|

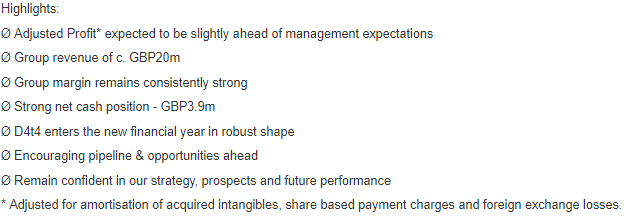

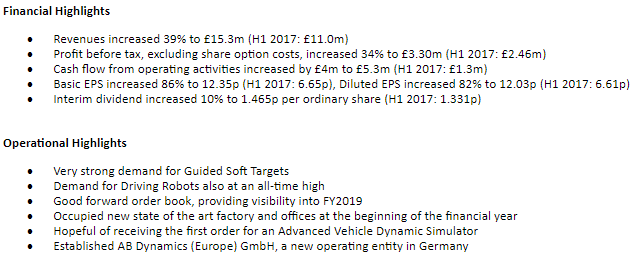

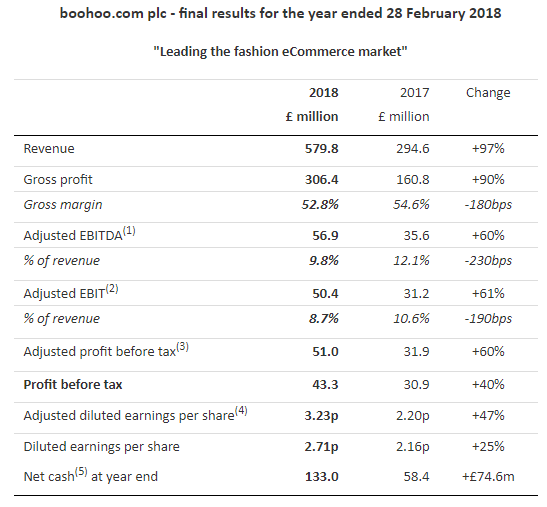

Voyager RNS Log WC 22/04/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Starting with a Green: what I would say about these notes are that they are honestly and simply my interpretation of the newsflow RNS issued by companies within the Voyager portfolio. If I think something is encouraging, then I will say so. Equally, if I feel a company has temporarily gone off the rails, again I will say so as honestly as I can. Oh, what a Saturday at Carlisle as the Hatters gained promotion into League 1; such joy. I absolutely love the passion in football, the emotions, the highs, the lows and also having a couple of beers with friends and local supporters on my travels. I think that something like this actually helps an individual as an investor as in my case the drainage of the emotional side of my brain with sport leaves no emotion for stocks which is a good thing in my opinion. Stocks are simply vehicles that after hopefully diligent research, will in maybe half of the purchases, react well whereas those that appear as one of my less worthy decisions are jettisoned with barely the shrug of a shoulder. Why am I such a fan of RNSs? Well, simply they are my rapid window into what is happening within the business. Companies provide so much valuable information and whilst you have to sometimes dig through the director speak clutter & CFO “adjustments”, it’s not that hard to do and all there for free without the personalised interpretation of a journalist. Also RNS’s are great as with a bit of sifting you get as close as you can to the real vibration of what’s going on in the business. Why is this important? Well for absolutely years now I have been banging on about “investment noise” you know the stuff we see in newspapers, investment magazines, social media etc: there is just so much of it these days that bombards the PI with advice and tips. I honestly feel that PI’s should Do All They Can To Tune Out The Noise it simply a distraction; apologies for shouting! To supplement the RNS service, the private investor has the opportunity if they so choose, to attend AGMs, exhibitors, ShareSoc events etc to talk to the directors of a business. However, just a cautionary word that such events would be absolutely invaluable if the senior directors were all fitted with polygraphs calibrated to detect fibs and misalignment of claimed prospects with reality; it’s just the odd few fibs as sometimes CEO can just become blinded by their tunnel vision, so, take care as you can't naively believe everything you are told. Having said that, once you are comfortable with the honesty and integrity of a companies directors such as Somero, then really listen to what they have to say. This week we have Mello 2018 but that is not what I would define as noise; it’s much more sound educational mentoring from well-respected investors who are speaking at the event. Incidentally, a great deal of the mentoring I received back in the late 90’s early 2000’s was from one of the smartest investors I have known, Jim Slater and believe me, this type of learning is invaluable. Before we go onto this weeks RNS review, I will reiterate possibly the most important lesson I have learnt in 30 years of investing and I will do it in the form of a straight copy & paste from the 2017/18 review article on the blog page of this site:  Onto the RNS news flow: Monday 23/04/2018: D4t4: Mkt Cap £50m: Year End Trading Update RNS:  My View: A fair bit of waffle in the TU in my opinion and whilst in overall terms things look reasonably decent, I note that that the revenue is seen as £20m compared to analysts expectations of £23m: something to keep an eye on and this combined with a touch of profit-taking probably depressed the share price by a few %. We of course have the almost obligatory adjustments profits to paint the rosiest of pictures which is downright annoying when the adjustments include share-based payments; is not that a company cost i.e directors total remuneration package? The TU is mo more than reasonable in my view but for now I am tempted to continue to hold. Also, a quick move early on Monday morning to close my AA spread bet for a nice profit. Tuesday 24/04/2018: RWS: Mkt Cap £1254m: RNS Trading Update: Half Year Trading Statement RWS Holdings plc ("RWS", "the Group"), one of the world's leading language, intellectual property support services and localisation providers, today provides an update on trading for the half year ended 31 March 2018 ("the first half"), ahead of the announcement of its half year results on 7 June 2018. Trading & Financial Update RWS has performed well during the first half, albeit has faced significant exchange rate headwinds as flagged in our AGM statement in February 2018. Notwithstanding these headwinds, the business has achieved revenues of GBP139.6 million for the first half, compared to GBP76.6 million in the first half of 2017, broadly in line with our expectations. The Group expects to achieve Adjusted PBT of at least GBP30.0 million in the first half on a constant currency basis, broadly in line with our expectations for the full year which continue to anticipate a second half weighting. However, the average exchange rate for the first half was $1.37: GBP1, compared to an average of $1.24: GBP1 during the prior year, meaning that we expect the Group to achieve Adjusted PBT of at least GBP28.3 million including the currency effect. The Board will continue to monitor exchange rates over the remainder of the year. However, if the current rates prevail, we would expect a profit outcome slightly below market consensus. This first half saw a steady performance from our Patent Translation & Filing division, following its record performance in 2017, reflecting a strong contribution from our Worldfile product offering and good growth in our Chinese operations. Patent Information continued to perform well (+11%*) and Language Solutions has seen the benefits of last year's restructuring (+11%*). We also saw an excellent first half from our Life Sciences division (+9%*). The successful integration of our two US acquisitions in the space, LUZ (acquired in February 2017) and CTi (acquired in November 2015), has delivered very positive results and enabled the division to grow revenue with several key customers. Our acquisition of Moravia, which completed in November 2017 for a cash consideration of US$320 million, has brought the Group a leading European provider of technology-enabled localisation services to some of the largest technology companies in the world. The acquisition enhances RWS's global presence, adding operations in the Czech Republic, USA, Japan, China, Argentina and Ireland; provides further geographic diversification; and adds an additional profitable, cash generative division of scale to the Group. Since acquisition, Moravia has continued to grow its relationships with its existing major technology clients; however, with over 95% of its revenue in USD and the majority of the cost base in Euro/CZK, the business has seen foreign exchange headwinds. In addition, its performance has been held back by a lower volume of activity than expected from a few clients. Despite this, we are encouraged by Moravia's first half client wins and its pipeline of new opportunities. The integration process is proceeding well and, in particular, a higher level of synergies has been identified which will deliver additional annualised cost savings. My View: well quite a few things that make me feel uncomfortable as follows: albeit has faced significant exchange rate headwinds: Normally I am not overly bothered with exchange considerations especially if I intend to hold a stock for a long time but it just concerns me that this is the very first thing mentioned in the trading update: possibly to divert us and buy a little time. achieved revenues of GBP139.6 million for the first half, compared to GBP76.6 million in the first half of 2017, broadly in line with our expectations: Now that’s director speak to say income will be at the bottom of analysts expectations or in my words let’s say likely not to meet market expectations in turnover. Adjusted PBT of at least GBP30.0 million in the first half on a constant currency basis, broadly in line with our expectations for the full year: Again, that’s director speak to say profits will be at the bottom of analysts expectations or in my words let’s say an almost mild profits warning. Maybe not such as issue if the share traded on a PE of let’s say below 15. Then the RNS goes on to give a further little warning: However, if the current rates prevail, we would expect a profit outcome slightly below market consensus. So, profits in the second half of the year could not be a little less than needed to meet today's TU which in itself is a mild profits warning. Then we have: In addition Moravia, its performance has been held back by a lower volume of activity than expected from a few clients. So, another possible pothole to rock the cart if things don’t improve in the second half of the year. Finally on my don’t like list, based on this TU, RWS is, in my opinion, going to have to motor ahead rather fast and have a good H2 in order to reach brokers consensus forecasts. All in all, whilst I accept that RWS is a quality business, it may have temporarily be having a little wobble, maybe a touch of indigestion after swallowing Moravia, which leads to uncertainty and with a share that is highly rated in PE terms, that just does not give the market's confidence. I did a very quick “first impression” of the TU on the iPhone whilst drying off after the morning swim (it was only 0725 in the morning and it caught me with my knickers down if you follow; my changing room reading of the RNS); got home before the market open to dig a little more and as is normal for me in these circumstances decided to sell as early as I could. Overall, I got a decent price and took a fall of 11% on last nights price. As I always say, you are not going to get all of your stocks going in the desired direction and that’s just not within your control but you can manage downside risk by jettisoning a stock from the portfolio, in this case the Voyager, when risk is identified. Tuesday 24/04/2018: AB Dynamics: ABDP: Mkt Cap £178m: RNS is about:  Tony Best, Chairman of AB Dynamics, commented: "We are pleased to report on an excellent start to the current financial year based on a strong commercial performance. We have built a good forward order book, both for the remainder of 2018 and into next year which gives us confidence in meeting market expectations. The Group continues to invest in its people, products and facilities, and we now have 130 employees, an increase of 41% over the last year. We continue to evolve our structure to support a large and growing installed base of equipment and systems across the world, whilst also ensuring we carry on delivering the innovative new products and services that our customers expect. During the period, we established a new operating entity in Germany which will provide improved customer support and a local engineering resource. The Board is pleased to announce the increased dividend to shareholders of 1.465p per ordinary share that is supported by the strength of our business and future prospects." Tony Best went on to say: We are pleased to report that the forward order book provides a sales pipeline for the remainder of this financial year and into the next and we look forward to the full year with confidence. My View: a very sound set of results with revenue up by 39% and PBT up by 34%. Oh yes, once again we have the adjustments for the dreaded “share option costs” this is really part of the remuneration package which is simply part of the cost of running the business so should be accounted for within Cost Of Sales. Apart from that, nothing I can see there to cause concern in fact quite the opposite, they instil confidence. If you strip out the share options costs from H1 for 2017 & H1 for 2018, we have operating profit @ H1 increasing from £1.6m in 2017 to £2.9m in H1 of 2018 which is a very appreciable rise. Doing a quick fag packet set of calculations based on the half-year results and the broker's consensus full year, these are very good H1 results and I rather expect that they will comfortably beat the current consensus forecast for 2018. An innovative quality company delivering a very good ROCE and high-profit margin. In my opinion, it’s making splendid progress and I am very happy to continue to hold plus I will be looking to add further should we see a price dip in the coming weeks. Wednesday25/04/2018: Persimmon: PSN: Mkt Cap £8.3b: Trading Update RNS: Persimmon plc ("the Group") announces the following trading update covering the period from 1 January 2018 to date, ahead of its Annual General Meeting ("AGM") which is being held at 12.00 noon today. Since the start of the year has been encouraging with the Group's total enquiry levels running c. 13% ahead of the prior year. The Group's forward sales position remains very strong with total forward sales revenue, including legal completions taken to date in 2018, of £2.76 billion, being c.8% higher than last year (2017: £2.56 billion). As announced on 27 February 2018, additional payments under the Plan of 125p per share will be paid over the next three years in late March/early April each year. The first of these additional payments of £389 million, was paid to shareholders as an interim dividend on 29 March 2018. At the same time the Board recommended that the scheduled return of 110p per share, or c. £345 million, will be paid to shareholders on 2 July 2018 as a final dividend. With the scheduled payment on 2 July 2018, the total value of the capital returned by that date of £2.22 billion will be £1.36 billion greater than that originally planned at launch in 2012. The additional payments over the next three years will bring the total value of the Plan to £13.00 per share, more than double the £6.20 per share original commitment made by the Board in 2012. The total value of the Plan is now c. £4.07 billion. My View: listed above are a few selected snippets from the trading update and whilst accepting that PSN operates in a cyclical market, that direction on that market still favours the patient shareholder. Absolutely no complaints from me with a near 100% return on a generous slice of PSN tucked away into my ISA immediately after that surreal Brexit referendum in mid-2016. Can’t see any reason not to continue to hold at the moment. However, I feel that the proposed £75m bonus even if it is to be offered in shares to the CEO, is simply outrageous but I suppose that when it rains gold from the skies, the hard working CEO’s put their buckets out to catch the free gold. Anyway, maybe the greedy grabbers won't get the buckets of gold, after all, see link: www.moneymarketing.co.uk/aberdeen-standard-votes-excessive-pay-persimmon/ Wednesday25/04/2018: Boohoo: EPIC: Mkt Cap £1775m: Final Results RNS:  Outlook and guidance

Trading in the first few weeks of the 2019 financial year has made a strong start. Group revenue growth for the next financial year (FY19) is expected to be 35% to 40% with adjusted EBITDA margin between 9% to 10% and capital expenditure of £50 to £60 million. Looking beyond the current year we will continue to lead the market on value, service and proposition in all our key geographies. Whilst this will require a continued investment in people and infrastructure, we believe that the benefits of our investments in marketing and warehouse automation will generate economies of scale to allow us to drive sales growth of at least 25%, whilst maintaining a 10% EBITDA margin. My View: As a previous holder who enjoyed a comfortable profit albeit maybe an overly early exit on BOO in the past, as I wrote last week after much deliberation waiting to re-enter as the price continued to fall, I bought again last week well aware that there was a risk involved just one week ahead of the year-end results. The Free Cash Flow (FCF) has increased from £5.4m for 2017 to £29.8m for 2018 whilst the ROCE still hovers around 30%: it all spells out as a quality business very much enjoying its moment in the sun. The results have been well received by the market and I am sure that as this one is such a darling of private investors having been championed by the very worthy Paul Scott in the past; there will be some relieved investors today. I am happy enough and will continue to hold. Thursday 26/04/2018: Taylor Wimpey: TW.: Mkt Cap £6.3b: Trading Update RNS: UK current trading The underlying housing market has remained stable in the first four months of 2018, with continued good accessibility to mortgages at competitive rates. During the first few weeks of March, the poor weather conditions had a noticeable impact on sales and build rates but activity has since recovered. Solid consumer demand continues to drive a healthy sales rate against a very strong comparator. Average private sales for the year to date were 0.85 per outlet per week (2017 equivalent period: 0.93) in line with our expectations. Cancellation rates remained low at 13% (2017 equivalent period: 10%). As at 22 April 2018, our total order book value stood at approximately £2,155 million (2017 week 16: £2,210 million). This represents 9,050 homes (2017 week 16: 9,219 homes), excluding legal completions to date. My View: a rather uninspiring update I felt and decided it was time to take profits so sold on the morning of the RNS; whilst my sale was some way off the top of the market price of 210p back in early January, the fact is that in a long career of investing I reckon I have only sold at the top on a handful of occasions: Never feel you are clever enough to buy at the bottom and sell at the top; it just doesn’t happen apart from the “smart crew” on bullectin boards & we all believe them don’t we! TW was one that has earnt its keep in the high-yield portfolio (that massively unexciting stuff) delivering a return of over 15% in the year but I felt that the update may lead to some drift and really time to move on as I have plenty of housebuilder exposure in a PSN & also the TEF a company as I rate as the most exciting in that sector. Friday 27/04/2018: Air partner: AIR: Appointment of Interim CFO RNS: Air Partner PLC is delighted to announce the appointment of Chris Mann as Interim Chief Financial Officer. Chris is a chartered accountant who has worked in finance positions at senior level within a range of listed and private companies, most recently with KONE Corporation and Gatwick Airport Limited. Chris will remain with the Company until a permanent Chief Financial Officer is appointed in due course. He will not be a director of the Company, nor a member of the Board. My View: decent move and an apparent safe pair of hands to draw a line under the previous accounting issues and hopefully swiftly move on. Whats On the horizon next week: To be honest, next week looks a little dull and I can’t see any Voyager companies with H1 or H2 results pencilled in or for that matter and trading updates that coincide with the same period as last year. This weekend sees the Hatters final League 2 home match for hopefully some years and then it’s onto League 1 for next season. Strangely in football, I have always had this theory that clubs get promoted to reach an equilibrium between competence and incompetence so let's see what next season brings. Certainly, there will be lots of different town & cities to visit and for me, that’s all part of a great day out. I am already looking forward to the Stadium of Light in Sunderland which will give me an excuse to call into Hartlepool for a couple of swift ones in that superb real ale bar called The Rat race. Happy investing; catch you all next week

1 Comment

Damo

5/5/2018 11:37:30 am

Nice work as usual SW , was so tempted with RWS this week but I'm trying hard to stick to my avoid falling knives strat. That said from inexperienced pov , it doesn't look a disaster 🤔. Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed