|

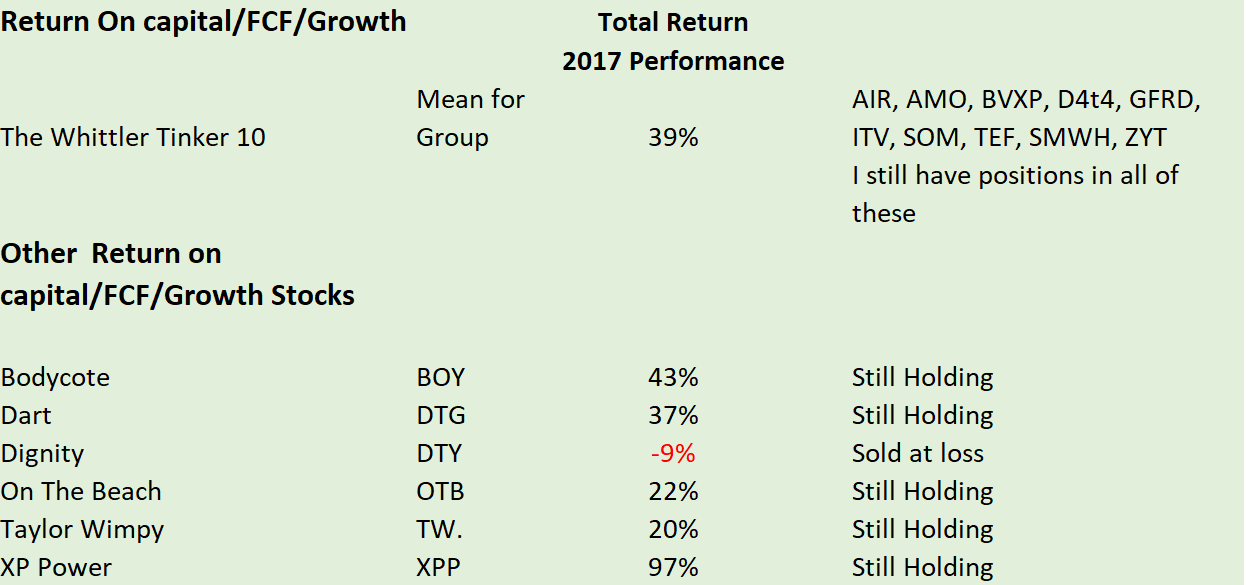

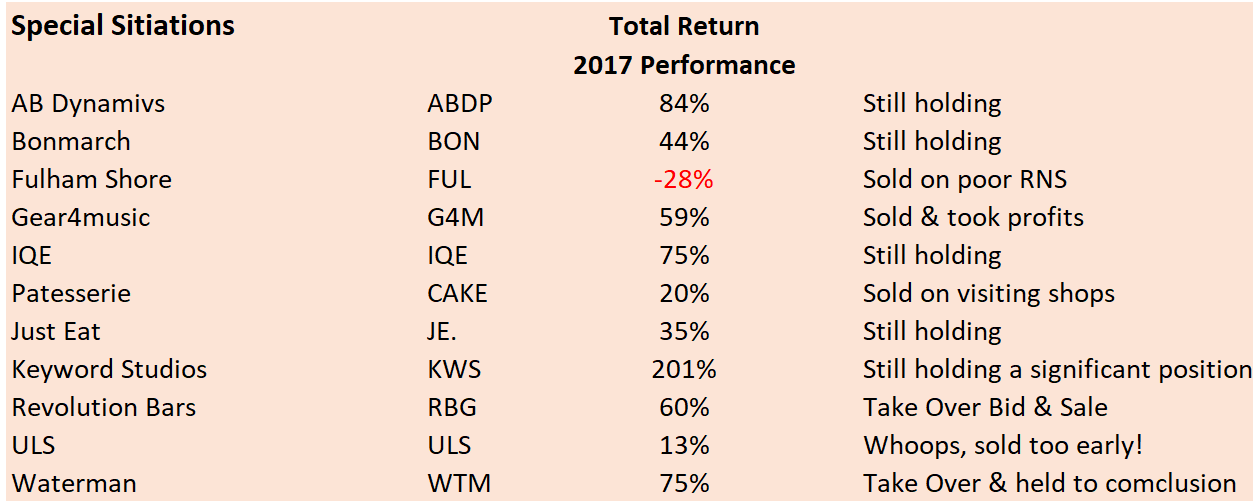

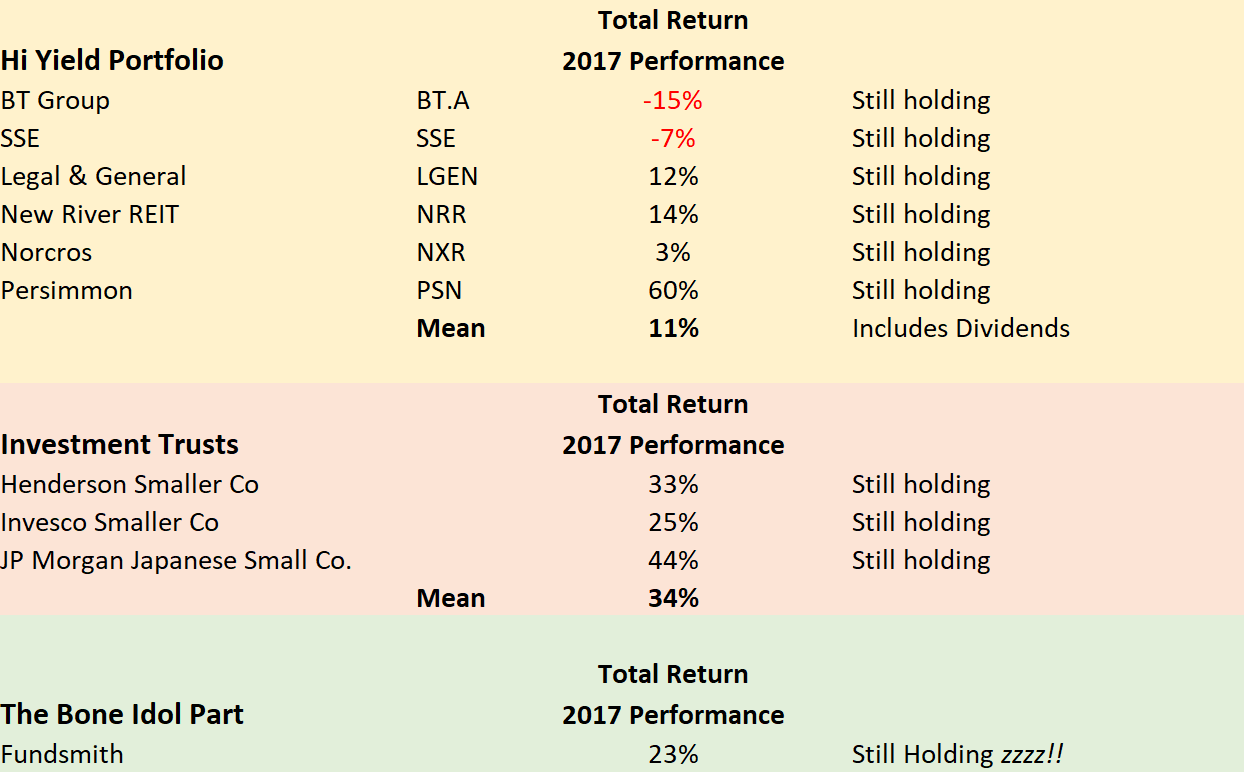

Well, it’s been an interesting year and indeed one of the most prolific years in recent times for many private investors exercising a degree of discipline and wise selectivity on the stock market. Of course every year we have stories of huge percentage gains made by what I term as punters on the markets investing in a hole in the ground in the middle east or some other excrement or bust enterprise. The thing is with these types of punter who usually appear on those dreadful bulletin boards is that they emerge to tell the world of their wisdom but then rapidly submerge again as investment reality kicks in: not my style or approach to investing but each to their own. Thankfully we have a very healthy Twitter community and some really excellent blogs where respected honest investors share their thoughts and long may that continue. So, a few thoughts on 2017: Firstly, have I changed in my thoughts on noise? No, most definitely not, I steer well clear of investment periodicals; have a look at my watching the detectives blog. I also take no note tipsheets which to my mind are a blasted nuisance should a company you are researching be filled by one of them. Also, I have to say that whilst never being the most prolific tweeter, I have become rather selective both in terms of reading and time spent on Twitter. To my way of thinking, investment is about choosing an approach or combination of approaches, you feel comfortable with, continually refining that approach and keeping a timely eye on any RNS from one of your stocks. Oh yes, let’s not forget the vitally important ruthless weeding out on any stock showing a risk to the bottom line of the investment basket. Secondly, Have I changed my investment approach in 2017? Not really as my universe is still based on a number of building blocks. That’s two major blocks that probably cater for the bulk of my investments are firstly a combination of Return on capital/FCF & Growth and another fairly big section covering what I call special situations. Bringing up the tail I have three more minor sections covering high yield, investment trusts and finally a few years worth of ISA subs in Fundsmith; that’s the bone idle part that Terry Smith manages so very well. The two main blocks are in a little more detail: Firstly a combination of attractive returns of capital invested and good cash flow/free cash flow and some growth stocks with properties along the lines of the great Jim Slater, a chap that taught me so much back in the late 1990’s. SecondlyThe Special Situations Block: this block may to an extent to having some of the characteristics of the first block described above but will really be looking at companies that have something relatively exciting happening; possibly a potential takeover situation, a game-changing event or maybe just simply a stock that the market has in my estimation dreadfully mispriced. We then have other smaller blocks: The Income Stocks Block: just doing what it says on the tin but avoiding income traps where an apparently attractive yield is miserably covered and indeed nowhere near covered by free cash flow (utilities are of course an exception). Investment Trusts Block: I have for years been a fan of investment trusts and indeed some of my very first investments were in these vehicles The Totally Bone Idle Block: this consists of an appreciable block of the superb Terry Smith’s Fundsmith which I have held within an ISA wrapper since shortly after the fund was introduced to the market. Why do I like Terry’s approach; well for two reasons: firstly his approach to ROCE and cash flow with quality businesses mirrors my own approach to investing and secondly it gives me very valuable overseas exposure. So, what if anything has changed in terms of my writing in 2017? Well in July 2017 I added a new section into the Whittler blog to cover a roughly weekly review of any RNS stories that affect stocks from within my portfolio. As with everything I write, it is in no way a recommendation to either purchase or sell a stock but simply my sharing of my thought process. Oh yes, maybe I should mention that my ruthless jettisoning of any “did not get it right” purchase or resolve to sell immediately on a profits warning have become even firmer during 2017. I honestly just do not understand investors who cling on to a stock that is either underperforming or surrounded by bad news. To hold on to such a stock in the hope that you can be proved that you were “right in the first place” is to my mind totally flawed thinking. So, how have things gone for the markets in 2017? Well let's have a look at the various indices: FTSE100 gained 8.0% FTSE250 gained 14.7% FTSE Small Cap gained 15.2% FTSE All-share total return gained 13.2% FTE AIM 100 gained 33.3% Overall the markets were in a fairly good place during 2017 with worthwhile gains being had on the major indices but the real hard work being done on the AIM market. Now I appreciate that AIM may have had something of a bad press over the years and indeed that’s a well earned for many blue sky stocks pumped by mouthy CEOs and stocks from dubious locations outside of the UK. However, careful stock selection can be incredibly rewarding on AIM. As an example take the Whittler Tinker which I blogged about before bringing the series to a close. That portfolio of 10 stocks which closely mirrors my own overall approach and performance, appreciated by 39% in 2017 and 74% since January 2016 (I own or have recently owned all of the stocks within that series of blogs). Interestingly the lions share of the gain in 2017 being delivered by five quality AIM stocks; Bioventix (BVXP), Air Partner (AIR), Somero (SOM), Telford (TEF) & Zytronic (ZYT). The other major gainer within the Whittler Tinker in 2017 was my incredibly boring but lovely WH Smith (SMWH) which waded in with a total return of 53%; I love boring stocks. Now I should say that gains within a calendar year cut little ice with me as what significance does a calendar year have? I really don’t know. I find it far more sensible to consider the gains or losses one makes over a financial year as this at least ties in with the tax year and the ISA year. Indeed, I would go further as to say that gains only really become really meaningful over a period of let’s say five years. However, having said that, let’s for a bit of amusement at the end of 2017 see what the performances have roughly been over the last 12 months:-    The returns have been very decent in 2017 but as ever, I have been totally ruthless in removing any stocks where the original story or reasoning behind the purchase has changed. This vitally important approach has over the years done so much to preserve the capital within the overall portfolio. To give an example, in 2017 I sold Revolution Bars Group when an RNS informed the market that the third CFO in 12 months was leaving the business; simply a red flag in my opinion. Subsequently, RBG issued a profits warning and the skates were hammered by some 50%. The story then began to change when a new sector experienced CFO was appointed, accounting improved and a decent trading RNS issued. I then bought back in with two thoughts in mind. The stock had become what I term as a special situation firstly in terms of recovery and secondly takeover potential as the wounded RBG looked ripe for a predator to pounce. Fortunately, the competitive bid situation emerged and I subsequently sold at a very decent profit. It was a similar story with Waterman earlier in 2017.Was I lucky? Well undoubtedly I was but the more I persistently apply my approach based on sound research and quality companies, the luckier I seem to get. I should add that the number of underperformers that needed to be weeded out early in 2017 was the lowest number I have ever encountered; just a small few and thus having a negligible effect on the bottom line. What will 2018 offer? Well, I don’t have the slightest idea in fact truthfully nobody knows what the following 12 months may bring. All right, you get plenty of paid commentators offering their opinions but I just see this as totally irrelevant noise; put it another way, if they did not comment, they would not have a job. What I would say is that sooner or later we will be in for a couple of negative return years and then I suspect we as thoughtful investors will be more than happy with an annual return of 12-16% over a period of let’s say a 10-year timeframe. So for all of those investors who have enjoyed some really good gains in 2017, particularly fairly new investors, do take care of those precious gains as 2017 has been anything but a typical year. What do I plan to do in 2018? Well for certain there will be no new year’s resolutions; never really saw the point in resolving to do something that you give up on by February. What I will continue to do is research stocks for universe consideration, continue the Stochwhittler blog continuing to publish a weekly or thereabouts RNS log and continue with my football writing. I will also keep reading some of the splendid blogs written by some excellent twitterdrome investors. Whatever you plan to do in 2018, I wish you firstly good health and a successful 2018.

1 Comment

david houghton

1/7/2018 08:02:20 am

Well done over the past 12 months. Really enjoy reading your blog. Very thoughtful and sensible investment advice. Your comment will be posted after it is approved.

Leave a Reply. |

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed