What The Company Does: Trakm8 is a major provider of Telematics Solutions to a variety of customers that operate within three discrete business sectors to cater for all telematics requirements. By providing innovative solutions to suit different customer needs, Trakm8 are at the cutting edge of telematics design. Telematics hardware for Distributors, Integrators and ASP’s Trakm8 have market leading hardware devices that can be integrated into 3rd party telematics or Internet of Things (loT) solutions. These devices can be split into four product lines:

Trakm8 are market leaders in safety black box camera recording systems utilising the smallest and most rugged 1080p cameras on the market today. Cameras are being increasingly used in a wide range of applications, including a significant demand for forward facing vehicle cameras to record driving incidents and to mitigate the risk from ‘crash for cash’ accidents. Video data is increasingly used to monitor behaviour and to replay outcomes. The increase in the richness of the data generated by our telematics solutions will continue to provide the very best solutions within the telematics industry, making Trakm8 the number one choice. Engineering Services Trakm8 undertakes a wide range of customer specific development projects to assist the integration of telematics and all derived data into a customer’s management system. No job is considered too large or too small, and Trakm8 have a multi-disciplinary engineering team which is equipped to address most challenges Recent News: Outlook half Year Report 23/11/2015 The Group believes that we will continue to successfully execute our outlined strategy and as a consequence deliver growth in shareholder value. The second halves of our financial years have consistently shown increasing revenues including service revenues over the first half. This year we expect that this will be true again. This, along with a full period effect of DCS, means that we expect second half of the year revenues will be considerably ahead of the first six months. At the time of our Final Results in July we indicated that we expected to modestly exceed the market's then current expectations. The Board is now confident that the results for the year ending 31st March 2016 will again modestly exceed the market's current expectations. Proposed acquisition of Route Monkey Holdings Limited and £6 million placing 21/12/15 Adds fleet routing optimisation capability The Acquisition will be funded through a combination of a drawdown of new Trakm8 debt facilities, a placing of 1,801,802 new ordinary shares of one pence each in the Company ("Ordinary Shares") ("Placing Shares") at a price of 333 pence per Placing Share (the "Issue Price") to raise £6 million (the "Placing") and 184,441 new Ordinary Shares being issued as part of the consideration to the senior management shareholders of Route Monkey ("Consideration Shares"). The Placing with new and existing institutional investors, conducted by finnCap, was oversubscribed. The Placing adds new blue-chip institutions to the share register. The Acquisition is expected to complete ("Completion") on admission of the Placing Shares to trading on AIM ("Admission"). The Acquisition is in line with Trakm8's strategy of augmenting its organic growth with selective acquisitions that expand its telematics offering to both insurance and fleet customers. The Acquisition is expected to be immediately earnings enhancing. Est date of next trading update or results announcement: Probably April 2016 if same as 2015 Broker View @ Time Of Purchase Why I Like The Business: The business first seriously came to my attention following the half-year results in November 2015 and then after the oversubscribed placing for the Route Monkey acquisition in December 2015. The placing was at 333p and at the time I was caught in two minds i.e. expensive but excellent growth prospects V full take up at 333p by institutions. Luckily the share price fall caused by the so called bear-raid and the general market fall made me decide to put on hold any investment. The “grey areas” of concern have to my mind been very well laid to rest by the excellent interview with John Watkins, Exec Chairman by Paul Scott in the last couple of days. I should add that I was very fortunate, or should I say may have been very fortunate, to buy at close to a low today. Of course I may have bought early but I will have to wait and see. Turnover & Profit trend are very impressive and hence the mid-December highly rating of the shares. Whittling About the Numbers PE(f): this stood at about 24 in mid-December but has now fallen a PE(f) of 14 as the share price has drifted back on the recent accounting concerns ROCE: 18% Margin: 10-11% cps/eps; I am comfortable with cps being higher than eps; something I look for when making a purchase. Yield: no dividends are paid as yet as the company reinvests funds to grow the business at this stage. FCF cover of dividend: although no dividend is paid and funds are reinvested, the FCF over recent years suggests that when the growth phase slows down there should be cash available to pay dividends; maybe something for the future. Debt: does not appear to be an issue. Pension Deficit: none Current ratio: 1.5 Piotroski: 6 Stockopedia and 5 on SharePad Risks: as ever some competition risk plus possibly some selling by institutions who may want to offload shares bought at the placing price of 333p as the SP increases. Initial price target/Review: I have set this at 260p Stop Loss: I will set this at 170p due to risk around current market sentiment; a bit more generous on the low side than usual. It’s not a massive position but one I may add to if the overall market conditions don’t deteriorate overly in the coming months and of course if RNS announcements remain positive. Chart:

0 Comments

Forward Note: The following monologue concerns the investing of a notional £100k in a portfolio of stocks that pass through one of my free-cash flow/return on capital screens: three approaches to the management of the portfolio are detailed. An obvious question is “would I be investing a further £100k in the markets as they stand in January 2016”? The answer is a definite no, not at the moment and in fact I have been taking profit in many of my positions in the last month to manage risk in the uncertain market of January 2016. At the time of writing I stand at 65% cash in my portfolio. Therefore please consider the following notes as an exercise in managing a portfolio rather than “this is what I am going to do today to invest and make a return”. For a while now I have been fascinated by the discussion of the merits or lack of merits associated with continually trading within a portfolio. Some respected and famous investors feel that once quality companies have been identified the preferred approach is to sit on ones hands and let the quality business simply grow with time; in effect leaving things alone trading wise. This, of course, goes somewhat against our nature as investors as we always seem to be looking to tinker and “make things better”. Personally, I am not one for over tinkering and usually hold my stock purchases for around one to three years, reinvest the dividends and add to profitable positions. However, I thought it would be informative to apply my typical whittling methodology to a group of ten stocks and from these ten stocks form three portfolios that will be initially the same at day 1 but change over the period of monitoring which will be three years. The three portfolios will be firstly a buy and hold for three years, ploughing on regardless through economic conditions, profit warning and any other news either good or bad. I will call this the three year life portfolio (3YL). The only time a change to the portfolio will be permitted is if a business is de-listed for any reason: the funds liberated would then be discretionally invested between the remaining stocks in the portfolio. The second portfolio will start out with exactly the same holdings as the 3YL but each January the same cash flow screens/returns on assets screen will be run and a revised set of ten stocks nominated. This revised set of stocks will have the proceeds of the sale of the previous years stocks equally divided between them i.e after one year we have £110k of funds then a purchase of £11k will be made for each of the ten stocks. I will call this the annual sit on your hands portfolio (ASH). The third portfolio will again start the same as the 3YL & ASH portfolios but I will alter the percentage invested in each position within the portfolio in reaction to RNS announcements from the companies, economic conditions or any other reason that seem valid for altering, reducing or increasing a position. I will call this portfolio the managed annual tinker portfolio or simply the TINKER. All 10 stocks will remain within the portfolio throughout the year although the investment in each stock may vary. For example one stock, let’s say Hattersville Dream Co. may issue a particularly bullish RNS “results will be appreciably ahead of market expectations”. The Tinker may sell down one or more of the other holdings to invest more in Hattersville but still retain a position, although not equal positions, in the same 10 stocks that we started within January each year. In January 2017, 2018 & 2019 this portfolio would be treated in the exact same way as the ASH and funds equally balanced across the each of the ten stocks starting that year. The common rules for all three portfolios:

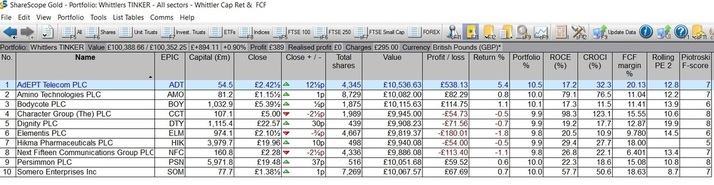

The ten stocks I have selected and invested a notional £10k into each one at the start of business on Monday 25th January 2016 are: Adept Telecom: Mkt Cap £54m Amino Tech: Mkt Cap £81m Bodycote: Mkt Cap £1032m Character Group: Mkt Cap £107m Dignity: Mkt Cap £1115m Elementis: Mkt Cap £974m Hikma Pharma: Mkt Cap £3979m Next Fifteen Communications: Mkt Cap £160m Persimmon: Mkt Cap £5972m Somero Enterprises: Mkt Cap £77m The stocks are shown in the above ShareScope portfolio invested: invested at market open on Monday 25th January 2016; the prices above are end of day prices. The stocks give a reasonable diversification across sectors. I have deliberately made a decision to exclude any stocks below £50m market cap and also deliberately selected half of the stocks to either FTSE 100 for FTSE 250 companies. I will keep the blog up to date with variations in the Tinker portfolio as allocation changes are made and the specific reasons for that change in allocation. I will also issue quarterly progress notes for all of the portfolios. At the time of writing I hold positions in two of the ten companies: Character & Somero. After three years I wonder which portfolio will come out on top? A bear market: Whittler’s definition: a bear market is where good news gets you a slap, no news gets you a kick and bad news gets you carted off to A&E.

After the very fruitful years of 2013, 2014 & 2015 when plenty of gains were made, we have found ourselves in the uncertainty of early 2016 where a number of issues are having a negative effect on market sentiment. Possibly the greatest fear at the moment is the slowdown in China; do we believe the Chinese projections, are they credible or indeed are they known and understood? Well over the years I have developed a philosophy that focused on only worrying about the things that I can control whilst at the same time making the best of the aspects of my environment/world that I cannot control.

Well, that’s the Rab C. Nesbitt philosopher bit done; so practically how do I intend to act until the markets sort themselves out and for sure at the time of writing, I don’t know when that may be. Do we have a correction, a serious correction or a bear market? Who knows and for sure there will be many experts with an opinion that at some time in the future will be crowing about how right they were etc. My view at the moment is that there is a serious risk to some considerable gains that I have accumulated over recent years; seems obvious really given that the FTSE has fallen from a high of 7100 at the end of April 2015 to the value at the time of writing, 5673; a pretty decent 20% fall but maybe that’s being a touch over dramatic. What we do know is that the FTSE 200 day MA has taken a prolonged downward path since mid-August 2015 and we probably have not seen that sort of thing since the second half of 2011. Additionally we have had the Chinese worries during August giving a 12% fall, an early December 9% fall followed by a touch of recovery and now a 10% drop since the end of December 2015. I can’t control that stuff and, therefore, try not to waste mental energy worrying about something I have absolutely no influence over. What can I control? Well as a private investor I can control the positions I have open in the market. Firstly I have to take a view on what might happen with the markets over coming weeks, what the risk may be and how I may wish to mitigate that risk. My view currently is that there is a very real risk to my accumulated stock market dosh and, therefore, I have taken steps to mitigate that risk. The steps are:

The net effect of all of the above is that I now have in excess of a 55% cash position in my ISA and non-ISA trading accounts. Whether this is wise or not is fairly immaterial to me, what is material is the fact that I feel comfortable with this position at the moment and I really look forward to when the markets have sorted themselves out and possibly the nasty bear has gone back into hibernation. I will then have a very healthy pile of cash to hopefully invest in an appreciating market. In my view, it’s all about doing what you as an investor feel comfortable with and in my case it’s about the mitigation of risk and keeping my powder or, at least, a healthy amount of it, dry for another day. Happy investing; well hopefully! A recent top up of a current holding has been Somero. Somero produces laser-guided equipment that automates the process of spreading and levelling volumes of concrete for commercial flooring and other horizontal surfaces. An extract from their 7th January 2016 trading update is shown below: In the six months since 30 June 2015, the Company performed strongly, particularly in the final quarter with monthly sales at an all-time high in December, which is not traditionally the strongest month of the year. As a result, the Board is pleased to announce that the Company now expects to report Revenue ahead of current market expectations for the full year. Furthermore, as a result of an improved gross margin performance, the Company now expects to report EBITDA materially ahead of current market expectations for the period. The Trading update goes on to say: The year-end demand for the Company's products in North America was predominantly driven by technology upgrades and fleet additions, highlighting lengthy project backlogs for our customers that extend well into 2016. While it is too early to provide detailed guidance for 2016, the Board is confident that it will deliver another year of growth and that the high-level of activity in December will continue into 2016 providing a solid start to the year. All in a very pleasing update that prompted me to add a third tranche of Somero shares. The figures continue to look attractive to me: Revenue is increasing year by year as are profits PE(f) of 8.6 with a market cap of £76.9m and supported by £10m cash and no debt. This makes the rating, in my opinion, look even more attractive when you take into account the cash position. In common with a lot of stocks I like, cash-flow ps appreciably higher than eps and also lots of free cash-flow: yes, once again it’s boring but I like being bored. Stockopedia has the ROCE increasing from 2012 to 2015 year by year over the three years as 25.3, 39.4 & 42.5. The operating margin is shown as a very attractive 22.6%. A reasonable yield is provided at 3.5% which is well covered and easily paid from an abundance of FCF. My old friend Prof Piotroski weighs in with a value of 8 which is very reassuring. The two stock ranking systems operated by Stockopedia and by Sharelockholmes also look impressive and add to my feeling of comfort. All in all, to me it appears a great value sound business paying a decent dividend and offering reassuring trading and outlook statements. Is it too good to be true? Well, unfortunately, the market seems to think so either that or it’s just a tad overlooked! It may be that the market sees the business as highly cyclical and will not award a better rating to Somero. Also the latest broker estimate on the 7th January after the trading update only projected a modest increase in eps in 2016, maybe after the release of the full year results there may be a more bullish revision; we will have to wait and see. As regards performance since I first bought in September 2015, the total return is about 4%. Maybe I will catch a cold with this one, who knows. As ever, this is just my whittling on about my thought process in making a share purchase and in no way should be seen as a recommendation to purchase. At the end of last week, I decided to make a top up of my already successful purchase of Cambria which is up around 80% from my original purchase. I don’t consider myself smug at all in this top up even though the price has risen following an RNS on dealerships on 11th January 2016. The truth is I have been a sluggish investor here and should have topped up months ago as the restrained nature of the good news kept flowing. However, no more moaning, I just had better put up and become a touch sharper! I have some spare cash in the portfolio that’s lazing around and not earning it’s keep hence a top up albeit not as compelling as my other purchases of Camb.

Just a few lines on what I like about the business: Well, let’s start with the turnover and profits which have appreciably increased year on year since 2012. To my mind, Cambria is simply a business that is going in the right direction whilst enjoying a favourable climate. I like Cambria it although I am mindful of the cyclical nature of such businesses. The ROCE is decent at 18.1 & the three year average CROCI stands at an impressive 27%. The operating margin is what it is for a car dealership business, not brilliant but it makes profits. Cash-flow ps appreciably higher than eps and also lots of free cash-flow: yes, I know it’s boring but I like being bored. There are no issues with debt which is nice to see and the company also has plenty of cash on the books. The dividend which is nothing to get excited about at 1.1% but to be fair Camb are trying to grow it by 20-25% a year. The dividend is of course massively covered and also the FCF dwarfs dividend payments. The company continues to look for acquisitions and post my recent top up released an RNS on 11/01/16 regarding the Jardine Motors Group which Cambria anticipates will be immediately earnings enhancing. We have a very healthy Piotroski at 8 which gives me confidence. Also, the Stock Ranks given in Stockopedia look incredible at 98. As ever, I cross check to see if that confidence is echoed by Sharelockholmes and I am pleased to say it is as they have a market score of 1(1 is the best score with Sharelockholmes and 100 the worst). So really in terms of ranking you can’t get much better. Just a word of caution with rankings, they tend to confirm or give comfort to my purchases and they are definitely not the sole driver! There have been a few discussions, articles recently concerning Cambria; some feel it’s now time to book profits but I feel albeit with a degree of caution, that further gains can be made. I have to ask myself if I am becoming overly keen on this business and becoming a touch biased; biased is a much more acceptable term than “falling in love with a share”. Well, to my view asking that question of myself keeps me aware of such a potential weakness, an awareness that needs to remain sharp with all portfolio holdings. It’s also very pleasing to know that some very respected private investors continue to hold positions in the business. It was also interesting to listen to a couple of radio interviews of David Stredder who continues to be an admirer of this business that under promises and over delivers. Within these interviews, Camb was discussed along with a good number of other companies. Of course, there are risks with car dealerships as they are a cyclical business but it’s up to us investors to keep on our toes and not get to be overly greedy. As for a price target, I am looking for another 20% from last week’s purchase price of 81p before I evaluate further. I have taken the opportunity to top up on Zytronic, the opportunity having been created by an opinion given by Bearbull in the IC. I have some reference to the article but not a copy as such; I don’t subscribe to IC. I understand that the article said that the share was overvalued by 40% or something ridiculous well everybody has an opinion on stocks and after all, that is what makes the market function but it’s not a view I share.

My view of Zytronic is that it is an exciting growth company and to that end is priced very reasonable for a growth business. If you look at the PE(f) as given in Stockopedia this shows a value of 15.6. However, Zytronic has a decent amount of cash on the books and once you strip this out you come to a PE of around the mid 12’s; expensive, well no, I don’t see it that way. How do the other numbers that attract me to this stock stack up?

We have a very healthy Piotroski at 9 which gives me confidence. Also, the Stock Ranks given in Stockopedia look very healthy SR of 96. Cross checking to see if that confidence is echoed by Sharelockholmes and I am pleased to say it is as they have a market score of 2 (1 is the best score with Sharelockholmes and 100 the worst). So all in all, I am comfortable with what I see. Also just to keep me up to date I listened to an excellent interview of the CEO, Mark Cambridge, that Paul Scott did in the middle of December; all reassuring stuff. Personally, I am in no rush with this one as I think it is a grand little company and am taking a view of at least a couple of years rather than a few months. To that extent if the share price does ease further then I may be tempted to top up again. |

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed