|

Oh dear, this investment lark can be a worry. Well, I need to qualify that remark as it’s not so much a worry with my own money as I understand the risks about stock market investment and I am happy enough with those risks. What is a worry is discussing possible ways to invest a spare few £000’s that a close relative may have tucked away under the mattress. Anyway, such a discussion came up recently with a relative who had a few thousand pounds totally frustrating him as it was essentially doing nothing for him in terms of increasing the size of his wealth. For reasons of amusement and anonymity of the said relative, I will describe the tale in a story style conversation. Oh yes, before I do that I had better give the relative a name to spare his blushes; I will call him Matt and of course his surname will be Ress; come on keep up, MattRess, got it! So onto the conversation:- Well, Matt comes along to see me after much worry about his investments that are sitting in a simple interest account at his bank. Matt is really frustrated as in total on this spare £15000 he is earning in the order of £130 a year interest which in real terms he considers to be an erosion of this spare chunk of cash. Matt asks my advice regarding what he should do with such an amount of cash to make the cash work harder for him and make at least a decent return of his cash. Well, no surprises there as the answer is simple “sorry Matt I never give advice to others regarding investments”. Of course, Matt was very frustrated with my blank & closed response, this was not at all what he was looking for from his once favourite uncle who was becoming less of a favourite by the minute. I then reasoned with Matt that at least having his money where it sits at the moment does not expose that money to any real risks other than the bank going bust but even then he would eventually get all of his money back. Now Matt was not going to let this one go away and asked my general views on investment that fits with my character. Ok, I said but let me give you a little old fashioned advice in bullet point form below:

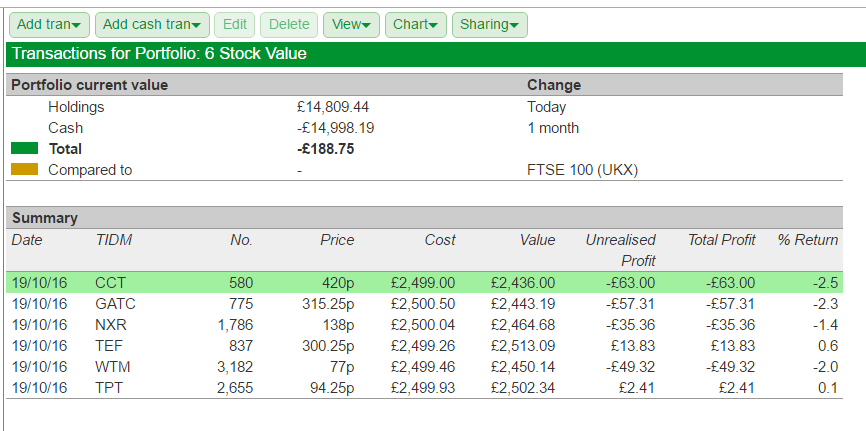

To spread the risk, we will in this practice portfolio have six stocks; why six? Well, Matt, it’s to spread the risk. For example if one company comes out with a dreaded profits warning and the share price immediately falls by 25% that would be a bit of a disaster if you only held that one share. However, if that share was one of a number within a basket of shares, in our example six shares, the overall hit on the portfolio would be much, much less, say about 4%. Ok, Matt said, as he grasped that point but then went on to say won't that have the opposite effect if one of your shares goes up by 25%? Well, of course, it will but this is what we call risk management: remember that greed can kill! So, on we went to create this portfolio investing a hypothetical £2500 in each of the following six stocks: Character Group (CCT), Gattaca (GATC), Norcros (NXR), Telford Homes (TEF), Topps Tiles (TPT) and Waterman (WTM). Once we had entered our “buys” into SharePad and taken account of those odd little annoyances such as the bid/offer spread, the brokers charge (even at a bargain £5) and the stamp duty of 0.5% on main-market listed shares (we don’t pay stamp duty as a rule on AIM shares) Matt’s portfolio of pretend £15000 cash had already fallen an amazing £280 in value without any real movement in the prices of these shares. Oh hell, said Matt that’s equivalent to a weeks holiday in Benidorm. Ok, I did go on to tell Matt that all things being equal and assuming that the stock prices remained stable for the next 12 months he would receive a theoretical batch of dividends of about £780 that could, with luck leave him £500 better off. By the look on Matt’s face, I could tell he was a worried chap, all of this risk for maybe making £500 in dividends and that in itself could be badly hit if one or more of these companies hits a really rough patch. Matt’s final words were to say that he was glad it was only pretend money and not his own as the thought of actually losing money was not one that appealed to him greatly. So, we will leave it there for now and come back shortly for another chat with Matt as his education continues.Well, we were going to do just that but as Matt looks at the screen his “losses” have now in a few minutes have shrunk to only -£188. How can that be, asked Matt? Well, Matt, I said, the stock market is a dynamic beast; it moves all of the time and the tool we need to use is one called patience. One great investor famously said “I make more money simply sitting on my hands and being patient”: do you think you would be comfortable showing patience Matt? Matt’s “portfolio valuation” a couple of hours after creation is now given in the SharePad table below:  Note: I should point out that as well as researching this batch of stocks, I currently hold positions in all six stocks mentioned in this article. However, my risk balance for any of these six stocks is actually much more favourable than in Matt’s portfolio as the size of my basket is currently 36 stocks. So should any one stock suffer the dreaded profits warning and slide by 25% then it’s effect on the overall portfolio would be no more than an annoyance.

3 Comments

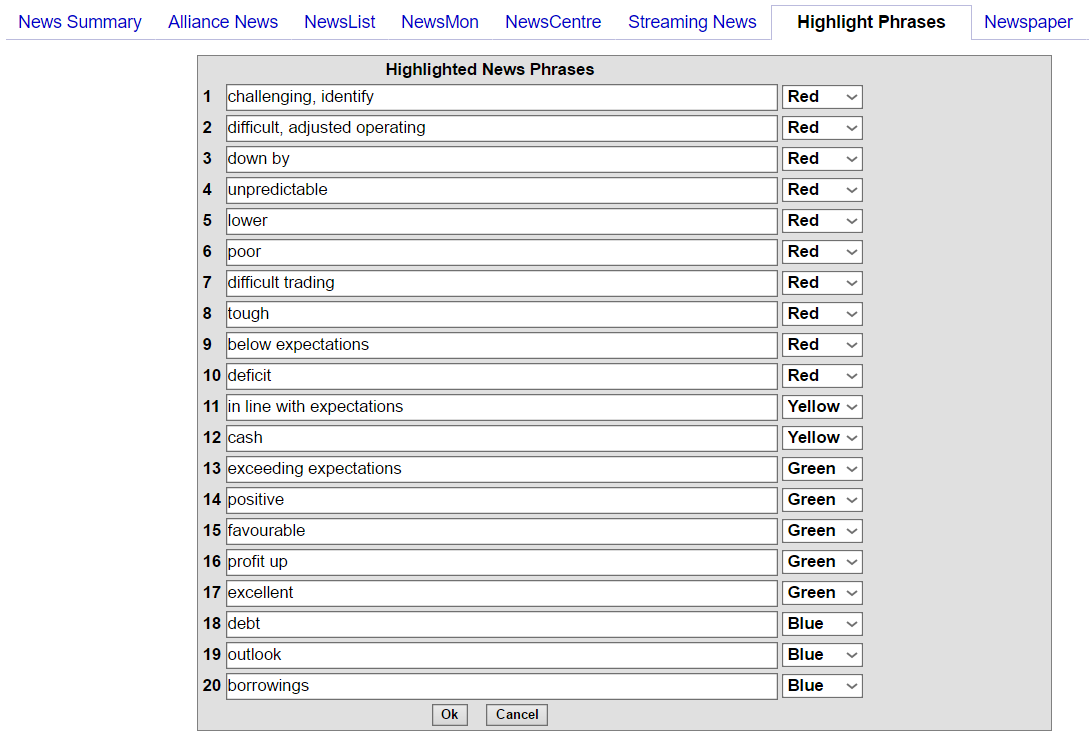

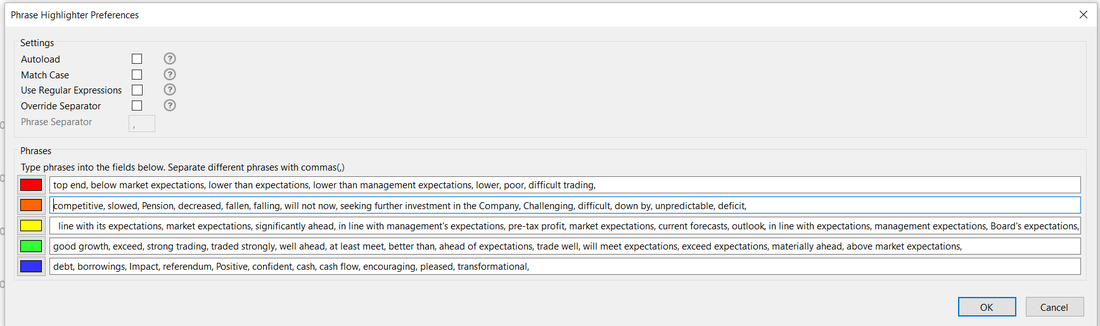

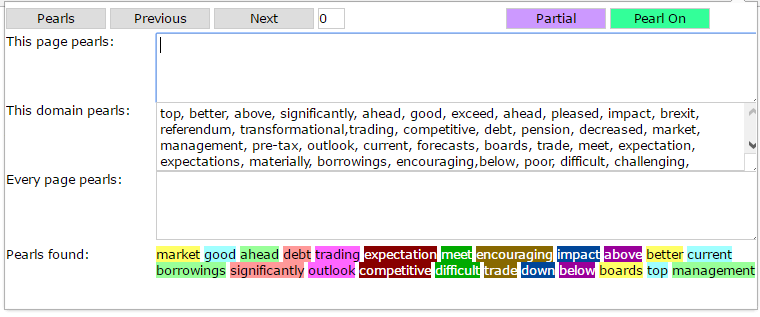

These days we have a vast number of investors for whom the stock market plays a fairly major part in their daily life. Some will be active part-time investors who fit their investment activities around paid employment and others may well be “living the dream” and be loosely classified as a full-time investor. Strange thing is, how do you identify or characterise a full-time investor? Is it somebody who sits at a screen all day watching every move of the market and trading frequently or is the Terry Smith type sitting on one's hands and doing very little to a quality portfolio. Well in truth, both extremes are really full-time investors just simply different styles. When I look at my style of investing it identifies much more closely with the Terry Smith style than the active trader style wanting to make a fast buck and exit the position before moving onto the next trade. With style in mind, the style of my investing rather than by usual laid-back attire of the summer months, sandals & shorts, I thought I would write a few notes of the typical day in the life of a whittling investor: Well getting up and out of bed in the morning has always been easy for me. The only period in my life where I have struggled with this was in my early 20’s when I suffered “Sunday migraines” but later found that was beer related. I usually get up at about 6am and find myself in front of the screen by around 6:30 then go through my diary of planned RNS announcements expected that day and also every few days, do a quick run to see if any new opportunities have been identified in my investment universe (see blog dated 24th April 2016). Then with a nice cup of coffee at hand, as 7:00am arrives, I open up Investigate to scan the days RNS’s of interest to me. I have a preset list of “my list” within Investigate that should if all goes well, immediately flag up any RNS for a company that I have shares in. Then, of course, we could spend some time sifting through every word in an RNS or as I do, use word & phrase highlighting tools. The first highlighter I used a few years back was the one on ADVFN. This works fine but you are limited to 20 phrase boxes, see below:  The next one I moved onto was within Firefox using their phrase highlighter add-on. You have to remember to switch it on and off otherwise, it will highlight those nominated words and phrases from any web-site you visit and that can be a bit of a pain.  Finally, I settled for one that works on both Chrome and my preferred browser, Opera. The one that really does the trick for me is Pearls extension and the really clever thing is that it is web-site specific. I have mine set just for Investigate:  An actual Pearls example for a Norcros trading update from July 2016 is given below:  Using these highlighter tools enables me to quickly rattle through any RNS of interest and take a preliminary view of what action I may take for example if I see a profits warning I almost invariably sell at market open but this can be a pain as it delays my daily swim. Oh yes, I then send out a few tweets and where appropriate declare whatever interest I hold in the company. So assuming there is nothing overly worrying identified, I am off to the pool for a quick mile returning for a plate of porridge and blueberries at about 9:15; I did read that blueberries are supposed to stimulate the brain, so why not.

Then over breakfast it’s a question of pondering over what Mr Market makes of things and finishing the working day by about 10am; I quite like this lifestyle. Occasionally the day will drift on a little longer if any stocks are identified from the screens that I run on SharePad. Then the process of more in-depth research starts. Just one more check and that’s at the end of the day when I check to see how things closed off on Sharescope. Personally, it’s a lifestyle that fits well with my personality and I only wish I had made the move away from paid employment many years ago but the opportunity was not always there. Let’s see what tomorrow brings! Happy investing! In April this year I wrote an article entitled Creating an Investment Universe. The purpose of the article was to describe my approach to screening the entire LSE universe of over 2000+ shares to come up with my own very limited investment universe based on strict financial criteria. That massively slimmed down universe, then forms a list of apparently financially strong stocks for further in-depth research. Of that 2000+ shares approximately half are located on the very hostile planet called AIM, a very inhospitable place with large areas reminiscent of the USA wild west with bandits, rustlers, snake oil merchants, Klondike prospectors, savages and medicine men. All in all, a difficult place for the settler venturing onto planet AIM to stake a claim and make a sustainable, risk-averse investment in his or her future.

Certainly, my approach to AIM during the period from its inception in 1995 to 2010 was simply to simply exclude AIM stocks from any screen; apart from the odd punt, I just would not consider making a serious investment in an AIM stock. My reasoning for excluding AIM was a combination of its lightly regulated market conditions, the spiv “Private Walker” type CEO’s, the abundance of “jam tomorrow” companies, the disappearing businesses and the exclusion until 2013 of AIM stocks from ISAs. From the planet AIM, there has always been the stories of the rapid 10 bagger, the resource prospectors that struck it rich mixed with a liberal sprinkling of tales of companies that are little short of fraudulent vehicles designed to make their directors very wealthy at the I should say that within my non-ISA stocks I have had for years a sprinkling of non-AIM stocks mainly based on fairly careful selection but over the last five years, my number of AIM investments has rapidly increased to form around 50% of my ISA portfolio and 50% of my non-ISA portfolio. One of the reasons for this shift in percentage has of course been due to the eligibility of AIM stocks to be held within an ISA as from 2013. However, personally, that was very much a secondary consideration. The main reason for my increased numbers of AIM stocks was the realisation that in amongst that hostile planet AIM there existed some truly wonderful companies that are managed on a very sound financial basis. My approach is simply to screen the entire AIM community to come up with a tiny handful of stocks that meet my strict financial criteria that I apply to any stock listed on the main market. You know, sometimes I feel that investors who are reasonably successful on the main market and then take on AIM, are similar to successful businessmen who decide to become directors of football clubs. Once the successful businessman becomes that football club director, the usual common sense that has proved so sound in his business world is left behind and financial problems are not far behind. The fact is that any rules or investment philosophy that you apply on the main market must be applied “with bells on” to the AIM market and that is exactly what I try to do. I am not saying for a moment I have the perfect answer, I am sure I will get hit with the occasional profits warning, I know for near certainty that I won’t get the elusive “10 baggers” but that’s totally fine with me. So over the past five years how have these hopefully less risky stocks performed that I have plundered from the inhospitable planet AIM? Well an analysis year by year and it’s really only a handful in fact 17 stocks from the hostile planet AIM’s population of 1000+ is given after the following notes: Notes:

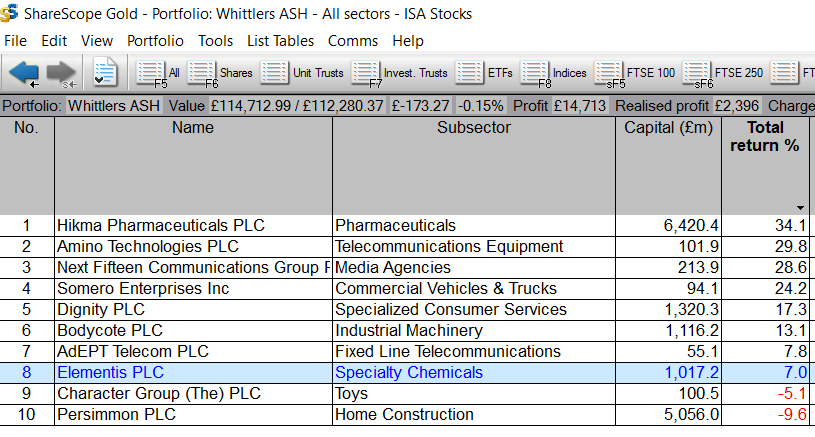

2012: no new stocks identified; just two identified and these are ones also identified in 2011/12, DTG and NICL that as a basket of only two gave an annual average performance of 56.6%pa compared to the AIM all share average over the same period of 2.8%pa over the four-year period. 2013: three new stocks identified along with three stocks identified from previous years. The average annual return of this basket of six stocks was 19.5%pa compared to the AIM all share of 0.7% pa. 2014: Only one new stock identified and two previously identified stocks again confirmed as currently meeting my return on capital/cash flow criteria. The average annual performance over each of the following two years for this basket was 12.2%pa compared to the AIM all share at 1.8%pa. 2015: Three new stocks identified and a basket performance of 14.3%pa over the year compared to the AIM all share of 4.6%pa. Over this period the strict financial screening of the inhabitants of planet AIM has worked very well for me and I have taken positions over the years in nine of the seventeen stocks identified for further consideration. I still hold legacy positions in all of the companies identified and also positions in companies identified over recent months. The AIM stocks that I currently hold that have been identified by my return on capital/cash flow screen are DTG, TEF, AMO, NFC, CCT, IGR, SOM, ZYT & ABDP (sadly a late addition, should have bought earlier!). One of the stocks TEF is currently going through some post-Brexit London property turbulence but I am confident enough to continue to hold. I certainly can’t predict what the future will hold; will TEF be loved again soon, will ZYT’s unpredictable order book lead to a profits warning, I simply don’t know. What I do know is that by taking considerable care with AIM stocks I can greatly increase my chances of enjoying sustainable returns from a basket of stocks from the dangerous planet AIM. Footnote: I should also say that I do also purchase other shares on AIM that don’t strictly align with my return on capital/cashflow criteria but these themselves such as Bioventix, Tristel, Cambria will qualify for a purchase due to other criteria but good cash flow will always be a requirement. We have now reached the first full half year of the Passive v Reactive Whittler portfolios so it’s time for a quick review to see how my meddling ;has done compared to Mr Cool who simply sits on his hands and lets time do the work. I have again restated the basic rules for the management of the portfolios; see the last section of this article. All of the ten stocks common to the three portfolios were identified via my routine free cash flow+ returns on capital screen i.e. they all exist within my whittled down universe from which I make the majority of my real life share purchases. At the time of this six month update, I hold positions in four of the ten companies: SOM, CCT, NFC & PSN. I also held Hikma as a spread bet so that’s a financial interest in 50% of the stocks within this exercise. Update & Trading in Half Year (Feb to July 2016): Of course following the rules of the exercise no trading took place in the 3YL (three year life portfolio) or the ASH (annual sit on hands) portfolios. Trading did take place in the Tinker portfolio and these are listed below: 1/2/2016: sale of 60% of position in Bodycote following a broker downgrade and the funds used to purchase further shares in Dignity. 1/3/2016: sale of 50% of position in Amino Technologies & the reinvesting of the proceeds in Somero following excellent preliminary results. As you can see there has been no additional alteration to the Tinker portfolio since the first quarters reported performance. My intention is to not just trade for the sake of it but to only trade as I would within my real-life portfolio. How are the three Portfolios doing? Well as 3YL & ASH are identical composition and allocation in the first year, they are identical with the original £100k now reaching £114.7k, a 14.7% increase in the first 6 months of the exercise. The Tinker with its two trades sits at £113.8k an increase of 13.8%. The comparator for “how are we doing” is the FTSE ASTR (ASX.TR) which rose by 14.6% in a generally volatile February to July period that included the once in a lifetime Brexit event and the following market turbulence. Overall, all of the three portfolios are performing well enough at this early stage: the five best performing stocks over the first half year of investment were:- Hikma Pharmaceuticals, Next Fifteen Communications, Amino Technologies, Somero Enterprises and Dignity The full performance of the 10 stocks is listed in the table below  Only two of the stocks so far are showing a loss as both Character Group (-5.1%) and house builder Persimmon (-9.65) took Brexit hits from which they are still hopefully recovering. Persimmon was particularly hard hit following the referendum and at one time was down by over 40%. Personally I took advantage of the Persimmon opportunity and added to my real life portfolio once the stock had started to recover.

Six Month Verdict In conclusion at the six month stage all portfolios are performing very well with the passive marginally ahead of the Tinker but such are the weekly movements, this is not really significant at this early stage. It will be interesting to see how the gap(s) show themselves as time moves on over the three years of the exercise. As an aside, I normally set a trailing stop loss on my stocks but never an automated one. Had I set an automated one i.e. one that reacts to any movement regardless of stock specific or general market turbulence effecting all stocks, the performance would have looked appreciably less favourable. With stop losses I set an initial 15-20% to allow the stock to breath and then as it hopefully appreciated in price convert to a trailing stop loss of 12-15% but NOT automated with my broker, the trailing stop losses are treated as advisory events that force me to take a reasoned decision. The original 15-20% stop loss set at the time of purchase are often acted upon in practice as a coldly admit I may have not got a particular trade right. Rule No1 limit your losses; rule No2 is simply remembering rule No1 and live by it. Happy Investing! Reminder Of The exercise Rules. The three portfolios will be firstly a buy and hold for three years, ploughing on regardless through economic conditions, profit warning and any other news either good or bad. I will call this the three year life portfolio (3YL). The only time a change to the portfolio will be permitted is if a business is de-listed for any reason: the funds liberated would then be discretionally invested between the remaining stocks in the portfolio. The second portfolio will start out with exactly the same holdings as the 3YL but each January the same cash flow screens/returns on assets screen will be run and a revised set of ten stocks nominated. This revised set of stocks will have the proceeds of the sale of the previous years stocks equally divided between them i.e after one year we have £110k of funds then a purchase of £11k will be made for each of the ten stocks. I will call this the annual sit on your hands portfolio (ASH). The third portfolio will again start the same as the 3YL & ASH portfolios but I will alter the percentage invested in each position within the portfolio in reaction to RNS announcements from the companies, economic conditions or any other reason that seem valid for altering, reducing or increasing a position. I will call this portfolio the managed annual tinker portfolio or simply the TINKER. All 10 stocks will remain within the portfolio throughout the year although the investment in each stock may vary. For example one stock, let’s say Hattersville Dream Co. may issue a particularly bullish RNS “results will be appreciably ahead of market expectations”. The Tinker may sell down one or more of the other holdings to invest more in Hattersville but still retain a position, although not equal positions, in the same 10 stocks that we started within January each year. In January 2017, 2018 & 2019, this portfolio would be treated in the exact same way as the ASH and funds equally balanced across the each of the ten stocks starting that year. The common rules for all three portfolios:

The year of 2013 was very productive with a staggering performance of the FTSE 250 with many companies, about a dozen as I recall, increasing in value by over 100% and another 30 increasing by some 50%. The FTSE 250 appreciated by some 26%; indeed only about 12% of the FTSE 250 declined in value during that sweet year. How good was 2013 when compared to other recent years? Well, maybe the best way to answer that is to take a look at the wider indices the FTSE All Share which itself gained 17% in 2013 whilst only one of the bracketing years of 2011, 12 & 2014, 15 gave a positive return. So where does this lead us? Well to my view it just shows that the majority of the time we exist in a stock picker's market. Yes, we can be risk averse and just simply go for an index tracker route or as I do, invest via the stock picking route. For myself, stock picking by and large has been for the best part of the last twenty years based on screening stocks (or may I say whittling) down the total universe of shares to come up with a relatively small number of shares for more in-depth investigation. My process had become more honed over recent years by the late 2000s; still seeking the usual characteristics such as increasing revenue/profits, sustainable and decent margin and little or at least manageable debt but I had upped my selectivity criteria in terms of one of my main criteria, return on capital. As I continued to hone my approach I developed a liking for CROCI in addition to ROCE as the former is calculated on cash as opposed to profits. I just think it gives me a slight additional edge. To a fairly minor extent, I tended to mix that approach with what I perceive to be value opportunities; areas that the market for whatever reason has passed over or overlooked. It often takes a long time for these value types to deliver and personally I find it helps to adopt the sunk money philosophy; don't fret just let the passing of time do it's stuff yet if it appears I have got it wrong, don't be stubborn, head for the exit. Anyway, back to what was going on around this time: All In all 2013 was a very good year for investors but in 2014 & 2015 various factors weighed on the markets including the Eurozone crisis with Greece, Spain and Italy niggling away at the markets combined with worries regarding China’s slowdown. Its just a fact of life that Mr Market always finds something to fret about. That's all part of the game but at least as individuals we can by whatever process we feel comfortable with, strive for an edge on the markets. Assuming I have approached some degree of wise maturity over the investment journey, I felt some analysis of what was going on in my entire investment portfolio over the period 2013 to 2016 may be worthwhile. Note: I only went back and analysed the 2013-2015 happenings purely because of writing my journey articles; just shows how useful doing something like this can be as it prompts a bit of self-analysis and to my experience, we are not very good at that. Over this three year period I owned about 120 stocks passing through or in some cases, still residing in my portfolio and a touch of detailed analysis from my ever reliable Sharescope shows the following from my combined trading and ISA accounts: Of course for various reasons, not all stock investments turn out to be a success in your desired timeframe. I like to think that I purchased stocks that following my methodology have a reasonable chance of succeeding within that reasonable time frame. The way of the investment world is that even attractive companies can encounter problems such as product delays, contract delays, consumer slowdown within their area, competition, economic events etc. Happily, my good purchases outweigh the ones that did not work out as planned, not only in terms of a number of stocks but also in terms of letting the winner continue to perform. At the same time I continually added to successful stocks upon encouraging RNS. Within reason and totally without a trace of emotion, I cut the poor performers early and run the good performers but of course like all investors, I don’t always get it right: simply part of the territory that comes with investing in the stock market. Over the last three years, I have been fortunate to hold businesses that have been the subject of a successful take over; I like to think this was because I had bought attractive businesses. Ones that did particularly well for me were:- Kentz Fiberweb Anite CSR In fact, I added bit by bit to Kentz over a reasonable period and it paid handsomely. Profits warnings over the period since 2013 to 2016: well there were 8 in total, all of which I cut & run quite swiftly. It’s interesting to note that 7 of these stocks went on to significantly decline further in value, hence sticking what works well for me i.e selling on the first profits warning and moving on. Unfortunately after one profits warning there seems to be a good chance of a second and sometimes a third. I realise that this is a particularly personal one for each investor and to a fair extent it depends on the type of stocks that one invests in but my get out quick works for me by limiting my losses. Incidentally of those eight companies at the time of writing only Shoe Zone, sold on PW in April 2015, has recovered to my sale price: the others continued to drift lower after I sold. It’s important to remember that it’s not just small companies that can continue to fall after a profits warning; I sold Stagecoach for a 14% loss on their December 2015 profits warning, it has since drifted to a price at the time of writing that would have given me a 45% loss. As I say, this approach of cut and run following a profits warning does the trick for me. If the stock once again looks attractive, I can always go back and buy in again. I sold Tristel first thing on the day of their February 2016 profits warning for 123p for a return of 70%; I like the company and bought back in at 96p in early July when I felt they had bottomed out yet still looked attractive and I like the business. Just because you may have sold on poor news does not mean that you can not revisit and purchase a stock again once things appear to be a touch better.   Profitable stocks I sold too early, yes we all have those, don’t we! Well out of the winners I would have done appreciably better to have held on longer for the ride: I am afraid that I sold the very impressive JD Sports way too early. I had a sizable position in JD and to be fair I made a very good return but on reflection, my reasoning for selling at the time was just not convincing. Similarly, I sold WH Smith the ultimate in boring stocks, the type I love, a touch too early for a 20% profit simply as I felt the price had stalled a touch: shame as there was another 30% in the tank. Similarly to profits warnings, I am not too proud to admit a mistake and bought back into JD Sports in following their Christmas 2015 trading update.

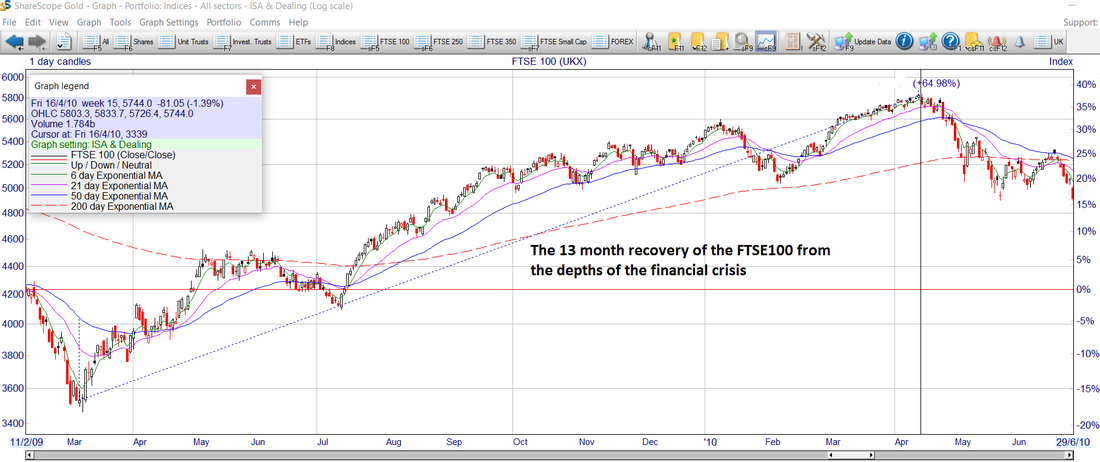

It is highly unlikely that I will have an abundance of those unicorns we know as 10 baggers in my portfolio these days, well unless I hold some real quality for many, many years, and I think that largely reflects the investment style that I have developed. To explain that further, the rapid rise 10 bagger type stocks are to my mind more associated with stocks with potential to become winners and possibly a touch more speculative than the stocks I currently deal with. I would guess that an investor would only come across those a few times in an investing lifetime and I have had some with the likes of Helphire many years ago. My style is to search for quality stocks that are currently winners and will hopefully stand a better than average chance of continuing to be winners. In terms of measuring my portfolio performance, unless I am doing something of a project style piece of work, I stick to assessing performance over a financial year or in reality over 3 to 5 years. A few years ago I was constantly assessing portfolio performance and in reality, for the majority of the time just seeing the effects of market noise which as I have said before I studiously strive to block out these days. So for me the major assessment is done at the end of the financial year this makes sense as it fits with CGT and ISA allowances. I really do not fret over the day to day valuation moves within my portfolio; personally checking over frequently just does not lead to a relaxed investor, at least as far as my personality is concerned. Actual performance over the financial years 2013, 14 & 15 has been very pleasing, well it has certainly kept me very happy as I deliver ahead of benchmarks far more demanding that the FTSE All-share total return. In fact I just don't understand why investors choose such a soft measure to assess their performance against. Reading investment books; as a scientist, I collect and assess information; I enjoy it and I guess I will never change. However, of all of the investment books I have read and it’s a lot, I would say only a very few merit the usual 200 or so pages that’s often dedicated to padding or waffle. This comment even applies to Joel Greenblatt’s book that could be slimmed down and called the Incredibly Little Book That Beats the Market. Just so many could have been condensed to say 20 or 30 pages to adequately get the message over but there again would the average person spend say £20 on such a short publication? Hang on, I feel another blog subject coming on here! I have mentioned before that a need to have a punt exists within me, after all, I am the guy who spent many an hour in the bookies in my earlier years searching for that perfect Yankee. I have been a very well behaved boy for quite a few years now with very few punts. At the time of writing this section, my last punt was Seeing Machines, I closed in early 2015 for a modest 15% profit; I am not sure I will continue to be good but at least I will try. Heavens I almost forgot to mention Twitter! I first opened a Twitter account back in 2011 simply to get the Luton Town FC team news an hour before kickoff time: rather nice to get advance footy news whilst in some local ale house sipping a pint of a local brew. It was not until the middle of 2015 that I had a look at some investment activity on Twitter; from there on in it developed for me and I met, albeit electronically, some very pleasant and genuine folk who go out of their way to help fellow investors. It’s a nice community and I am happy to be part of it. I post on Twitter usually in the early part of the day, around 7am, commenting on any RNS that may be loosely linked to a stock I have an interest in. I comment at the time of my Tweet if I have a holding in that particular business or if it’s on the watch list etc. At the time of penning these notes, June/July 2016, it's worth asking the question am I a better investor now than when I was investing say 15-20 years ago? Well I like to think so, I have learnt a lot and like all investors made my share of mistakes but on the whole most lessons have been digested and proved of benefit to me. The trick is to not repeat the same mistake time and again; so to that end, I don't punt stocks, follow tips from folk on social media/bulletin boards & when a purchase does not work out I cut my small losses very quickly. So after seven episodes, well eight really as I did a part 3a & 3b, my journey comes to a temporary pause and maybe in three or so years time I will give an update on progress. Oh, hang on, there is one more part I am working on that will be published in a week or two and that will take the form of a summary of what I have learnt during the 25+ years of stock market investing. I have enjoyed writing the journal and really feel that a touch of inward self-analysis is a good thing. Also, I hope that you have enjoyed my whittling on over the course of my investment journey; if there are any scraps in there that may be of help to others then I will have achieved my goal. Happy Investing. The recovery of the FTSE 100 from its March 2009 low of 3500 continued at a reasonable pace reaching 5800 in April 2010 a fairly remarkable increase of 63% in the major indices in little over a year. Some sectors were just going phenomenally well and in particular, house builders were simply rocketing. The likes of Barratt Developments, Taylor Wimpy that had seen a 95% fall in its value over the financial crisis had regained a significant portion of their loss but were still some 80% down from their pre-financial crisis share price; a real measure of the rout that had occurred in some sectors. I wish I had invested in more house builders at the time but unfortunately had only invested in one, the partly bombed out AIM listed Telford homes in 2009 which were doing well enough over this period and in the construction sector another love-hate stock Costain. Is it not strange that somehow we all have a share or so in our portfolio whos figures and outlook say the right things yet continually frustrate and disappoint in terms of stock price appreciation. Yet we have that almost certain knowledge that should we sell the stock it will immediately appreciate in value.  I may not have realised it at the time but the trauma of the two FTSE collapses was having an effect on my investment approach as we began our recovery from the lows on 2009. I found myself becoming more cautious than at any other time during my investing career and holding a far greater percentage of unproductive cash in my portfolio than pre-2008 I would have envisaged. To my mind, I had had my luck, possibly my degree of good fortune in terms of exiting both the 2000 & 2008 market routs with appreciably more money than I had in 1997 & 2003, the productive years before the two collapses. Whilst I exited on both occasions with worthwhile profits, of course, they were way off the high of the paper profits at the pre-fall respective peaks. Would my luck hold in future in wondered? In my day job, I had a meeting with my Director early in early 2010 to explain my plan to leave the comfort of employment and do something else. I wanted to be as fair as I could and inform them 12 months in advance of my intention to leave the pastime of full-time employment. As it turned out there was a touch more negotiation in the wind and my eventual departure came about some 21 months later rather than the planned 12 months. I was fairly relaxed about the situation as I wanted to be as fair as I possibly could to a company that had been such a big part of my life. Where does this fit within my investment journey? Well, it was always my plan to become something of a full time investor whilst enjoying the comfort of a good company pension and also the final 21 months of employment meant that I could invest a ridiculously high percentage of my salary in my AVC pot; 40% tax gift at best and why not take it! During the period 2009 to 2012 a fair proportion of my investments could I suppose be described as the safe type; Astra Zeneca, AMEC, Aberdeen Asset Management, BP, Centrica, National Grid, ITV, Tate & Lyle, CSR & SKY. Well, I should say supposedly I mean after the experiences with the likes of Barclays and Northern Rock, in reality, what was safe? Certainly, BP started to look a little less than safe when news broke of the problems in the Gulf of Mexico with their rig Deepwater Horizon. To me, things looked pretty bad and my mind went straight to the potential environmental impact that the incident may have and the mauling that BP could get from US litigation: in a quick decision I sold way before the eventual bottom of the share price plunge. I had over the years developed the approach that if something really does look wrong with a share, then just don’t sit on your hands but consider the risks and potential further downside. Once sold, there is always the option to purchase again. The overall portfolio was ticking along well enough but I did start to feel a little envious of a mate who was doing really nicely in oilers. Now for whatever reason exploration oil companies or indeed any natural resource exploration business had never really been my thing, just not the speculative stuff I felt comfortable with I suppose an element of greed persuaded me to take a couple of small positions in Gulf Keystone Petroleum and Rockhopper Exploration. Immediately I bought then I felt out of my comfort zone: what the heck was I doing buying two popular and massively ramped bulletin board darlings; one stock in unstable Iraq and one working in the inhospitable deep water off the Falkland Isles. Well maybe these exploitation companies were not that bad after all as both share prices started to appreciate fairly rapidly; was this to be a touch of excitement to spice up my portfolio? When the news of the Fukushima disaster broke the uranium exploration companies were hit very badly. Taking my mind off my trusted fundamentals, I reasoned that this uranium crash was surely only going to be temporary after all unless we used uranium wisely the lights around the world would simply go out at some time in the future. I decided to speculate a very small amount of my portfolio on a couple of uranium exploitation companies listed on the Australian market. This mixed bag of punts into resource exploration stocks did not improve my overall portfolio performance; I made a small profit from the oilers but the uranium punts made fairly small yet annoying losses. Whilst I did not consider myself as a hugely successful investor, I was doing fairly decently yet one thing I seemed to have in common with many investors, even some well known successful UK investors that I greatly admire, was the inbuilt ability to occasionally abandon investment principles and have that wayward punt. I could understand it with myself as I had the suppressed gambler inside of me, the chap from earlier years who had spent hours at the bookies searching for the ultimate Yankee; yet why did really smart investors with incredibly sound financial backgrounds occasionally drift off course and have a punt? Around this time, probably 2010, I had been reading a couple of books covering the subject of FOREX trading and whilst accepting the risks involved, decided to allocate a few £k to the venture. This I would not really describe as a punt as I had a well worked out a financial management plan. I realised from the material I had been reading that the key was managing risk and indeed only risking a small percentage of your allocated FOREX dedicated post on each individual trade. To my amazement after a few months I was considerably ahead; I had latched onto the reasonable length trends of some currency pairs and in particular had success in trading the GBP/NZD, not the most widely traded currency pair but certainly one that worked for me. The trouble was that I was reading so many articles about the high risk of currency trading that I eventually decided that it was best to get out whilst in very good profit and in truth never returned to that investment area but maybe one day! I continued to invest in the more sensible fundamental companies at the time; buying solid growth business such as Staffline Recruitment, purchasing more SDL and Fisher. I also started to search for trending shares, ones with a predictable way moving and bouncing over time between support and resistance. One particular gem in this area that served me well was the incredibly predictable Morrison supermarket whose price bounced off support and resistance every few months for several years.   For a couple of years after leaving employment, I spent time travelling around the globe. A couple of winters taking the slow route to Australia and an equally slow route back were really enjoyable. I was armed with my laptop in order to keep tabs on my investments and of course follow my football club which I was greatly missing; a serious downside to escaping winter. Listening to football commentary at about 3o’clock in the morning in Perth or Adelaide is not really that relaxing on reflection but that’s addiction! So, more steps had been taken on the lifelong investment path. Had I learnt any more lessons to add to this that I listed in part 4 of my journey? Well yes:

Well, things had been chugging along well enough since the Iraq invasion back in early 2003 and by the end of 2007, the portfolio was looking in a very healthy state. I was really enjoying my investment life almost more so than my professional life. I was employed by an excellent company, essentially the same company for over thirty years. I had grown within that company, my career flourished and I had in truth been far more successful than my humble ambitions ever warranted. However, as with all big companies, there is forever a need of the various CEO’s to own a cultural change within a business. In truth, many such changes are simply the previous sets just repackaged and delivered by another group of consultants. Now I am not saying this is necessarily something that would put anybody off within a business but in my case, I felt like I had been on the roundabout too long and the desire to jump through the same or similar hoops was simply diminishing. I decided that I needed to accelerate my AVC contributions vastly and laid a plan to retire early from science no later than 2011 and become essentially a full-time investor. Heavens, just think I could still be employed in what is still honestly a wonderful company but I just do not miss the performing tricks part of company culture one bit. Well, the plan was set in place and the finances carefully arranged; the stock market had been kind to me but as we reached the end of 2007 a few little dark clouds started to appear on the distant horizon; namely chatter about banks in the USA made loans to citizens that were unlikely to be paid. The area of main concern was sub-prime mortgages if effect the banks were making loans to people who did not stand a realistic chance of coping with that loan. Alfie, a colleague who dabbled in shares and was rather like an Italian version of Private Frazer from Dad’s Army, came bounding into my office to tell me “toxic debt mate, I tell you it’s really bad, really bad”: what is it this toxic debt stuff Alf, I asked, “don’t know mate, but I tell you it is really bad” replied Alfie. That conversation was typical of the time as we rapidly entered a period when everybody used the term toxic debt and fast became a financial expert. However, in common with all experts associated with the financial world at the time, nobody really had a clue about what was wrong, who it affected or indeed the eventual magnitude of that effect. One of the first UK banks to have the jitters was Northern Rock. Foolishly to me at the time it looked a bargain and I added a few into my ISA only to sell them nine days later for a 30% loss after the news reported massive queues of customers wanting to withdraw their cash from the bank despite the government pledge to guarantee savings up to £80k . Had I waited a short while longer, my loss would have been greater than 85%; decisive swift action or luck, I don’t know but at least my loss had been limited. It felt like a Groundhog Day moment, "Déjà vu all over again", surely the market declining pattern of early 2000 was not about to be repeated; no, surely not!  Feeling I had been in this place before, I quickly went on a massive selling spree getting rid of just about everything within my portfolio and turning to the relative safety of cash. My portfolio had taken a battering and a significant portion of my paper profits made over that four year period 2003 to 2007, had been reduced but at least I would live to fight another day. I watched from the sidelines as the FTSE once again relentlessly ground its way down to its comfort zone of 3500. The bottom was eventually found in March 2009. However, even as we hit the bottom of the market, it seemed that the world was doomed as pockets of the nasty toxic debt stuff continued to be discovered all around the globe within all sorts of financial institutions.  Once again I felt that I had been relatively fortunate compared to some. Indeed good old Alfie, the very man who preached how bad things were with toxic debts 12 months ago, came to see me with a tale that completely threw me. It turned out that Alfie’s parents had invested just about just about all of their “comfort in later life funds” into Lloyds bank shares and were now feeling quite understandably frantic; they were both in their 60’s. Why, I wondered, had Alfie the man who was going on about toxic debt some 12 months ago not had that discussion with his parents? There were other horror stories about at the time such as investors who had taken up significant positions in small companies and finding that they were just unable to sell them with any degree of ease. In effect they were taking severe hits as spreads widened and market maker showed reluctance to anything but small batches of stock; overall 2008 was a very unpleasant time and a time that just drained the confidence from many an investor. Personally, I vowed that I would never again include banks within my portfolio. To this day, I just wonder how the banks and other financial institutions could have behaved in such an irresponsible and stupid way to create the catalyst for a world recession. I had just been exposed to my second really serious bear market/recession, there had been previous relatively minor downturns earlier in my investment life but nothing like the 2000 and 2008 downturn which saw the FTSE 100 & FTSE 250 just about half on each occasion: character building stuff you might think but I could do without it. My friend Bob, the one with unflappable loyalty to his technology stocks that eventually became penny shares, had decided that he would now only invest in an area he understood; that being utility companies and in particular water companies. As it turned out this was a wise decision by Bob. Water companies although not immune to the global downturn paid very good dividends, had a captive customer base and the need for the product, water, would never go away as you can’t live without it. In effect, Bob had found his investment universe, an area he felt totally comfortable with and had some expertise within. My leave the rat race plan was still intact albeit a little bruised. The AVC contributions were increased further and I was determined to stick with the plan to eventually become a full-time investor. I was sitting on a comfortable cash pile in my ISA and trading accounts but physiologically felt a little damaged after those two severe bear markets. However, little did I know that we were about to enter a golden period for investment as the world gradually awoke from its financial crises nightmare. I gently started to move some cash back into the markets buying mainly liquid stocks such as Astra Zeneca, Aberdeen Asset Management, BP, Centrica, National Grid, ITV, Tate & Lyle, CSR, Costain, the return to old favourites James Fisher, GSK, Green King (how could I desert my Abbot), plus other FTSE 250 companies. Additionally, I took some more risky positions in a few smaller companies: Character Gp, Goals Soccer Centres, Harvey Nash. As the clock ticked it’s was to midnight on the last day of 2009 I reflected on how things looked some ten years earlier on new year’s eve 1999; two almighty stock market recessions and a lot had been learnt on my part as an investor. Was this investment lark really worthwhile? Would this steady group of stocks now within my portfolio be sufficiently safe to get the wheels going on the portfolio again I wondered? Well as we headed toward the end of 2010 the signs were looking fairly optimistic but who knows what the future holds; for sure Mystic Meg had hardly developed a reputation for being successful over many years in predicting the future: without a crystal ball, what chance did I have?  The journey continues! When we invest in companies we do so with the view of making some sort of hopefully decent return on the capital we have risked. If we are absolutely honest with ourselves not all of our investment decisions result in success. In fact, I would feel that if the average investor actually analysed the individual success rate of each of their investment decisions over a few years, that there is likely to be a significant number of decisions that did not turn out anywhere near as originally planned. Our investment in a stock may decline for a number of reasons; the overall market may be bearish, sentiment to a sector or individual stock may not be favourable or the company is not progressing as anticipated. Within the not as anticipated category, we have the dreaded profits warning that we see within an RNS at 7:00 am when a company tells us that profits are going to be less than the market/company had expected. The warning may come in various flavours i.e. “profits for the year xxyy will be significantly/materially lower than previously indicated” or maybe a milder warning “profits will be at the lower end of analysts expectations”. Either way, it’s not going to bring immediate joy to the portfolio but it’s something all investors will experience. The key thing is in my view how do you deal with it; oh and by the way “head in the sand” is not a serious option in my book. Personally, I have a natural scepticism of CEOs especially the ones of smaller companies as they often have a tendency to be over-optimistic and paint a brighter picture than actually exists at the time of the profits warning. If we are unlucky, then the initial profits warning may well not be the only one that that company issues; with small companies they can have a habit of coming in threes. My scepticism together with many years of character building whilst learning in the school of hard knocks moulded my approach to dealing with warnings. My general stance with a profits warning is to simply sell at the earliest opportunity unless there is a compelling reason that suggests to me that things will really get better quickly and the warning is to a large extent outside of the companies control e.g. at the lower end of expectations due to unfavourable currency exchange; not a great worry in my view. What I am actually trying to do when I sell into a profits warning is to simply reduce the risk of further loss of capital and hopefully retain that capital to invest in a stock that has better apparent potential. So let’s have a look at the six profits warnings my overall portfolio has suffered these past three years, note It’s actually 7 if I include yesterday’s warning from Portmeirion which I had sold by 10:00 am, but time will tell how that one pans out:

Notes:

the % change on buy to sell is simply the profit or loss on that transaction. the SR is the Stockopedia stock rank on the day of the RNS/profits warning Overall taking a hit and selling as the closing price on the day of the warning would have resulted in an average loss of -21%: in practice as I tend to sell early after opening, the loss is usually appreciably less that the close of day % fall I show in the above table. Hanging on in hope for six months would have increased the % fall from the RNS warning day to an average of -49% and holding on for 12 months (or 9 in the case of GMS) increases the average fall to -61%. My inclusion of the Stockopedia SR is in no way a criticism of that fine system but merely a demonstration of the fact that the above stocks would be seen as attractive at the time of the profits warning; we are not talking about dodgy stocks. As with everything I write on this blog, it’s not advice just me sharing what I have learnt over the years and generally what works for me. Edit: Missed one: I also owned TSTL which gave a profits warning on 24/02/2016. At the time TSTL had a SR of 81. I sold early in the day at 124p, the price on opening was 143.5p. The price had drifted by the end of the profits warning day to 109p, a 25% fall on the day. Today, TSTL is standing at 91.5p which is a 38% fall from the opening price on profits warning day; that is 5 months later. Overall a good investment for me in getting out early on the warning and I made a profit of 67%. Happy investing! Don’t you just hate it on the daily routine of looking at RNS’s for companies in which you have a holding issue the dreaded words that appear in colour on your chosen highlighter. Well this morning a company I have held stock in for a fair while and added to just a few months back, issued the following: Total revenue for 2016 is expected to be ahead of 2015, notably because of the recent acquisition of the Wax Lyrical business. However, pre-tax profits are expected to be materially below the record level of £8.6 million reported for 2015. At the Annual General Meeting, we reported an unexpected decrease in demand from Asian markets. In particular, sales to South Korea still show no signs of recovery and the performance of our distributor in India has continued to be extremely disappointing. In addition, we have seen negative effects on demand in the UK before and following the leave vote at the EU referendum. The potential benefits of a weaker pound have yet to translate into firm overseas orders. However, the United States continues to perform well. That phrase materially below, never sits well with me but such is life particularly with smaller companies; simply a part of the inherent risk/reward we have to live with when investing in the small market capitalisation stocks. Now my normal practice on a profits warning is to ask myself the question every 10 seconds for 30 seconds and just about always come up with the same rapid answer of SELL. It has served me well in the past and certainly limited losses indeed since commencing writing about my buys and sells in this blog, swift action got me out of Sprue Regis at 185p; they subsequently fell to 120p and have as of today, partly recovered to 145p. I appreciate this approach is not for everybody but experience over the years has taught me to bail out as soon as I can on a profits warning thus hopefully limiting my losses. If I get it wrong and the company subsequently start to recover and the fundamentals still appeal, then I can always buy back in again. Returning to today’s announcement from Portmeirion, I went back through recent trading updates and their final results issued on 19th March 2016. What I wanted to do was to take a good look at the geographic spread of their sales:

So we have the USA which is doing ok, the UK was doing ok but already seeing signs of a pre & post-Brexit slowdown, South Korea not recovering as previously planned and India, last year’s star, now listed as “distributor continued to be extremely disappointing”. Wax Lyrical, the recent acquisition, is also mentioned and credited for the reason for 2016 revenue being ahead that of 2015. Now Wax Lyrical was to my mind a decent bolt on acquisition but the thought that it really struggled through the last downturn did not quite light that candle for me.

All in all, I took the decision to sell. My initial purchase was at £6.50 but the top up at £11.40 so overall a minor kick on the portfolio but even though I am heavily in cash at the moment, I expect that these minor kicks to become fairly frequent over the next two or three years of political turmoil as the “baby boomers lead us to salvation in a chorus of land of hope and glory”. Yes, I am very bearish at the moment. I actually think in three years time we will be absolutely fine, maybe even stronger than had we remained within the EU, but for the moment I am a bear looking at a potentially painful and unsure path to the future. As I came away from the eventual .COM carnage I started to realise that overall I had done reasonably well from that particular episode. I exited that couple of years with appreciably more funds than when I had entered but still felt that self-critical nagging that if only I had sold some of those high fliers earlier; maybe even got out at the top. As it happens I had learnt from my earlier experiences that once a good thing starts to come to an end, get out. On reflection although I had made money, I had not been that clever at all: I had really been a member of the herd running into IT stocks as if nothing else existed and in truth setting aside my earlier learning of trying to find and analyse growth companies that actually turned in profits year after year: it was time to head back to that base.  So my approach from late 2000 was to revert back to trying to identify Zulu type growth companies but this time around it just did not seem so easy; it’s a simple fact that when the market is in a depressed mood even apparent high-quality businesses are held back. I was finding it a real battle to make much of an impact against a background of a steadily declining FTSE 100 that gradually fell from a high of about 6950 at the start of 2000 to a low point of 3300 in early 2003: times were tough and I was being ever cautious and sat on a fair cash-pile. From 2000 to 2002 I did not really make any significant money from the overall basket of stocks that I held; investment life was difficult as the FTSE ground out it’s slow yet relentless path to the eventual bottom. I suppose that I was managing to “hold my own” was down to much greater care than in the .COM herd time. Yet, I still kept beating myself up: hey, I was this kiddie who could do 40% a year in the late 90’s, why won’t it happen now? Yes, I know, on reflection plain delusion of an investor who had become accustomed to making easy money during the last half of the 1990’s. Incidentally during 2000 to 2002 was one of my busiest times in my working life, coupled with the fact that I had moved home into a very old building that became a restoration project, meant that I just did not have much time to meddle. The lack of trading in itself became a real lesson i.e. if you have done some decent research, limited risk by going for quality, then the best friend may well be time in the market. Also at this time funds were needed on the restoration project; the complete re-thatching of a large roof is a jaw-dropping cost but I guess that was a wise use of some of my previous market gains.  That dreaded herd mentality was definitely something I wanted to try and avoid in the future if at all possible. My stock purchases at this time were mostly those with potential for growth but also supplemented by ones that paid a decent yield hopefully to protect the downside and of course the majority of my detective/screening work would be via my trusty Company REFS which thankfully became available in a CD form. There were a few gems that I picked up in 2001/02 as VP at 92p, Wolverhampton & Dudley at an equivalent of just over a pound in today’s money, Fisher(James) and Clarkson both at under £2. Just to give a flavour, my ISA & PEP accounts, yes they were separate in those days also included Hardy & Hanson, Greene King, Scottish & Newcastle, Prudential, Scottish Power, Azlan, Dairy Crest and Vodafone. Not a massive number of stocks but many of which I held onto for a few years and mostly rewarded my loyalty by becoming real stars which is more than I can say for Vodafone post the costly Mannesmann acquisition; the Vodafone performance proved a real drag on the overall portfolio. My mindset wanted to control risk in my ISA/PEP world and do the more risky stuff within my trading account; the logic being that at least I could recoup a percentage of the sillies via CGT offset. In addition to the continued retracement after the .Com bubble there were, of course, worries when our old buddy Sadam had squirrelled away copious amounts of what became known as WMD. Thankfully, at least for investors, the Iraq question came to something of an end in early 2003 when we had the invasion of Iraq and Baghdad bounce. What a lovely time that was as we moved away from the cliff edge and into a beautiful incline FTSE 100 & FTSE 250 that would last for about five years. The portfolio was chugging along really decently, no 40% years but the pot was larger and making respectable gains. Frustratingly over the period from 2003 to 2007, although I was making decent returns, for the first time in my investment journey I was falling behind the gains I would have enjoyed had I simply invested in the entire FTSE 250. Was I meddling too much or over trading? Maybe accepting a larger portion of risk with some AIM stocks: would I have been better off avoiding risky AIM stocks, just buying quality growth stocks and sitting on my fiddling hands? The answer is I don’t really think I will ever know for definite but I suspect the sitting on hands bit would have won the day. As work quietened down a touch and the heavy time demanding house renovation eased, I had more time available, more time to research REFS for quality & growth; that was good but conversely, I also had the time to again chase a few story stocks in my dealing (non-ISA) accounts. The stocks making me profits after 2003 was quality stuff such as VP, Fisher, Clarkson, SDL, AMEC, Peacock, loads of breweries; I probably held stock in the majority of breweries at various times when I think back and let’s not forget banks and insurance companies. Yet it was the silly adventurous purchases mainly on AIM that kept my acceptable enough performance below that of the run-away FTSE 250. I was probably spending too much time reading about “hot stocks” on bulletin boards, a hot tip in IC or some other publication. Remember the “next big thing” types, the likes of Aerobox, Accident Exchange Group, Inion, Media Square, Bioprogress ; the inventors of the dissolvable colostomy bag, I mean can you imagine!. Still, I did learn valuable lessons from my BB experiences and just vowed never to get sucked in again by those claiming to be ITK; I was also bolting on to my armoury the knowledge that debt can be a killer to a small business. Although this list of adventurous “next big thing” AIM stocks did not help portfolio progress they were mainly either cut at a 20% loss or on the first profits warning; to my mind valuable lessons that remain bolted onto mindset from that time onwards. Incidentally, a lesson for every investor to my mind is to have a decent number of reasonably diversified companies and concentrate on the overall basket performance. If you have to “gamble around the edges” then do this with a very limited percentage of your overall pot outside of your tax-free account; better still, if you need that style of excitement take up bungee jumping, glider flying or some other less dangerous pastime. Within my “day job”, my own company, whose performance I never counted within my percentage returns as that was simply my good fortune of being in the right place at the right time, was bought out for almost £16 in 2006 by a consortium of Canadian and Australian insurance/pension companies. I was a very happy man as I had studiously taken up almost to the limit, every share-save offer with prices ranging from £2 to £6: I was just gob-smacked by the eventual return of funds. Totally no skill involved apart from the discipline of maintaining the continual drip feed purchase of AWG shares at an advantageous price and very importantly, the passage of time, in fact, lots & lots of time. By mid 2007 the whole investment world was buzzing along cheerfully enough for me as I was close to being fully invested not solely in growth stocks but also in those lovely safe financial institutions namely the large unexciting insurance companies plus various banks including the newly listed ex-building society types; what lovely safe dividends these boys paid; I thought at the time what could possibly go wrong to rock this steady little investment world that I enjoyed? Epilogue: Learning Points as at December 2007

Memo to myself in late 2007: Learning Points so far that I would do well to remember but being as fallible as the next person, would almost certainly temporarily forget from time to time:

|

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed