dithered a little last week as I needed to find out a touch more about the increase in receivables (4211) v 2121. However, I eventually felt comfortable enough to take an initial position at 140p. Since my purchase, a tip in SCSW has sent the shares up to 170p which bizarrely is more of a hindrance than a help in terms of adding further positions. ITV: again a share that has come up on my cash flow screens in recent months but was drifting back somewhat. That drift seems to have stabilised and I took an initial position on 6/12/16 at 171p. Very good yield and exceptional returns on capital: ROCE 40% & CROCI 23% plus decent enough trading update on 10/11/16. Overall the financial year is progressing well and certainly much better than I thought it would be following the shock Brexit vote. I do havea few Brexit beauties that have proved real bargain buys but thats another story. Incidentally, I always measure portfolio performance in terms of FY as it ties in with CGT and ISA timelines for the addition of cash which pleasingly increase to £20k next April. As ever, all dividends are reinvested in the relevant stock. We have now reached the third quarter for year 1 of the Passive v Reactive Whittler portfolios so it’s time for a quick review to see how my meddling has done compared to Mr Cool who simply sits on his hands and lets time do the work. I have again restated the basic rules for the management of the portfolios; see the last section of this article. All of the ten stocks common to the three portfolios were identified via my routine free cash flow+ returns on capital screen i.e. they all exist within my whittled down universe from which I make the majority of my real life share purchases. At the time of this third quarter update, I hold positions in five of the ten companies: SOM, CCT, AMO, NFC & PSN. I also held Hikma as a spread bet so that’s a financial interest in 60% of the stocks within this exercise. Update & Trading in Third Quarter of Year 1 (Aug to Oct 2016): Of course following the rules of the exercise no trading took place in the 3YL (three-year life portfolio) or the ASH (annual sit on hands) portfolios. Trading did take place in the Tinker portfolio and these are listed below: 3/8/2016: sale of 90% of position in Hikma Pharmaceuticals following a fairly mild profits warning. Note: following a profits warning I almost invariably sell at an early point; it’s what works for me and fits my approach to investing. Reinvestment of the £10570 from 90% of the Tinker holding in Hikma Pharmaceuticals: I was very tempted to purchase another block of Somero shares but that would have made the Somero investment far too weighty within the portfolio and therefore not the best risk mitigation management: Somero is, after all, a fairly low market capitalisation stock at about £90m. So, the £10570 surplus cash was reinvested by equal amounts in two stocks: 3/8/2016 Next Fifteen Communications with the purchase of 1748 shares at 305.5p per share. Reason for the purchase of NFC: simply the performance of the shares and very encouraging outlook/update statements from the business. 3/8/2016 Persimmon with the purchase of 314 shares at 1679p per share. Reason for the purchase of PSN: the post Brexit gradual recovery of house builders after they were initially trashed following the vote to leave the EU. I also consider PSN to be a high-quality business. So in the third quarter we have a had a touch of tinkering but in reality the amount of tinkering over the first three quarters of the like of the portfolio closely reflects my usual approach to the markets where I do not over trade and generally take a patient outlook to life unless I see a reason to alter a position due for example to a compelling good or bad news RNS from the company. How are the three Portfolios doing now we have reached the end of the third quarter? Well as 3YL & ASH are identical composition and allocation in the first year, they are identical with the original £100k now reaching £115.0k, a 15.0% increase in the first 9 months of the exercise. The Tinker with its three partial sales of holdings and associated reinvestment over four other current holdings; in effect top ups, now sits at £117.0k an increase of 17.0%. The comparator for “how are we doing” is the FTSE ASTR (ASX.TR) which rose by 17.6% in a generally volatile February to October period that included the once in a lifetime Brexit event and the following market turbulence. As ever, dividend which contributed approximately £3250 for each portfolio over the 9 months were reinvested in the relevant stock. Overall, all of the three portfolios are performing well enough at this early stage: the five best performing stocks over the first three quarters of investment were:- Next Fifteen Communications, Amino Technologies, Somero Enterprises, Elementis and Dignity. The full 9 month performance of the 10 stocks is listed in the table below for the ASH “sit on my hands” for a year and don’t trade portfolio and the Tinker:   Busy day Saturday, off to Nottingham to watch the Hatters take on Notts County and on a fairly tight time schedule and not really expecting a call from Matt to talk about shares as he ponders if the stock market is really a place for him rather than leaving his spare money, the stuff he definitely does not intend to use for the immediate few years, safely tucked away in the bank/building society. I must admit after my last discussion with Matt just over a week ago, I rather felt that he had almost already decided that it would not be for him.

Anyway, Matt is today all fired up with enthusiasm as the phantom portfolio I am using to teach him a little about the markets with is up by about 3% since we opened it. Oh no, I think to myself, from “don’t like the risk of losing money” Matt has now turned to “do like the idea of making easy money”. Ok, I tell Matt, not a bad start but it’s really little more than noise in the grand scheme of things. Investment, particularly in neglected/value stocks is not about performance over 9 days, 9 weeks: to my view, sticking with 9 you are more realistically looking at 9 months to a couple or so years. Of course, this unwelcome damp cloth place on Matt’s smouldering enthusiasm did not go down well as I could tell by Matt’s hesitant response “well, I sort of thought that things looked good, don’t you”? Well Matt, let’s look at the very choppy waters that these six stocks have to sail through over the coming five weeks. The dodgy time for stocks are Matt is usually when they release either trading updates, interim results and final results. Why do I say dodgy? It’s then that they give us an account of how current trading is going; historic performance does not really matter that much as it’s all generally built into the share price; what the market really wants to know is how are things going now, what does the order book look like? Now for each of these six stocks I have discussed their fundamentals on my Stockwhittler site in the past, so Matt, check back there if you feel the need. However, do look at the following schedule of news release and brace yourself; the current trading will most probably be in-line i.e. no shocks and as expected. However, it could well be a touch negative or hopefully a touch positive. The dates to put in your diary Matt are: 3/11/16: Final results (year-end) for beaten up Gattaca; yes, what a silly name for a company; what was wrong with Matchtech? Also, yield > 6% 17/11/16: Interim (1/2 year) results for Norcros; I like the company but the market seems scared by the pension deficit which I see as well mitigated. The average age of those collecting pension from the fund is late 70’s so without wishing to sound overly callous, it’s overall liability will shrink fairly rapidly in the coming few years. Just one little negative phrase and the shares will fall a few pence. Norcros is a strange one to get your head round in terms of basic numbers; the yield is just about the same as PE; crazily undervalued or the territory for a fool? 29/11/16: Final results for Topps Tiles: the market was spooked by their last trading update; me, I thought it was fine for the medium term but that’s what investing is about, taking a view. 30/11/16: Telford Homes Interim Results: I really like this share but the market seems to be very suspicious of it and it was heavily brexited back in the summer. Am I right, well very positive noises from the company suggest all is well but we will have to wait and see: yield about 5%. 01/12/16: Character Group Final Results: certainly not loved over the last 12 months but has Mr market got it wrong? I suspect Mr Market has got it wrong but there again, just my view! 08/12/16: Waterman interim dividend: ok nice to have Matt but you have to remember that the share price invariably falls by the same amount as the dividend paid on ex-dividend day. Do remember Matt, that I am not always right with my perception of a company; like all investors, I certainly make my fair share of purchases that in retrospect don’t head in the desired direction but that’s investing. When I get things wrong, I try to close my position as soon as I hit the appropriate stop loss but when I am right I try to be brave and ride the wave as high as I reasonably can. So, Matt, that’s a little bit of interest and worry for you over the coming weeks; your theoretical 3% gain could so easily be a -10% loss or more within five weeks with all of this news about to be released: could you sleep easy with that Matt? I have to dash for a train now as a couple of foaming pints of ale await me in Nottingham; catch you soon once the news flow begins |

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed