|

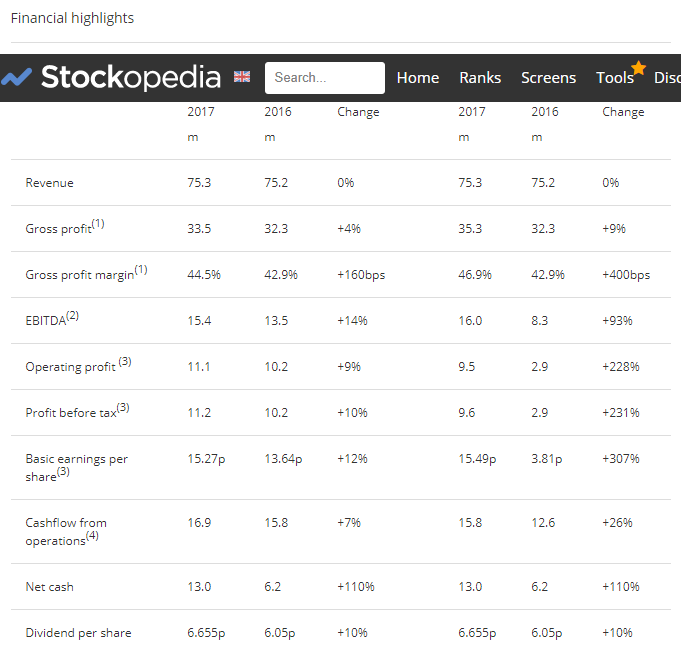

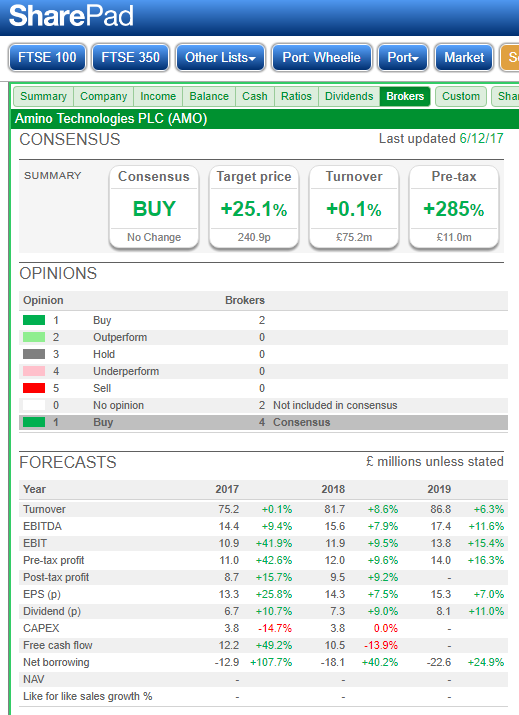

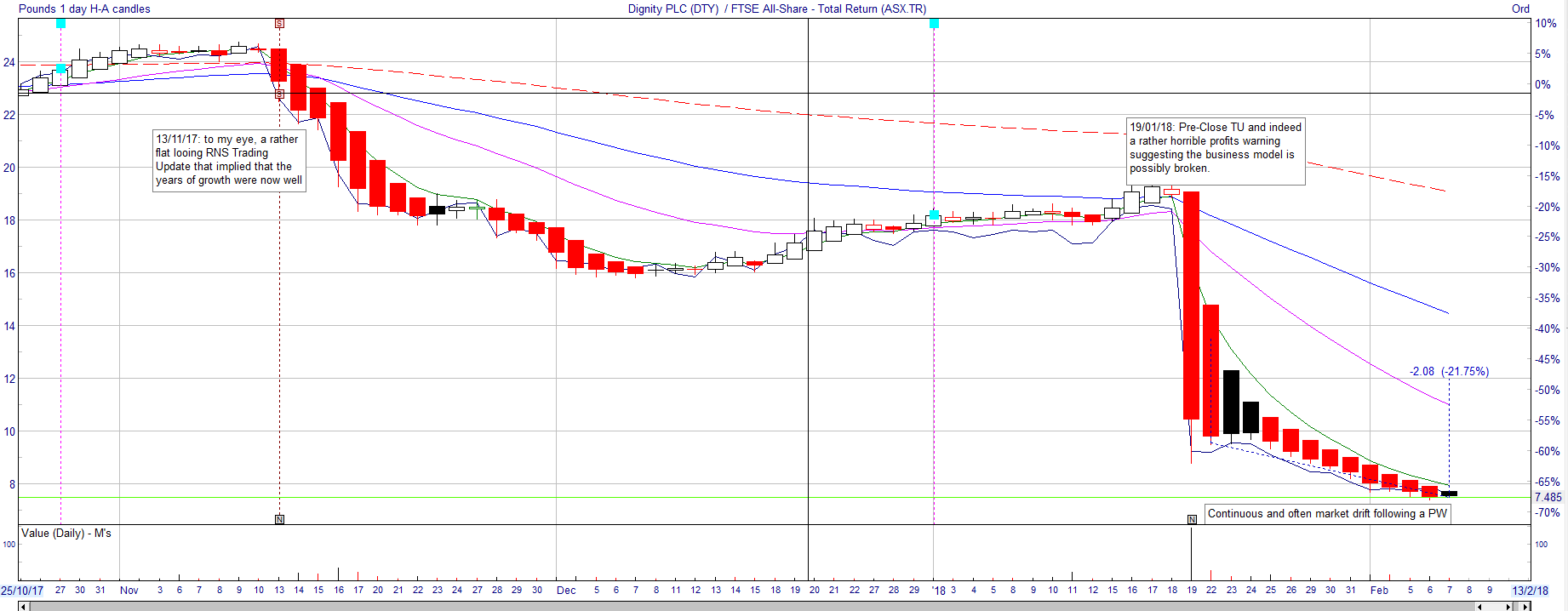

Voyager RNS Log WC 04/02/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Oh, how I dislike February, such a dreadfully cold month; this year I just keep asking myself why have I not flown off to somewhere warmer? I have tried Oz on a couple occasions as a winter retreat but the trouble is down under that if you venture to the warmer parts such as Queensland then swimming is the sea is a definite no as something either wants to eat you or do irreparable harm to you. Yet if you head to Victoria or Southern Australia where the water is just too cold for box-jellyfish or crocodiles and certainly too cold for a southern softie like me. I shall have to have a think for winter 2019, maybe SE Asia, maybe Barbados or a bit closer to home, the Canaries. Mind you if Murder In Paradise is anything to go by, visitors drop like flies in the Carabian so who in their right mind would go there or even closer to home, be foolish enough to set foot in Midsomer. Just how would you get travel insurance for such places? Probably me just thinking a little too deeply. As I have written before on this site, I generally pay no attention to market noise and definitely don’t check price progress anything remotely like daily as I prefer to be RNS driven. However, with storm clouds forming in the USA and falling markets on Friday & Monday, I did a little trimming back on a small number of positions that had maybe become a little stretched, taking profits on FDEV and a few small company IT’s focused on Japan and the UK. Just risk mitigation on the fringes of the overall portfolio where things had become a little stretched. In this column in the past, I have mentioned that I took out all of my original costs for the purchase of KWS which due to its meteoric rise since my tranches purchased, maybe, I thought I might de-risk a little further and sell a few more? However, I then discovered that the considerable holding I have retained are all in my dealing account and not in the tax-free environment. What a wally I am, the CGT is already bulging for 2017/18 and any further sale would just add a horrible 20% gift to that gruesome chancellor bloke, yes the very one who scuppered our £5k tax-free income on share dividends. Looks like I will become a long-term supporter of KWS and eek them away over the next couple of years; long live Mecanno and the fat-finger, or maybe more correctly her, the blind eye syndrome. Oh well, all the KWS are running for free, so who knows! Following Tuesdays sell-off that was hitting the markets worldwide, I decided to do a little shopping and repurchased some GFRD for >20% lower than I had sold in mid-January and also added to my special situations holdings in RWS as they drifted south to what looked a rather bargain price for a quality company, and also topped up on Spectra Systems who issued a couple of ahead of expectations RNSs recently. Yes, there are risks with GFRD contract implications with Carillion but with a dividend of almost 10% which subject to change, is covered by FCF, it’s worth adding to the high yield portfolio. Interestingly on Twitter this week there have been a few views expressed on the use of stop losses; some folk use them whilst some folk don’t. I guess it’s whatever you feel more comfortable with and indeed to a large extent, the quality of the company in terms of its sound accounting practices, debt, realistic market prospects and momentum. Personally, as I have said many times before, taking steps to avoid the destruction of one's capital tied up with a falling share price is simply fundamental to the way I invest. With a stop loss, for a smaller cap company, which for me is £50m to £250m, I usually start with a 20% stop loss that then trails as the SP hopefully increases and as I reach good profits, then I reduce the trigger back to say 12%. If the trigger is hit, I don’t automatically sell but seriously reappraise the investment asking myself “if I did not already own this stock, would I purchase it today with the information currently at hand”? If the answer is yes, then I continue to hold and maybe even take the opportunity to top up; if it’s no, then of course I sell. I have friends and acquaintances who have steadfastly refused to listen to the alarm bells ringing. Is it because they would still buy the share today, maybe because they are terribly loyal or could it be can’t bring themselves to so crucially admit that they got that purchase wrong. Staying with a company that has hit you for a 40% loss requires a 66% gain for break even, a 50% loss requires a 100% gain and an 80% loss a five-fold appreciation in the share price to break even. For me, the answer is easy and you can always go back in such as in the case of GFRD mentioned a couple of paragraphs above, and repurchase again and often at a better price but as ever, each to their own. Looking at the end of last week and going through this week, are we heading for a crash or simply a market correction? Well, I don’t forecast these things and in truth, the “experts” don’t either. The experts are expert only and that’s one thing is looking in the rearview mirror and telling you where you have been but don't have the slightest clue about where we are headed. Where would they be without retrospect? Although in no way a prediction, I rather suspect that the current sell-off is just a correction as markets have really got a touch ahead of themselves and so slide back; it happens and is simply part of stock market investing. Recent examples of corrections are there to see: January 2014, August 2015, January 2016 and of course Brexit. Here we have in my view just got way overstretched in terms of the likes of the Dow Jones so maybe a fall back of as much of 12-15% could happen; yet as I say, predictions hold little value. When markets get maybe a little overvalued, I start to assess each RNS even closer and gradually, if it seems the prudent thing to do, cut reduce some positions i.e. my pre Christmas reductions in ZYT, BVXP, SMWH and KWS. I still hold these stocks but have just taken out some rather decent profits. The rest of the time I tend to ride the turbulence in a slightly more buoyant de-risked boat and hopefully pick up buying opportunities from the cash pile as I see fit. I should also say that after being a freebie, or is that tightfisted, member of ShareSoc, I took out a paying membership this week. Simply can't argue with what these guys do and I am very happy to support their efforts and who knows, I may well turn up at the odd meeting or two. Blimey, I am rabbiting on a bit this week. Let’s get down to discussing any RNSs that have an impact on the portfolio: Monday 05/02/2018: No RNS of interest to the portfolio Tuesday 06/02/2018: Amino Technologies: AMO: Mkt Cap: £140m: Final Results:   Notes (1)Adjusted Gross Profit is a non-GAAP measure and is defined as gross profit before exceptional items (2)Adjusted EBITDA is a non-GAAP measure and is defined as earnings before interest, taxation, depreciation, amortisation, other operating income, exceptional items and share-based payment charges (3)Adjusted profit before tax, adjusted operating profit and adjusted earnings per share are non-GAAP measures and exclude amortisation of acquired intangibles, other operating income, exceptional items and share-based payment charges (4)Adjusted cash generated from operations excludes cash from exceptional items Keith Todd CBE, Non-Executive Chairman, said: "2017 was another year of progress for Amino with strong profit growth and cash generation. We have continued to innovate and steer through the changing customer landscape whilst building a broad product portfolio and customer proposition. Revenue for the year at GBP75.3m was broadly the same as the previous year (FY 2016: GBP75.2m). Profitability was in line with market expectations, with adjusted operating profit(1) of GBP11.1m representing a 9% increase over the prior year (FY 2016: GBP10.2m). Operating profit was 228% higher at GBP9.5m (FY 2016: GBP2.9m) as there were minimal acquisition related costs in the year. The Company's ability to generate cash remains strong with the year-end cash position ahead of market expectations at GBP13.0m (30 November 2016: GBP6.2m). We have large addressable markets and our recent investment in software, services and the emerging Android TV opportunity, coupled with a strong backlog and pipeline, supports our confidence in 2018 and beyond." Outlook Amino has made a promising start to 2018 and has a solid order book and sales pipeline visibility to the end of the year, with a return to our normal seasonality in terms of a stronger second half financial performance. With this positive momentum and clear portfolio and positioning, the Board expects the Company to deliver sustainable profitable growth in the coming year My View: the results look to be bang on target, being in line with market expectations, the dividend was raised by a nice 10% to give a handy yield of about 3.5%. Also, that dividend is amply covered by FCF. The brokers forecasts for 2018 suggest that the company should continue to grow albeit not at the stella rate that would attract the more adventurous investors. The outlook statement reads well enough to me and whilst accepting the risks associated with an AIM technology stock, I rather like the company and it has done quite well for me, I will continue to hold. Also nice to see the CFO, Mark Carlisle, dipping his hand into his pocket to buy an initial position of 5000 shares which is about time as he has been in post since August 2016. I always take notice of CFO/FD share purchases or sales. Tuesday 06/02/2018: Frontier Developments: FDEV: Mkt Cap £495m: Interims I will only cover this one very briefly as it exited the portfolio at the start of the week as I did a little derisking. FDEV was one of my special situations and did ok for me over the few months I have held the stock but with the USA having a wobble on Friday last and that continuing into the Monday, I decided that it was time to manage risk and sell as to my mind the valuation was looking very stretched with absolutely no room for disappointment. The results did not look that stunning to me with minimal increase in turnover and a gradually declining operating margin. Anybody who knows me will be aware of the disdain I have for the PE ratio but I have to admit that a projected PE of 55 is a touch stretched. Maybe I am getting overly cautious but as I am locked into Mecanno KWS for the foreseeable future for tax implications, there is only so much risk I want to carry and anyway, I can always come back at a later date. Wednesday 07/02/2018: No RNS of interest to the portfolio Thursday 08/02/2018: On The Beach: OTB: Mkt Cap £653m: RNS AGM Trading Update AGM Trading Update On the Beach Group plc (LSE: OTB.L), the UK's leading online retailer for beach holidays, today issues the following trading update for the four months to 31 January 2018, in advance of its Annual General Meeting to be held today. The international sites in Sweden and Norway have continued to show strong growth YOY and the Group will shortly launch its international proposition, http://www.ebeach, into its third market, Denmark. The Group continues to increase its investment in talent and technology while building its exclusive supply position and growing awareness across all brands. The Board believes the full benefits of these investments and the incremental marketing investment in the Sunshine.co.uk brand will continue to flow through in the remainder of this financial year. The Group will report Interim Results for the six months to 31 March 2018 on 10 May 2018. Simon Cooper, Chief Executive of On the Beach Group plc, commented: "The first four months of the new financial year has delivered another solid period of growth for the On the Beach, Sunshine and ebeach brands. Our strategy of investing in our brands, talent and technology to drive growth has delivered performance in line with the Board's expectations, with consumers attracted to our wide range of value for money beach holidays. Our third nationwide television advertising campaign started on Christmas Day and has helped drive this strong performance as our brand awareness continues to grow. The Board remains confident in the Group's outlook and will continue to evaluate opportunities to enhance its market share position." My View: I remain comfortable with OTB and appreciate the inline update which encouragingly demonstrates growth and also expansion into other countries to grab a slice of the online holiday market. A very good company in my opinion and I shall continue to hold Glad I Am Not There: well, it’s a place I was there at one time but sold out of Gattaca over 12 months ago once again to preserve capital and manage risk. Back in the late 90’s, a very experienced and well-read investor told me that if a company changes its name then that may well tell you something about the competence of the management of that company especially if that name is just plain stupid. Look at Compel back in the late 1999/2000, Norwich Union, Consignia in the mid-2000’s: now it’s not always the kiss of death and sometimes has no detrimental effect, simply a wise warning to keep a guarded eye open. So, enter Gattaca (GATC) previously known by the name of Matchtech and historically quite a decent business and one which I have pleasingly owned on a couple of occasions. Well, guys that totally ridiculous name change just did not work and as well as failing to give a reasonable account of the reasoning for that chosen name, you have managed to cock-up quite alarmingly and on Wednesday at 2:30 pm issued the following Trading Update/profits warming in an RNS: Taking a more prudent assessment of the economic outlook, we have tempered our expectations for growth in H2 and consequently, we are undertaking a review of our cost base, so as to identify savings, some of which will be achieved in H2. Notwithstanding these savings, profits before tax excluding non-recurring costs are now expected to be in the order of 15% below the Board's previous expectations. The management at Gattaca have steered the share price of the business from well over 600p in 2014 to today's price of just north of 200p; possibly Calamity may have been a better choice of name. Oh yes, the yield which could draw in the casual unsuspecting punter who fails to dig a little deeper, suggests it is now about 10% and will in my opinion, surely be severely cut as there is just not enough FCF to anywhere near cover the payment. Indeed the TU does make reference to the dividend in: In light of the revised full year expectations the Board has decided to reset the rate of dividend in order to restore a more sustainable dividend cover ratio, to enable the pay down of debt, and to reflect a more normalised yield. The Board intends to set the dividend cover at approximately 2x (2017 1x). My view is that the dividend will be reset with reference to the current valuation to be in the order of 4% which is quite a hit for current shareholders. Very glad I don’t hold any GATC and as a final thought, I really mistrust a company that chooses to issue such an announcement significantly later than 7:00 am; this one was released at 2:30 pm, simply poor in my opinion. I last purchased GATC at 322p in October 2016 and sold my holding on2/2/2017 on reading their TU that looked anything but inspiring; I simply asked my self “would I buy this share today knowing what I know now? The answer was a full and rapid NO and the stock was immediately sold, including the stock I had purchased a year or so earlier, for a total loss of around 15%. Not great but at least I was protecting my capital and this approach to capital protection is fundamental to me. Note, I applied the same logic with DTY when they issued what I perceived to be a warning bell; back in November I wrote: DTY a stock I sold at the bell on 13/11/2017 when they released a trading statement I just did not like; not a disastrous statement but nevertheless one that just did not make me feel in the slightest comfortable. I did have a medium sized position in the stock and thankfully escaped relatively unscathed: if in doubt, get out! Now I said relatively unscathed in my Voyager report back in November and checking the numbers, it was a manageable loss of 9%. The shares were, of course, hit by a rather horrible profits warning on 19/01/2018 and fell by a further 50%. Yet another point that I regularly bang on about is that if you are caught up in a profits warning, and believe me it happens to us all, my action is to immediately sell at the opening bell. Investors who failed to do this with DTY having been hit with that awful 50% drop already, would have seen their remaining capital hit by a further 25% in the following couple of weeks: I have written about my handling of profits warnings back in 2016 and since that time, Ed Crofts team have also written a very thorough mini-book on the subject which reaches the same conclusion: SELL on a PW as in the coming weeks and months the stock is most likely to continue to drift south.  Finally, let,s add another green one that in my opinion is just so true:

Overconfidence can be a killer and I suspect after the sweet spot of 2017 that many PIs will feel they are very good investors. However, a strength for an investor is to remain very self-critical and examine the downside at least as much as you enthuse about the possible upside. This weekend I travel to the UK City Of Culture, Stevenage. Actually, I am quite thankful to the New Towns Act planners as they have actually created a town that manages to make my old hometown of Luton, look marginally attractive and that does take some doing believe me. The football ground itself is totally unappealing and the stewarding just about the most inhospitable and incompetent I have come across. The things I do in the cause of football! Whatever you are doing, I wish you a good weekend and definitely feel very envious of those investors residing in warmer climates. As ever, happy investing!

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed