|

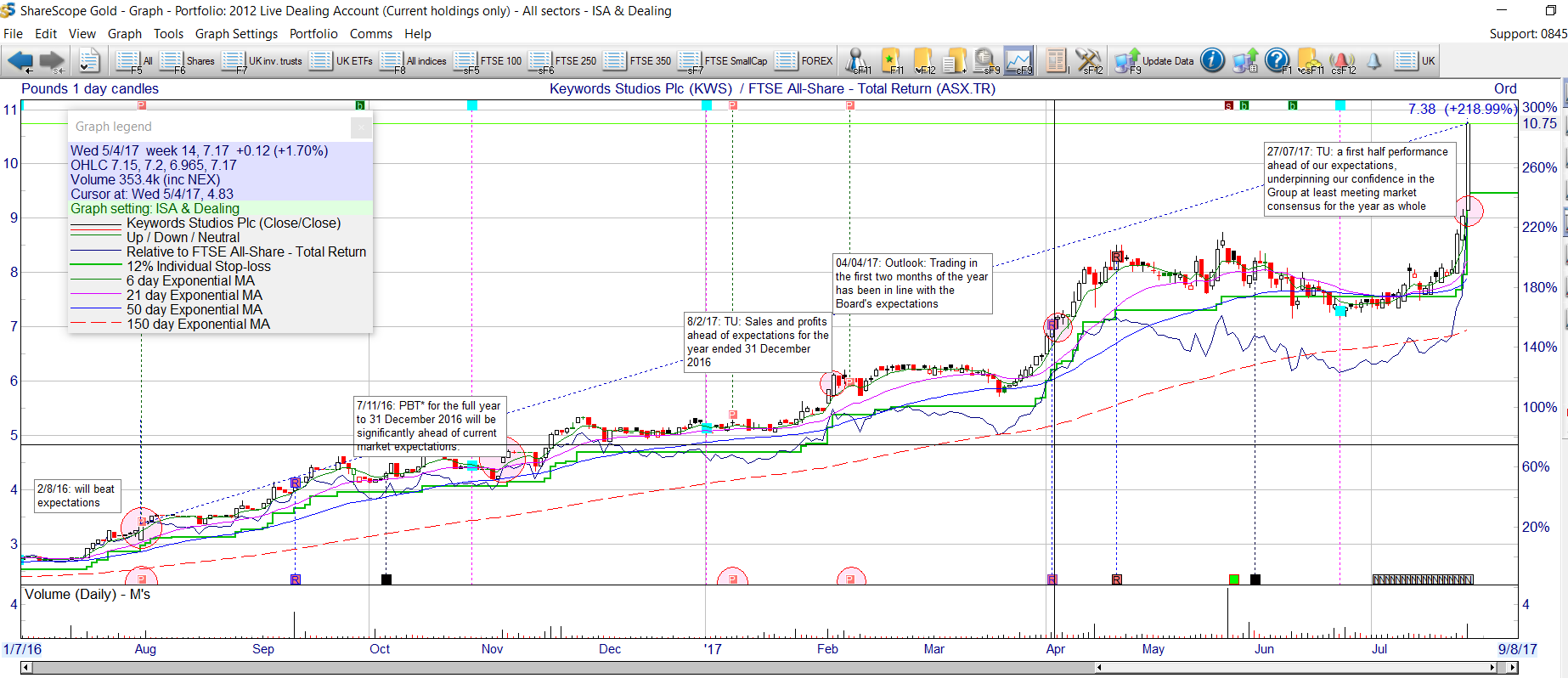

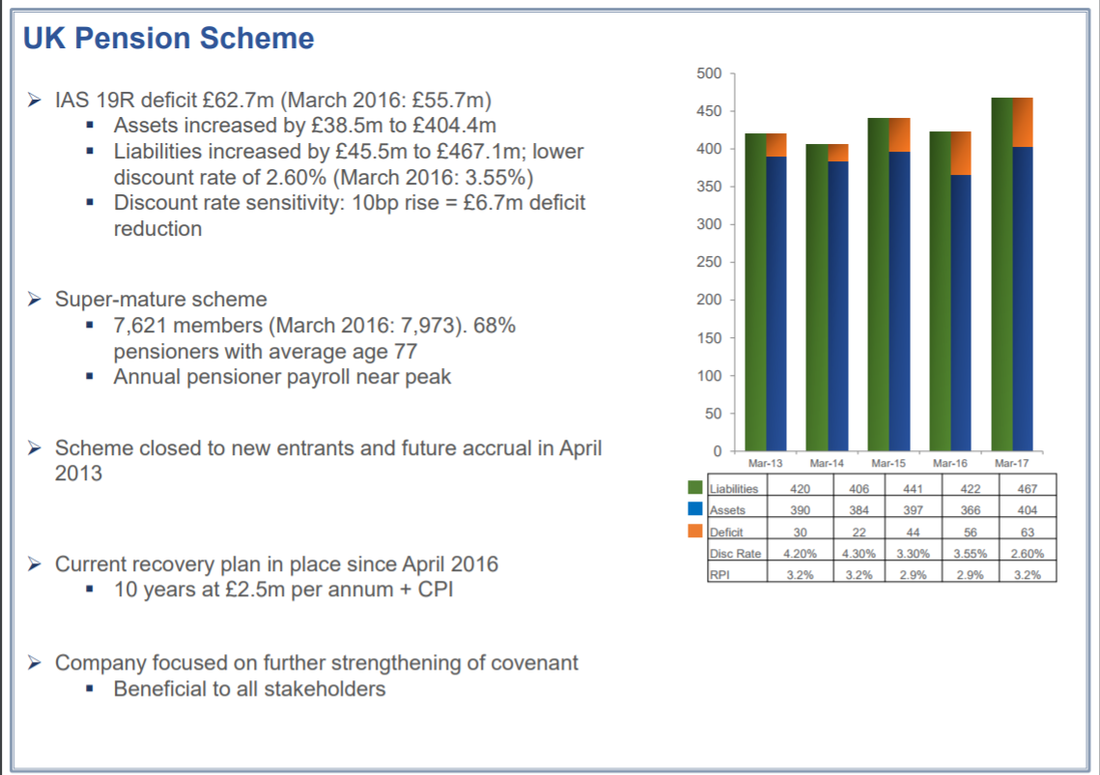

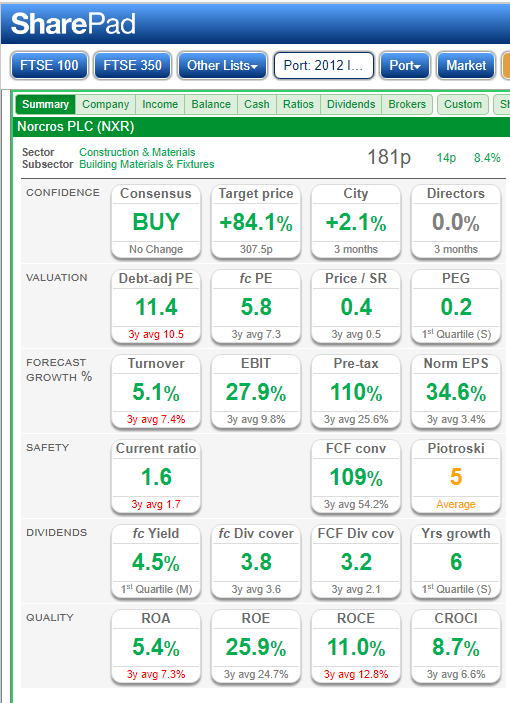

Week No 3 of The Voyager RNS Log Note: straight lifts from each RNS are in italics and my scribbling in normal text. Monday 24/07/2017: as expected a quiet RNS day for the portfolio but I did follow up on last week’s consideration of BOY and purchased another top up. Tuesday 25/07/2017: no RNS’s from stocks within my portfolio or universe of interest. Wednesday 26/07/2017 ITV: Interim Results: Firstly quite a boring read and possibly penned by Coronation Street’s Ken Barlow but those who have become accustomed to my investment philosophy will know by now that I rather like boring companies. Anyway, a reasonable set of results and in line with management expectations. It was pleasing and reassuring that there were no nasty surprises and that alone should reassure the markets and brokers who got into the habit of downgrading ITV forecasts. The numbers themselves do not hit you in the eye and say this is a buy but they are from my viewing encouraging as things as now new worries emerge and to my view this gives a superb base for the new CEO Carolyn McCall to build on; an excellent time for a dynamic leader to take up the position of CEO in a few months time. The outlook statement reassures that the business is on track to meet the current year's forecasts: No change in full year guidance • Confident that ITV Studios will deliver good organic revenue growth with adjusted EBITA broadly in line with last year, impacted by ongoing investment in drama and the timing of programme deliveries • ITV Family NAR forecast to be down around 4% in Q3 and we expect to again outperform the TV ad market in 2017 • Online, Pay & Interactive will deliver good growth driven by a strong performance in Online and Pay • Will deliver £25m overhead savings and a £25m reduction in the programme budget as previously announced My View: Given the future landing of Dame Carolyn McCall as CEO, I think that is a very impressive appointment, I feel very optimistic about ITV’s future and continue to hold what I consider to be a good value business paying a decent dividend. Thursday 27/07/2017: Keyword Studios: KWS: Half Year Trading Update: “The Group has performed strongly during the first half, with preliminary unaudited revenues for the period up by 50% to €63.7m (H1 2016: €42.4m) and a 60% increase in adjusted PBT* to €9.6m (H1 2016: €6.0m)”. “All the Group's service lines showed good organic growth, as measured on a like-for-like basis, with the exception of Audio which had a particularly tough comparative due to the exceptional performance of Synthesis in H1 2016, as previously reported. The underlying like-for-like** revenue growth was 17%, or 28% when excluding Synthesis in both periods”. Andrew Day, Chief Executive of Keywords, commented: "We are delighted with our progress so far this year. This has enabled us to deliver a first half performance ahead of our expectations, underpinning our confidence in the Group at least meeting market consensus for the year as whole”. The TU reads very well for my favourite Meccano company but I tell you what, it does worry me just a touch how the management will continue to successfully juggle and integrate the bolt on businesses that seem to be constantly acquired. However, for now, as in the game of musical chairs, whilst the music plays and momentum is there, it does look very good. I bought my first of a few fairly significant batches back in the summer of 2016: I must admit that at the time I felt, as with DTG, that I had missed the boat (or aeroplane in Dart's case) as KWS had appreciated by over 50%. Since that first purchase, I have added further batches with the last one being in early January this year at about 530p. This reinforces my belief that while market conditions are favourable and the RNS flow is positive then maybe it's not too late to take a position and carefully ride the momentum This has certainly been my experience in bull markets but as ever we all need to listen to that music and make sure there is a chair to sit on when the time comes.  My View: One I will continue to hold but keep an eye on as simply by virtue of its growth, in a fairly short space of time it has now become a significant holding in the portfolio. Thursday 27/07/2017: Norcros: NXR Trading Update The TU reads: ”The Group's overall trading for the first quarter was in line with the Board's expectations”. “Group revenue for the 13 week period was 8.2% higher on a constant currency basis compared to the same period last year and 16.8% higher in Sterling terms reflecting a stronger South African Rand”. “UK revenue was 10.9% higher than last year reflecting both share gains and higher prices with growth across all channels, particularly within the trade and export sectors. We continued to experience growth in our South African business with revenue 3.5% higher on a constant currency basis and higher by 29.7% in Sterling terms”. I have held this company for a number of years now and to be truthful it's quite a reasonably sized holding that at the same time as delivering a reasonable return, has frustrated me no end at times. In the early days, the frustration was often down to the exceptionally dour wording by the accountants in the TU/Results. At the time I had the distinct impression that they were the sort of people who could look out of the window on a glorious sunny day and say "it's going to rain at some time"; don’t you just love accountants! However, they have improved their PR act, appear to be managing the pension deficit well and are growing the business. I should balance my “reserved accountant” comment by adding at least we don’t have an Arthur Daley type at the helm! A Quick look at the pension issue as shown in slide 10 of the year ending 31/03/2017 results presentation:  Now whilst I am not a pensions expert, I really strongly question if there is anything to worry about with the REAL “closed to new entrants as from April 2013” pension scheme. My reasoning being that firstly the scheme in pension talk, is super mature with 68% of pensioners over the age of 77(78+ as of today) and 7621 members with the scheme, as seen on the slide, at it’s peak: in 5 years time it’s a simple fact that a significant number of members will sadly pass away. Secondly, the deficit is reliant on a discount rate and that if that rate rises by a simple 10bp it wipes over 10% of the pension deficit away. An even greater but still small rise in the discount rate over that 10bp would have a hugely significant effect in greatly reducing the pension deficit. So, for these two reasons, I think that both Mr Market and the market commentators are seeing a problem as far more of a millstone than it actually is! My View: A good encouraging positive TU from NXR yet they remain a touch unloved by Mr market and I am convinced that two of the main reasons for that are firstly the perception of its pension deficit and secondly the apparent incredibly boring nature of the business. As for me, yes you have guessed it, boring is good and I like the numbers: NXR sits on a PE of 5.8 that is reasonably close to their yield of just under 5% which is handsomely covered 3.2 times by FCF and a very decent forecast eps growth giving a PEG of 0.2: I should also say that Stockopedia have it on a stock rank of 96. I have included below the useful financial summary, what I call the dashboard, from the excellent SharePad:  Thursday 27/07/2017: Bodycote: BOY: Interim Results.

At the time of writing last week’s RNS log, I did say that following that very positive "game changing" RNS last week that I would consider topping up by original holding bought in early 2016 and I duly topped up early Monday morning. The results were really quite sparkling & to my mind, real quality: extract of key numbers · Group revenue up 18.8% (up 8.3% at constant currency) · Organic constant currency revenue growth of 4.8% · Headline operating margin increased 90bps to 17.8% · Headline earnings per share up 29% to 23.6p · Free cash flow doubled to £42.1m (2016: £20.9m) · Net cash of £17.7m (2016: net debt £5.5m) · £36m growth investment projects approved in the period · Interim dividend of 5.3p, up 6.0% The outlook also looks very positive: “Bodycote achieved strong revenue growth in the first half, with good momentum in virtually all parts of the Group. Notably, the General Industrial business, which represents almost 40% of Group revenues, experienced a broad based recovery after over three years of decline. Automotive and Aerospace also moved ahead. The growth strategy of bolt-on acquisitions and greenfield investment contributed 5.5% of the 8.3% constant currency growth. Investment in new projects has been stepped up. The high margin Specialist Technologies continue to perform strongly and the margin expansion programme in European AGI is seeing further success. The positive momentum achieved in the first half is expected to continue. While our business, by its nature, has limited forward visibility, the Board now expects the full year result to be towards the upper end of market expectations”. My View: I just don’t feel that the market has priced in the significance of last weeks game changing announcement from BOY; a conservative company I have followed, invested in and respected for many years. Just to refresh, the RNS said “Bodycote has decades of experience creating complex, high integrity components from powdered metal. Bodycote Powdermet® technologies now incorporate new, patent-pending techniques that combine 3D printing with well-established net shape and near net shape techniques. This new technology dramatically reduces the manufacturing time and production cost of a part compared to producing the same part using 3D printing alone”. In fact, I don’t think it's a bad thing Mr Market being that slow as it gives us PIs a bit of an edge: as ever, all just in my opinion and most definitely not advice. I am very happy to continue to hold and should there be an attractive pull back shortly, will add to the current holding yet again. Incidentally, looking at the numbers and the very positive announcements from Bodycote, I expect some significant increases in broker forecasts* for this quality business to be announced. *Footnote: just seen a note this morning; brokers have indeed started to raise forecasts but at this stage I suspect they increase in forecasts is mainly centred around yesterday’s very good interims :

Thursday 27/07/2017: Just Eat: JE.: Interim Results and what a pleasant set of interims these are with headline numbers comparing to the same period as last year Financial Highlights (taken from RNS)

However, we continue to drive channel shift and are pleased that 75% of total orders are now placed on mobile devices. In the UK, we have seen increased traffic to our website and improved consumer reorder rates, demonstrating the strength of our brand loyalty. Our international businesses, now 43% of Group revenues, have enjoyed further good momentum. In particular, the acquisition of SkipTheDishes has generated revenues above expectations and consolidated our market-leadership in Canada”. The outlook goes on to tell us “Revenues for the First Half were ahead of management's expectations. Reflecting this more positive outlook for the Group, we are pleased to raise our revenue guidance for 2017 to between £500 - £515 million up from £480 - £495 million. In line with our strategy, we intend to reinvest this revenue outperformance into additional profitable growth opportunities, including further building on the momentum within the business and increased collaboration with branded UK restaurants. Therefore, EBITDA for the Full Year is still expected to be between £157 - £163 million." Therefore the company are telling us that EBITDA for this year will be either in line with or slightly below the current forecast EBITDA due to this extra reinvestment to grow the business: I am ok with this but it may spook some due to the current high rating of the shares. My View: I will continue to hold JE which is really building on what is a very dominant market position. The shares pull back a touch but in my view one to keep holding and possibly add to on the pull backs. Just a footnote that ordering through Just Eat can have its advantages compared to as simple call to your local takeaway. My son ordered a pizza which failed to arrive anywhere near on time, the shop’s fault: JE credited the cost of the order and arranged for a complimentary pizza to be delivered. The result one happy customer comfortable with unhealthy take away food. Thursday 27/07/2017: Bonmarche: BON: Trading Update: Note: I took a bit of a contrarian position in BON recently as although on first look it appeared to be a business in decline it was at least to my view, in a transformational stage in its move to move into online sales, the encouraging if adventurous appointment of the Helen Connolly as CEO on August 2016 plus the well covered almost unreal dividend of 8% plus tempted me after a touch of responsible research. Todays TU is very encouraging “Total sales for the 13 weeks ended 1 July 2017 increased by 7.6% against the corresponding period in FY17. Store LFL sales increased by 4.2% and online sales increased by 39.0%”. Out of italics now so it’s back to me: now it’s early days but that increase of 39% but at the same time remember that that large percentage increase is based on a reasonable modest online income last year of just under 10% of total sales but nevertheless very encouraging increase in online sales that could substantially boost earnings in the future. The outlook informs us ”Trading during the first quarter of the new financial year has been in line with the Board's expectations, which are therefore unchanged in relation to the full year's result. The financial position of the business remains sound”. My View: I am very comfortable with my position in BON, the dividend looks sound and the market should be reassured with today’s announcement: I will continue to hold and may be tempted to add a few more. Friday 28/07/2017: RNS news for my me to consider BT: BT.A: 1st Quarter update which shows them as trading in line: in my opinion the bad news is all in the share price and I am looking for recovery from here. I bought these at a low price looking for some degree of recovery over the next 12 months and the added comfort of a 5% yield. Note I see there is a trading update from G4M out today but I will leave that alone as I took some very good profits and no longer hold. As ever, all views scribbled here are simply me sharing my thoughts with fellow private investors and in no way should be taken as recommendations to either buy or sell a stock. Almost into August and in a few days time the real football starts; I simply totally ignore that grossly overrated “could not give a monkeys” premier league nonsense; no, it’s league football for me. So that means a return to writing about the Hatters exploits; indeed, life can be cruel at times! Have a good weekend & as ever happy investing.

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed