As a private investor, we aren't unlike the crew of the Starship Enterprise. We are permitted to roam within the investment universe as we seek new gems that we may add to our investment portfolio. Unfortunately, that universe is a vastly big place and we are not naturally gifted at birth with the emotionless logic of Mr Spock that may enable him to find those investment gems more readily than a mere earthling. All too frequently investors latch onto some of the space-junk that drifts in the vacuum of space. Many private investors that journey in the investment universe take a random journey as they bounce from one idea to another, from hot tip to hot tip, from chaotic bulletin board "in the know tart" to the next hot thing suggested by part-time journalists.

Now that universe is a difficult place to travel, so how can we make that journey a little less random and improve our chances of beating the FTSE index? I suspect that the majority of private investors, especially inexperienced investors, invest to some degree with a random approach, selecting stocks that sound the real thing! Sometimes this random approach works, sometimes it fails as I found out many years ago in my early days as a PI. The approach I adopted some years ago is to shrink that universe greatly; in fact creating my own universe of stocks; hopefully, a universe that I may continue to feel comfortable with and understand. A good number of investors take this universe approach by becoming specialised in such sectors as utilities, oil stocks etc and carry out the bulk of their trading within their chosen specialist area. Others may develop an understanding of value stocks, growth stocks or hitch a ride on momentum etc. The common thread is that they understood their universe and severely limited their diversions to random space walks that invariably lost them money. My Approach: The Whittler Universe: Well, firstly absolutely no jam tomorrow stocks, bulletin board stocks or following of tipsters in any way: been there, done that many years ago and learnt the lessons. My investment universe is very heavily biased to stocks that are already displaying the characteristics of winners. I screen entire listing of LSE stocks for shares that includes AIM, to come up with a relatively small number of stocks that meet the rather demanding criteria that I apply for universe membership. The criteria I apply are all linked to returns on capital (ROCE & CROCI) & cash-flow, particularly free cash-flow; I also treat debt with real caution. I don’t like to overpay for stocks but have more faith in cash-flow valuations, cash profits valuations than I have on the PE ratio although I do tend to set an upper limit on the PE when screening. After each screening, I tend to end up with about 20-25 stocks and it’s surprising that over a given period the numbers of stocks that reappear month after month. In fact looking back over the past five years, only a total of ninety five stocks have entered my universe via my screening. Do I invest in all of these stocks? No, firstly I keep a very close eye on the recent and current company RNS particularly outlook statements. I look to see if there is anything obvious lurking in the numbers that may suggest that the story I originally perceive is not the true one. I then take a view on the strength/current favourability of the sector; then I apply some very simple TA; where does the price sit to the 200 day MA, recent trends etc. Finally, if I am still comfortable and I see the stock as being available at a fair value, I buy. My approach will never identify the Gulf Keystones of this world, thankfully, it will also miss many, many high flyers but it is a universe approach that I feel comfortable with and certainly gives me the edge over beating the FTSE All Share index. Do all of these stocks go on to increase in value? Well, no, of course, they don’t otherwise an infinite way of legally printing money could be claimed. The majority do go on to increase in share price but some are inevitably the victims of changes in market sentiment, sector downturn or falling behind market expectations. My particular application of screening tends to create a universe of fairly boring stocks. Over the past 5 years the unexciting large caps such as GVC, SMWH, NXT, ITV along with smaller caps stocks such as XPP, NFC, ZYT, CCT & DTG. I have mentioned that over the last five years that ninety-five shares have entered the universe for further appraisal and roughly one-third of that number have then been bought/sold or continue to hold. There are another couple of parts to my universe but these are a touch smaller and close to Jim Slater’s Zulu principle followed by a splattering on stocks that I see as undervalued. The real point I am trying to get over in this article is that to improve one’s chances of success, in my experience, it helps greatly if you have a fairly large portion of your investment portfolio made up from a universe of shares that meet your criteria. A universe of shares whose fundamentals you both understand and whose degree of risk you feel comfortable with. The sources of data I use for screening for my universe are: SharePad Sharescope Sharelockholmes I then seek data for confirmation from Stockopedia and RNS data from Investegate or the company's web site. Happy Investing!

0 Comments

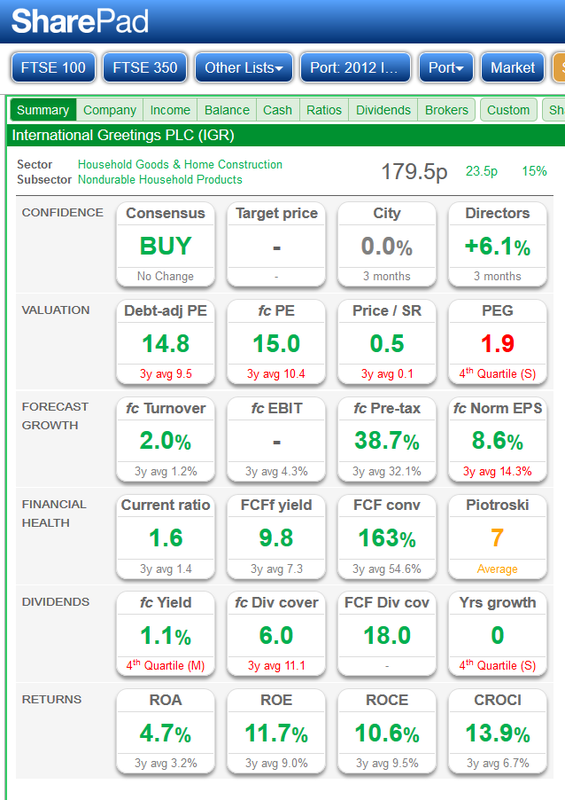

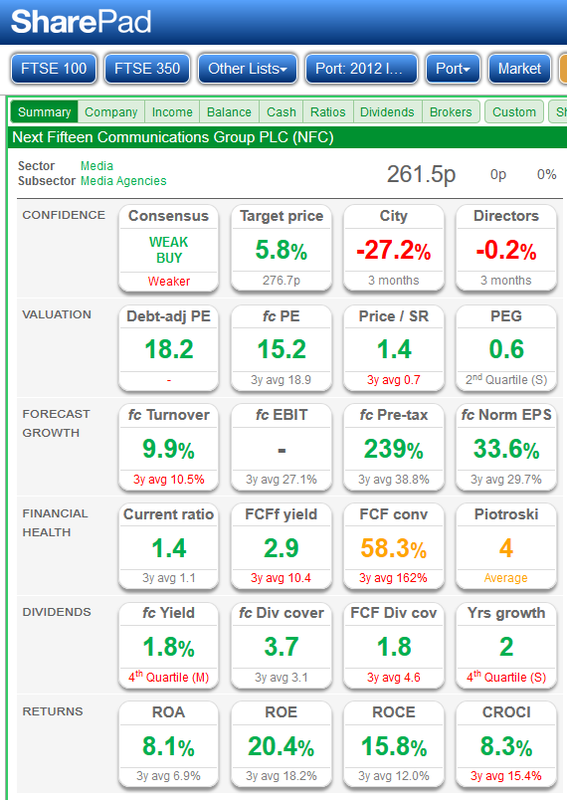

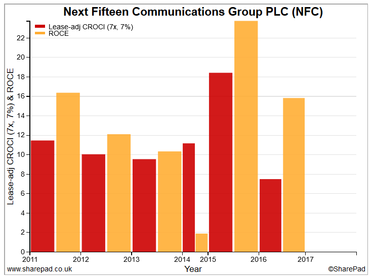

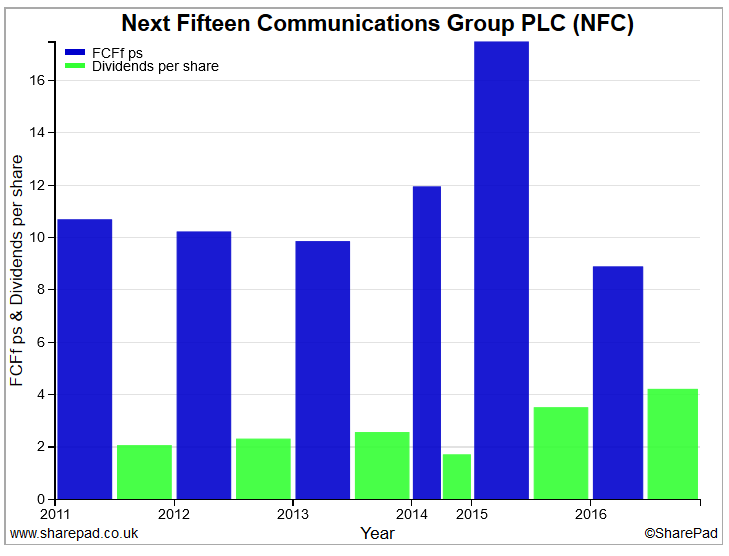

International Greetings issued a trading update in relation to the 12 months ended 31 March 2016. The Trading Update Reads: Financial performance is ahead of expectations, resulting in a further year of double digit earnings per share growth Operational cashflow and debt reduction continues to reduce leverage significantly ahead of expectations. Property held available for sale at Aberbargoed in Wales was sold with proceeds of £1.45m received on 31 March 2016 The strength of our performance and resultant cash generation underpins the payment of a final dividend for FY16 ahead of market expectations. The Company intends to pay a final dividend of 1.75p, resulting in an overall full year dividend of 2.5p (FY15: 1.0p) The Group is delighted to confirm that all regions have delivered year on year growth and an overall outcome ahead of market expectations. In the UK and China, record sales combined with an excellent manufacturing performance has delivered profitability ahead of forecast. In Continental Europe, sales growth and effective management of mix have successfully mitigated anticipated foreign exchange transaction headwinds. Trading in the second half of the year in Australia has resulted in significantly enhanced overall total profitability. In the USA, the commercial, operational and financial performance of our business has been extremely encouraging. This has included the successful implementation of phase 2 of our programme of fast payback investment in manufacturing. This investment will accelerate and enhance our capability to profitably grow our share in the world's single largest market. Commenting on the year's performance, Paul Fineman, Group CEO, said: "It is especially pleasing that we can report profits growth throughout all regions of the Group. This is a particularly exciting stage of our development in which we remain well positioned for organic growth and continue to seek compelling acquisition opportunities. Our culture of continuous improvement and our focus on creating commercially successful designs and products delivers a winning combination for our customers and trading partners. We are delighted to be meeting our core objectives of growth in underlying EPS and dividends whilst reducing average leverage all ahead of schedule." My View It’s always nice to see such a very positive trading update especially one which shows all areas of the business progressing well. I also like the large proposed increase in the dividend moving to 2.5p from 1.0p last year: whilst not a massive dividend, the increase does show confidence. I would expect some revision upwards of broker’s estimates and hopefully a further life to the share price. Although I don’t tend to select shares solely by either the Stock Rank of Stockopedia or Market rank equivalent of Sharelockholmes, I do tend to look to see what they score for my holdings. IGR reassuringly has a Stockopedia Rank of 93 and a Market Rank of 4 (equivalent to 96 when compared to the Stockopedia rating). Happy to hold!  Sprue Aegis provide a trading update today, 18th April 2016, that did come as a bit of a surprise and to be honest, it just left me feeling very uncomfortable about the company. My Thoughts Firstly the battery defect whilst probably not life threatening in terms of the functioning of an alarm, to my mind it could seriously dent confidence in the products from SPRP. If SPRP deal very professionally with the rectifying the problem, then given time, reputation should recover. There is a certain amount of forgiveness in the market once a company identifies an issue and then applies first class customer care: we will have to see. I am not overly impressed with the “third party supplier” handle as the batteries in SPRP product; it’s down to them to make sure the components used are fit for purpose. The trading statement then goes on to say: Challenging trading conditions in France, principally due to overstocking, and weaker sales in Germany, due to product certification delays, are likely to significantly adversely impact the Group's expected results for this year. Consequently, the Board has revised its guidance for the full year 2016. Subject to no major changes in exchange rates, the Board now expects a first half operating loss* of approximately £1.9m (which includes a restructuring charge of £0.2m as a result of reducing certain fixed overheads), and an operating profit* in the second half of approximately £3.8m with sales and operating profit* in the full year of approximately £55.0m and £1.9m respectively. The estimated saving in 2017 from the fixed cost reduction is approximately £0.8m. Graham Whitworth, Executive Chairman of Sprue, said: "Unfortunately, overstocking in France and weaker sales into Germany, have resulted in us issuing revised guidance for this year. We expect to rebuild trading momentum in the second half of 2016 with certified new products and enter 2017 with normal levels of trading. In my view, that does raise a question regarding management really having their finger on the pulse in terms of both their suppliers and their customers. So putting all of that together shortly after the RNS came out, I decided to sell the relatively small holding I have/had, about 1.5% of the portfolio. It’s fairly standard for me to sell on a profits warning and I managed to get a sell away with iWEB on an at best deal first thing this morning. Also swiftly looking at projections, and my criteria for investing, the case for continued ownership based on my investment principals’ was destroyed. After this morning fall, we now have a business with a market cap of around £65m, a projected operating profit, from the RNS, of £1.9m. At the time of writing the SP had fallen to about 155p; just my opinion but I feel it could have further to fall on what I see as overall confidence issues and revised valuation. I don’t normally like dealing blind like that and fully expected to see a sale price in the order of 130-140p; I was very happy to see that I actually got 185p. This sort of thing can happen with relatively small companies especially ones on AIM; it comes with the territory, so no moaning from me. So it's onto the wood-burner for SPRP, although hopefully without too much smoke as I can just hear a low battery bleeping! It’s time I gave an update on portfolio activity in the last few days. There have been three new additions to the portfolio and one top up of a current winner. The new additions include two purchases identified my cash is king screen/free cash flow screen (CashKi.FC, not a third division Polish football club but a screen I regularly use to identify companies with good free cash flow and good returns on capital). The new additions are Next Fifteen Communications (NFC) and XP Power (XPP). One purchase of a fairly boring buy steady consultancy, Waterman Group (WTM) and finally a top-up of a current holding in Portmeirion Group (PMP). NOTE: I am moving to use a financial dash board as per SharePad on my blog notes when discussing share purchases and sales. For those who do not use SharePad, I can only suggest that you give it a try: a totally superb tool in my opinion. Next Fifteen Communications: Market Cap. £189m NFC previously held and allowed myself to get bumped out by the “noise of experts”; quite silly really, you listen to the noise, ignore the numbers and the genuine news and before you know it you have hit the sell button. When I sold NFC I had made a 90% total return in 12 months but the fear of losing some profits combined with that dreaded noise resulted in the sell button being pressed. Had I done the sensible thing and just let the trailing stop loss do its work, I would have made a gain of around 220% for just holding for another 18 months. A strange part of investor psychology is that it can be very difficult for an investor to convince themselves to go back and buy a share that they have previously sold at a lower price having taken a profit; just the way we are wired I guess! Anyway, my CashKi.FC screen kept showing NFC and in addition, I was impressed with the finals for NFC delivered on the 12th April; summary below. Final Results of 12th April 2016 Highlights:

Current trading and Outlook Looking ahead, the Group has made a good start to the new financial year with trading patterns continuing as in the second half of our last fiscal year. The Group has made two further acquisitions in the UK of Publitek, a specialist content agency, and Twogether, a technology-focused digital agency. My View So there we are, a purchase that as with most of my purchases will not be looking to generate a fast buck. I will use an initial 20% stop loss on ShareScope but manually execute if applicable. Price target? Well, I will set a target of 20% TR and review if we get to that level. Oh, for good measure a fairly decent Stock Rank of 78 on Stockopedia and a value of 18, equivalent to 82, on Sharelockholmes: with Stockopedia 100 is best and it’s reversed on Sharelockholmes with the lower figure being the best. The financial summary looks attractive, the returns on capital CROCI/ROCE are attractive and the dividend is well covered by FCFfps.

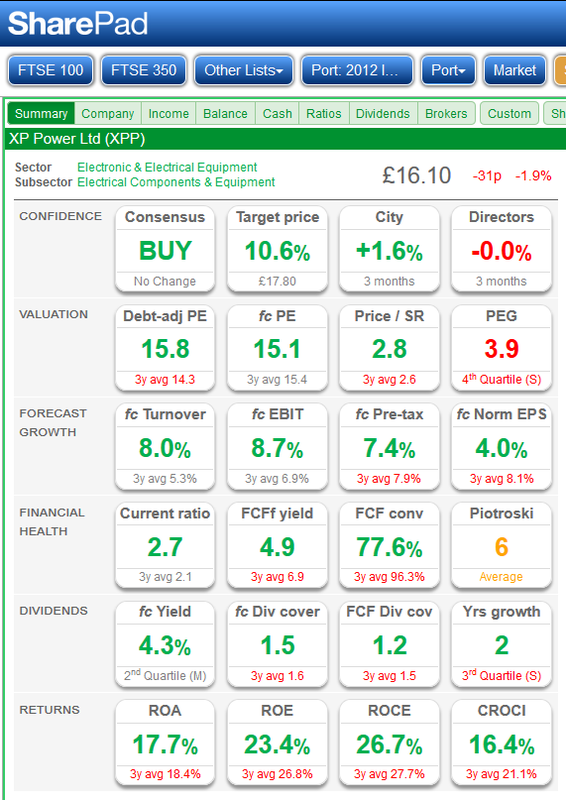

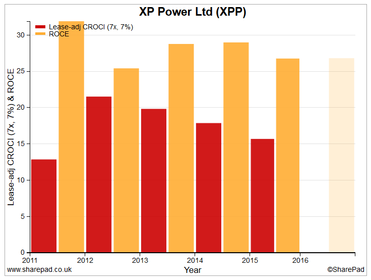

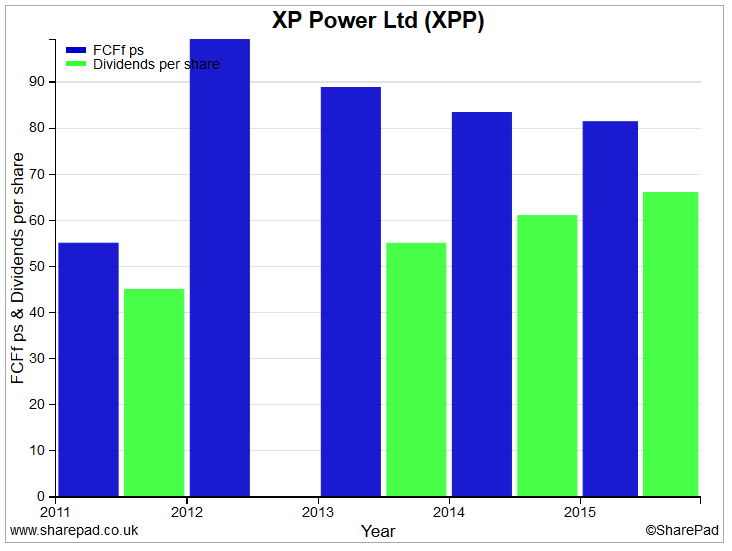

XP Power: Market Cap. £310m Another share that came through my CashKi.FC screen is XP Power. It’s not a share I have owned before but it’s attractive enough for me to make a purchase. They produced their most recent finals on 22nd February and whilst not stunning, they were solid.

Outlook We are encouraged by the stronger order intake experienced in the fourth quarter of 2015 following the weakness we saw in the North American order intake in the third quarter and by the progress of the integration of EMCO. Despite the mixed global economic picture, we have positive momentum and therefore expect further growth in revenues in 2016. We now have a high voltage product offering, which we believe we can grow using our direct sales channel and approved supplier status with our existing customer base. We also have a strong balance sheet and a business model that provides excellent cash generation to fund our existing needs and targeted acquisitions to further broaden our product offering and engineering capabilities. Trading Update 11th April 2016 Trading in the first quarter has been strong. Group revenues in the three months to 31 March 2016 were 28.2 million (2015: 25.6 million) up 10% from those achieved in the same period a year ago. In constant currency, revenues were up 6%. My View I am attracted by the financials, excellent free cash flow and the prospects for steady growth in profits. For good measure, Stockopedia have a Stock Rank of 94 whilst on Sharelockholmes they have a value of 3 which is 97 in Stockopedia terms (with Stockopedia 100 is best and it’s reversed on Sharelockholmes with the lower figure being the best). The financial summary looks attractive, the returns on capital CROCI/ROCE are attractive and the dividend is well covered by FCFfps.

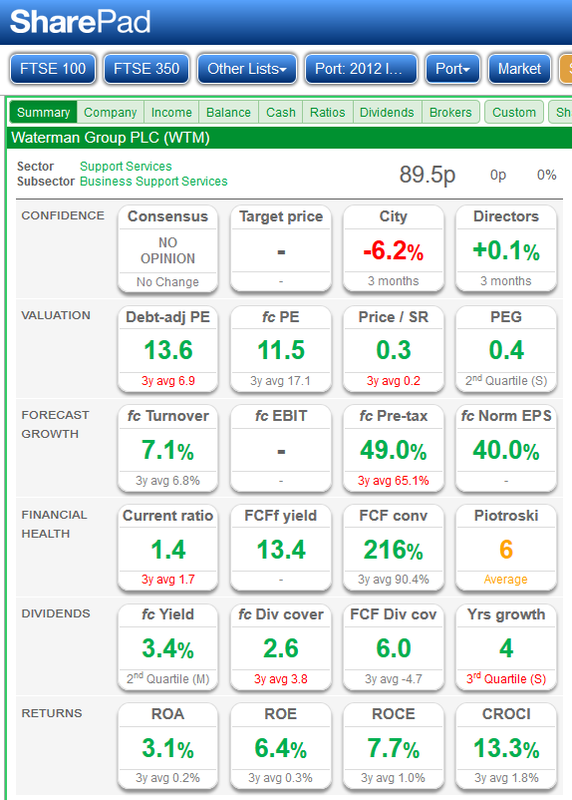

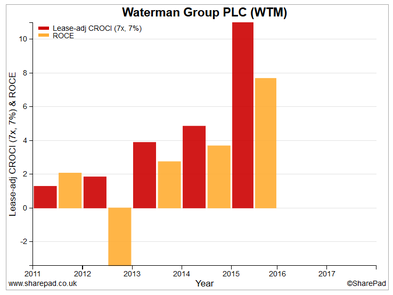

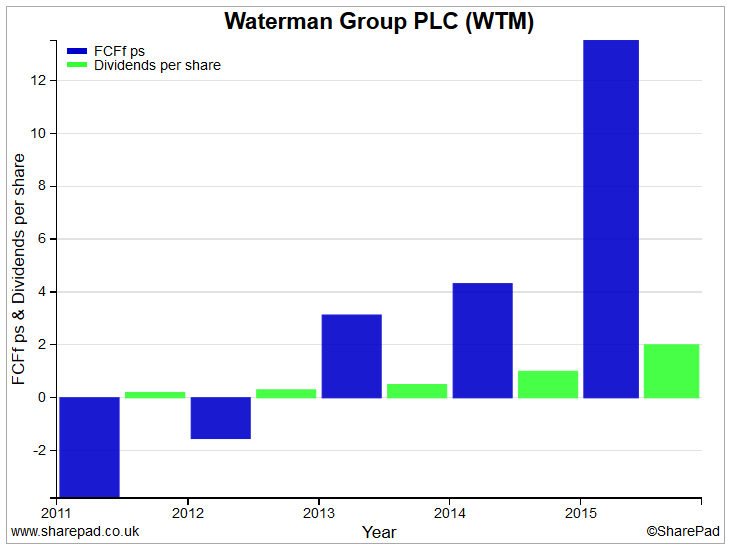

Waterman Group: Market Cap. £27m This one is a fairly boring consultancy group. The Company, through its subsidiaries, is engaged in the provision of design services and advice in the fields of civil, structural, mechanical and electrical engineering together with environmental and health and safety consultancy. All fairly unexciting stuff but somebody has to do it and also make money at the same time. In truth, they are a touch on the small side for me with a market cap of around £28m. They don’t have any debt and after a fairly lean 2010 to 2012, their operating profits have been climbing nicely resulting in net profit in 2015, decent projections in both the current FY and next FY. The business is cyclical by nature and not very high margin. Heavens, I am almost convincing myself to sell it as I read the text I am typing! No, seriously I do feel there is scope for some SP appreciation and they also carry a fairly decent yield at over 4%. However, the most interesting part sits in the outlook statement below with target increases in PBT, ROCE, and operating margin. Highlights Interim results of 29th February 2016 6 months to 31 December 2015

Outlook Waterman is on target to exceed its previously declared financial objectives to triple adjusted annual profits before tax to £3.3m over the three year period to 30 June 2016, with a return on capital employed (ROCE) of 20%. In October 2015, the Board announced a new aspiration to increase the Group adjusted operating profit margin to 6.0% by June 2019. As noted above, the Group's progress against this objective is positive with adjusted operating margins increasing from 3.3% to 4.1% over the last twelve months. The Board expects further progress to be made during the second half of the current financial year and beyond. The results have benefitted from the Board's strategy of focusing primarily on the UK, where 90% of Waterman's revenue is now generated and this focus is anticipated to continue for the foreseeable future. Waterman's long-standing relationships with blue chip companies continue to generate repeat business year on year and the Board expects this to continue whilst the UK economy is strong. The Board looks to the future with confidence. My View I quite like the business and whilst not wanting too many of it’s type in my portfolio, I feel comfortable enough to have bought a reasonable but not large holding in terms of % of my portfolio. For good measure, Stockopedia have a Stock Rank of 99 whilst on Sharelockholmes, they have a value of 4 which is 96 in Stockopedia terms (with Stockopedia 100 is best and it’s reversed on Sharelockholmes with the lower figure being the best).

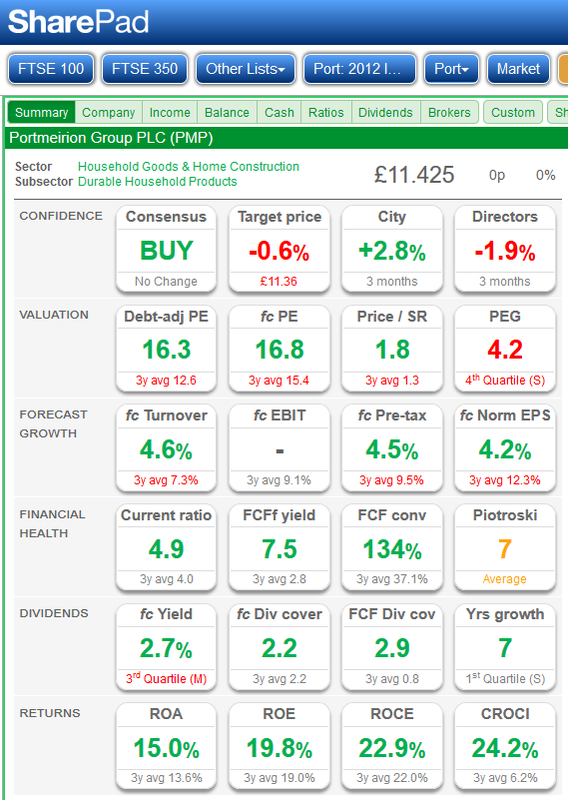

Portmeirion: A Top-Up: Market Cap. £130m Simply another top up of a current holding that has already given me an increase of 80% since my original purchase two years ago. A nice boring, unexciting company with steadily rising revenue and associated profits and offering a yield of just under 3%.  Happy investing!

Financial Year End

At the end of each financial year, I carry out a number of administrative tasks on my investment portfolio. They include all the usual bits and pieces such as a final check on the CGT position to ensure the maximum allowance has been gained for the financial year. In truth, this FY the CGT was sorted a couple of months back. Another task I carry out is having a look at the performance of my overall portfolio over the FY, not so much to gloat or kick myself but just to see how things are progressing. What have I learned during the year, what could I with ease have done better etc. Firstly performance: I measure my performance against the traditional FTSE All Share Total Return FTSE ASX.TR and then throw in two or three more challenging benchmarks in the form of two funds, Fundsmith & Marlborough Special Situations along with the well respected Henderson Small companies trust. My desire is to beat as many of my benchmarks as I can; If I can’t then there is a reasonable argument that I may as well just hand over my money to one of the above mentioned and spend a bit more time doing other things. A fine argument possibly but in truth, I do enjoy investing. So how do the figures stack up for the financial year 2015/16: Stock Whittler portfolio: +11.9% FTSE All Share TR: -6.1% Fundsmith Equity T Ac +18.9% Marlborough Spc Sit: +13.5% Henderson Sm Co’s IT -0.5% So overall not too bad although yet again a massive congratulatory applause to Terry Smith for the excellent performance of his Fundsmith T Acc which had a superb performance during the second half of the FY at a time when many investors portfolios, including my own, stuttered as worries over angry bears and a Chinese slowdown gripped the market. The major work for the portfolio was done by the likes of Dart, Cambria Auto, Dixon Carphone, Berkeley, Tristel, Topps Tiles and Bioventix. Of course, some investments which on paper looked decent at the time of purchase did not do so well but happily I remained unemotional forming no attachment with the shares and stop losses were actioned. Moving Forward Into 2016/17 Well, I will not be greedy in the sense that I will not chase jam tomorrow shares: I will continue to work within my universe of stocks that generate lots of cash, have either no debt or at least acceptable levels of debt and make a good return on capital employed. What will I try to do better in 2016/17? Well that’s fairly easy to answer in that I must really add to winners more than I have done in the past. I do top up on the better ones but there is always some reluctance or mental hurdle that I have to overcome in paying substantially more for a stock that a purchased a few months before for much less: strange but that’s my little battle. Conversely, I will continue to dispose of any stock that hits my stop-loss trigger. I do suspect that the first three months of 2016/17 will be somewhat difficult and I feel the markets will be twitchy ahead of the Brexit referendum on June the 23rd but I rather suspect that whatever the result of the referendum, we may see a rally for a little while at the end of June and hopefully continuing over the summer. Changes in taxation, of course come into effect during 2016/17. These changes include the taxation on interest on bank/building society accounts which will enable me to receive £500 tax-free but get clobbered with 40% tax on the remainder. Also, we have the introduction of the £5,000 per year allowance for tax-free dividends on shares held outside of a tax-fee wrapper. This appears nice but does have the sting in the tails of 32.5% taxation on all dividends above this amount. To help marginally mitigate these tax concerns I have already today used my 2016/17 ISA allowance with my broker and I look forward to next year when the ISA contribution increases to £20,000. In terms of success this year, I would be happy with any appreciation over 5% but we will have to wait and see as the FTSE has been on a slow grind downwards since April 2015 but has at least stabilised a touch in March and April 2016 As ever, happy investing. |

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed