|

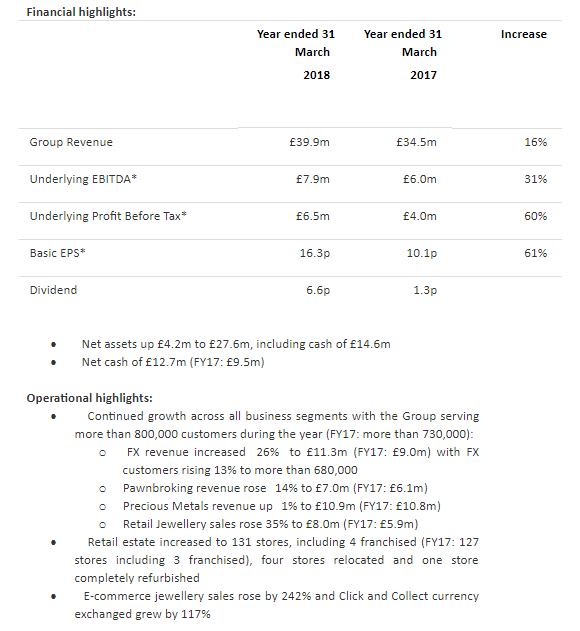

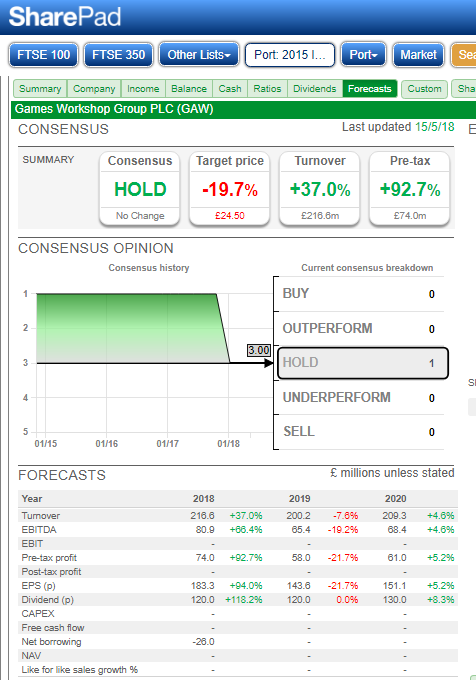

Voyager RNS Log WC 03/06/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Great news and on my birthday as well as I received a letter confirming my successful appeal against my council tax banding and a fairly substantial refund going back to 1999; happy days! Incidentally, my request for a re-evaluation was rejected at first but after more legwork, I was able to provide sufficient evidence for the process to begin. If anybody else is considering this approach then I suggest you give it a try & link guidance: https://www.moneysavingexpert.com/reclaim/council-tax-bands-change. For my birthday meal with family, I relaxed my low salt diet and had a very tasty if salty, Lamb Rogan Josh. Incidentally talking of salt, I remain convinced that if the general public reduced their salt intake on a daily basis to less than 6g then the profits of the pharmaceutical companies would decline as the blood pressure of the population reverted towards something more like 120/80. On a general note, often when I sell a share especially if I do so as I see something I don’t immediately like yet still feel the business if of decent quality, I will not be averse to buying back in either as a spread bet or as shares once I deem that the fall is complete and I see a bowl of recovery on the chart. Two very recent examples where I bought back in via spread bets are RWS & OTB and pleasingly after both had been heavily marked down they are both rapidly heading upwards. The reasons for my earlier sales of both RWS & OTB which of course were RNS catalysed, can be found in earlier RNS weekly logs on this site: as ever if I see a doubt I either get out or substantially reduce my holding. I suppose it makes me sound like a trader but that’s not how I work: once I see a risk, I take action to either diminish or remove that risk and should an attractive opportunity occur again with that company, then I will happily re-enter. In the case of RWS & OTB, both of which I consider as quality companies, they really to my mind became oversold and hence sufficiently attractive to me after their price falls. Anyway, onto this weeks log which I apologise in advance for being possibly a touch less in depth as I have been away from the office for so much of the time. Monday 04/06/2018: Xpediator: XPD: Mkt Cap £71m: Acquisition of Anglia Forwarding: Xpediator, (AIM: XPD) a leading provider of freight management services across the UK and Europe, is pleased to announce it has entered into an agreement to acquire the entire issued share capital of Anglia Forwarding Group Limited ("AFGL"), a UK-based international freight forwarder with road, sea and freight capabilities (the "Acquisition"). The initial cash consideration payable upon completion is £1.5 million, plus a further cash payment reflecting AFGL's surplus working capital position at completion estimated to be approximately £700,000. Deferred cash consideration of up to £2.0 million may also be payable contingent on profits generated by AFGL over the two years ending 31 May 2020. My View: to my eye, the acquisition of Anglia Forwarding for £1.5m plus deferred cash of up to £2m; looks a very sound purchase. Looking at the numbers provided it looks a reasonable enough acquisition for XPD and I suspect that more acquisitions will follow. The EBIT margin of XPD is by nature of the sector, not massive but from what I can put together it suggests that the margin will slightly increase as these bolt-on acquisitions come into play plus of course other synergies offering cost saving and contract opportunities. XPD is at the moment is only a small starter position within the folio. Monday 04/06/2018: Amino: AMO: Mkt Cap £149m: Kabelnoord rollout and on Wednesday 06/06/2008 a Trading Update Kabelnoord, the leading Dutch cable operator, is to deploy Amino's MOVE end-to-end multiscreen video platform. This will allow Kabelnoord to offer next generation TV services as part of a major rollout of its fibre-to-the-home (FTTH) network. Then the TU: Amino entered the current financial year with a strong order backlog and during H1 2018 booked over 40% more orders than in the first half of 2017. This, along with good pipeline coverage, means that the Board's expectations for the full year remain unchanged. As communicated previously and following the change in phasing of orders by one of our major customers, we expect to return to our normal seasonality in the current financial year, with revenues weighted to the second half of the year. Consequently, we expect revenue for H1 2018 to be lower year-on-year at approximately $41 million (H1 2017: $49.8 million). (Sterling equivalent H1 2018: approximately GBP30 million revenues; H1 2017: GBP39.9 million revenues). We continue to see momentum in areas of strategic priority, such as software and recurring revenues. Earlier this week we announced that Kabelnoord, the leading Dutch cable operator, is to deploy Amino's MOVE end-to-end multiscreen video platform in the second half of the year. Revenues from software and services sold on a standalone basis continue to increase and are expected to be 12% of total revenue in the period (H1 2017: 8%). Exit annual run rate recurring revenues increased in the period to circa $5 million (H1 2017: $3.7 million). (Sterling equivalent H1 2018: GBP3.8 million revenues; H1 2017: GBP2.9 million revenues). Net cash at 31 May 2018 was $15.1 million (31 May 2017: $16.8 million). (Sterling equivalent 31 May 2018: GBP11.3 million net cash; 31 May 2017 GBP13.1 million net cash). My View: well the roll-out contract win sounds encouraging but no real financial numbers can be offered and I can’t offer even a rough scratch calculation on the revenue significance; so, we will just take it as encouraging. However, what did not strike me as quite so encouraging is the required stretch from H1 revenues ( as predicted in this RNS) to H2 full year expectation. I am not saying it's not achievable or indeed doubtful but to my view simply looks a touch more challenging than I would feel comfortable with. I note that AMO tell us that expectations for the full year remain unchanged but a quick dig into the current H1 prediction & the full year expectation does worry me a tad; they may well make the numbers but after looking at recent historic H1/H2 ratios for AMO, it just looked a bit risky to me. My Action: I did try to sell 50% of my holding at the market open but as is so often the case with small-cap/AIM stocks, a decent trade selling price can be difficult to achieve on screen. However, I did take profits on 50% of my holding the following morning. My reasoning for this 50% sale was simply to control risk and AMO, which still looks a decent attractive business, is now demoted from my top 10 holding. Monday 04/06/2018: IQE: Mkt Cap £856m: Not an RNS as such but an AGM statement that can be found on the companies We are pleased to confirm strong wireless activity and that we are actively engaged in VCSEL qualification programmes with over 10 additional key VCSEL chip manufacturers, which are progressing in line with the board’s expectations. We confirm our guidance for a 40:60 revenue split H1:H2 2018, with a shift back from wireless to photonics as we enter H2 2018. The commissioning of the new Newport Foundry is progressing to plan, with the first five reactors now all on site and in various stages of acceptance testing, commissioning and qualification. The second five reactors are expected to be delivered on site commencing Q3 2018, with acceptance testing, commissioning and qualification during the rermainder of 2018. “Our new technologies portfolio, including GaN on Silicon, NanoImprint Lithography (NIL), Crystalline Rare Earth Oxide (cREO), and Quasi Photonic Crystals (QPC), is rapidly gaining strong traction and engagement with key customers around the globe for a wide variety of high volume applications.” The Group will announce its Interim Results for the six months ended 30 June 2018 on Tuesday, 4th September 2018. An analyst briefing will be held later that day at a time and venue to be announced. My View: firstly I wish companies would spell check in a better way as even a word blind dyslexic such as me can spot errors; that’s disappointing. I took profits of a recovery stock The Restaurant Group and bought back into IQE today having previously made some very decent profit on my sale of IQE earlier in the year. In fact, my association with IQE goes way back some 8 years but sadly I took time away from IQE for some of that time and missed the rise form the 20’s to the 70’s but at least I re-entered to catch a nice special situation that went on a charge through just about all of 2017 (half of that charge was better than no ride at all). Since that time and my sale in the 140’s, the share price has drifted down significantly after periods of ramping and negative ramping/excessive shorting in the investment community. I thought that the AGM statement was positive enough for me to buy back into what I tend to classify as a special situation stock. It’s not without risk but does contain a substantial amount of promise. From what I can see, the AGM statement has also been received well by the brokers. Tuesday 05/06/2018: No RNS of impact to Voyager Wednesday 06/06/2018: Amino: AMO: Mkt Cap £149m: Trading Update: SEE AMO Notes above & sale of 50% of holding. Thursday 07/06/2018: Ramsdens: RFX: Mkt Cap £57zm: Final Results:  My View: maybe I should start by saying that morally I don’t usually invest in the likes of pawnbrokers, loan-shark companies, tobacco companies, cheap booze companies etc as the exploitation of the less affluent is not something that I choose to profit from. However, I just about convinced myself that RFX was only partly a pawnbroker, conscience somewhat cleared, and therefore in recent weeks have been steadily building up a position in RFX with an average buy price of 188p. I like the financial numbers and ratios and indeed I see that Stockopdeia has given it a stock rank of 91. I should say apologies for the limited notes here as my office time is very limited this week; simply suffice to say that I see RFX as a decent quality business progressing well and it’s first set of full results since joining AIM look impressive to me. Indeed, I was very taken by these results which fractionally beat expectations (I think they are only covered by one broker but anyway, so the expectation does suffer from bias) and took a further slice of RFX and it now replaces AMO in the top 10 list. The strength in the numbers comes from their FX service, up 26% to £11.3m & Jewellery which was up 35% to £8m. The EBIT margin looks encouraging according to my rough fag-packet increasing from 13.2% in 2017 to around 15.8% in 2018. Friday 08/06/2018: Games Workshop: GAW: Mkt Cap £986m: RNS Trading Update: TRADING UPDATE ON CLOSE OF FINANCIAL YEAR ENDED 3 JUNE 2018 Games Workshop is pleased to announce that the sales and profit growth, which was discussed in the trading update released on 4 May 2018, has continued in the period to the end of the financial year. Sales growth has been across all sales channels. We expect the Group's sales for the 53 weeks to 3 June 2018 to be approximately £219 million and the Group's profit before tax to be at not less than £74 million. Royalties receivable from licensing are c. £10 million. In recognition of our staff's contribution to these results, we paid during the year a bonus amounting in total to £5 million. This was paid equally to each member of staff. My View: it looks a very decent trading update to me and I particularly like the bonus arrangement for all staff sharing in a £5m pot; that to my mind is excellent and really get employees feeling that they are more than just a servant to the company. The end of year figures look bang on the brokers and that leads me to a couple of thoughts: Firstly with a company doing as well as GAW and approaching a market cap of £1b I would have thought that more brokers would commence coverage of GAW. Secondly given the very positive newsflow from GAW including the introduction of new offerings and the royalties stream of income, I would think the forecasts would be moved upwards a touch for 2019 as at present the broker suggests a drop of 5% in revenue and a drop of 22% in pre-tax profit.  Interesting times; I am happy to continue to hold and may add further on future share price weakness as profit taking sets in.

Whats On the horizon next week: Results: Finals from IG Design Group: IGR on 11/6/18 & Finals from Norcros on 14/06/18. Oh yes, also maybe AIR on 11/06/2018 if they complete the accounts worked then return from suspension. Possible Trading Updates? BOO & SOM. This weekend I intend to enjoy a nice family BBQ, fillet steaks marinated in kampot pepper/Lime/olive oil & chicken marinated in ginger/garlic/lime/soy sauce all cooked over charcoal and maybe washed down with a little red! Whatever your plans, enjoy the summer while it lasts! Happy investing; catch you all next week

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed