|

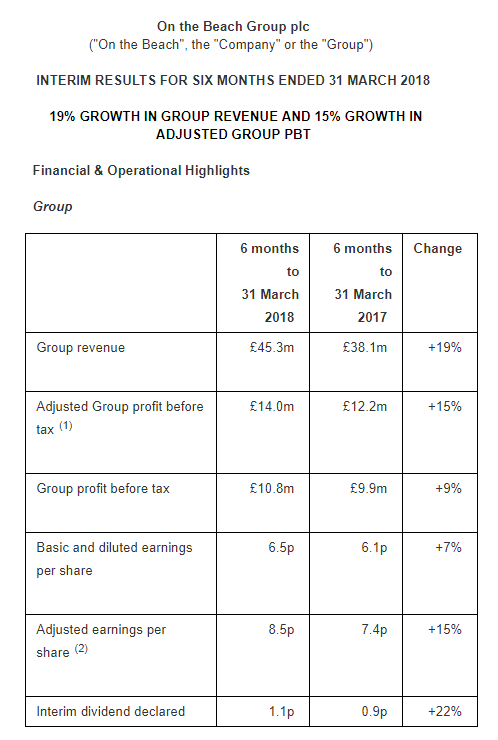

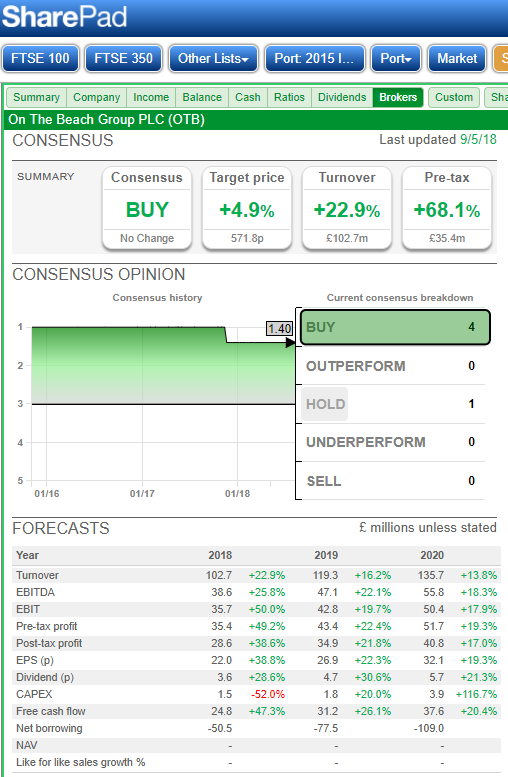

Voyager RNS Log WC 06/05/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. It's becoming increasingly difficult to find attractive companies that meet my cash flow requirements and are on offer at reasonable entry prices. Also, it’s getting a bit thinner on the ground in terms of special situations, those oh so rewarding companies where something may be changing that causes them to move up a gear or two. Is all of this a sign that overly stretched optimism may be priced into the market? There are certainly some very attractive companies on the market but in most cases, you really have to pay high rated prices to purchase them. I suppose if I were to be really brave then I could search much deeper below my £50m market capitalisation threshold but then the problem on the normal market size and thinness of the order book can so easily bite you in the bum particularly if bad news strikes and you decide to make a rush for the exit. On another financial front, I am challenging the council tax banding of my property. In honesty, this is something I should have done 18 years ago when I moved in but as ever, I guess I am just a touch to laidback. It’s a very nice property and I certainly don’t have any complaints on that score as it’s a few hundred years old and certainly has character but why it should be rated so much higher in council tax band terms, I really can't fathom out. Anyway, after first being refused by the powers in charge, I provided sufficient evidence for them to at least initiate a review. If that does not do the trick then I will take it to an appeal tribunal which I am familiar with having conducted one for my Laboratory which yielded over £1m return of overpaid council tax; maybe if I can get upwards of £10k back for overpayment over 18 years then that would be a result. Turning to a review of RNS for stocks within the voyager, last week was a very quiet week and this week seems only a touch more active. One to catch up on from last week is Games Workshop; bizarrely a stock I first identified as a buy some 15 months ago but my prejudice regarding the surreal practice of adults playing war games with toys, just kept me away from the early ride. Strange really, in that I can't stand video games yet went in heavily to KWS but I suppose seeing my two sons keep faith with the pastime these last 25 years gave me a better acceptance if not tolerance. Anyway, the GAW trading update was “ given the high operational gearing of the business, profits for 2017/18 to date are therefore slightly above expectations.”. The market did not react dramatically and I suppose some punters were again looking for “greater than expectations” buy so far, so good. Of course, the operational gearing is something to keep a close eye on at the first sign of change in fashion for the GAW products; probably a fair risk in my opinion. This week’s RNSs for the Voyager: Tuesday 08/05/2018: No RNS significant to the portfolio Wednesday 09/05/2018: No RNS significant to the portfolio Thursday 10/05/2018: ITV Mkt Cap: £6.5b: RNS 1st Qtr Trading Update: Carolyn McCall, ITV Chief Executive, said: "We have started the year well both on and off screen. Total external revenue increased 5%, driven by 11% growth in ITV Studios revenue and 41% growth in online revenue. ITV total advertising which includes NAR, online and sponsorship was up 3%. "Our strong viewing performance has continued, with total minutes viewed across the ITV Family up 4%, share of viewing up 6% and time spent viewing online on the ITV Hub up 31%. This reflects the strength and breadth of our schedule across our platforms. Highlights include strong performances from Coronation Street and Emmerdale, the successful return of Dancing on Ice and both Saturday Night Takeaway and our long-running drama Vera delivering their best series ever. And we have an exciting schedule for the rest of the year including Britain's Got Talent, the Football World Cup, the return of Love Island and our new period drama Vanity Fair, from the producers behind Victoria and Poldark. "ITV Studios has delivered a strong performance with organic revenue up 9%. We have a solid slate of new and returning programmes internationally for both broadcasters and OTT platforms with Unforgotten, The War of the Worlds, Snowpiercer, Good Witch, Suburra, The Voice, The Chase, Big Star's Little Star, Queer Eye for the Straight Guy, The Four and Forged in Fire. "While the economic environment remains uncertain online advertising continues to grow strongly. We expect ITV total advertising to be up 2% over the first half, but profits will reflect the timing of the Football World Cup. Over the full year we are on track to deliver double digit growth in online revenue and good organic revenue growth in ITV Studios. "The strategic refresh is progressing well with great input and engagement from ITV people across the business. I look forward to sharing an update at our interim results in July." My View: encouraging enough words from Carolyn McCall and revenue streams are all just about moving in the right direction. My simplistic view is that ITV has made a decent start with this first quarter and should be on target to meet expectations and I eagerly await their interims in July to see how profits are panning out. I will continue to hold but still just a little underwater with this one; great potential but will Mrs McCall be able to steer the cast of Coronation Street and the appalling Love Island to apparently safer waters to be possibly gobbled up by a predator? Thursday 10/05/2018: On The Beach: OTB:Market cap £710m: Interim Results RNS:   My View: Since the turn of the year, OTB has been a phenomenal performer with the share price possibly getting a touch beyond itself. Again applying my trusty fag packet (incidentally it’s decades since I smoked) I tend to think that they may well have to really stretch to meet the market expectations for the year. It’s just simply that my quick calculation suggests that in the most recent ½ years, that’s discreetly H1 & H2, their turnover has been in £m:

2016: 35.5, 35.8: Ratio H2/H1 = 1.01 2017: 38.1, 45.5: Ratio H2/H1 = 1.19 2018: 45.3, forecast 57.4 : Ratio H2/H1 required to meet expectations = 1.27 Note: the Sunshine Holidays acquisition (The Board believes that the acquisition will be earnings enhancing in the current financial year to 30 September 2017 because of the Group's ability to quickly leverage its modular technology platform) we were told was earnings enhancing from financial year ending September 2017 so you would expect to see a really significant effect in FY 2018 and that will be built into the consensus/expectation for a turnover of £102.7m. From my fag packet, see above, that looks a bit of a stretch to meet turnover expectations. Given the fact rather high valuation of the business, I just think that the lurking chance of a mild profits warning in the October 18 trading update (“at the lower end of expectations”) exposes me to too much downside. Now, without doubt, OTB is a quality business but I now suspect there may be a touch of short-term risk as an investment; it’s simply travelled so far in a short space of time and given the interims, may just be overstretched. It was also bought as a special situation whilst also having some attractive ROCE figures which are in truth a bit flattering/unreal as it is really an asset-light matching service; matching ticket flights from the various airlines with hotels. So as ever, relying on the trusty fag packet calculation, I sold on the morning of the RNS for a very decent profit of well over 60%. I will keep an eye on OTB and maybe buy back in at some time but for now, thanks for the ride. If in doubt, get out and protect your capital. Thursday 10/05/2018: XP Power: XPP: Market cap £668m: Acquisition RNS: Acquisition of Glassman High Voltage Inc. Glassman, based in New Jersey, USA, supplies the industrial and technology sectors with a range of standard, modified and custom high voltage, high power conversion products, which are generally used in applications involved in the ionization and acceleration of particles. Typical applications include semiconductor manufacturing equipment, vacuum/plasma processing, analytical instrumentation, medical diagnostics and test equipment. Glassman has the most comprehensive standard product portfolio in its sector, with the capabilities to also provide customer specific power solutions. In the fiscal year ended 31 December 2017, Glassman recorded sales in the US of US$17.3 million (£12.4 million), profit before tax of $2.9 million (£2.0 million) and had gross assets at the year end of $9.5 million (£6.8 million). The Acquisition also includes the purchase of Glassman’s small European sales business. Total consideration of US$44.5 million (£31.8 million) will be paid in cash on completion which is expected to be effective in May 2018. The Acquisition is on a debt and cash free basis and was funded with a US$45.0 million extension of the Group’s existing revolving credit facility. The Acquisition is expected to be enhancing to XP Power’s earnings in 2018*. My View: well it looks a decent acquisition, not massive relative to the current XPP turnover but overall quite attractive as Glassman made $2.9m PBT on a turnover of $17.3m. XPP are paying $44.5m and that suggests they are getting Glassman for about 15x PBT which in takeover terms, seems decent enough. The earlier acquisition of Comdel was at about 13x PBT & XPP itself trades at around 20x profits. The change in the net debut situation again seems quite manageable and the trusty fag packet suggests that after the acquisition debt won't be a show stopper at 0.7xEBITDA. Also, I reckon that EPS should be enhanced by 3 or 4 % this FY by Glassman. All in all, it looks a decent acquisition and that aligned with the good track record of XPP’s management give me confidence to maybe top up a little on the dips. Friday 09/05/2018: No RNS significant to the portfolio What’s on the horizon next week? Well, not a great deal; at the moment I can only see one of the Voyager stocks with a scheduled RNS; G4M year-end results on 15/05/18 but you never know, so let’s see. As ever, it pays to remember that no matter how diligent you may be, the next profits warning may just be around the corner. On that cheery note, may I wish you a great weekend and as ever, Happy Investing

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed