|

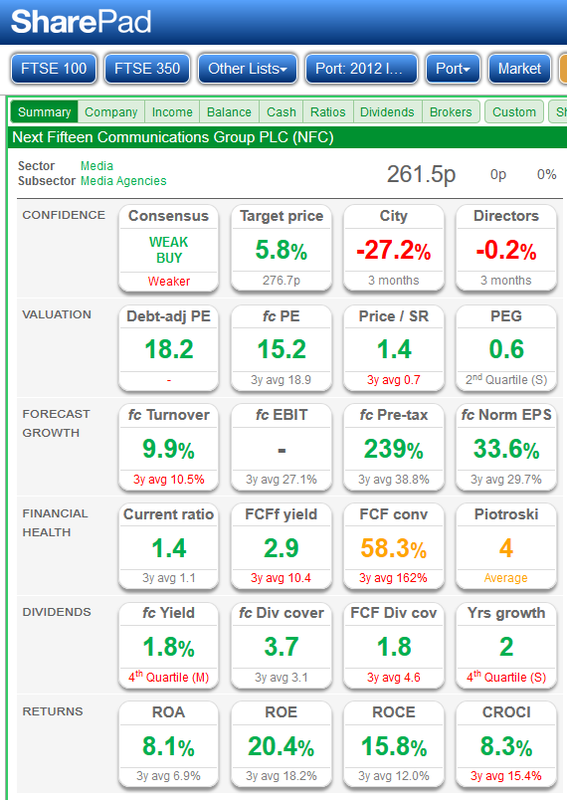

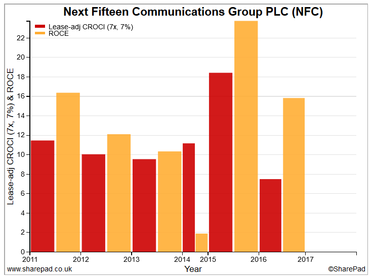

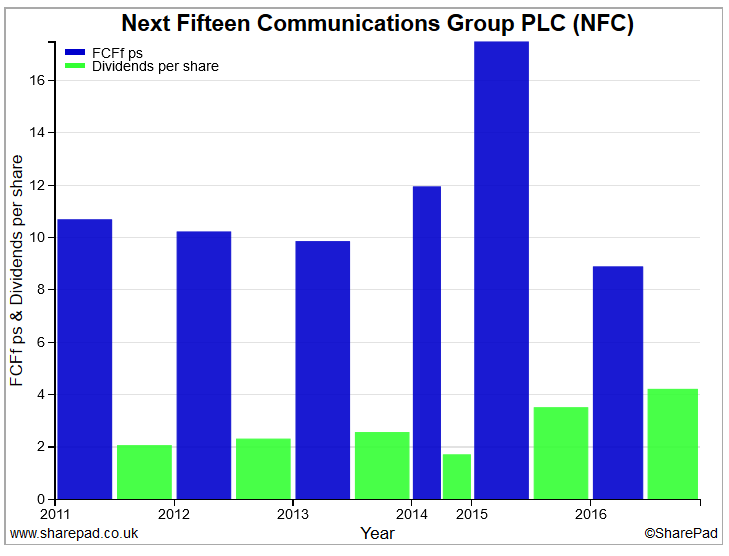

It’s time I gave an update on portfolio activity in the last few days. There have been three new additions to the portfolio and one top up of a current winner. The new additions include two purchases identified my cash is king screen/free cash flow screen (CashKi.FC, not a third division Polish football club but a screen I regularly use to identify companies with good free cash flow and good returns on capital). The new additions are Next Fifteen Communications (NFC) and XP Power (XPP). One purchase of a fairly boring buy steady consultancy, Waterman Group (WTM) and finally a top-up of a current holding in Portmeirion Group (PMP). NOTE: I am moving to use a financial dash board as per SharePad on my blog notes when discussing share purchases and sales. For those who do not use SharePad, I can only suggest that you give it a try: a totally superb tool in my opinion. Next Fifteen Communications: Market Cap. £189m NFC previously held and allowed myself to get bumped out by the “noise of experts”; quite silly really, you listen to the noise, ignore the numbers and the genuine news and before you know it you have hit the sell button. When I sold NFC I had made a 90% total return in 12 months but the fear of losing some profits combined with that dreaded noise resulted in the sell button being pressed. Had I done the sensible thing and just let the trailing stop loss do its work, I would have made a gain of around 220% for just holding for another 18 months. A strange part of investor psychology is that it can be very difficult for an investor to convince themselves to go back and buy a share that they have previously sold at a lower price having taken a profit; just the way we are wired I guess! Anyway, my CashKi.FC screen kept showing NFC and in addition, I was impressed with the finals for NFC delivered on the 12th April; summary below. Final Results of 12th April 2016 Highlights:

Current trading and Outlook Looking ahead, the Group has made a good start to the new financial year with trading patterns continuing as in the second half of our last fiscal year. The Group has made two further acquisitions in the UK of Publitek, a specialist content agency, and Twogether, a technology-focused digital agency. My View So there we are, a purchase that as with most of my purchases will not be looking to generate a fast buck. I will use an initial 20% stop loss on ShareScope but manually execute if applicable. Price target? Well, I will set a target of 20% TR and review if we get to that level. Oh, for good measure a fairly decent Stock Rank of 78 on Stockopedia and a value of 18, equivalent to 82, on Sharelockholmes: with Stockopedia 100 is best and it’s reversed on Sharelockholmes with the lower figure being the best. The financial summary looks attractive, the returns on capital CROCI/ROCE are attractive and the dividend is well covered by FCFfps.

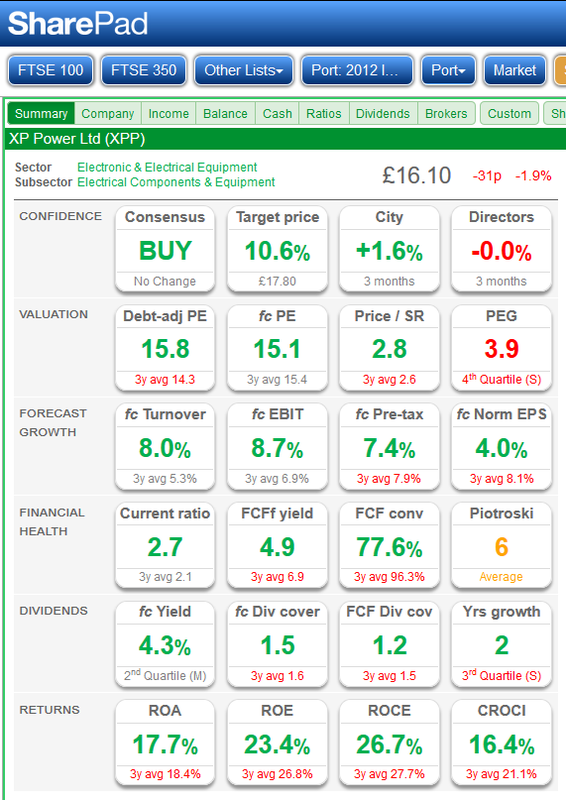

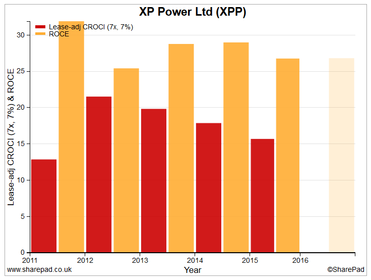

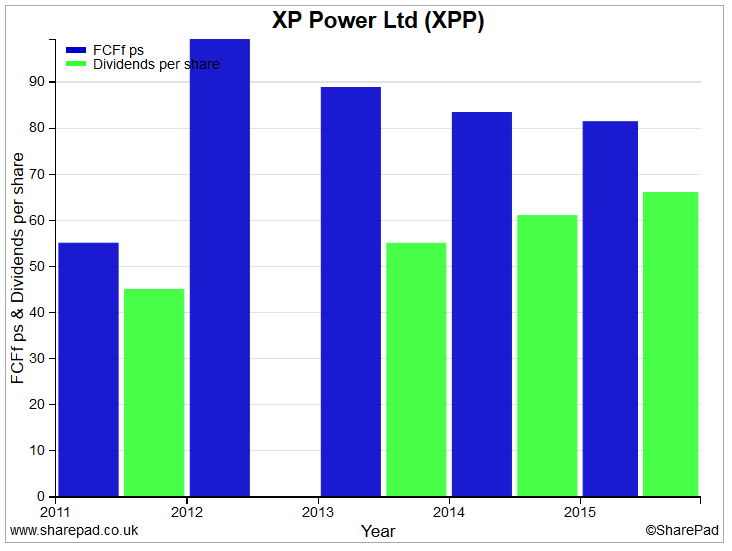

XP Power: Market Cap. £310m Another share that came through my CashKi.FC screen is XP Power. It’s not a share I have owned before but it’s attractive enough for me to make a purchase. They produced their most recent finals on 22nd February and whilst not stunning, they were solid.

Outlook We are encouraged by the stronger order intake experienced in the fourth quarter of 2015 following the weakness we saw in the North American order intake in the third quarter and by the progress of the integration of EMCO. Despite the mixed global economic picture, we have positive momentum and therefore expect further growth in revenues in 2016. We now have a high voltage product offering, which we believe we can grow using our direct sales channel and approved supplier status with our existing customer base. We also have a strong balance sheet and a business model that provides excellent cash generation to fund our existing needs and targeted acquisitions to further broaden our product offering and engineering capabilities. Trading Update 11th April 2016 Trading in the first quarter has been strong. Group revenues in the three months to 31 March 2016 were 28.2 million (2015: 25.6 million) up 10% from those achieved in the same period a year ago. In constant currency, revenues were up 6%. My View I am attracted by the financials, excellent free cash flow and the prospects for steady growth in profits. For good measure, Stockopedia have a Stock Rank of 94 whilst on Sharelockholmes they have a value of 3 which is 97 in Stockopedia terms (with Stockopedia 100 is best and it’s reversed on Sharelockholmes with the lower figure being the best). The financial summary looks attractive, the returns on capital CROCI/ROCE are attractive and the dividend is well covered by FCFfps.

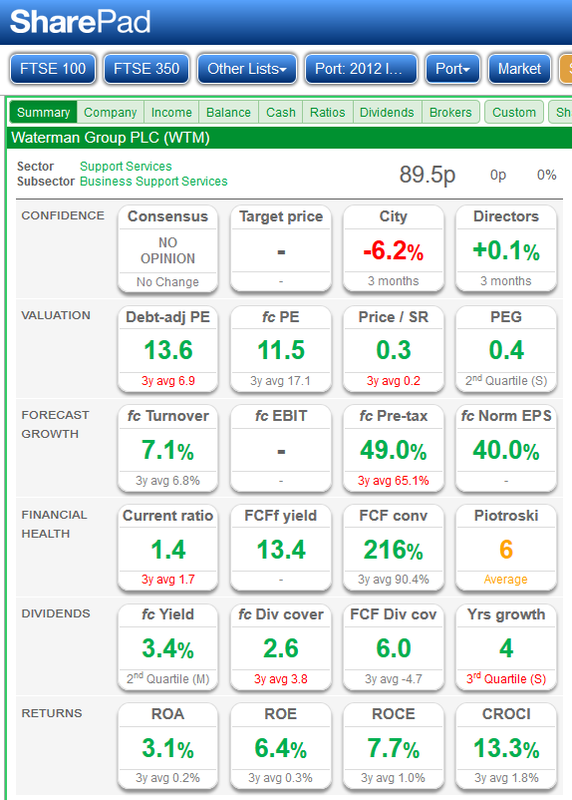

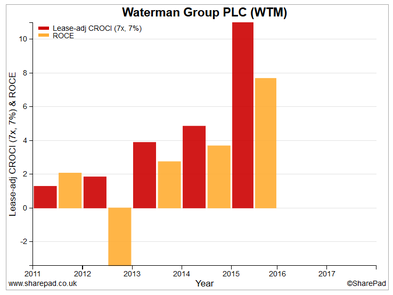

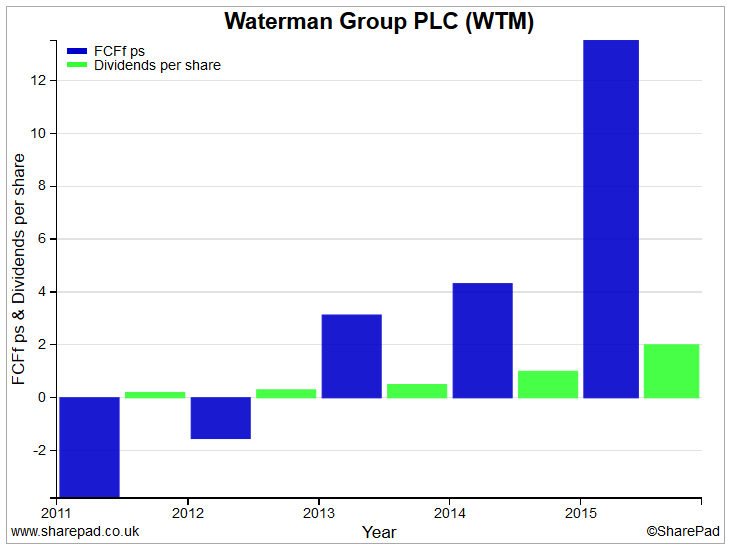

Waterman Group: Market Cap. £27m This one is a fairly boring consultancy group. The Company, through its subsidiaries, is engaged in the provision of design services and advice in the fields of civil, structural, mechanical and electrical engineering together with environmental and health and safety consultancy. All fairly unexciting stuff but somebody has to do it and also make money at the same time. In truth, they are a touch on the small side for me with a market cap of around £28m. They don’t have any debt and after a fairly lean 2010 to 2012, their operating profits have been climbing nicely resulting in net profit in 2015, decent projections in both the current FY and next FY. The business is cyclical by nature and not very high margin. Heavens, I am almost convincing myself to sell it as I read the text I am typing! No, seriously I do feel there is scope for some SP appreciation and they also carry a fairly decent yield at over 4%. However, the most interesting part sits in the outlook statement below with target increases in PBT, ROCE, and operating margin. Highlights Interim results of 29th February 2016 6 months to 31 December 2015

Outlook Waterman is on target to exceed its previously declared financial objectives to triple adjusted annual profits before tax to £3.3m over the three year period to 30 June 2016, with a return on capital employed (ROCE) of 20%. In October 2015, the Board announced a new aspiration to increase the Group adjusted operating profit margin to 6.0% by June 2019. As noted above, the Group's progress against this objective is positive with adjusted operating margins increasing from 3.3% to 4.1% over the last twelve months. The Board expects further progress to be made during the second half of the current financial year and beyond. The results have benefitted from the Board's strategy of focusing primarily on the UK, where 90% of Waterman's revenue is now generated and this focus is anticipated to continue for the foreseeable future. Waterman's long-standing relationships with blue chip companies continue to generate repeat business year on year and the Board expects this to continue whilst the UK economy is strong. The Board looks to the future with confidence. My View I quite like the business and whilst not wanting too many of it’s type in my portfolio, I feel comfortable enough to have bought a reasonable but not large holding in terms of % of my portfolio. For good measure, Stockopedia have a Stock Rank of 99 whilst on Sharelockholmes, they have a value of 4 which is 96 in Stockopedia terms (with Stockopedia 100 is best and it’s reversed on Sharelockholmes with the lower figure being the best).

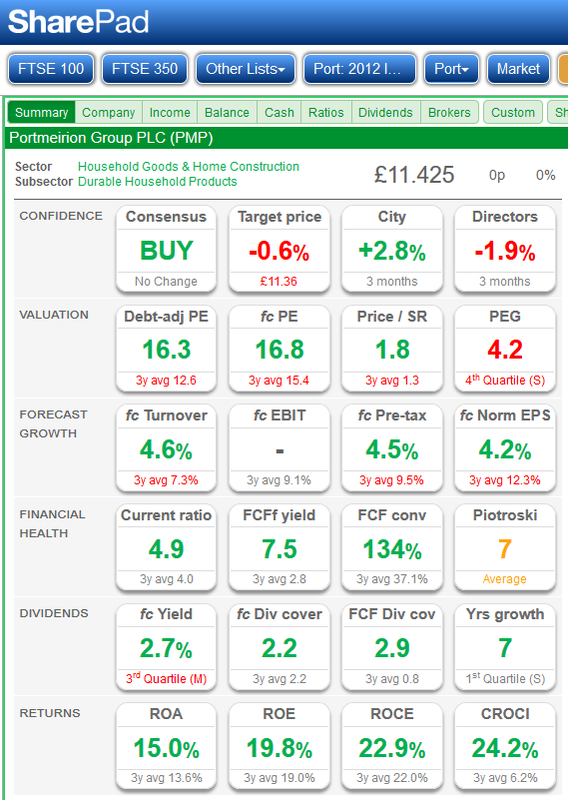

Portmeirion: A Top-Up: Market Cap. £130m Simply another top up of a current holding that has already given me an increase of 80% since my original purchase two years ago. A nice boring, unexciting company with steadily rising revenue and associated profits and offering a yield of just under 3%.  Happy investing!

0 Comments

|

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed