|

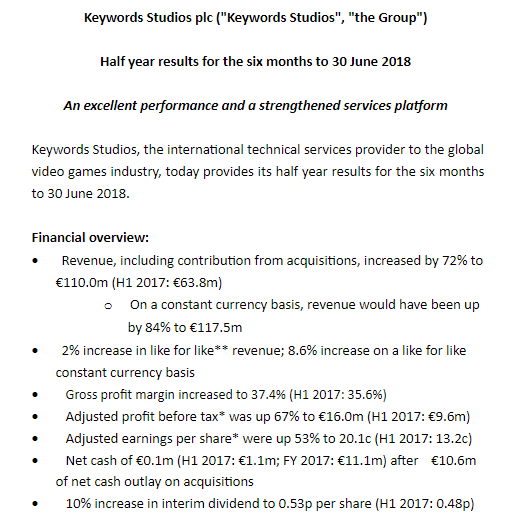

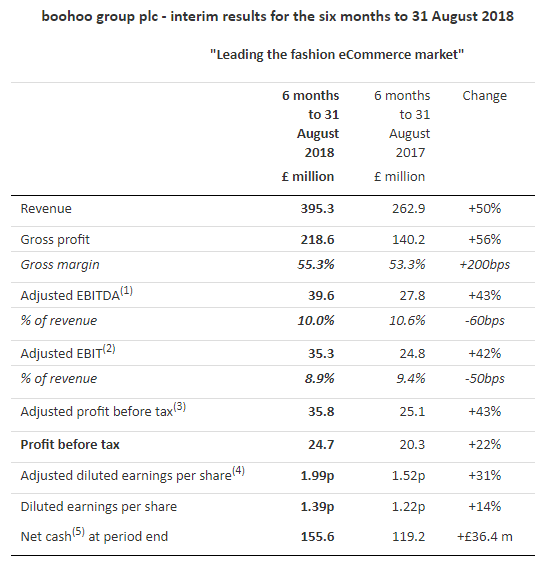

Voyager RNS Log Weeks Commencing 16/09/2018 & 23/09/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key to the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. After the game at Blackpool last Saturday, I had a few days away walking in The Lake District; I never need much of an excuse to visit some of the lovely locations in the UK and try wherever possible to blend it in with an away game. Sorry, I am in relaxed mode and drifting along but a point that I was mulling over when walking was how long does one really want to stay active in the market? After you have reached a point of sustainable comfort why do investors continue to strive for more and more? Why do Buffett and the like keep investing when the financial need has long been satisfied? What keeps such investors going? Why do folk such as Bezos of Amazon keep accumulating massive fortunes yet have such unhappy staff? Lots of questions yet no real answers that I can come up with but nevertheless interesting. Oh well, time for another lazy chunk of loot to be looked after by Terry Smith within his new Investment Trust, Smithson. I already have a sizeable holding, which I have held for a good number of years, in Fundsmith and indeed I use it’s excellent performance as one of my benchmarks. This IT will concentrate on “small to mid-cap companies” that Terry defines as between £500m & £15b but typically around the £7.5b market cap” which still to my reckoning are pretty substantial businesses but not the giants ROCE players of Fundsmith. Terry’s approach is difficult to fault giving an outstanding performance for lazy money since inception. For that reason, I rather expect the IT may trade at a premium to NAV; I do so much prefer Its over Unit Trusts/OEICs. General view on the markets: Still in my view, a degree of uncertainty lingering over the market and I rather doubt that will disperse until the UK’s future in its ongoing relationship with the EU is resolved. The FTSE All-Share index is down about 2% since the turn of the year and has experienced a fair amount of volatility and at one time was down by around 10%. So, most definitely a stock pickers market but as in my case with plenty of powder kept dry. Just a thought on software: whatever type of financial software you use, it’s so important in my opinion to become really familiar with all the facilities it offers. My favourite by some distance is SharePad but like anything, you really need to invest time learning how to get the very best out of the system; works so well for me right from the early morning RNS filtration to historic and current financial ratios. In a couple of previous Voyager logs, I have mentioned before the investment book I am bringing together that will cover 25+ years of my investing journey, approach, protection of capital, market timing and many other points learnt from both making mistakes and learning from the best investors. I am currently tinkering with a title, rather irrelevant I know, maybe the hitchhiking investor, maybe the hitchhikers guide to the investment universe; who knows! I hope to update in a couple of weeks time progress and then start to introduce the book by modular chapter/subject on the StockWhittler site. It’s not designed to be an “oh what a clever dick I am book” but rather a book that will aid some in their own investment journey. Onto the RNS log which does really remain a little sparse as there is just not much in the way of announcements recently. I am pleased to say that I dodged the bullet with respect to Bonmarch BON which issued a profits warning on Thursday 27/09/2018. I sold BON for a 25% profit at the end of July as a started to seriously reduce risk & exposure in the Voyager. I feel there are times to be fully invested and times to be cautious and at the present time, I place a lot of faith in the protection of profits. Tuesday 18/09/2018: Keyword Studios: KWS: Mkt Cap £2.2b: RNS Interim Results & a 2nd RNS regarding the acquisition of the Sound Lab and also The Trailer Farm: The key numbers  Outlook: Trading in the second half has been good and we expect to meet market expectations for the full year before the positive impact of any additional acquisitions. My View: every time I write about KWS it seems that the market capitalisation has gone up appreciably since the last time I hit the keys. When I first wrote about KWS it’s market cap was a touch over £100m we now have it bloated to over £1.2b is it grows at a speedy rate both via its highly acquisitive nature and organically. Is it pricy? Well, you could argue that it is but then how many companies are there on the LSE with such a proven track record at this high level of market capitalisation with such a great growth story. As for the acquisitions, in the early days of holding KWS I visualised the risk of the boardroom with all of those spinning plates on sticks representing each of the many acquisitions; these days, I take comfort from the excellent track record that KWS have of integrating these many bolt-on businesses. Unlike many companies, the CEO of KWS Andrew Day does a very good job of communicating with investors and the excellent PI video gang have again given Andrew a platform to discuss the results with investors. I am happy to continue my free ride and will keep holding. A link to the excellent PI World video where CEO Andrew Day talks us through the interims and discuss progress may be found on the following link: www.piworld.co.uk/2018/09/18/keywords-studios-kws-h1-results-september-2018/ Wednesday 19/09/2018: Games Workshop: GAW: Mkt Cap £1.25b: Trading Update: Games Workshop Group PLC announces today that trading is in line with the Board's expectations. Cash generation also remains strong. My View: although I normally dislike the approach of releasing an RNS on trading other than at 7 am, this looks absolutely fine. Its very simple, very concise yet the initial market reaction was subdued. I just reckon that many punters expect to see “Ahead….” Time after time. However, no matter, the shares duly pushed ahead over the next few days and even topped the £40 mark. I am happy to hold and just possibly for a rather long time. Then on Thursday after markets closed we had another RNS informing the markets that the ex-chairman Tom Kirby was selling via a placing in the order of £20m of shares. The shares were within an hour of that announcement at £36-50. That sale will probably have a little knock on the share price and maybe offer an opportunity for a little top up. Monday 24/09/2018: Spectra Systems: SPSY: Market Cap £49m: RNS Interim Results:  Commenting on the results, Nabil Lawandy, Chief Executive Officer, said: "The Company's revenues for the first half of 2018 are 11 % higher than 2017 and were driven by delivery of a large G7 customer order and royalty and license revenue from our agreement with a major banknote supplier. As a result of our operating gearing adjusted EBITDA for the first half of the year is markedly higher, 30%, than last year resulting in strong midyear profitability. The continued in line performance of the Secure Transactions Group as well as Brand Authentication puts the company in a strong position to meet market expectations for the full year. The delivery of two quality control devices to a tobacco manufacturer has increased our chances of introducing our TruBrand smartphone authentication technology in China. This is in addition to the recent allowance by the United States Patent Office of our patents on this technology. The Board therefore believes that the Company, by achieving key business milestones, will continue to perform well for the remainder of 2018 with excellent prospects for ongoing earnings growth thereafter." My View: well I have held SPSY for over 12 months buying at just over 80p and making further top ups a little later. Note: I usually limit my exposure to the more illiquid stocks and tend to never hold more than one sub £50m Market Cap in the Voyager. If something goes wrong it can be so difficult to sell small-cap stocks and even ones of around the £200m Mkt Cap for that matter. Anyway, the results and outlook look absolutely fine and indeed rather encouraging in my view yet Mr Market was a touch relaxed on the news. Finally, I see that the market has decided by Thursday 27/9 that “hey these are rather good” and the shares put on a spurt to 118p. Note although I don’t select stocks via the Stock Rank (SR) system, I see that SPSY scores a SR of 82 which is reasonably comforting. It also enjoys a nice royalty stream of earnings and pays a 4% yield; fine for me I will continue to hold. Wednesday 26/09/2018: BooHoo: BOO: Mkt Cap £2.5b: RNS Interim Results  Guidance

Group revenue growth for the year to 28 February 2019 is expected to be 38% to 43%, up from our previous guidance of 35% to 40%, with adjusted EBITDA margin between 9% and 10%. We reiterate our medium term guidance to deliver sales growth of at least 25% per annum and EBITDA margin of 10%. My View: I have traded BOO a few times since the days of 25p post its early profits warning shortly after IPO. Without doubt the growth rate in revenues of the group is impressive as is the management team who certainly seem to know their business area inside out. Note: an RNS dated 17/09/2018 covered the appointment of John Lyttle currently CEO at Primark who will become as from 15/03/2019 the new CEO of BOO. The headlines accompanying the interims choose to focus in on gross margin which is indeed impressive but I prefer to look for the EBIT margin which is just down a tad by 50bps but the cash position is looking very healthy. Overall nothing to worry about and indeed a good set of results: the market certainly reacted positively to the results: note in mid-September BOO was trading at 170p, as I write this log the price has risen to 220p. I will continue to hold. For investors who wish to hear a discussion of the results then log onto: protect-eu.mimecast.com/s/yVdaCvgOQhEDREOuQnSTn?domain=webcasting.buchanan.uk.com One new purchase added to the portfolio: Adept Telecom (ADT) Mkt Cap: £90m. ADT, which has been on my radar for a fairly long time having what I believe is a good business model with recurring contract revenues, increasing EBIT margin, increasing and good CROCI, modest dividend of 2.5% covered by more than 3x FCF & the good Prof Piotroski sees it as pretty sound with a Piotroski value of 7 and also loved by the SRs well into the 90’s. An RNS of 27/09/2018 gave a rather upbeat trading statement and announced that the company was changing its name: “Included in the AGM resolutions there is a proposal to change the name of the Company to AdEPT Technology Group plc. With more than 75% of revenues being generated from managed services and IT, the board believes that this new name better reflects the products and services being provided by the Company. Should the resolution be passed, the Company is expecting the change of name to take effect from Monday, 1 October 2018”. Note: generally I am not impressed when a company changes its name e.g. Matchtech to Gattaca, Post Office to Consignia but in this case, I fully understand and support the rationale for the change in company name. Well, that’s it for now. The next Voyager log will depend upon RNS news flow which should pick up a touch as we move into October. In the next couple of weeks I expect to see trading updates from XPP, TEF, NXR and finals from BVXP. As ever Happy Investing, have a good weekend and catch you again soon.

1 Comment

Peter Howat

9/30/2018 08:15:31 am

"Carving a cut of the profits" Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed