|

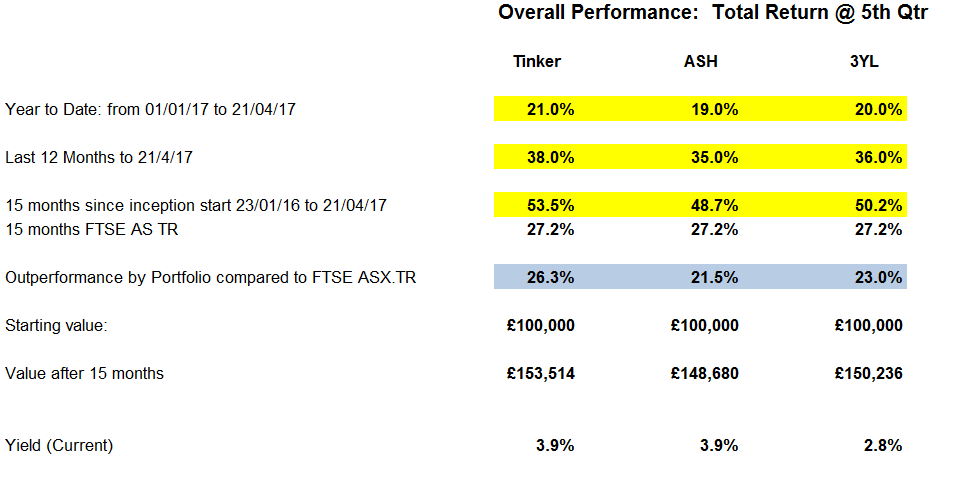

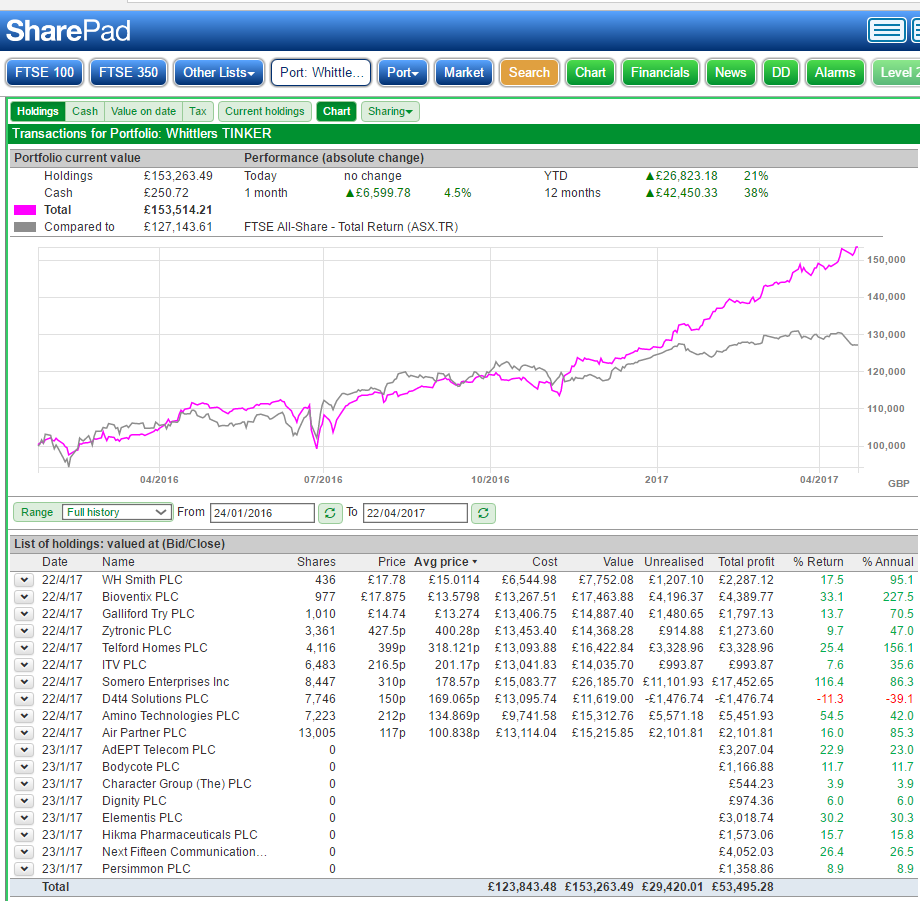

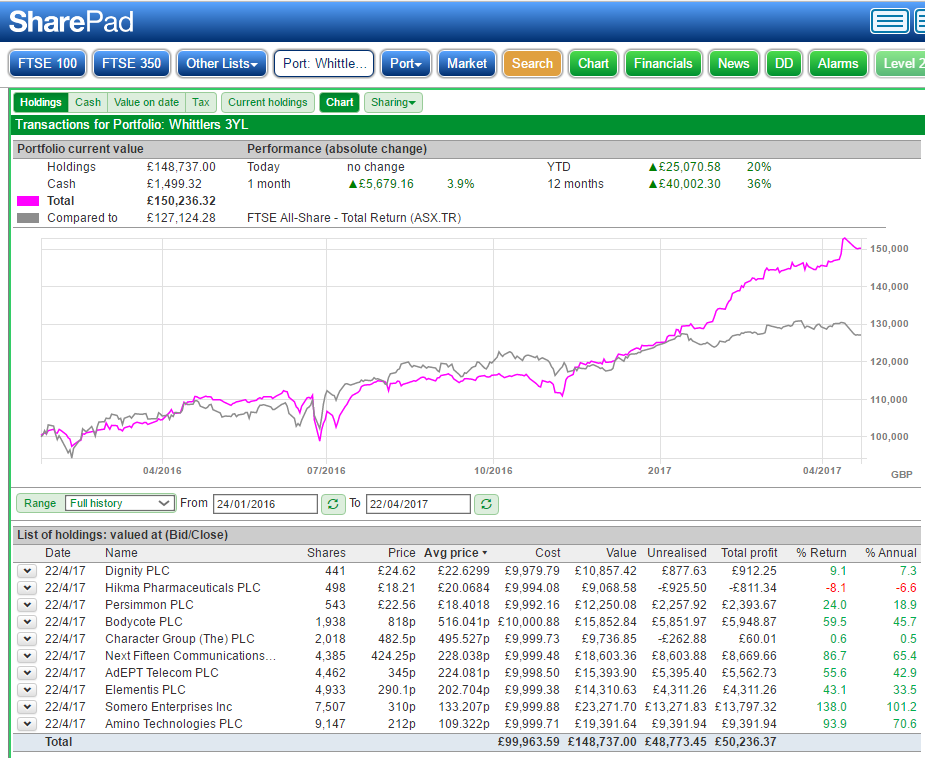

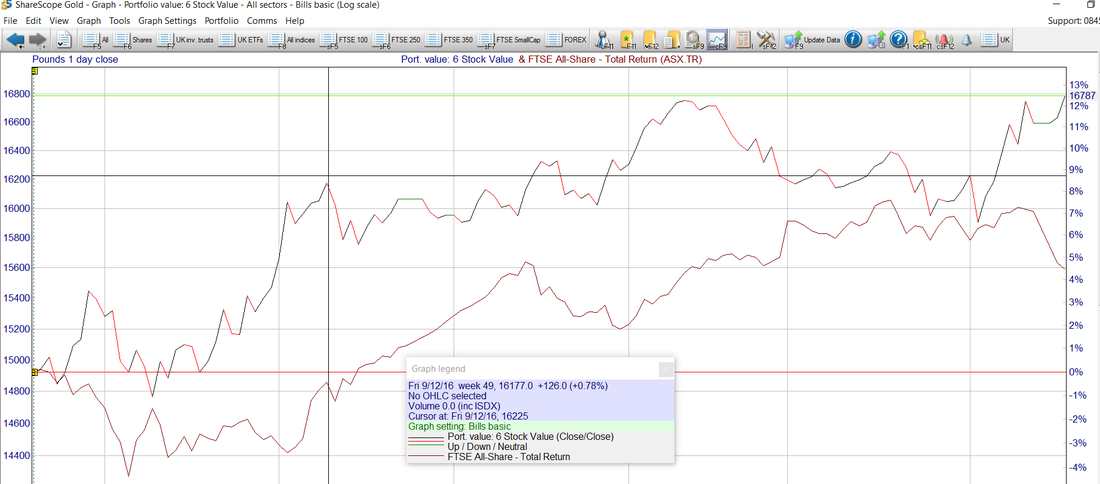

We have now reached the end of the fifth quarter of the Passive v Reactive Whittler portfolios so how are things going? The Tinker and ASH (annual sit on hands) had 8 stocks sold at the year-end review; see earlier blog of January 2017, to be replaced with 8 stocks identified from my investment universe. For clarity & to declare ownership: since the start of this Tinker series back in January 2016, a total of 18 stocks have been involved across the 3YL (leave it alone and don’t do anything for 3 years apart from reinvesting dividends), ASH & Tinker. All of these 18 stocks form or have formed part of my “best 10” portfolio and I still hold the majority of these 18 stocks and they form the backbone of my portfolio. The quarterly performance and dealing history, warts and all, is openly & honestly published within this Stockwhittler site. By way of a reminder, the ten original stocks common to the three portfolios and the eight replacement stocks identified in January 2017, come via my routine free cash flow+ returns on capital screen i.e. they all exist within my whittled down universe from which I make the majority of my share purchases. This universe shrinks the 2000 or so LSE shares down to about 40-50 for further really detailed appraisal: interim & final reports, all RNS news and particularly outlook statements. Within the rebalanced Tinker once the eight new stocks had been added following the sale of eight original stocks on 23/24-January 2017: In the Tinker and ASH out went Adept Telecom, Bodycote, Character Group, Dignity, Elementis, Hikma, Next Fifteen Communications & Persimmon. They were replaced with: Air Partner, Bioventix, D4t4, Galliford Try, ITV, Telford Homes, WH Smith & Zytronic. In Tinker portfolio terms I say out and replaced however, in terms of my actual investments, I continue to hold and indeed top up the majority of the 18 stocks discussed in this series to date. As mentioned previously in this series I am a great believer in the security of investing in a basket of stocks. Within that basket, you may well have a few outstanding stocks whose overall impact on the portfolio performance is somewhat diluted by other less well-performing stocks but conversely, a basket approach reduces risk when a couple of stocks are not heading in the desired direction. Now, of course, the rules I apply to this Whittler/Tinker exercise limit the ownership to my 10 best ideas as identified in January of a particular year and only in the Tinker can I manipulate the % on any of the 10 stocks in that portfolio in a 12 months period. Turning to the general concept of one’s entire portfolio i.e. stepping out of this 10 stock scenario for a moment is that many investors struggle with is the size of that basket and I usually run with a basket of around 30 stocks. You could argue that 30 stocks are a touch high and difficult to manage but personally using the systems that I operate, it’s a doddle. Yet I do feel that my overall performance which I must say I am generally happy with, could up a notch or two if I had the conviction to simply invest in my best 20 or even 10 ideas rather than the 30ish I usually manage. Having said that, I do ruthlessly and without emotion weed out stocks where it seems I did not get it right i.e. ones where the fundamentals for example or the story/original reason to buy no longer appears to be sound. Anyway, enough of this waffling on about the number of stocks within one’s portfolio, let’s see how the three ways of managing a portfolio discussed in this series, Tinker, ASH, 3YL, have performed by quarter 5 that’s 15 months since inception  I have also included tables from the excellent SharePad showing Tinker and 3YL: I reckon I must be one of Sharescope’s original customers many years ago and now am also hugely appreciative of the SharePad version   The performance of the 18 stocks across the Tinker, ASH & 3YL has been really very good since this series started with 10 stocks at £10,000 each back in January 2016. The Tinker is slightly ahead at 53.5% gain over this five quarter or 15 month period but really there is nothing significant to mark one portfolio out from another as the performance of all three strategies has been really very good. Thankfully the shares discussed here have been the backbone of the total portfolio I run and as such have contributed handsomely to my annual performance and I confess to being a happy investor.

Maybe we will see a more significant difference in performance within the three portfolios within the coming months but to my mind, all performance has been extremely good and too close to draw any significant conclusion as to portfolio management approach other than to again see that quality counts in investments. The comparisons with the returns that would have been made had we invested in the FTSE all share total return, FTSE ASX.TR are given in the tables SharePad below and as you can see the FTSE ASX.TR has been very significantly left behind by Tinker, ASH & 3YL but who knows what the future mat bring? After all the next profits “Oh no it’s a profits warning” or delightful “exceed market expectations” RNS may just be around the corner. Trading within the Tinker since 21/01/17 i.e. since rebalancing in January this year: well only one trade has taken place and that was on 3rd march 2017 when ½ of the WH Smith holding was sold and reinvested in that lovely high-quality stock Somero: I have to confess that I have held an appreciable quantity of SOM in my ISA since 2013. Not falling in love with a particular stock, but an appreciation of quality and backing a winner. As ever, anything produced here should not be taken as investment advice but rather a sharing of the whittling methods of a fellow investor trying to openly and honestly communicate the quest for reasonable returns from the stock market. Once again the rules of the exercise are reproduced below. Happy Investing! Appendix: The boring stuff! Reminder Of The exercise Rules. The three portfolios will be firstly a buy and hold for three years, ploughing on regardless through economic conditions, profit warning and any other news either good or bad. I will call this the three-year life portfolio (3YL). The only time a change to the portfolio will be permitted is if a business is de-listed for any reason: the funds liberated would then be discretionally invested between the remaining stocks in the portfolio. The second portfolio will start out with exactly the same holdings as the 3YL but each January the same cash flow screens/returns on assets screen will be run and a revised set of ten stocks nominated. This revised set of stocks will have the proceeds of the sale of the previous years stocks equally divided between them i.e after one year we have £110k of funds then a purchase of £11k will be made for each of the ten stocks. I will call this the annual sit on your hands portfolio (ASH). The third portfolio will again start the same as the 3YL & ASH portfolios but I will alter the percentage invested in each position within the portfolio in reaction to RNS announcements from the companies, economic conditions or any other reason that seem valid for altering, reducing or increasing a position. I will call this portfolio the managed annual tinker portfolio or simply the TINKER. All 10 stocks will remain within the portfolio throughout the year although the investment in each stock may vary. For example, one stock, let’s say Hattersville Dream Co. may issue a particularly bullish RNS “results will be appreciably ahead of market expectations”. The Tinker may sell down one or more of the other holdings to invest more in Hattersville but still retain a position, although not equal positions, in the same 10 stocks that we started within January each year. In January 2017, 2018 & 2019 this portfolio would be treated in the exact same way as the ASH and funds equally balanced across the each of the ten stocks starting that year. The common rules for all three portfolios: • Start January 2016 with the same 10 stocks each having £10k invested. • The basis of stock selection will be common to all purchases and in line with my usual investment principals based on strong cash flow, good returns on capital and sound financial health. • Dividends will be reinvested. • All three portfolios will be continuously fully invested in the relevant 10 shares. • The 3YL will not have any actions taken apart from dividend reinvestment and be left alone to prosper or otherwise over the three year period. • The ASH & Tinker will commence each January as fully invested in 10 stocks. However, the Tinker will have the discretion to rebalance the allocation of funds to one or more of the 10 stocks in the portfolio. • Transaction charges will be £5 per transaction with stamp duty deducted as relevant. • Dealing are now applied to the reinvestment of dividends as per iWEB costs.

0 Comments

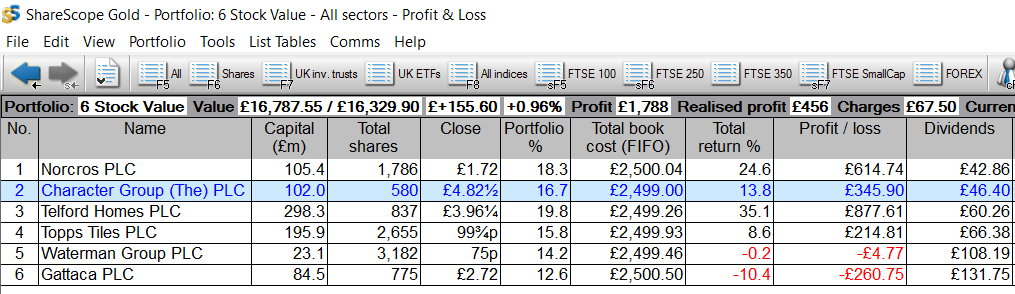

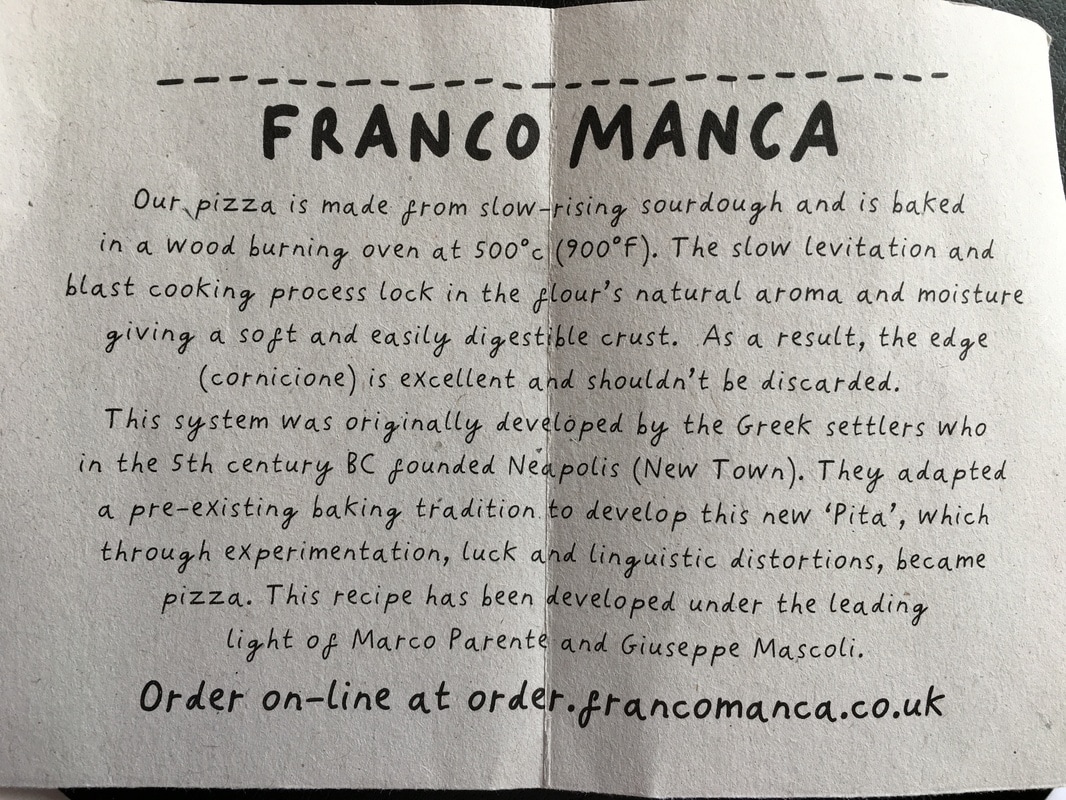

Just as a refresher; this article is the third and last in the brief series “Is The Stock Market For Matt”? Now my relative Matt, not his real name but as I said in part 1, I protect his anonymity buy calling him Matt simply because the silly so and so keeps a fair sized chunk of spare cash around the house under the mattress if you like; so he is Matt Tress. Anyway Matt has the usual bank accounts etc. but with interest rates as they are he feels why bother just leaving money in the bank as the current rate of return although risk free, is just so very poor. So six months back I sat down with Matt and devised a phantom portfolio where his spare £15000 would be invested in six value stocks paying tolerable to good dividends and in my judgement having an acceptable risk as the stocks are all lowly rated being a touch unloved but by and large sound businesses. Today six months after the start of this exercise, Matt still has his £15000 which has of course not gone anywhere apart from a little nibbling at the edges by that annoying little mouse called inflation. Let’s have a look at the performance of that £15000 had it been invested in equal £2500 amounts in the companies in the phantom portfolio whose dealings were sown in part 1 & part 2. Note I do need to say at this stage that at the time of construction of Matt’s phantom portfolio I held positions in all six companies; so walking the talk if you like such American expressions. The table below gives the progress Matt would have made over the six month period and it shows a total return of about 12% equal to an annual return of 24% and that includes £456 in dividends or as a %, 3% over the six month period. Had Matt invested that money in a bank he would have had a top end return of well under £100 over that six months. Had he invested in the FTSE All Share, which has performed quite well, he would have made around 4.5%; still fairly attractive. How does Matt feel about that tempting but definitely not guaranteed return? Well, to be honest he is impressed and slightly kicking himself for not taking the plunge but don’t kick yourself Matt, that’s life.  How does this compare to the FTSE AS Total return:  Now as I don’t give advice on share purchases, can you imagine the phone calls from Matt late at night if things go wrong, it’s really up to Matt to decide how to enter the world of stock market investing. He does not yet have what he feels is the expertise to select individual shares and certainly not the time to monitor RNS progress for companies yet he really wants to make a start. Matt than asks about these things called unit trusts and investment trusts and comments that I benchmark my portfolio performance against three of these, Fundsmith, Marlborough Special Situations and Henderson Smaller Companies Investment Trust. After a discussion about track record, the managers involved and fees, Matt decides that this is for him and will now invest £5000 in each of these three with a view to the long term and happily tells me that he will only look at progress monthly. Now with funds and investment trusts that is one bit of advice I was happy to give Matt as there is simply no point in looking more frequently and getting the negative or positive feeling as the funds move with each day. I can almost guarantee that the negative feeling of loss will outweigh the exhilaration of gain so why give yourself that pain? So in the end I feel quite comforted that Matt has decided to try and make his cash work for him and I am of the opinion that as long as he takes a long term view, say 5-10 years, he will do well. Strange you know, over the years I have made some of my best returns from attractive companies by simply sitting on my hand and doing little else but reinvesting the dividends. Happy investing Matt! As an investor it’s always nice to try the products from a company one invests in. The trouble is that I have little use in my daily life for the laser flat concrete from Somero, sheep monoclonal antibodies from Bioventix and certainly am not ready to personally sample the final drive services of Dignity. So in truth my chances to sample the quality of the service & products offered by the companies I invest in is down to the likes of Dart Group, WH Smith and a recent initial purchase in Fulham Shore who run the Franco Manca & Real Greek restaurants.  Now I should say that Fulham Shore is a fairly unlikely investment for me to even take a small initial holding in and that’s simply for the following reasons: The less good bits:

The bits that interest me:

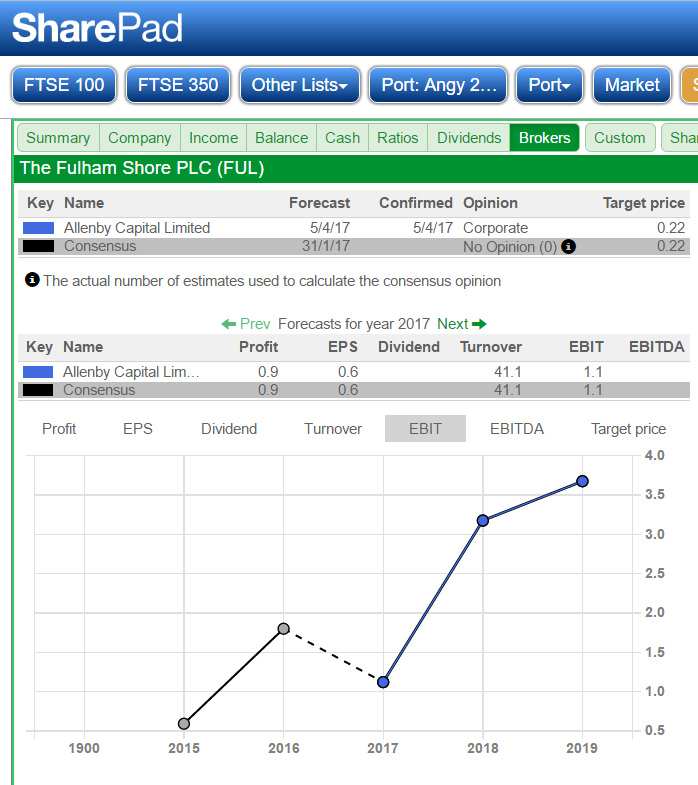

Now pizza itself is not my number one choice of food as I find the majority of high street offerings simply far too heavy with stodgy bases and well overdosed with tomato base. I do in fact make my own Australian pizza at home using a pizza stone. Why Australian? Well although I am a pretty decent in the kitchen, the round pizza shape escapes my skills and every pizza that sits on the stone resembles the map of Australia, sometimes even Tasmania can be seen. So after some late 2016 research, I took a small position in Fulham Shore in January this year fully appreciating the downside risk. As it happens, on Saturday my Hatters travels took me to London, we were playing Barnet, giving me a perfect opportunity to have lunch at the Tottenham Court Road Franco Manca. Yes, I know it’s nowhere near Barnet but who cares when you have a multi-zone travel card for the day: terrific value. I was impressed with my visit I have to say. The service was very good, a free jug of tap water in a recycled wine bottle delivered to your table on arrival. The drinks reasonably priced and the sourdough pizza one of the most impressive I have had; you could appreciate the taste of the fresh ingredients so rapidly cooked via their blast cooking process. Also, the staff were hugely impressive and appeared genuinely attentive. All in all a thoroughly enjoyable eating experience at very reasonable cost in the centre of London: two plate-sized pizzas, a glass of red and a glass of white with a bill of £25; can’t be bad. The broker view: data from SharePad:   Well, where do we go from here? In truth, it’s only a tiny % of my portfolio at well under 0.5% but it’s something I will keep an eye on and maybe add to as time progresses remembering that it’s a crowded marketplace and roll outs can by their nature become self-limiting in terms of growth.

Happy eating & happy investing. Investing in shares is not a love affair and to my mind, an investor has to evaluate not only when to make the purchase having completed your thorough research but also without emotion decide when it is time to leave. With some shares, this holding time can be very lengthy e.g. Somero, Bioventix, Dart Group which met my buy criteria in 2013,14 and continue to look attractive investments.

As I have mentioned in previous blogs my approach is to create a mini-universe of shares that qualify for consideration by virtue of attractive metrics such as free cash flow, returns on capital (CROIC and ROCE), increasing turnover, increasing profits etc. I should say that I also spend a fair amount of time pondering over what could go wrong with a business before I feel comfortable to make an investment. I don’t invest in anything that could be described as a blue sky stock: each company I invest in has to be a proven profitable business with real and not imaginary profits. As ever, I find myself building into winning positions as confidence in them gains: not the easiest of things for an investor to do “why should I pay £2.31 for something I paid £1.97 for a couple of months ago? My investments are for the bulk part held within a tax-free environment and I have been utilising PEPs and subsequently ISAs going back into the mid-1990’s. One thing I am certain about with investing, well at least with my outlook on life, is that in the early days of one’s investment journey you make many mistakes and you also have the odd wonderful year. In my experience the rates of return on small value portfolios, say under £100k, where you may have a greater appetite for risk as the potential loss is possibly not life changing in monetary terms, decreases markedly as your pot of dosh increases. The bigger the pot, the more risk averse one becomes. In terms of overall returns, your volatility tends to even out as you become comfortable with your investment approach, nurture the winners and ruthlessly jettison the stocks that don’t move in the desired direction. In general terms, once I “found myself” as an investor, I estimate that over a period of many years averaging out the good and bad years should with discipline yield in the range of 12-16% PA. Investment returns are not governed by magic tricks, they are dictated by a combination of individual company performance and the overall health of the market: fortunately the markets in 2016/17 were in pretty good health. In terms of performance measurement, I tend to go against the flow whereas most investors assess on a calendar year, I measure performance on a tax year. It seems sensible to me as that coincides with topping up the ISA pot and balancing CGT. The year 2016/17 was an unusual year with the FTSE all share total return taking a significant tumble at the end of June after the unexpected Brexit referendum result. We also had the unexpected result of the USA presidential election where a man who would need an annual review due to his age to retain employment in the UK took the most powerful job on the planet. Both results were unexpected and certainly not predicted by the well-paid commentators; who needs experts! So, onto the overall performance of the Whittler portfolio for the financial year 2016/17; the performance against my usual comparators are given below: Stock Whittler portfolio: +28.4% FTSE All Share TR: +23.8% Fundsmith Equity T Ac +24.4% Marlborough Spc Sit: +22.0% Henderson Sm Co’s IT +19.1% Overall the year 2016/17 was a good year to be investing even if on the end of June, post-referendum, it did not look that way. However, one can be easily misled into thinking that 2016/17 was a vintage year overall as it was Oil & Gas, Commodities, Miners & Banks that did all of the really hard work; these sectors between then averaged a gain of 77%. If you strip those sectors out then the gain for the FTSE all share fell to a more modest 13.6%. Now I rarely invest in any holes in the ground and after the financial crisis, I won’t touch banks with a bargepole so overall I am very happy indeed with a return of just over 28% from what I call proper companies that don’t live in the more speculative sectors. Now although I am delighted with that performance, I am ever mindful that the markets will at some time take a dip and at some time we will enter a bear market. I am also very mindful that the next profits warning for a stock within my portfolio may be just around the corner. The fact is that these events happen and the important thing is how you react to them. Note as I write the example portfolio I blog about the Tinker which is roughly my best 10 ideas taken as a modest initial investment of £100k is up 39.0% for the financial year 2016/17. Incidentally I will write up the 5th quarter’s performance at the end of April. I actually wonder if one day I will be brave enough to eventually just run with by best ideas in a concentrated portfolio of 10 stocks rather than the roughly 30 that I perpetually run with; I am sure that would be an even more productive way forward. Happy investing |

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed