|

Well, the first steps in my investment journey had really gone well with the easy stuff of buying shares in the utility company I worked for. I had also branched out just a tad, and bought into some investment trusts run by Edinburgh fund managers and that gave me a buzz in terms of doing something a little more myself rather than just taking the safe pickings from utility flotations. The next logical step of the journey was, of course, to really become a big boy and buy some shares in individual companies but how would I select them. Possibly via tips in newspapers or via tip sheets. In the end, it was a combination of tip sheet and the papers with the first purchase being a house-builder that was rapidly acquired by a larger player for a premium; nice, I thought! I started to read a penny share tip sheet that suggested two really hot companies to get into were Azur; a ladies fashion company and also the British Taxpayers Association; both traded on the OFEX market. The write up for each seemed to be very convincing and the fact that you needed to subscribe to the penny share publication to obtain these privileged hot tips, gave me the confidence to buy both. I was naive of course and the collective investment soon proved to be a bit of a disaster; I learnt that such very junior markets were not for me: lots of promise of jam tomorrow but as my old granny used to tell me, “tomorrow may never come”.  Bound just to be a temporary setback I convinced myself and boldly strode onwards. With just basic research of the Helphire prospectus and the confidence of reading in the press the high regard of the management of the business, one the first day of trading in late 1997 I purchased some Helphire shares. Within a few weeks, I was handsomely in profit; this share price just kept going up and up; obviously one for me to hold onto; no intention of selling these boys quickly! Some of my colleagues at Anglian Water, flushed with the success of AW share ownership, were also becoming impatient to dip their toe into the stock market pool and decided it would be a good idea to form an investment club. Our meetings were held in a pub in Cambridge: it was rather nice and very social. The format was for at least one potential purchase to be nominated, followed by a discussion of merits and voting. For our first purchase, I nominated Helphire, telling the group of my very wise decision to buy and boasting that I was already 20% up on the deal. My powers of persuasion came to little as the vote, went in favour of the nomination of a wiser sage within the club who had been investing for many years. Our sage wanted us to stay local within Cambridge and buy shares in Ionica a telecommunications company in Cambridge. The club was good fun but after Ionica, despite our unrelenting loyalty and refusing to sell, went bust, the investment club became less active. The investment club continued for a couple of years but the realisation to some members that they may actually lose money severely dampened their enthusiasm for the venture. Undaunted and possibly bolstered by my already growing experience of share success and failure, I confidently continued on my investment journey. I say confidently, although I was honest enough with myself to realise that the dramatic Helphire success, which by this time had trebled in value, owed much more to luck than my prowess as a stock picker: of course, when I did regale the story of my success, it was all down to my smart decision making. I decided I really needed to build my knowledge on what may make a good investable company over a poor company. I continued with various tip sheet publications: The Analyst, Technivest, Quantum Leap and others came within my radar but I never really felt comfortable with either their reasoning or that fact that the share price was usually up by about 15% directly on the Monday morning following publication. I continued to plough through newspapers and then stumbled upon a couple of columnists that struck the right note with me: Jim Slater writing in the Mail on Sunday and Paul Kavanagh in the Sunday Times. I did not realise it at the time but these two guys would have a considerable impact on my investment journey as we headed towards the turn of the century.  I was becoming very impressed with the work of Jim Slater and bought his incredibly well-written book “The Zulu Principle”. The reasoning within the book was to my mind so very sound, understandable and convincing. Within my salaried employment I was managing a budget of £10 million pounds and dealing with accountants on a very frequent basis and maybe my confidence with financial budgets made the book all the more appealing. Jim mentioned such sensible things as a reasonable valuation for the expectation of future growth in earnings, the relative strength of the share price, the non fudging of profits and returns on capital: all aspects that would become hard coded within my thinking. Following Jim’s well-reasoned guidance and understanding a little more of the financial criteria, I bought another two stocks: Blacks Leisure and DCS. Both of these stocks rapidly began to motor and I was a very happy investor. Wow, this was really good stuff and as I was feeling absolutely fabulous, I bought another growth stock; Harvey Nichols. Unfortunately, Harvey Nichols failed to move in my favour but the good point was that I was rapidly developing the realisation that even with reasoned share selection, it’s the performance of the collective basket of shares in your portfolio that determines joy or sorrow.  "No worries dear, just this months Company REFS arriving" My thirst for knowledge started to take up more and more of my time as I read various investment books including What works on Wall Street, Beating the Dow but I was so impressed with Jim Slater’s works that I followed up his association with Company REFS and took out a subscription. At the time the publication consisted of the equivalent of a couple or more telephone directory size catalogues; they were heavy beasts as they mounted up and pre-computing took a massive amount of time to sort. The good thing was, however, that absolutely superb financial data had become available to joe public but at a cost. So for me, the post service became a source of not only data but the contract notes for my share trading. The trading commissions themselves could easily eat a hole in your portfolio value as at least one broker I was using at the time had a charge of £45 per transaction; nothing like the £5 for any amount that we are spoilt with today.  I started to attend various meetings & lectures in London, particularly ones involving lucky Jim; they were really so informative. I also remember attending one hosted by the owner of the Analyst tip sheet where it was explained to the audience that JJB sports was a share that you should plan to hold for life; although I held JJB at the time, I found the “hold for life part” a touch difficult to follow. The internet was now coming of age but to get on-line at work back in 1997 was something of a challenge: whatever did the directors think we were going to do with such access. It became clear that I needed to buy my own PC for home use and I invested £2000 in a start of the art 4GB hard drive, 64mb RAM monster with a 15-inch screen; now we are flying with my dial-up internet connection! This was my first PC since a Sinclair ZX Spectrum, heavens I hated that thing! Now getting online; wow was I lucky, all of this information on free bulletin boards written by people who were obviously in the know yet willing to share their wealth of knowledge to all: welcome to the world of ramping. Overall I was a happy chap, I was learning all the time about share selection and making money. I used to have many coffee break discussions with Gordon who had the contract to maintain the power facilities in the labs. Gordon was a very keen investor but each coffee conversation started with his cursing of Adil Nadir and Polly Peck; Gordon had suffered a particularly bad experience in that area. Anyway, on this particular morning, Gordon said “my broker has been trying to push me in the direction of Fibrenet, reckons technology is the next hot thing”, “what do you think Bill”?  Hmm now there is a thought; the journey continues!

0 Comments

Patisserie Holdings is a share I have been keeping a watch on for a few months. Strangely I first visited one of their outlets when I was attending a football match following the hatters. The local police would not let any football supporters into any pub within town; even a pleasant mature chap like myself: Well no beer, so I sought out the next best thing; coffee and cake. The outlet I attended was indeed impressive and I made a mental note. Oh, the match was a fairly dull goal less draw in atrocious wet conditions that saw us defend the shallow end in the first half.  Today, 18th May 2016, Patisserie Holdings issued their half-year results for the period to 31st March 2016 and to my mind, they were a really sound set of results.

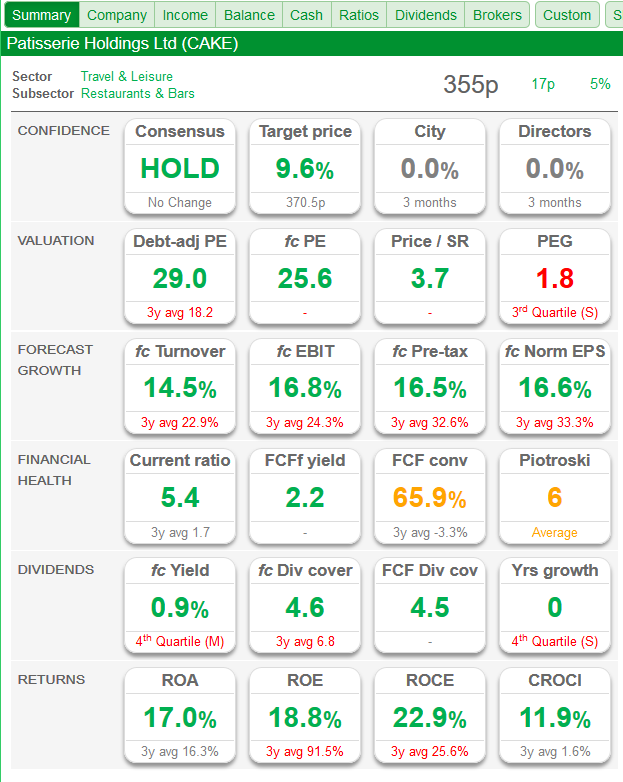

From the RNS: Current Trading and Outlook These results represent another strong performance from the Group. We continue to control costs tightly, make efficiencies in our supply chain and with the quality of the new site openings in the first half of the year, the developed pipeline and continued solid trading from our premium offerings I am confident of achieving the Board's expectations for the full year. My comment: The company are increasing the size of their estate and as they put it, very pleasingly funding the roll out from its own funds. Back to today’s RNS: Cash flow & Balance Sheet The Group remains solely funded from reserves and operating cash flows and at the end of the period had net cash of £8.9m (2015: £3.0m). Operating cash generated in the period was £10.2m (2015: £9.2m) and after interest and tax payments, free cash flows available for investment were £8.9m (2015: £8.0m). We invested £4.4m on property plant and equipment, which includes investment in new stores and a refresh of the existing estate. My comment Even after that, they manage to allow funds for the payment of a small but possibly growing dividend. In summary, the company has the following attributes that I like: Increasing turnover Increasing profits No debt Very good operating margin Very decent ROCE Good cash flow A concept that is being rolled out under what appears to be a well managed system. The dash board from the excellent SharePad shows:  The recent share price graph from ShareScope shows that the price has come off about 30% since the high the high in early 2016 but has been creeping up a little in the last few days and also got a nice 4% lift today (not shown on the SP graph below) with the interims:  My View on Patisserie Holdings

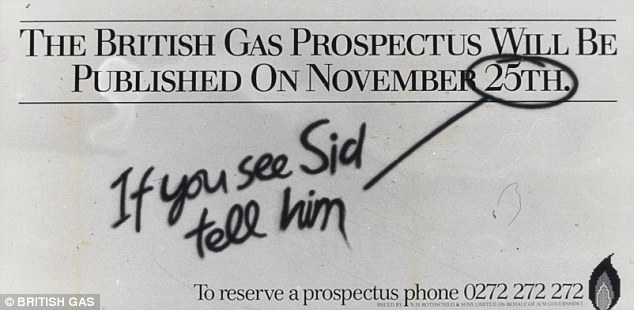

I like the company and the financial numbers but was a touch concerned at the end of 2015 that the valuation had become a bit excessive. To some extent this has improved as the share price has fallen back as much as 30% but then even to some, the share will appear overvalued. With today’s interims looking so strong and with the rate of growth and no debt, I am happy to take today as a buying opportunity and take my first nibble of CAKE: will it prove too rich for my palate? Only time will tell! As ever, these notes are not investment advice. They are just a rambling on my thought process that resulted in my purchase of a position. -All private investors that at some time consciously took an investment on the stock markets did so as the start of an investment journey. For many that journey would have ended fairly quickly having suffered a series of poor investment decisions and for others, a little success probably kindled a spark of enthusiasm to go a little further on that investment journey. This three-part series is a story of my own journey starting back in 1989 to the present time, 2016. Part 1: Early Steps on My Investment Journey During the 1980’s a relatively new phenomena were being brought to the eyes of the great British public: the privatisation of various services that were state-owned assets via a listing on the stock market: industries such as gas, electricity, water, transportation & telephony went through the process of privatisation. Of course, there were massive arguments for and against the process but it was a snowball that was gathering pace and momentum during the 1980’s and 1990’s.  For many ordinary members of the public, it was really the first time they had been actively encouraged to own shares in a company. The "tell Sid" advertising campaign prompted many thousands of people to buy shares in British Gas. The “have you told Sid” promotion to raise public awareness of the privatisation of gas in the UK was absolutely inescapable and for many people the first real time they had directly owned part of a business; being a shareowner.

Like so many, privatisation was my first exposure to the world of share ownership and indeed the great publicity campaign that the accompanied the ongoing process. I had joined Anglian Water at the time of the formation of the water companies in 1974; that in itself was a grand place for a relatively young chap to be. The company was incredibly supportive I worked through part-time study to complete my professional qualifications in science and become a Graduate of The Royal Society of Chemistry. What I did not realise at the time was that this lad who joined the very large analytical laboratory service of this new business at the very first run of the career ladder would be fortunate enough to eventually spend twenty years managing one of the largest analytical services in East Anglia: you just never know how things will turn out! It was Anglian Water that introduced me to the racy world of the stock market as the company went through the privatisation process. Lots of publicity work took place within each of the companies heading down the road to the stock market and my own company was no exception with political figures involved in high profile publicity events. Just to name drop a touch, well why not, I gave tours of our scientific process to the very charming Lord Hesketh of motor racing fame and also Michael Howard a man destined to become a leader of the Conservative party; I have to say I took to one of these individuals much more easily than the other. As was common with all businesses about to be privatised, employees were offered preferential terms to take part in the privatisation issue and quite honestly it was a no brainier. The company was duly floated, nice phrase for a water company, on the stock market and the flotation price of £2-40 closing its first day’s trading, in 1989, some 15% up: I had become a shareholder, I was excited and my investment journey had begun. In those early days, I had not the slightest idea that the stock market would play such a large role in my future. Following the listing of the various energy, water company’s etc people who worked within the newly floated businesses were regularly offered share-save schemes. These basically allowed staff to buy shares in the business at a previously discounted rate and via monthly contributions from their salary over periods of 3, 5 and 7 years. To me, it sounded just too good to be true and I filled my boots as they say over the years building us a considerable holding in the business: I had become a fully fledged investor. There was no stopping me now from investing within my comfort zone and I took part in lots of other privatisations going on the time and became what is now known as a stag, buying shares in these newly privatised industries and with the exception of my own business, selling them relatively quickly and making some easy money. I decided I really liked this privatisation stuff, well at least in term of making me a wealthier chap. What I did not know at the time was that although it was fine making a very nice fast buck in staging, the real money and wealth would come to those with patience who took the very generous dividends and reinvested them the purchase of additional stock. My investment journey had begun and I felt quite pleased with myself: my lovely shares were rapidly increasing in value and paying very handsome dividends. Yes, I really liked this investment lark; what could possibly go wrong? Woops, I had meant to update at the end of April following the finals released by GVC on 25th April. Anyway, better late than never I suppose and a few brief notes for completeness are included here.

I originally purchased GVC in mid-January this year as the company having many of the attributes that I see in a prospective purchase:

The shares had already risen 25% in December following a good trading update together with more news of the acquisition of bwin.party. The company also announced it’s intention to move from AIM to the main market. Although it’s nice to be backing winners there is always the tendency to think “have I missed the boat”, am I now overpaying, simply it’s just the way we are wired that makes us think in that way. Anyway, the purchase went ahead at 472p and as we ploughed through the horrible January market decline, they fell to 420p before recovering along with the general market. GVC release their year-end results on 25th April 2016 and the figures were both pleasing and accepted well by the market. Kenneth Alexander, Chief Executive of GVC, comments in most recent RNS 24/04/2016: "GVC has had a momentous year. Not only has the Company seen a fifth consecutive year of revenue and clean EBITDA growth but the completion of the bwin.party acquisition in early 2016 affords us an opportunity to take the Group to the next level". "GVC has never been in a stronger position going forward. The enlarged Group is already enjoying encouraging trading, resulting from our unique mix of diversified products and strong brands. There is much work to be done, nevertheless, with GVC brands and bwin.party brands (including PartyPoker), growing, together with synergy benefits, we look forward with confidence to another successful year." My Other Thoughts: It’s an average sized holding in my folio, rather than a large position as I am always concerned about regulatory risk within this sector. Since my purchase, GVC has moved to the main market and has a fairly substantial market cap of £1.62 billion. The company is taking a dividend holiday for 2016 as part of the conditions of its financing of the bwin.party acquisition and this seems sensible to me. As I have said in other company notes, I don’t live or die by stock ranks but it’s nevertheless reassuring to see that Stockopedia give a stock rank of 91, however, Sharelockholmes are way less confident giving a market rank of 39 roughly equivalent to 61 in Stockopedia terms. The shares currently trade at 558p, up 18% on my initial purchase price: happy holder. I rather like the acquisition of Lighthouse Holdings by Portmeirion announced today, Lighthouse own Wax Lyrical Ltd the UK's largest manufacturer of home fragrances. They produce such items as reed diffusers and scented candles and there seems to be good demand from the public for such items with every supermarket stocking various varieties of each. Amusingly I first came across reed diffusers a few years back whilst staying in a rather nice Hong Kong hotel. I was washing my hands in the plush bathroom and thought I would try this “rather nice oriental handwash in a bottle containing sticks for application to ones hands”; enough said!

The £18m acquisition won’t in my view have any real impact in terms of carrying debt as the £18m consideration has been funded from cash reserves and debt draw down on new banking facilities comprising a £10 million loan facility, a £10 million revolving credit facility and a £2 million overdraft facility from Lloyds. Previous to this acquisition Portmeirion had no debt; a market cap of £127.6m and an enterprise value of £116.5m so no worries at all there. Lighthouse looks a solid business these days and the accounts for the year ended 31 December 2015 recorded revenue of £13.8 million, a pre-tax profit of £2.1 million and net assets as at 31 December 2015 of £7.6 million. That’s a very decent operating margin of 15% which bolts nicely onto the latest declared operating margin for Portmeirion on 12.5%. Incidentally Portmeirion have grown this margin year on year over the last six years. I particularly like the comments in the RNS: Strategic Highlights The Acquisition brings the following strategic benefits for Portmeirion:

It’s also good to read that Joanne Barber, the current Managing Director of Wax Lyrical, will continue to run the business: always good to see continuity. I did blog a note on the 17th April regarding my top up of my Portmeirion holding and all in all I am a happy holder. It appears that Mr Market is fairly happy today with the news as the share price has nudged up a modest but pleasing 3%. It’s time for the first quarterly update on the Passive v Reactive Whittler portfolios; I have again restated the basic rules for the management of the portfolios; see about 5 paragraphs down. All ten stocks common to the three portfolios were identified via my routine free cash flow+ returns on capital screen. At the time of this update I hold positions in three of the ten companies: SOM, CCT & NFC.

Update & Trading in Quarter (Feb, March, April): Of course following the rules of the exercise no trading took place in the 3YL (three year life portfolio) or the ASH (annual sit on hands) portfolios. Trading did take place in the Tinker portfolio and these are listed below: 1/2/2016: sale of 60% of position in Bodycote following a broker downgrade and the funds used to purchase further shares in Dignity. 1/3/2016: sale of 50% of position in Amino Technologies & the reinvesting of the proceeds in Somero following excellent preliminary results. On reflection the sale of 60% of the Bodycote shares was a slightly poor move that came about due to my listening to the market noise: yes I do whilttle on about not listening to market noise but somehow I did. How are the three Portfolios doing? Well as 3YL & ASH are identical composition and allocation in the first year, they are identical with the original £100k now reaching £109.9K, a 9.9% increase in the first 3 months of the exercise. Strangely the Tinker with its two trades also sits at £109.9k an increase of 9.9%. The comparator the FTSE ASTR (ASX.TR) rose by 7.3% in a generally happy February to April for the indices. The three best performing stocks were the smaller market capitalisation: NFC, ADT & SOM. The best performing large cap stock was BOY; the one where I listened to the noise and sold 60% on the holding in the actively traded Tinker portfolio. Reminder Of The exercise Rules. The three portfolios will be firstly a buy and hold for three years, ploughing on regardless through economic conditions, profit warning and any other news either good or bad. I will call this the three year life portfolio (3YL). The only time a change to the portfolio will be permitted is if a business is de-listed for any reason: the funds liberated would then be discretionally invested between the remaining stocks in the portfolio. The second portfolio will start out with exactly the same holdings as the 3YL but each January the same cash flow screens/returns on assets screen will be run and a revised set of ten stocks nominated. This revised set of stocks will have the proceeds of the sale of the previous years stocks equally divided between them i.e after one year we have £110k of funds then a purchase of £11k will be made for each of the ten stocks. I will call this the annual sit on your hands portfolio (ASH). The third portfolio will again start the same as the 3YL & ASH portfolios but I will alter the percentage invested in each position within the portfolio in reaction to RNS announcements from the companies, economic conditions or any other reason that seem valid for altering, reducing or increasing a position. I will call this portfolio the managed annual tinker portfolio or simply the TINKER. All 10 stocks will remain within the portfolio throughout the year although the investment in each stock may vary. For example one stock, let’s say Hattersville Dream Co. may issue a particularly bullish RNS “results will be appreciably ahead of market expectations”. The Tinker may sell down one or more of the other holdings to invest more in Hattersville but still retain a position, although not equal positions, in the same 10 stocks that we started within January each year. In January 2017, 2018 & 2019 this portfolio would be treated in the exact same way as the ASH and funds equally balanced across the each of the ten stocks starting that year. The common rules for all three portfolios:

|

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed