|

Voyager RNS Log WC 08/04/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Oh, What A Noisy World! Twitter: I do like Twitter and it’s a great place to keep in touch with fellow investors but without care, it can become very hungry on one’s time. On the pro side you can get very rapidly the thoughts of other respected investors but on the con side, unless you really manage your Twitter time well, you could get sucked into a black hole of noise. It’s something that I have become increasingly conscious of these last few months. In some respects, the time reading on Twitter may well be a compliment to the very readable comments made by other investors and certainly, the links often posted are first class. However, like most things in life its quality of information rather than quantity that counts: with shares you can easily sieve characteristics to get to the stocks that may be of interest to you but with Twitter with those that you follow, there are no real shortcuts; well at least not any that I am aware of. Thankfully some of the most respected successful investors are relatively infrequent Tweeters and when they do tweet you really take notice of what they have to say. It's really just an observation and one that runs alongside the drum I have been beating for years now about cutting the market noise. Incidentally, the idea about market noise first came to me many years ago whilst flying to Australia. The plane was an old QANTAS beast and noisy as hell until I put on my “oh so flashy” noise reducing headphones: bliss, I could think again as I deliberated Sharescope on my laptop. That’s when I thought how great it would be to cut out market noise and that’s what I do with a passion these days; I honestly can't recall the last time I bought IC magazine or similar; not knocking them but they just simply add to the noise. For me, decision making within investing is about the financial numbers & ratios, the RNS flow from the companies that make it to the Voyager universe and a mandatory need to have as far as we can tell, a credible CEO & CFO running each particular business. On the other hand, I do read the comments of some of the thoughts of a number of very astute investors on the Twitter and also regular articles posted by excellent commentators including such as Paul Scott (Stockopedia), Phil Oakley & Richard Beddard (both on SharePad): these guys actually try to educate the private investor with relatively infrequent but quality analysis. It’s then up to the individual investor if they choose to be spoon-fed or learn from mentors and make their own investment decisions. As for managing my time on Twitter, I now try to limit myself 15 minutes in the morning and 15 minutes in the evening or at least that’s what I try to do until somebody includes a useful link that I simply can’t resist reading: blast, there I go again, time ticks away with Twitter. Anyway, let's have a look at what’s being going on in the Voyager Universe this week. Monday 09/04/2018: Keywords Studios: KWS: Mkt Cap £1060m: RNS’s are about:

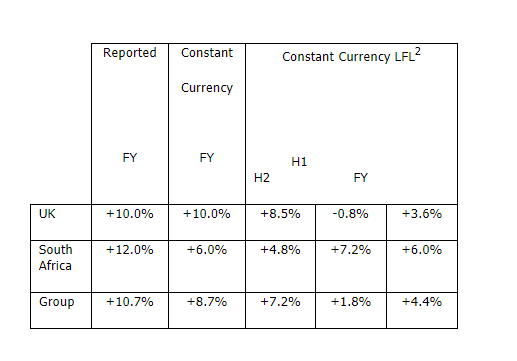

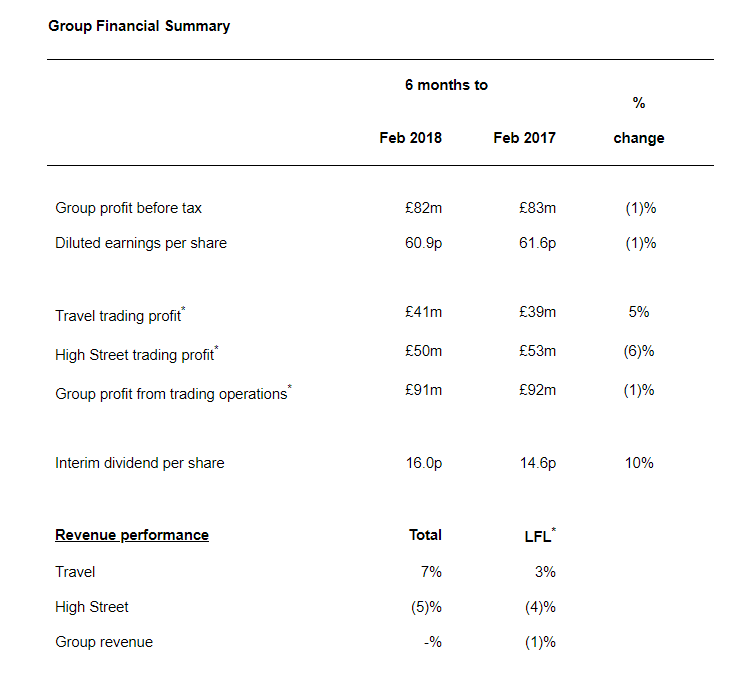

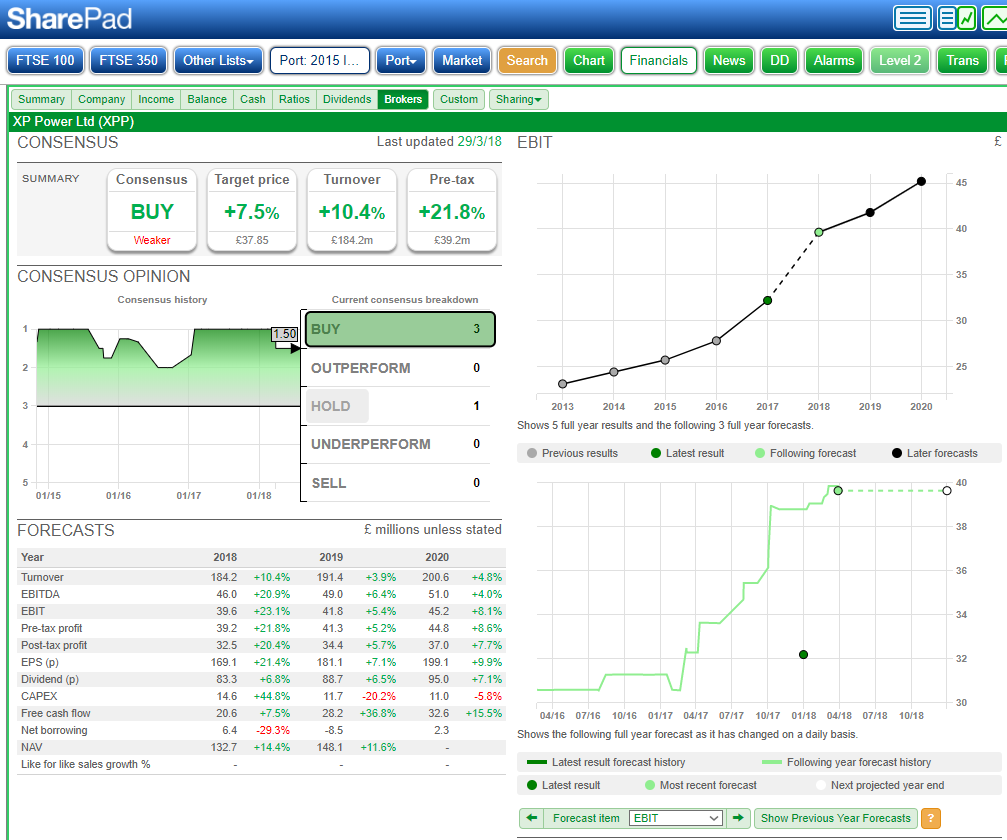

Financial overview: Group revenue (including effect of acquisitions) increased by 57% to €151.4m (2016: €96.6m) Adjusted EBITDA* up 57% to €26.3m (2016: €16.7m), representing a margin of 17.4% (2016: 17.3%) Adjusted profit before tax* increased by 55% to €23.0m (2016: €14.9m) Adjusted basic earnings per share* up by 52% to 31.18c (2016: 20.59c) Adjusted operating cash generation** increase of 48% to €21.9m (2016: €14.8m) Net cash*** of €11.1m (2016: €8.7m) Final dividend of 0.98p (2016: 0.89p); 10% increase in total dividend to 1.46p per share (2016: 1.33p) My View: the numbers themselves are right at the top end of the revised market expectations; the revisions being made when KWS provided a strong trading statement back in early February this year. There are of course lots of adjustments but this is inevitable with a company growing at the rate that KWS and continually making bolt-on acquisitions but nevertheless the numbers are highly impressive. The market, which is incidentally highly fragmented, for the work that KWS offer is simply huge and the CEO Andrew Day, estimates this to be $5 Billion; that’s some market and KWSX is now becoming recognised as a “go to” provider for many of the requirements of this huge market. Incidentally, it’s well worth a look at the results presentation that KWS did on Pi World this Monday, Link: www.piworld.co.uk/2018/04/09/keywords-studios-kws-fy-results-presentation-9th-april-2018/ Regular readers will know that I first bought into KWS back in mid-2016 when the shares were just over £3 and did make several top-ups as the “beating expectations” RNSs kept flowing. I eventually reached a point where the percentage of KWS in my portfolio was becoming a touch sill and that together with my ongoing thoughts about the risks associated with managing so many acquisitions, lead me to sell some shares in kws to the value of my original investment: just simple risk mitigation. However, due to the continual upward trajectory, despite my top-slicing, KWS remains as one of my most significant stocks by percentage value shares within the Voyager. At the moment, I am happy to continue to hold and hopefully sleep well. Tuesday 10/04/2018: D4t4: D4t4: Mkt Cap £50m: RNS Trading Update & Contract Wins: The Company is in the process of its year-end close and intends to provide a more detailed update on financial performance on 23 April 2018, in advance of this, the Directors are confident that the revenue and adjusted* profit before tax will be ahead of the comparatives for the year ended 31 March 2017. Details of the recently converted opportunities are as follows: Data Management: · A major multi-year contract with a global US headquartered financial institution for our Private Cloud Data Analytics solution. Data Collection: · A new contract for our Celebrus data collection software with a Taiwanese bank. · An extension of a global contract in the financial services sector with the addition of a new data collection channel using our Celebrus data collection software. · A capacity extension contract for our Celebrus data collection software with a major online retailer in the UK. · A capacity and functionality extension contract for our Celebrus data collection software with a major online retailer in the UK. · A capacity extension contract for our Celebrus data collection software with a major European retailer. · A new contract for our Celebrus data collection software with a major Japanese car manufacturer who will be utilising our GDPR compliance functionality. *Adjusted for amortisation of acquired intangibles, share based payment charges and foreign exchange losses. My View: I did write a few months back that when D4t4 released that ”results will be weighted to the second half of the year” RNS, that I greatly reduced by holding again simply as risk mitigation. Well, although I am fairly ruthless in jettisoning a risk to the portfolio, once I feel confident about better news then I am happy to either but back in or consider increasing my holding. I thought that this RNS was both reassuring about this year’s prospects and the new contract wins certainly add more confidence in going forward. The one thing I did not like about the RNS was the vague wording “profit before tax will be ahead of the comparatives for the year ended 31 March 2017”. Just why not say we will meet market expectations and save the poor investor some legwork in terms of chasing back through historis reports? All in all, I am happy as I bought back my previously sold stock at a lower price than I had sold them for and the share price looks to be appreciating nicely: happy enough with that one. Wednesday 11/04/2018: Norcros: NXR: Mkt Cap £150m: RNS Trading Update: Group underlying operating profit for the year is expected to be in line with the Board's expectations. Group revenue for the year is expected to be in the region of £300m (2017: £271.2m), 10.7% higher than the prior year on a reported basis, 8.7% higher on a constant currency basis, and 4.4% higher on a constant currency like for like basis2.  UK revenue for the year was 10.0% higher than the prior year reflecting in part the first time contribution from Merlyn which was acquired on 23 November 2017. Merlyn has been seamlessly integrated into the Group and performed in line with the Board's expectations. On a like for like basis2, UK revenue was 3.6% higher than the prior year. Second half UK LFL revenue declined by 0.8% compared to the 8.5% growth seen in the first half. This was largely due to lower retail revenues at Johnson Tiles and a tough comparative period last year. Johnson Tiles apart, H2 UK LFL revenue was 8.4% higher (H1 +11.4%). Our South African business again delivered strong revenue growth despite a challenging market environment, 6.0% higher than the prior year on a constant currency basis and 12.0% higher on a reported basis, continuing the sustained progress of recent years. Reorganisation - Johnson Tiles UK In 2017 we implemented a restructuring at Johnson Tiles UK designed to improve its operating performance and increase manufacturing flexibility. Notwithstanding the benefits of this restructuring the business remains loss making as market conditions experienced in the second half proved more challenging than expected. As a result, the Board has implemented a further restructuring programme which will involve the loss of up to 50 jobs. This will result in a charge of around £2.1m, to be treated as an exceptional item and recognised in the financial year ended 31 March 2018 with the subsequent cash outflow occurring in the first half of 2018/19. Annualised savings are expected to be at least £2m. Financial position Closing year end net debt is expected to be around £48m (2017: £23.2m), in line with the Board's expectations. Pro forma Net Debt to EBITDA is expected to be circa 1.3x, in line with the guidance at the time of the Merlyn acquisition. My View: I greatly reduced my position in NXR which formed part of an Income portfolio, towards the end of February (see earlier blog notes). I still like the company and it had indeed delivered all one could ask for in a high yield portfolio but I felt as the market continued to be blinded by the pension issues that it was time to take a 50% or thereabouts top slice. Incidentally, those pension issues as I write so often, are simply not a serious issue as the pension fund is closed to new entrants and the average age of members in now in the early 80’s. I am happy to hold my remaining share and trust the issues that have held the company back at Johnson Tiles will be sorted shortly. I always feel for employees that are to be made redundant, I have done enough of that “breaking the bad news” in my career but a quick fag packet look at the numbers suggests that the staff will be treated reasonably well. Without doubt whilst the accountants who run NXR may be described as a safe pair of hands, their RNSs and presentations are as dull as dishwater completely lacking in inspiration but I will nevertheless hold my reduced holding for now. Wednesday 11/04/2018: Air Partner: AIR: Mkt Cap £47m: RNS FURTHER UPDATE ON ACCOUNTING REVIEW: Our review has made good progress, and is ongoing. At this stage, we believe that the total cumulative impact arising between the financial years ended 31 July 2011 and 31 January 2018 will not exceed £4m. The final amount will be confirmed to the market after completion of the review. In accordance with accounting practice, amounts relating to prior periods will be recorded as restatements of comparative financial information. Any amount attributable to any period will be treated as a non-cash item. On the advice of its advisers, considering the work required to restate appropriate historic accounts and complete the full year audit, the Company believes it prudent to reschedule the announcement of its full year results for year ended 31 January 2018 from 26th April 2018 to 31 May 2018. The RNS then goes on to reassure by After appropriate restatements, the Board expects that the Company will have sufficient distributable reserves to pay dividends. The Board intends to recommend that the final dividend payable for the year ended 31st January 2018 will be 3.8 pence per share. The Board further wishes to take this opportunity to reaffirm its ongoing commitment to its dividend policy, which targets cover of between 1.5 and 2.0 times underlying earnings per share. On 6th February 2018, the company announced, "underlying pre-tax profit for the financial year ended 31 January 2018 is expected to be not less than £6.4m". Prior to adjustment for any expense attributable to the period arising from this matter, this statement remains valid. The Group currently maintains a strong balance sheet with over £8.6m of its own cash at the end of March 2018. Any one off costs and fees associated with the review will be expensed in the financial year ended 31st January 2019 and clearly identified as such. Whilst our review is ongoing, we will not comment on rumour or speculation, and shareholders should expect official statements to be issued to recognised Regulatory Information Service providers as appropriate, ensuring full compliance with regulatory obligations. My View: well that’s quite a reassuring update from AIR and to a large extent dispels some of the market fears that AIR could become another CVR. In my view AIR was nothing like the CVR situation; with AIR somebody in the accounts department has been let’s say irresponsible with bad practice remaining undetected and whilst this is a worry, this RNS does clear the air ( I like that, clear the air). Last week I wrote in this journal that I sold all of my AIR at the opening and took my profits as the stock carried too much risk and could easily drop appreciably further and of course, it certainly did and indeed so much further than I expected and more than probably justified. Early on the day of this latest reassuring RNS, I bought back into AIR at a price very significantly cheaper than I had sold them at last week. I now see AIR as a special situation with, given time, an attractive upside but with a touch more risk that most of the other stocks within my portfolio. My view is that whilst even at the best of times the share price is prone to turbulence, this stock has potential given time for a maybe 25-40% upside. Note: although I do sell with a rather ruthless unemotional streak, and this is done in order to protect capital, I am very open to returning to that stock once the risk has diminished: recent in 2018 include PMP, D4t4 & AIR. For me, it’s all a question about acknowledging the risk, mitigating that risk and NEVER being too proud to either sell or repurchase once the situation has changed and the stock risk altered. Thursday 12/04/2018: WH Smith: SMWH: Mkt Cap £2180m: RNS Interim Results: The figures tend to show in my opinion that SMWH is possibly treading water a little this last six months:  My View: well after a very good association with SMWH which had delivered my a splendid return from one of my favourite “most boring” companies, it’s time to bid the stock farewell and bank the profits. It’s a lovely company and the travel section is still progressing well but the attractions in terms of ROCE/CROIC remain, I see limited upside and indeed by trailing stop loss has been pinging little messages to me since mid-February. For me, it’s time for now to bank the profits. Friday13/04/2018: XP Power: XPP: Mkt Cap £677m: RNS Trading Update: The Company has made a good start to the new financial year as the strong order intake reported in 2017 continued into 2018. Order intake in the first quarter of 2018 was £51.2 million (2017: £47.0 million), 9% ahead of Q1 2017 on a reported basis or 19% ahead in constant currency. On a “like for like” basis, removing currency effects and the impact of the Comdel acquisition, orders increased by 12%. Group revenue for the three months to 31 March 2018 was £46.6 million (2017: £39.6 million), 18% ahead of Q1 2017 on a reported basis, or 28% ahead in constant currency. On a “like for like” basis revenue increased by 17%. The Book to Bill ratio, which tracks the relationship between orders received and completed sales and is an indicator of future revenue growth, was 1.10 for the first quarter. Financial Position Net debt was £6.8 million at 31 March 2018 compared with £9.0 million at 31 December 2017. Dividend The Board has declared a dividend for the first quarter of 16 pence per share, a 7% increase over the prior year, which will be paid on 11 July 2018 to shareholders on the register at 15 June 2018 (2017: 15 pence per share). Outlook The momentum seen in 2017 has continued into the first quarter of 2018 and we are encouraged by the continued strong order intake experienced across the business and the book to bill level gives us confidence for the future. The Board’s expectations for the Company’s full-year performance remain unchanged. My View: A solid trading update from XPP and let’s remember this is for the first quarter of 2018 so you are quite unlikely to get “ahead of expectations” predictions for the full year at this stage. I have held XPP for a couple of years now and it has been a fine performer in the portfolio. I really do like the company as they offer so many of the attributes that I seek in a solid business: of course, like most stocks it is not without risk but with good management at the helm, you get a comfortable feel. For information the brokers forecasts are shown below; I see Stockopedia also allocates an attractive stock rank of 87 to XPP.  Friday13/04/2018: Air Partner: AIR: RNS Directorate Change: Following the announcement of Air Partner's intention to restate certain historic results, the Company today announces that the Chief Financial Officer, Neil Morris, has offered his resignation to the Board of Air Partner. This has been accepted, with effect from today. Neil will remain available to the Company to contribute to the ongoing review, in respect of which, there is no further update from the RNS released on Wednesday. The Company is reviewing candidates for the position of Interim Chief Financial Officer that are available immediately. Air Partner will be engaging an external recruitment consultancy to assist in the search process for a permanent Chief Financial Officer. My View: Well, no an unexpected announcement but nevertheless a touch cold as we don’t even have a “we would like to thank Neil….” In the statement and it makes it fairly clear that no internal candidates will be considered. I would think there will be a whole lot of changes in the finance department at AIR. Whats On the horizon next week: Let’s start with Sunday when I hope to do blog on the Voyager performance in FY 2017/18; it will be a fairly high-level overview in terms did the Voyager bear the benchmarks applied. I can’t see any results pencilled in for next week but would have thought that we could possibly see some Trading Updates from RWS, TEF, IGR & BON shortly. This weekend the stumbling Hatters have the opportunity to lurch a little closer to promotion when we take on Crewe at Kenilworth Road. I had better mention next week's game now as although I have a train ticket booked that gets me into Carlisle at mid-morning well ahead of the 3pm kickoff, I might just waste the ticket and take a couple of days around Grasmere before heading off to Carlisle; I will take a late decision on that one. If it is a few days walking in the Lakes then I may have to sacrifice next weeks voyager. Happy investing; catch you all next week

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed