|

Oh dear, this investment lark can be a worry. Well, I need to qualify that remark as it’s not so much a worry with my own money as I understand the risks about stock market investment and I am happy enough with those risks. What is a worry is discussing possible ways to invest a spare few £000’s that a close relative may have tucked away under the mattress. Anyway, such a discussion came up recently with a relative who had a few thousand pounds totally frustrating him as it was essentially doing nothing for him in terms of increasing the size of his wealth. For reasons of amusement and anonymity of the said relative, I will describe the tale in a story style conversation. Oh yes, before I do that I had better give the relative a name to spare his blushes; I will call him Matt and of course his surname will be Ress; come on keep up, MattRess, got it! So onto the conversation:- Well, Matt comes along to see me after much worry about his investments that are sitting in a simple interest account at his bank. Matt is really frustrated as in total on this spare £15000 he is earning in the order of £130 a year interest which in real terms he considers to be an erosion of this spare chunk of cash. Matt asks my advice regarding what he should do with such an amount of cash to make the cash work harder for him and make at least a decent return of his cash. Well, no surprises there as the answer is simple “sorry Matt I never give advice to others regarding investments”. Of course, Matt was very frustrated with my blank & closed response, this was not at all what he was looking for from his once favourite uncle who was becoming less of a favourite by the minute. I then reasoned with Matt that at least having his money where it sits at the moment does not expose that money to any real risks other than the bank going bust but even then he would eventually get all of his money back. Now Matt was not going to let this one go away and asked my general views on investment that fits with my character. Ok, I said but let me give you a little old fashioned advice in bullet point form below:

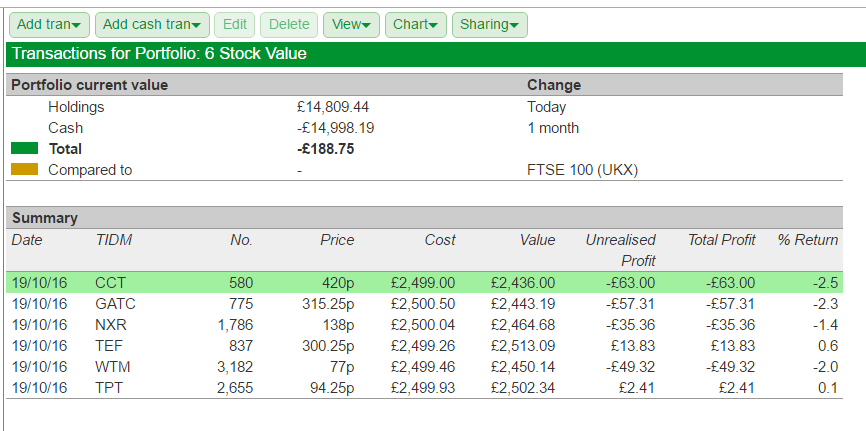

To spread the risk, we will in this practice portfolio have six stocks; why six? Well, Matt, it’s to spread the risk. For example if one company comes out with a dreaded profits warning and the share price immediately falls by 25% that would be a bit of a disaster if you only held that one share. However, if that share was one of a number within a basket of shares, in our example six shares, the overall hit on the portfolio would be much, much less, say about 4%. Ok, Matt said, as he grasped that point but then went on to say won't that have the opposite effect if one of your shares goes up by 25%? Well, of course, it will but this is what we call risk management: remember that greed can kill! So, on we went to create this portfolio investing a hypothetical £2500 in each of the following six stocks: Character Group (CCT), Gattaca (GATC), Norcros (NXR), Telford Homes (TEF), Topps Tiles (TPT) and Waterman (WTM). Once we had entered our “buys” into SharePad and taken account of those odd little annoyances such as the bid/offer spread, the brokers charge (even at a bargain £5) and the stamp duty of 0.5% on main-market listed shares (we don’t pay stamp duty as a rule on AIM shares) Matt’s portfolio of pretend £15000 cash had already fallen an amazing £280 in value without any real movement in the prices of these shares. Oh hell, said Matt that’s equivalent to a weeks holiday in Benidorm. Ok, I did go on to tell Matt that all things being equal and assuming that the stock prices remained stable for the next 12 months he would receive a theoretical batch of dividends of about £780 that could, with luck leave him £500 better off. By the look on Matt’s face, I could tell he was a worried chap, all of this risk for maybe making £500 in dividends and that in itself could be badly hit if one or more of these companies hits a really rough patch. Matt’s final words were to say that he was glad it was only pretend money and not his own as the thought of actually losing money was not one that appealed to him greatly. So, we will leave it there for now and come back shortly for another chat with Matt as his education continues.Well, we were going to do just that but as Matt looks at the screen his “losses” have now in a few minutes have shrunk to only -£188. How can that be, asked Matt? Well, Matt, I said, the stock market is a dynamic beast; it moves all of the time and the tool we need to use is one called patience. One great investor famously said “I make more money simply sitting on my hands and being patient”: do you think you would be comfortable showing patience Matt? Matt’s “portfolio valuation” a couple of hours after creation is now given in the SharePad table below:  Note: I should point out that as well as researching this batch of stocks, I currently hold positions in all six stocks mentioned in this article. However, my risk balance for any of these six stocks is actually much more favourable than in Matt’s portfolio as the size of my basket is currently 36 stocks. So should any one stock suffer the dreaded profits warning and slide by 25% then it’s effect on the overall portfolio would be no more than an annoyance.

3 Comments

Deep&Crisp&Even

12/8/2016 12:37:26 pm

Do you really think that most people lose money investing ? What do you base that on ?

Hi Steve,

DEEP&CRISP&EVEN

12/9/2016 02:35:01 pm

Ah, the Conkers Corner. Most of the podcasts are excellent. One recent one was awful - he could not get a word in edgeways. Your comment will be posted after it is approved.

Leave a Reply. |

Welcome to my Blog Page - I hope you find my whittling on to be of some interest. I am a private investor who is happy to share thoughts on the market and individual stocks. Please remember that I am definitely not offering tips or investment advice. Archives

June 2019

Categories

All

|

RSS Feed

RSS Feed