|

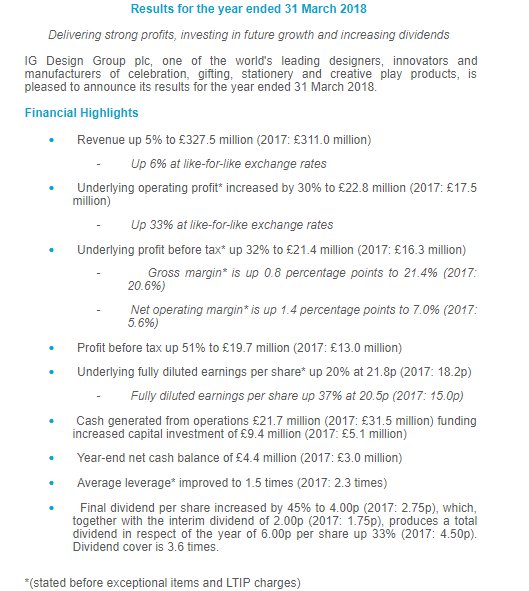

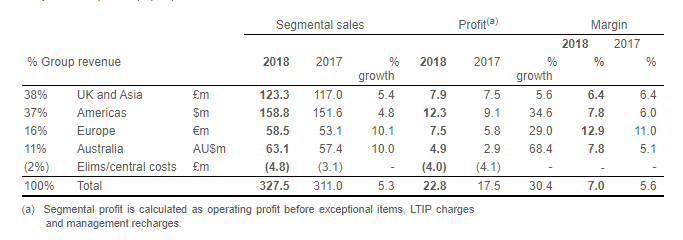

Voyager RNS Log WC 10/06/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Oh great excitement this week as we head towards the FIFA World Cup; such a fine organisation FIFA and according to the various guys who have run the organisation over recent years, operates without the slightest sniff of corruption. Call me a fool, but honesty and integrity lead me to admire such an organisation who for the 2022 venue choose Qatar, a country where the temperatures during the June and July of the tournament will be around 42C; simply ideal for football: in FIFA we trust! Yet sadly my own planning for the current world cup held in Russia the very cradle of democracy, hit the buffers on Tuesday evening when the Samsung TV issued a profits warning and suspended itself from trading. Never mind, in truth, the TV has had a fine run but never been exposed to the likes of the X-Factor or Love Island so I suppose that helped its longevity. Well, the new one, a rather nice big OLED job should be up and running for the Portugal/Spain Iberian battle on Friday evening so, we will be up and rolling with a modest supply of cold beer. Incidentally, I never would have thought a few years back that the Americans would be capable of brewing a decent beer as their “stolen” Budweiser and Miller are tasteless fizz; yet these days the smaller independent lads are brewing some incredibly good pale ale. Anyway, enough of this football and beer stuff and on with this week's log. Monday 11/06/2018: IG Design: IGR: Mkt Cap £294m: Full Year Results   Outlook Following the transformation of the Group over recent years, there is considerable scope for further growth across all aspects of the business. We remain focused on the profitable development of our business and confident that we have the team and agility to deliver further successes. We will continue to create value for all stakeholders through our strategy of developing diversified income streams across broad categories and markets, both organically and through well considered acquisitions. With a strong order book in place and a positive start to the new financial year, we are excited about the opportunities to deliver further growth in 2018/19. Note: video on results delay courtesy of Tamzin & PI World: Link www.piworld.co.uk/2018/06/11/ig-design-group-igr-full-year-results-2018/ My View: once again another very sound set of results from IGR that meet expectations and pleasingly contain a very positive outlook on the future growth of the business. I felt it worth including the table of Turnover, Profit and margin growth for 2018 v 2017 and it’s a credit to IGR in how they are making their geographic areas very efficient and delivering profit growth significantly ahead of revenue growth. If you get the chance, do have a look at the video on the link above where Paul Fineman, CEO of IGR, discusses the results and gives an insight into the forward strategy of the business. I see IGR as a very well managed business with the guys in charge being a safe pair of hands; ok, some might see the business as dull and unexciting and indeed it does not pay a massive dividend at around 1.4% but for me it simply ticks so many of the quality boxes I look for in my long-term holds. My purchase of IGR back in 2016 was not based on the Stock ranks system but nevertheless its pleasing to see that that worthy system gives IGR an SR of 88.  Monday 11/06/2018: Somero: SOM: Mkt Cap £224m: AGM Trading Update: Trading Update Somero is pleased with the broad contributions to the Company's growth at this early stage of the year and the positive market conditions we continue to see across our portfolio of territories. North America and Europe remain healthy markets with robust activity levels and we remain encouraged by the performance in China in the period as we continue to work on gaining traction in this significant market. We are similarly encouraged by solid activity levels in the Middle East, Latin America and our Rest of World territories and we see opportunities for growth in each of these markets. The Company continues to focus heavily on future growth initiatives and product development efforts, and has progressed in developing a solution for concrete leveling in the structural high-rise market segment. In summary, the Company feels comfortable with the positive trading environment across our footprint, and the growth opportunities visible in North America, Europe, China, Middle East, Latin America and our Rest of World territories. This constructive environment combined with solid margin performance and healthy operating cash flow generation means the Company's trading to date is ahead of the comparable prior year period and in-line with market expectations for the full year ending 31 December 2018. My View: An encouraging enough trading update from SOM which rather like IGR but of course in a totally different sector, is a well managed conservative business in my opinion.; so, yes, I am happy with that. Its also encouraging that SOM is very responsibly working on a three-year plan for the succession of the guys at the top of the business: I guess the identikit for the process would include qualities such as a) modest b) humble & c)realistic. I see the very credible Stock Ranks system also gives a boost of confidence with an SR of 93. Monday 11/06/2018: Keywords Studios: KWS: Mkt Cap £1160m: Acquisition of Blindlight: Acquisition of Blindlight Keywords goes to Hollywood Keywords Studios, the international technical services provider to the global video games industry, today announces that it has acquired Blindlight LLC ("Blindlight") for a total consideration of up to $10m, from the founder, Lev Chapelsky (the "Seller"). Founded in 2001 and based in Hollywood, California, Blindlight enjoys a leading position in the provision of Hollywood production services for the video games industry. The company works on behalf of game publishers and developers in procuring specialised talent and managing the entire production processes for the parts of games that benefit from Hollywood production resources. Blindlight's service disciplines include voiceover production, celebrity acquisition and rights management, game writing, music, sound design and motion capture. Blindlight works with top game producers around the world (including Bethesda, NCSoft, Sony Interactive Entertainment, and Ubisoft)making the creative expertise of Hollywood readily available for the video games industry. The addition of Blindlight to the Group will increase the value of the services provided by Keywords and contribute to making those services more accessible to a wider customer base. Blindlight achieved EBITDA of an average of $1m per annum over the three-year period to 31 December 2017. Under the terms of the acquisition Keywords is paying an initial $3.64m in cash and will issue 64,521 new ordinary shares in Keywords to the Seller on the first anniversary of the acquisition which will then be subject to orderly market provisions for a further 12 months. Deferred consideration of up to $4.8m will be payable to the Seller in cash depending on the performance of the business in the 12-month periods to the first and second anniversaries of the acquisition. Andrew Day, CEO of Keywords Studios commented: "Following our recent acquisition of music services companies, Cord Worldwide and Laced, we see excellent opportunities for Blindlight to bring these services to Los Angeles, as well as providing access to further opportunities for our downstream production services of translation and localised voice over." My View: the multiple paid by KWS for Blindlight appears reasonable and it will add a little to earnings on 2018 & 2019 plus, and I don’t know how significant this really is, gives them this Hollywood link. In truth, I ask myself what the hell am I doing here as I don’t either like or play video games. There again my conscience is rebalanced as I don’t wear mature ladies clothes but have some shares in Bonmarche (honestly, I don’t wear any ladies clothing but do confess to having bought men's shorts from BOO). So the question is are the shares expensive? Well, that’s a question for each investor to answer for themselves and a current PE of 42 may suggest initially that they are. However, a quick scan of the market for companies valued at over £1b suggests to me that they are not really overvalued as there are so few large companies with that historic & projected growth. Of course, my comment does include the proviso that the expected growth will continue and the track record and market position that KWS is carving suggest to me that it will continue to deliver. Monday 11/06/2018: Air Partner: AIR: Mkt Cap £52m: 2017 Finals at last: I will restrict the text here to just an overall impression of the results in bullet point form:

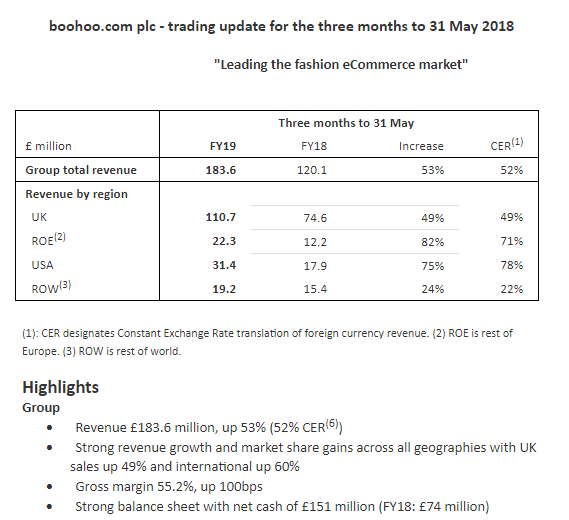

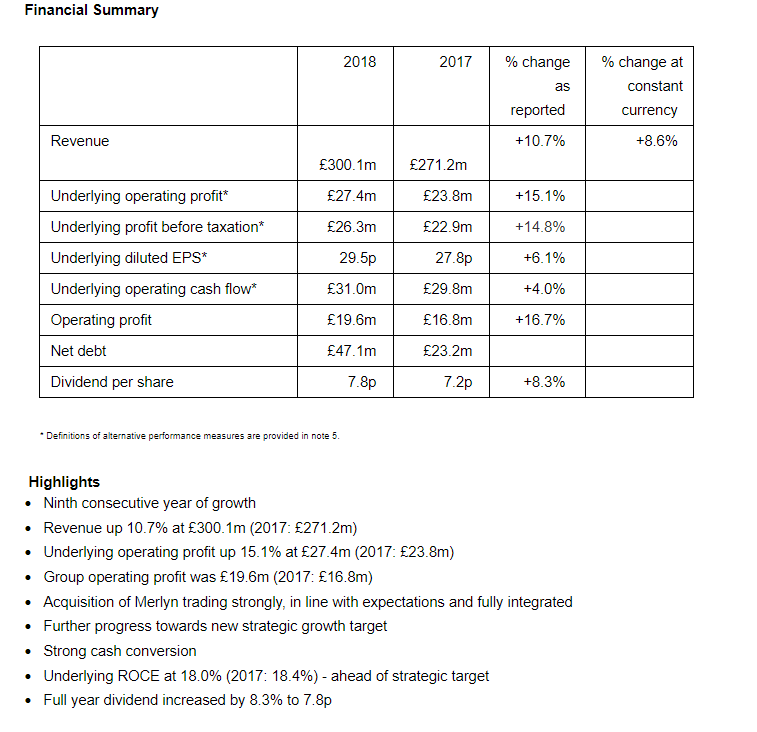

Tuesday 12/06/2018: Boohoo:BOO: Mkt Cap £2.53b: Trading Update:  Highlights Group Revenue £183.6 million, up 53% (52% CER(6)) Strong revenue growth and market share gains across all geographies with UK sales up 49% and international up 60% Gross margin 55.2%, up 100bps Strong balance sheet with net cash of £151 million (FY18: £74 million) boohoo Revenue £97.2 million, up 12% (10% CER) on last year's Q1 record growth Gross margin 52.0% (FY18: 53.9%). Retail gross margin 54.6%, down 170bps year on year, and improved progressively throughout the quarter, with an exit rate up year on year PrettyLittleThing Revenue £79.2 million up 158% (160% CER) Gross margin 58.7% up 490bps, driven by strong full-priced sales performance (retail gross margin 60.3% (FY18: 56.2%)) Nasty Gal Revenue £7.2 million up 149% (163% CER) Gross margin 58.9% (FY18: 69.9%), in line with FY18's exit rate and expectations My View: well it seems the excitement is in travelling to the trading update and then despite a decent update, the price eases back a touch: probably not unreasonable as the shares have had a very decent rally in recent weeks. The original core offering Boohoo is still growing nicely but is now rapidly being caught up in terms of turnover by Pretty Little Thing: Boohoo @ £97.2m and PLT @ £79.2m. Interestingly the combined revenue of Pretty Little Thing + Nasty Girl in this first quarter was almost half of the groups turnover and show an appreciably better gross margin (52% original BOO and 58.8% for PLT & NG). Overall a decent trading update with plenty of detail & guidance: I am happy to continue to hold. Wednesday 13/06/2018: Norcros: NXR: Mkt Cap £170m: Results for the year ended 31 March 2018 'Excellent progress towards our strategic objectives.'   My View: A decent enough set of results from NXR that meet expectations. The net debt has of course increased due to the acquisition during the year of Merlyn so, no shocks there. Whilst as I have written before, I don’t see the pension deficit as an issue that seems for some reason to be a touch misunderstood by the market, it’s pleasing to see it reduced from £62.7m in 2017 to £48m in 2018. As I have noted before the pension scheme is closed to new entrants and indeed 68%of those on pension average an age of 77: is there really a big risk there as time takes it’s toll on the population of claimants each year?

Norcros trades on a meagre PE valuation of 6.5, offers a yield of 4.2% that is very well covered (about 3x) by free cash flow and whilst it’s never going to be a stock to get the pulse racing, it has certainly earned its keep in the income portfolio. I am happy to continue to hold and rather think that at some time the market may well wake up to the attractions of NXR. Thursday 14/06/2018: AB Dynamics: ABDP: Mkt Cap £217m: Contract Win: First order for an advanced vehicle driving simulator (aVDS). The aVDS order, placed by a Chinese test house is valued at more than GBP2.0m with delivery expected in early 2019. Most of the value of the contract is expected to be recognised in the Company's next financial year commencing 1 September 2018. My View: Not material to this FY but as the note says, material to the next FY. Good to see a first sale and particularly good if other sales follow. Friday 15/06/2018: No RNS Relevant To The Voyager Folio: It’s been a busy week so a quiet day is very welcome/; an early finish by 09:30 beckons! Glad I Am Not There ( GINT): I should say these are not “clever dick” notes just simply an attempt to help investors learn from their mistakes and let's face it, we all make mistakes: the crucial point is what we learn from those mistakes. Well, predictably a mention has to go this week to Connect Group (CNCT) with a disastrous trading update that saw it’s share price collapse by 45% on the day. It was hardly a high expectation share within the market and happily one that I did not hold. Yet investors had plenty of time to look at the picture, heed the January 2018 profits warning followed by the continuously declining chart and reallocate their funds. I know it’s a case of each to their own but boringly I repeat that it's simply so crucial to protect capital by examining the downside in almost more detail than you may the upside. Another odd one and one I held profitably selling at the Stonegate hostile bid period is Revolution Bars (RBG) that issued an odd profits warning on Thursday 14/06/18 firstly blaming the cold snap in March and then blaming the unusually hot weather in May: “The adverse, wintery weather conditions in March combined with the unusually hot weather throughout May and early June, has curtailed typical late-night week-end trading”. The new CEO starts in a couple of weeks time and unfortunately for him, it looks like somebody has already chucked away the kitchen sink before he can get his hands on it; maybe he will find another kitchen sink to chuck thus clearing the decks with another warning? I feel there is the chance of a further profits warning here as the new CEO clears any semblance of bad news and also I can visualise the words “sales during a warm summer were impacted by the World Cup”; note this is the first world cup since RBG have been listed. Will another suitor be resisted by the new CEO I wonder? Whats On the horizon next week: I can’t see much apart from Bonmarche finals 19/06/18 also D4t4 but that’s pencilled in for the following week. Have a good weekend, catch you all next week. Happy investing;

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed