|

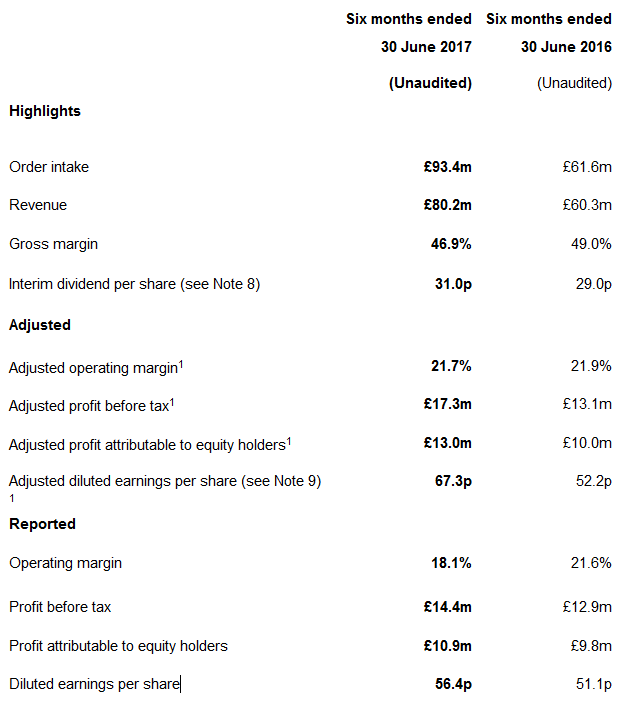

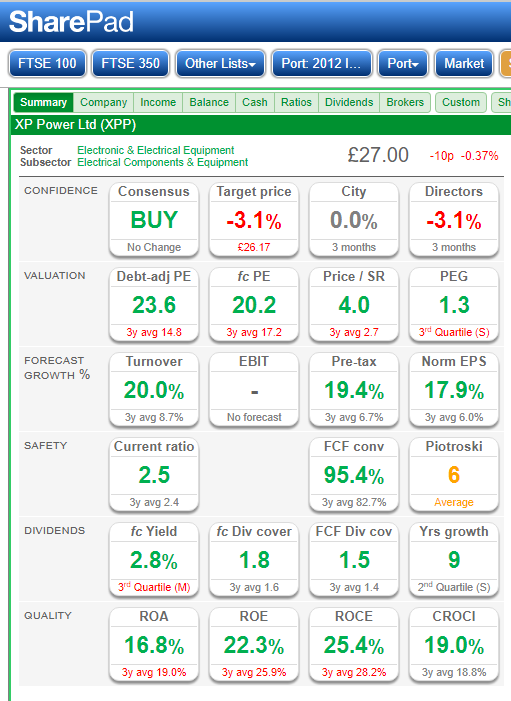

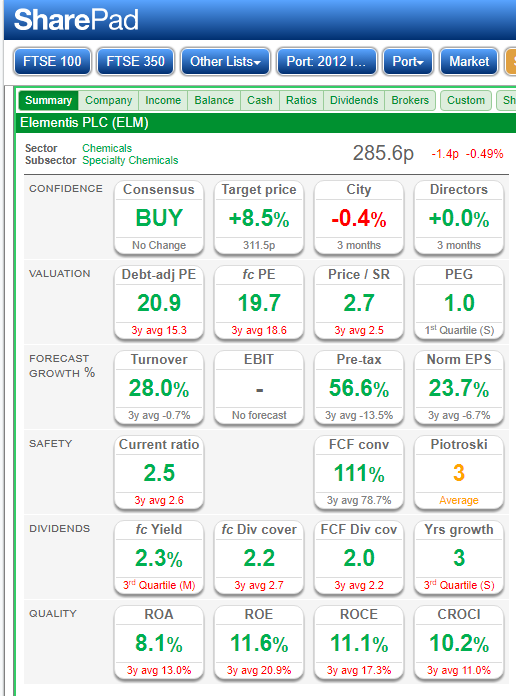

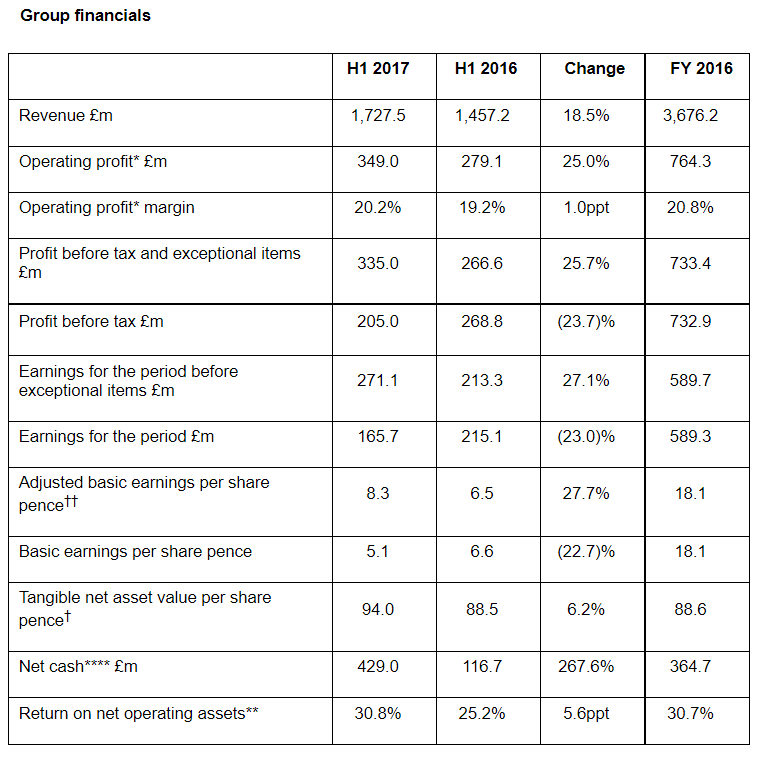

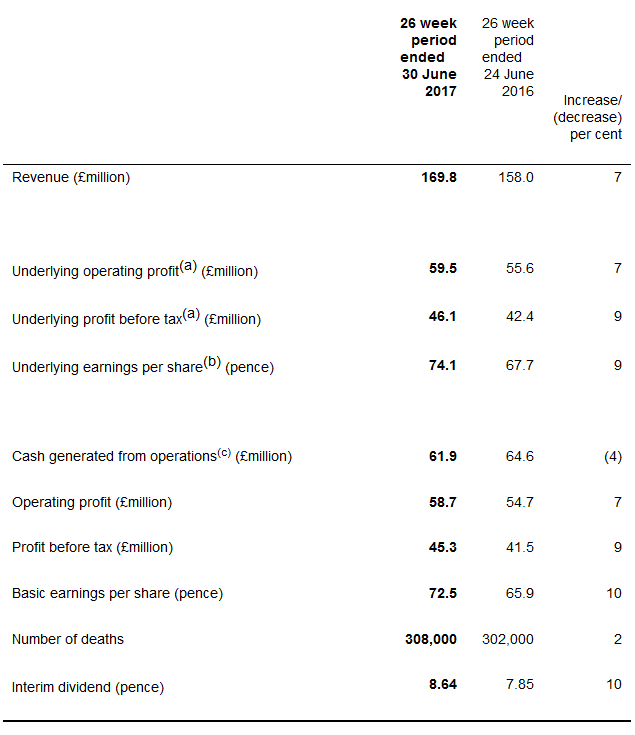

Week No 4 of The Voyager RNS Log Note: straight lifts from each RNS are in italics and my scribbling in normal text. Monday 31/07/2017: XPP: Market Cap £529m: Interim Results. The interims read very well:  Adjusted for intangibles amortisation of £0.1 million (1H 2016: £0.1 million), £2.8 million (1H 2016: £0.1 million) of advisory and aborted acquisitions costs and £0.8 million (1H 2016: Nil) tax deduction related to the aborted acquisitions. The Outlook in the XPP statement also makes very positive noises providing reassurance and promise of more growth to come: “We have made a very strong start to 2017 and the momentum experienced in the second half of 2016 has accelerated in the first half of the current year. We had a strong book-to-bill ratio in the first half of 2017 of 1.16 and a customer order book of £70.9 million. We are confident that our new product releases and design wins over the last few years are supporting our revenue growth. While we remain conscious of potential macroeconomic challenges, the combination of these factors means that the Board now anticipates the Group’s performance for the full year will be comfortably ahead of its existing expectations”. “The Group has a strong balance sheet which places us in an excellent position to make selective acquisitions to further broaden our product offering and engineering capabilities. We believe we are now well along the path to achieving our vision of becoming the first choice power solutions provider to our existing and target customer base”. The figures do use the suspect word “adjusted” but the notes gives a degree of explanation up front and I would say no reasons for concern there. Again up-front, the script does explain openly the positive effect that the decrease in the value in the pound has had for the business “Approximately 81% of our revenues are denominated in US Dollars and the translation of these revenues into Sterling for reporting purposes has had a beneficial effect. However, the majority of our cost of sales and a large proportion of our operating expenses are also denominated in US Dollars for which the translation into Sterling has a negative impact, thereby significantly dampening any effect on the operating margin”. I did a write up about the purchase of XPP back in April 2016 and at the time I was fairly optimistic about the company's prospects & indeed it turned out to be a decent purchase plus also offers a very decent yield that is comfortably covered by FCF.   Incidentally, there is an interim results presentation involving Duncan Penny CEO of XPP and Jonathan Rhodes FID; well worth a watch on the XPP web site. My View: I liked the company when I purchased into it in April 2016 and still like the company. I also like the degree of clarity in the way the results are presented. Where do we go from here? Well, I suspect there will be some broker upgrades to follow which in the medium term should keep a touch of a tail wind with the shares; I may consider a top up shortly as I just adore expressions such as comfortably ahead of its existing expectations. 31/07/2017: Revolution Bars Group: RBG: Market Cap £88m but subject to significant daily change!: Statement Re: Possible Offer. A bit surreal this one and worth a note I suspect from myself. I originally bought into RBG in January this year but following an announcement that the second CFO in a few months had declared he was leaving the business I sold my entire holding; 2 x CFO’s leaving in a short space of time just did not sit well with me. A few months later, May 2017, RBG duly issued a profits warning and the shares were absolutely caned eventually bottoming at about 50% of the pre-profits warning price in early July: hardly surprising as management credibility had declined and with it the trust on many investors. On Tuesday last week, RBG issued a very reassuring trading statement and it appeared the new CFO had brought a bit of sanity and reassurance to the business. I pondered for a couple of days and then bought back in on Friday afternoon. The reason behind the purchase was simply the prospect of recovery of the share price. Now I should say that I would think that 80% or more of my stock purchases are based on seeking strong cash-flow accompanied by impressive ROCE/CROCI but I also do purchase what may be termed as value positions/recovery situations and simply by good fortune, these can become the subject of a bid: seen recently with my Lavendon & Waterman holdings. I think with LVD & WTM it was a case of being patient waiting for recovery and pleasingly they were eventually the subject of successful takeovers. In the case of RBG it was again waiting for recover as the new CFO got to grips with the finances and I expected this could yield results in maybe 12 months: the possible bid coming in on Monday 31/07/2017 was purely really good fortune on my part and I take little credit for that potential windfall, sometimes Lady Luck smiles on you but you can bet your boots that that same Lady Luck will balance things out at some time in the future and give me a kick up the rear. Incidentally, other shares that I hold that currently sit under the value/waiting for recovery umbrella are BON, BT, GFRD, ITV & NXR. Sell or hold at the moment on a potential offer; always a bit of a quandary for an investor that one: will the potential bidder Stonegate after looking at the books walk away? I honestly don’t think so Stonegate is a very smart animal totally specialised in this sector having made some smart buys over the years: most will have heard of Yates & Slug & Lettuce (oh God, that’s just brought back to me the memory of SFI that completely fell off the bar stool in 2002). So I think it’s closer to being a nearly done deal than most investors think yet maybe another 10% may be added to the offer or an alternative bid come in as personally, I think that Stonegate sees a bargain at 200p especially with their hand at the tiller. Whilst I admire investors who bought in the recent trough and have decided to sell; then well done on making an excellent return. However, I intend to hold on to my shares in RBG for yet a while. I should say what a dreadfully strange time it was for RBG to issue that potential offer RNS, 16:22: why not simply wait until the markets opened the next day? Still not to worry the good news added a touch of extra vigour to my tedious task of making mushroom risotto that evening; lovely food especially with a touch of white wine and calvados but all that stirring! The celebratory drink of the evening was peppermint tea; Monday to Friday are “dry days” for a few months. Finally, on the subject of RBG, I have to say that the excellent article by Paul Scott following the TU helped push the buy button. Incidentally, on roll-outs, there have been some first class articles by Paul on the more bullish side and Phil Oakley on the more “take care” side of roll outs: two first class commentators in my view. Tuesday 01/08/2017: Elementis: ELM: Market Cap: £1,370m: Interim Results: all fairly positive but maybe the excitement in ELM has slowed for a while after enjoying a 50% rise from July 16 to Mid February 17. The shares are taking a breather now having been fairly locked within a trading range for the past 5 or 6 months. Overall doing OK and will remain as part of the 3YL portfolio.   The outlook statement reads: Outlook-on track to grow operating profit across all three segments in 2017. My View: a decent solid business with an unexceptional yield that is very well covered by FCF: for now I won’t be adding any more. Tuesday 01/08/2017: Taylor Wimpey: TW.: Market Cap £6,347m. The interim results are to my eye good with headlines presented as:  Note: the decline in PBT of £130m due to an exceptional item involving leasehold review: a paragraph reads: Within the AGM trading update in April we published the conclusions of our leasehold review, and announced that we would make a provision, before tax, of £130 million in the first half accounts, which we continue to believe is an appropriate estimate. We expect the cash outflow to be spread over a number of years. The process of negotiation with the owners of the freeholds to these leasehold properties is on-going, and is proceeding in line with our expectations, and we continue to keep customers updated on the progress of these discussions.  My View: overall a decent set of results and the previously announced leasehold revision of £130m has now been included as an exceptions cost in the interims. There is also pleasingly a special dividend announced again for next year with more cash being returned to shareholders. I was very overweight in housebuilders and took some very pleasant profits to reduce overweight sector exposure. However, in the aftermath of Brexit, the seduction of the sector was just too great for me to resist and I became a little obese but not grossly obese as I had previously been before selling some house builders in January 2016. Incidentally, I am always relaxed about having a bias to a few sectors that I consider to be going through favourable times and don’t really see a weighting across the major sectors as an imperative. Wednesday 02/08/2017: Dignity: DTY: Market Cap: £1278m: Quite a decent set of results in my view although comments such as an x% increase in the number of deaths do give one a spooky feeling. I suppose the DTY RNSs would go into overdrive with a touch of plague hitting our shores! Anyway, back to the results:  Non-GAAP measures The Board believes that whilst statutory reporting measures provide a useful indication of the financial performance of the Group, additional insight is gained by excluding certain non-recurring or non-trading transactions. These measures are defined as follows: (a) Underlying profit is calculated as profit excluding profit (or loss) on sale of fixed assets and external transaction costs. (b) Underlying earnings per share is calculated as profit on ordinary activities after taxation, before profit (or loss) on sale of fixed assets, external transaction costs and exceptional items (all net of tax), divided by the weighted average number of Ordinary Shares in issue in the period. See note 2. (c) Cash generated from operations excludes external transaction costs. Following a very strong start to the year, with the number of deaths seven per cent higher than last year in the first quarter, the half year concluded with the number of deaths two per cent higher than the same period in 2016. The Group's results for the first half of 2017 were in line with the Board's expectations with underlying operating profits increasing seven per cent to £59.5 million (2016: £55.6 million). Outlook: The Group continues to expect the number of deaths in 2017 to be slightly lower than in 2016. Our financial expectations for the full year remain positive and unchanged. I suppose a balanced portfolio could be along the lines of Tristel to as the first line of defence to kill the bugs followed by GSK to treat you if the bugs get through and finally Dignity to “look after you” should the grim reaper get his evil way! My View: overall a decent set of numbers but I somehow feel the best years of profits growth are behind DTY and they eventually will have to address the rather stingy dividend in order to make the shares a touch more attractive. Having said that, the business will always have customers; it’s not the sort of service to simply die away. Wednesday 02/08/2017: AdEPT Telecom: ADT: Market Cap: £80m: £7.3m BGF funding and Atomwide acquisition. Interesting acquisition in my view; the RNS part relating to the acquisition of Atomwide goes on to say “The Board of AdEPT also announces that it has signed an agreement with effect from 1 August 2017 to acquire the entire issued share capital of Atomwide a well-established UK based specialist provider of IT services to the education sector ("the Acquisition")”. The note goes on to say that the acquisition is expected to be earnings enhancing from completion (one would hope so!), Atomwide hold the IPR for their education applications and that’s nearly 80% of Atomwide revenues and gross margin are from recurring products and services. My View: will, of course, have to keep an eye on debt with ADT as well as the rather volatile nature of the share price but overall it looks like decent progress for ADT. The share has performed reasonably well for me in the last 12 months haven appreciated by just over 30% but I don’t think I will add further just yet. Thursday 03/08/2017: No RNS of interest to my portfolio or immediate watch list Friday 04/08/2017: Keywords Studios: KWS: Acquisition(s) of La Marque Rose SARL, Asrec SAS and the subsidiary companies of holding company, Dune Media SAS. I have to say I was getting a touch worried about KWS as they had not announced an acquisition for a few weeks but that was put right today. My View: to be fair to KWS, the bolt on businesses do look interesting and if KWS can manage and softly integrate whilst keeping the flair of the added companies, then the future could indeed look very promising. I have to say there is never a dull moment on the journey with KWS: I will continue to hold. New section: Glad I’m Not There ( a sort of reverse take on the old Judith Chalmers holiday programme briefly mentioning a dog of the week that thankfully I don’t own), surely a candidate for dog of the week has to be Real Food Group with it’s screwed up RNS announcements and it’s smoke & mirrors accounting. The increase in Capex/D&A ratio would have rang alarm bells with me and at the very least necessitated some in depth digging to get a feel for it’s validity. I do run a smoke and mirrors (S&M) screen to try to pick up rapidly such points; they may well be perfectly valid but at least the S&M screen directs me to have a look. Another candidate for the dog of the week may have been Utilitywise, UTW, but I somehow think that the announcement this week covering changes in accounting practices may draw something of a close to some of the obvious suspicions surrounding UTW. Strangely the company did sneak into the outer reaches of my universe but got rapidly defragmented due to its dodgy accounting practices and the revolving door of changes in the boardroom: it always makes me worry when a CFO leaves in order to pursue other career opportunities. Still not one for me I am afraid. Next Week: all I can see scheduled at the moment are interims from LGEN, oh what a beautiful Brexit bargain that was. So, hopefully, an easy week on the keys and not necessitating an overindulgence with the peppermint tea. In between that, we have the start of the football season; the real stuff & not that Premier League nonsense. So, it’s off to my beloved Kenilworth Road on Saturday ”the theatre of dreams” but sadly not recently ones with many happy endings. Have a good weekend.

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed