|

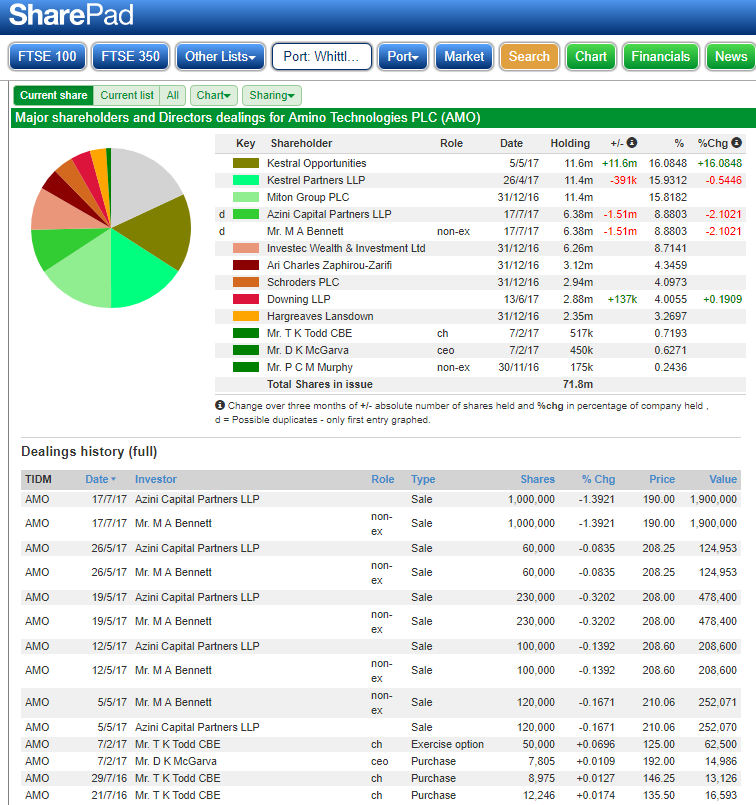

This is a new section fairly much in development within which I intend to offer some views on RNS ‘s covering shares I hold and maybe the odd comment on ones that I don’t currently hold. Being a new section it’s all a bit fluid but let’s see how it goes. Well, this is the second week of my RNS log involving owned shares within my universe. The first one appears to have been well received and to be honest it’s good for me to get a few up to date thoughts into print for each of my holdings as the RNS machine clatters it’s way through the week. It also helps me to seriously ask the question “if I did not currently hold this share, then would I buy it now?” Anyway, a few announcements in terms of RNS from my universe stocks the week just past. I have briefly added a few thoughts in the text below: as ever, not advice but just my take on the RNS. Tuesday 18/07/2017: Somero: SOM Trading Update. I felt that the trading update was solid enough with reassuring noises about business in both North America & an improvement in China:- “Group's continued expectation that trading for the full year will be in line with market expectations, as highlighted in the update provided on 5 June 2017”. “On a regional basis, June 2017 trading activity in North America was at the highest levels of the year as weather conditions improved and projects commenced. H1 2017 trading in North America will show a slight reduction in trading from prior year levels given that H1 2016 trading was particularly positive. Looking ahead the Company remains encouraged by the healthy US commercial construction market, extensive project backlogs being experienced by its customers and the high level of activity that is carrying over into H2 2017. H1 2017 trading in Europe has been exceptionally strong, significantly increasing over the prior year, driven by broad-based geographic contributions. Latin America and the Rest of World territories were also significant contributors to growth in H1 2017 with trading significantly increased when compared to the prior year. Trading in the Middle East ended H1 2017 slightly down from the prior year as a result of a number of opportunities in this territory having been carried over into the H2 2017. In China, June trading was also at the highest level of the year and despite H1 2017 trading falling below the prior year, the Company expects improvement in the second half”. My Action: well I still hold some SOM having originally bought in at just over 100p back in 2014. They had become a fairly significant percentage in my portfolio and I greatly reduced my exposure in late May & early June 2017 at an average price of slightly over 300p. The exposure I had to SOM at the time as well as getting to be overly dominant within the basket started to look about rightly priced for a cyclical business whose machinery is not patent protected. They have a reputation for excellence in 24hr 7/7 customer service/client help and I became slightly nervous that this differentiation could last for another couple of years; will the Chinese go with that reputation of bolt on that type of service to their own similar offerings? Nevertheless SOM is an excellent business and I am happy to retain an interest with a particularly significant position in the Tinker. Tuesday 18/07/2017: Amino: AMO: sale of shares by Azina 1 LP who had a considerable holding at 10% and sold a million shares to reduce their holding to 9%. Azina have been gradually reducing their position in AMO over a few months. Is it anything to worry about? Well no, I don’t think so as; have a look at the attached from SharePad:  Wednesday 19/07/2017: Tristel: TSTL: Trading Update:-

For the year ended 30 June 2017 Tristel will record turnover in excess of £20 million (2016: £17.1 million) and pre-tax profit (before share-based payments) of at least £4 million (2016: £3.3 million). Both turnover and pre-tax profit are ahead of market expectations. In the second half, revenue from overseas markets contributed 50% of the Group total compared to 43% in the first half, and for the full year overseas revenue represented 47% of Group revenue - a record level. Tristel has continued to generate significant levels of cash and at 30 June 2017 cash balances were £5.1 million (30 June 2016: £5.7 million). The Company has no debt. My view: I hold a much smaller position in TSTL that my original 70p purchase & various historic top ups but nowadays only maintain a fairly modest position. I think they are a decent company but two things just concern me a little; firstly the high valuation on the shares with lots of expectation built into the share price and secondly these share-based payments which are really “pay” but shuffled to one side and thereby possibly flattering profits. Note, I say possibly as we as yet don’t know the value of these payments but last year they were £0.7m and as I recall not mentioned in the July 2016 TU. This year the share-based payments actually get a specific mention in the TU; does that mean they will be similar or larger than the £0.7m of 2016? I really don’t know but will have to wait until the annual report is released in October to find out. Thursday 20/07/2017: IQE: Trading Statement: Well I do have some history with IQE having held over a period starting in about 2011 and lasting for all of three years until I became overly bored with them. Nevertheless, I have continually kept a watch on IQE with a mixture of mild curiosity thinking that that particular train would maybe never leave the platform let alone the station! However, things started to unfold a touch in December 2016 with a statement to inform the markets “the Group announces that it is on track to deliver FY 2016 revenue and adjusted operating profit ahead of expectations”. This was then followed by more reassuring director speak with the finals in March 2017 with the shares sitting around the 50p mark. Anyway, back to Thursday’s TU: “Strong growth in H1 revenues marks the start of increased VCSEL wafer demand for mass-market consumer applications, and triggers a capacity expansion to meet higher levels of expected demand in H2 2018”. The TU then goes on to say:- “As a result, the Board has now approved a capacity expansion plan to meet higher levels of expected demand for H2 2018 than previously anticipated. This follows increased investment during H1 2017 in operating costs, product development and working capital to help position the Group for the expected ramp and meet higher levels of growth in H2 of 2017”. The CEO then chips in (sorry about the chips!) to say “In light of recent progress and its increasingly confident outlook, the Board expects the Group will now exceed market expectations for the full year and whilst it remains early into the start of the mass-market adoption of our technology, it is possible that with the current contract momentum, a more significant upgrade to current market expectations could be delivered for 2018”. My Action: I will now sit on my hands and possibly add to my current holding if the share dips below 90p. It’s one of those shares that I find difficult to value by my prefered methods so maybe I will be content to rely on the ubiquitous and ridiculously overly respected PE rating which although in the high 20’s will surely fall as brokers up their forecasts. Of course, with any highly rated growth company, a slightly less than sparkling RNS, should that happen, will hit the share price but that’s what comes with investing in the slightly more exciting stuff. Thursday 20/07/2017: Bodycote: BOY: RNS Titled: BODYCOTE LAUNCHES GAME CHANGING Powdermet® TECHNOLOGIES “Additive manufacturing processes that can dramatically reduce production time and cost of 3D printed parts”. My Action: I am tempted to add to the current holding but will wait a week or so before taking a decision. Finally a share that I have mulled over but just could not convince myself to buy into Safestyle UK: SFE. Although the share came through my screens several times in recent years I just did not feel comfortable with the business maybe it was the bias created by those appaling “you buy one you get one free” adverts. Maybe it was down to my view that this was really a householder discretionary purchase for when folk are flush; maybe it was simply my detest of plastic window frames! On Tuesday 18/07/17 SFE issued a profits warning: “As outlined in our AGM statement, we expect to report marginal revenue growth in the first half of 2017, with reduced profits. Given the uncertain market conditions and weaker consumer confidence, we consider it prudent to expect only modest revenue growth again in the second half of the year. This would result in profits for the year being lower than previously anticipated and broadly in line with 2016. Cash flow has continued to be strong and we had net cash of £17.7 million at 30 June 2017 (30 June 2016: £23.6 million), the year on year reduction reflecting the investment in our new production facilities and the payment of a special dividend in July 2016”. My comment: looks a decent business still but even before the profits warning, the share price graph has been rolling over. As I say, I have not held any of these but in my view probably a decent business so maybe worth another look one day if I can get over my prejudices. While we are on the subject of profits warnings, I almost exclusively sell on a profits warning (PW) as soon after 8am as I can on the day of the PW. I did write a blog about my way with profits warnings a couple of years ago; in fact about a year before the excellent piece on PWs by Sharescope who came to the same conclusions as I had. Often it’s about six months for the dust ripples to dissipate after a PW; but straight after a PW is often an unnecessary risk to your capital by taking a position. Well, lets see what next week brings: I see we have interim results for ITV & JE scheduled so let’s see what the week brings. Happy Investing

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed