|

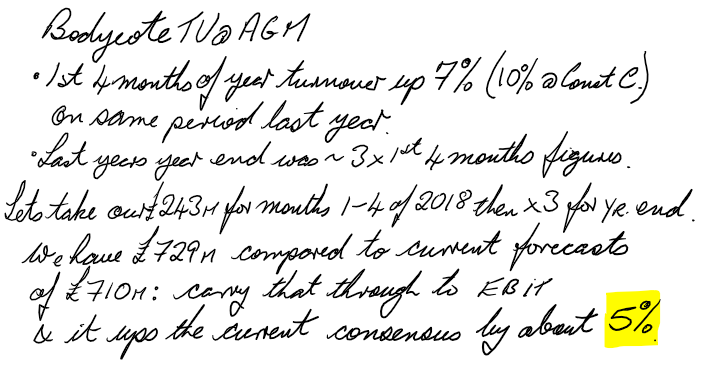

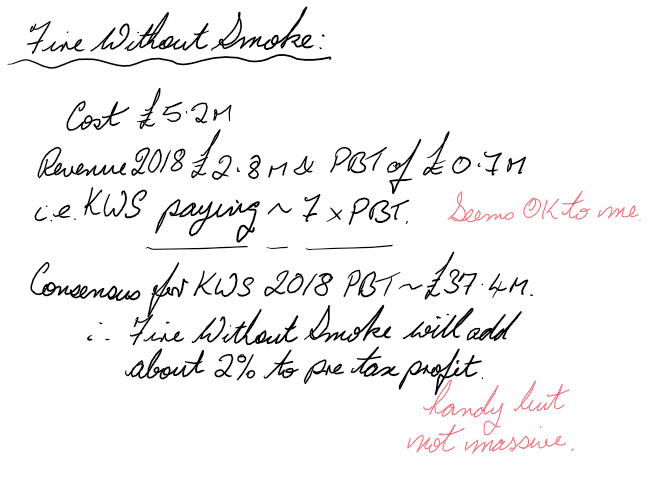

Voyager RNS Log WC 25/05/2018 As ever, although I may get keen about a stock, what I put into print here is purely me sharing my rambling thought process and NOT INVESTMENT ADVICE to either buy or sell a particular stock. The key for the colouring of text within these notes: Text in normal black: just my thoughts. Text in blue italics: direct lifts or copy & paste from the RNS issues by the business. Text in green: loosely, the investment principles that I feel comfortable with. Red is a disclaimer in that what I write is NOT investment advice. Only a short week with the bank holiday and a very quiet one at least to start with as there was very little RNS news on Tuesday apart from the market jitters as Italy and Spain struggle with their economies and the thankless individuals collectively called politicians struggle with a way forward. In truth, I have never been a political animal and feel fairly convinced that I could have found a way to prosper even in the likes of Albania in the 90’s. Anyway. Let’s hope Mr Market does not become overly upset over the next couple of months but if he does, I have a very healthy reserve that may be called on should any anomalies be chucked up for the better quality companies. Conversely, rubbish will be rubbish no matter what the market is doing. Onto this week's log: Monday 28/05/2018: Bank Hol, Markets Closed: Tuesday 29/05/2018: No RNSs relevant to Voyager portfolio. Wednesday 30/05/2018: Telford Homes: TEF: Mkt Cap £346m: Finals RNS:  Total profit before tax in the year to 31 March 2018 increased by nearly 35 per cent to £46.0 million (2017: £34.1 million) [1], ahead of original market expectations. This strong performance was reflected in an improvement in our adjusted gross margin of 4.2 percentage points and a 3.3 percentage point increase in our adjusted operating margin, up to 16.7 per cent (2017: 13.4 per cent). The margin improvements are partly due to the mix of developments that completed during the period but also a combination of other factors, particularly some prudent estimates for build cost inflation that were not realised. I am also delighted that we have been able to declare a final dividend of 9.0 pence per share, making a total of 17.0 pence per share for the year, an increase of 8.3 per cent compared with the previous year (2017: 15.7 pence). We expect to continue to pay at least one third of our annual earnings to shareholders in dividends. Outlook Telford Homes has delivered significant profit growth over the last three years with total profit before tax increasing from just over £25 million in 2015 to £46 million in 2018. Furthermore, we are well placed to achieve our stated goal of exceeding £50 million of total pre-tax profit for the year to 31 March 2019 which will represent a 100 percent increase over four years. Having arrived at this point in a short period of time the challenge now is to establish the business consistently delivering over £50 million of profit every year and furthermore to generate and sustain the next significant growth period. Without the advent of build to rent we would not have been able to achieve consistency of profits and would instead have fluctuated around an overall upward trend. Our industry is very capital intensive and the business would have required sustained injections of new capital just to maintain the profit levels achieved in the last few years on an ongoing basis. However our increasing success in the build to rent sector means we expect to consistently deliver profit in excess of £50 million over the next three years predicated on a certain level of new build to rent business. We also expect to set a platform for delivering the next significant phase of profit growth in the medium to longer term. The level of build to rent business we are able to secure will be crucial to achieving our ambitions and to outperforming them if the opportunity arises. The strength of our position and our ability to capitalise on the exciting possibilities ahead are a result of the hard work and dedication of the whole Telford Homes team. I am exceptionally proud of the customer recommendation and employee satisfaction scores we achieved last year and I am confident there is a relationship between them. I look forward to us building on the solid foundation we have created for Telford Homes both in the year ahead and beyond. My View: another very sound set of results from TEF which as I have said before, is my favourite stock in this sector as it’s simply geographically concentrated in the right place, London where there is a massive shortage of reasonably priced housing & the rental investment is flourishing; a large part of TEF work is in the buy to rent segment where they carry out the entire process to completion before handing over to large investor landlords. I just can’t really see that need, which makes this stock low risk, ever really going away. I see TEF as a very well managed business that manages expectations and simply delivers almost constantly at the top end of those expectations or even above them. For fellow TEF investors, here is a link to a video where Jon Di-Stefano, TEF CEO, and his FD talk through the results: Video: www.brrmedia.co.uk/broadcasts/5b06e7139e3d657120be37ee/telford-homes-full-year-results I view TEF as a very long-term hold and that I am happy to continue to treasure within the portfolio and likely add further on any share price weakness in the following months. Yes, it is an incredibly boring stock & not one for the “get rich quick mob” but I can’t help but like boring predictable stocks. Wednesday 30/05/2018: Bodycote: BOY: Mkt Cap £1770m: AGM Trading Update RNS: Trading Update Current trading Group revenue for the four months ended 30 April 2018 was £243m, 7% higher than the same period last year and 10% higher at constant currency. On a divisional basis, ADE revenues were up 5% to £94m (up 10% at constant currency), while AGI revenues were up 9% to £149m (up 10% at constant currency). Within the overall Group result, Specialist Technologies' revenues grew 12% at constant currency. The following review of the Group's markets quotes all movements based on growth against the same period in 2017, at constant currency. Car and light truck revenues grew 8%, with continued strong growth in Emerging Markets and good growth in Western Europe, while North American revenues were down slightly. Civil aerospace revenues grew 4%, held back by restrained demand in France stemming from capacity shortfalls in the aerospace industry supply chains. Overall growth of energy revenues was 24%, with continued strong growth in onshore North American revenues, as well as early indications of an upturn in Western Europe oil & gas revenues. Large frame industrial gas turbine (IGT) revenues were down in North America in line with the cut backs in IGT production announced by the OEMs at the end of 2017. In Western Europe, the IGT declines were more than offset by the increase in business from the new Long Term Agreement with Doncasters. General industrial revenues were 11% higher with good growth across all geographies. Margins have continued to improve although the profit drop-through from incremental sales has been partially offset by increased investment in business development. Financial position Net cash as at 30 April 2018 was £45m compared to £40m at 31 December 2017, reflecting continued strong underlying cash generation in light of the typical working capital outflows in the first few months of the year. The Board will pay a final dividend of 12.1p per share and the special dividend of 25.0p per share on 1 June 2018, at a total cost of £71m. Summary and Outlook We have seen robust growth in the first four months of the year in spite of the foreign currency headwind. At this early stage, and notwithstanding the Group's limited visibility, the Board now expects full year revenue to be higher than previously expected and headline operating profit to be slightly ahead of current analysts' consensus. My View: it seems to me that revenues are up some way more than forecasts & the fag packet looks quite encouraging:  All in all, quite an upbeat trading update from one of my top 10 holdings: it will never be the most exciting company but to my mind, a portfolio loaded with such steady well-managed companies would not be a bad portfolio. Wednesday 30/05/2018: Keywords Studios: KWS: Mkt Cap £1080m: Acquisition of Fire Without Smoke RNS: Strengthening the Group's Art Services Line Keywords Studios, the international technical services provider to the global video games industry, today announces that it has acquired Fire Without Smoke Ltd ("Fire Without Smoke") for a total consideration of up to £5.2m from the founders Will O'Connor, Michael David Thomson and others (the "Sellers"). Headquartered in London and with a studio in Montreal, Fire Without Smoke provides a full suite of creative and marketing services to game publishers and developers, creating assets such as game trailers, marketing art and materials for esports events, and providing marketing consultancy and general design services to the video game industry. Founded in 2013 and now with [40] staff between London and Montréal, Fire Without Smoke works with major game publishers such as Sony, Square Enix, Riot Games, Deep Silver, Sega, Capcom and Ubisoft. For the year ending 31 May 2018, Fire Without Smoke is expected to have revenues of £2.8m and adjusted profits before tax of £0.7m. Under the terms of the acquisition Keywords is paying a consideration comprised of £3.85m in cash, £0.5m of which is deferred until the first anniversary of acquisition and subject to certain performance targets, and the issue of 77,006 new ordinary shares in Keywords, which will be issued to the Sellers on the first anniversary of the acquisition and will then be subject to orderly market provisions for a further 12 months. My View: yet another deal by KWS as it builds its global offering: a quick fag packet calculation:  From what I can gather, two brokers have today have raised their price target for KWS to £21. I don’t place much faith in brokers price targets but anyway, that implies about a 20% upside from where we stand now. The Outlook statement that accompanied the finals on the 09/04/18 was very positive yet the shares may well drift a touch ahead of the next trading update which I expect to see around the end of July/beginning of August. Overall, I am happy to continue to hold this rather exciting company but as ever, the managing of all of these acquisitions does worry me a tad.

Thursday 31/05/2018: Air Partner: AIR: Mkt Cap £52m: RNS Finals for 2017: Temporary suspension of share trading Further to the Company's announcements of 11 April and 25 May 2018, the Board of Air Partner has agreed with Deloitte LLP, the Company's auditor, that the Company will not be in a position to publish its annual audited accounts for the year ended 31 January 2018 by close of business on 31 May 2018. The Company is working together with Deloitte LLP to finalise the audit and expects the audited accounts will be published no later than Monday 11 June 2018. Accordingly, the Board has requested that trading in the Company's ordinary shares on the London Stock Exchange be suspended with immediate effect pending publication of the audited accounts, following which the Company will request the suspension be lifted. This unforeseen delay is a result of the volume of work required to complete the accounting review and its impact on the financial year audit and the prior year restatements. It is in no way related to the Company's current trading, cash flow, banking arrangements or any underlying issue. Peter Saunders, Non-Executive Chairman of Air Partner, said: "The delay to the publication of our full year accounts, and the resultant trading suspension, is extremely frustrating and hugely disappointing for all connected with Air Partner. However, it is a reflection of the volume of work, which began 7 weeks ago, to conclude a transparent, thorough, and exhaustive internal review and audit. This delay is not related to the Company's current trading, cash flow, banking arrangements or any underlying issue. We thank our shareholders for their continued patience and support." My View: I did up until early April this year have a fairly chunky holding in AIR and they were very considerably up on my original investment that is until that RNS about their “accounting oversight”. On the first sniff of doubt i.e. that early April RNS, I immediately sold. In truth, it was a still a very profitable investment and as the share price continued to head downwards, my sale turned out to be a wise move. An RNS “things are not so bad” was released a couple of weeks later and I reentered at a new but very small starter position using a portion of my profits from the earlier holding; in fact the smallest position by some way in the portfolio. The reason I bought this fresh starter position was that I felt there was a real possibility that the accounts issue was historic in nature and a release of the promised results would once again confirm confidence in the business with the promise that things were under control. We then have two RNS’s the most recent one being 25th May (only 5 days ago) confirming that the year-end results would be issued on 31st May. So, after my swim, I got onto my iPhone & SharePad to have a quick look at the results but nothing there @ 7:15 but nothing; ok, I will ditch what I have as soon as the market opens, I decided. Whoops, hardly finished towelling myself dry when we have an RNS from AIR telling us that the shares are temporarily suspended but hey, everything is fine as “delay is not related to the Company's current trading or cash flow etc”. Now, it may well be that the delay is simply getting sustainable security and closure of the accounting issue or alternatively the audit may have found a few more unfortunate accounting issues when they lifted a few carpets around the place. Either way, I feel the company has really lost some trust and credibility which they may possibly have avoided had they more astutely funded the audit into the “anomaly”. Once they return from suspension I will likely sell the few I own. Friday 01/06/2018: No RNSs relevant to Voyager portfolio. Can’t help myself: A New Purchase: An addition to the portfolio: Purchase of Softcat: SCT: a FTSE 250 stock of £1.3b Mkt Cap. Bought at 724p. Briefly what I like about Softcat:

Softcat plc ("Softcat", or the "Company"), a leading UK provider of IT infrastructure products and services, today releases a trading update for the quarter ended 30 April 2018 ("the Period"). The Company has continued to trade well across all segments during the Period, maintaining momentum from the first half and reflecting further successful execution of its strategy. Market conditions and customer demand have both remained strong. Outlook The Board is confident that the Company will deliver full year results that are ahead of expectations. Glad I Am Not There ( GINT): I should say these are not “clever dick” notes just simply an attempt to help investors learn from their mistakes and let's face it, we all make mistakes and I am probably a graduate of the University of errors: the crucial point is what we learn from those mistakes. Photo-me International: PHTM: For investors, a very disappointing update and as PHTM say, Japan hasn't performed as expected. The outlook says “below current market expectations”. The stock was really bashed by the market falling about 25% and then fell again on the following day. Simply horrible things profits warnings but to my mind, every investor should have a plan of how they deal with them and that’s most certainly not burying your head in the sand. PHTM simply just one of those stocks that never really hit the spot for me i.e. I just never got what PHTM was about with its mix of photo booths and laundrettes seemed to be in something of a 1990’s time warp. I just was never overly impressed by the management sales pitch or presentations to investors. Whilst I agree they have no net debt and indeed have cash on the books, that very generous dividend of 7.7% has not been covered by FCF since 2014 and whilst they intend to pay that dividend this year, it looks to be in for a cut in the future. Note: the conventional dividend cover of eps/dps suggests all is well but looking at the free cash flow suggests otherwise and has done for a few years. Thankfully due to my overall feel for the stock and the quality of the cover, it just never tempted me to buy. Whats On the horizon next week: I can’t see much pencilled in for next week but expect to hear a trading update accompanying the Somero AGM and suspect a trading update will come from Amino (AMO) & Dart (DTG). Have a good weekend & as ever, happy investing; catch you all next week.

0 Comments

Leave a Reply. |

Archives

October 2019

Categories |

RSS Feed

RSS Feed